08 May 2020

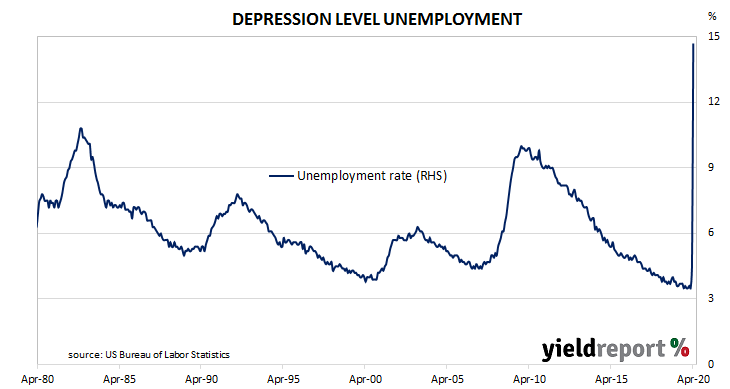

The US economy ceased producing jobs in net terms as infection controls began to be implemented in March. The unemployment rate had been around 3.5% but that changed in March 2020 when job losses began to surge and the rate increased by almost a full percentage point. The latest employment report indicates the full force of restrictions on the US economy has now been felt.

According to the US Bureau of Labor Statistics, the US economy lost a staggering 20.5 million jobs in the non-farm sector in April. The drop in employment was largely in line with the median expectation. Employment figures for February and March were revised down by a total of 214,000.

April’s unemployment rate increased in a ballistic fashion from March’s rate of 4.4% to 14.7%. The total number of unemployed expanded by 15.938 million to 23.078 million while the total number of people who are either employed or looking for work decreased by 6.431 million to 156.481 million. The fall in the number of people in the labour force significantly lowered the participation rate from 62.7% to 60.5%.

ANZ economist Hayden Dimes said, “The US labour market is very flexible, for good and ill, shedding and adding jobs at a bewildering pace.” US Treasury yields increased moderately on the day. By the close of business, US Treasury 2-year bond yields had gained 2bps to 0.15%, the 10-year yield had increased by 5bps to 0.69% while the 30-year yield finished 4bps higher at 1.38%.

US Treasury yields increased moderately on the day. By the close of business, US Treasury 2-year bond yields had gained 2bps to 0.15%, the 10-year yield had increased by 5bps to 0.69% while the 30-year yield finished 4bps higher at 1.38%.

ANZ’s Dimes noted “a decade’s worth of job-creation” had been lost and “May is likely to see more job losses regardless of the path of the pandemic.”

One figure which is indicative of the “spare capacity” of the US employment market is the employment-to-population ratio. This ratio is simply the number of people in work divided by the total US population. It hit a low in October 2010 at 58.2% before slowly recovering to just above 61% in late-2019. April’s reading fell from 60.0% to 51.3%, its lowest reading in the period from 1948 to the present.

06 May 2020

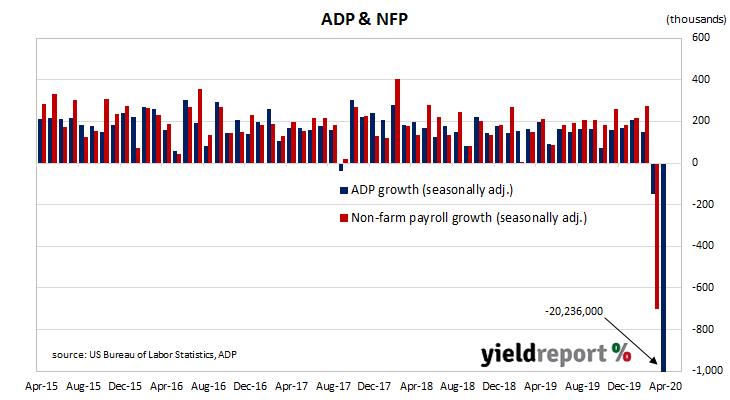

Summary: Private sector employment crushed in April; official payroll report to tank at end of week; employment numbers trashed across firms of all sizes; services sector accounts for 80% of losses.

The ADP National Employment Report is a monthly report which provides an estimate of US non-farm employment in the private sector. Since the report began to be published in 2006, its employment figures have exhibited a high correlation with official non-farm payroll figures, although a large difference can arise in any individual month. Unlike the March report, this latest report includes a month in which the full effects of US infection controls have been felt.

April’s report indicated private sector employment fell by 20,236,070. The fall was largely in line with the 20 million drop which had been expected.

“Non-farm payrolls on Friday are expected to show job losses of 21.3 million with unemployment expected to have risen to 16% from 4.4% in March,” said ANZ economist John Bromhead.

US Treasury yields rose across the curve, possibly implying the disastrous numbers had already been factored in. However, news of the US Treasury’s intentions to issue more long-term bonds also sent yields higher. By the end of the day, the 2-year Treasury bond yield had inched up 1bp to 0.18%, the 10-year yield had gained 4bps to 0.70% while the 30-year yield finished 7bps higher at 1.40%.

Employment numbers were trashed across the board, regardless of size. Firms with less than 50 employees lost a net 6.005 million positions, mid-sized firms (50-499 employees) shed 5.269 million positions and large businesses (500 or more employees) accounted for 8.963 million fewer positions.

06 May 2020

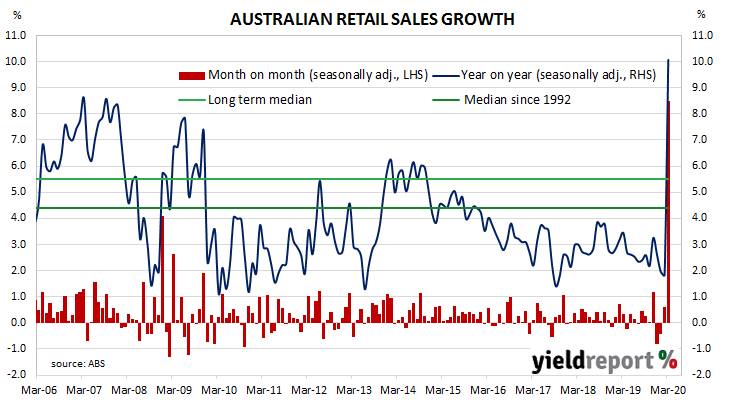

Summary: Retail sales jump in March; food stockpiling and price rises behind the increase.

Growth figures for domestic retail sales have been declining since 2014 and they reached a low-point in September 2017 when they registered an annual growth rate of just 1.5%. They then began increasing for about a year, only to stabilise at around 3.0% to 3.5% through late 2018 before trending lower through 2019 and early 2020. March’s figures bucked the trend.

According to the latest ABS figures, total retail sales jumped by 8.5% in March on a seasonally-adjusted basis. The gain was larger than the 8.2% increase which had been expected after “flash” figures were released on 22 April and it was a leap from February’s +0.6%. On an annual basis, retail sales increased by 10.1%, as compared to February’s comparable figure of 1.8%.

Westpac senior economist Matthew Hassan said the spike was “due to prices rather than volumes.”

The report came out on the same day as the March home loan data and Commonwealth bond yields moved higher, largely in line with US Treasury movements. By the end of the day, the 3-year ACGB yield had ticked up 1bp to 0.25% while 10-year and 20-year yields had each gained 5bps to 0.91% and 1.53% respectively.

In the cash futures market, expectations of a rate cut softened a little. By the end of the day, June contracts implied a rate cut down to zero as a 51% chance, down from the previous day’s 54%. July contracts implied a 65% chance of such a move in that month, down from 67%. Contract prices of months in the remainder of 2020 and through to mid-2021 implied similar probabilities, ranging between 43% and 60%.

Other economists were quick to point out the price-driven nature of the increase. “Grocery stockpiling somewhat offset the negative spending effects of COVID-19 lockdown constraints, but [it] wasn’t enough to create a spike in total retail volumes,” said ANZ economist Adelaide Timbrell. Westpac’s Hassan said retail volumes over the March quarter “rose just 0.7%, well below expectations of a 1.8% gain.”

06 May 2020

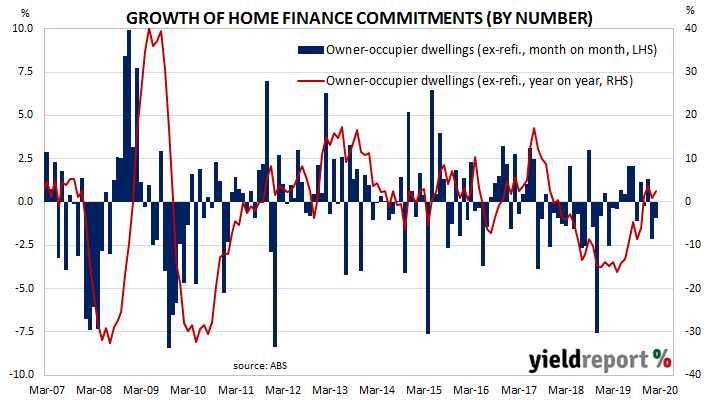

Summary: Home loan approvals fall in number but increase in value over March; owner-occupier loans rise; investor loans decline.

A very clear downtrend was evident in the monthly figures of both the number and value of home loan commitments through late-2017 to mid-2019. Then the RBA reduced its cash rate target in a series of cuts and both the number and value of mortgage approvals began to noticeably increase. Figures from February provided an indication the trend may have finished but the latest figures still do not provide some sort of confirmation.

March’s housing finance figures have been released and the total number of loan commitments (excluding refinancing loans) to owner-occupiers fell by 0.9%, a slower contraction rate than February’s revised figure of -2.1%. However, on an annual basis, the growth rate increased from February’s revised figure of 0.9% to 2.5%.

Westpac senior economist Matthew Hassan said, “This is a throwback to pre-coronavirus [times], reflecting the strength of conditions earlier in the year.” The report came out on the same day as March retail sales figures and Commonwealth bond yields moved higher, largely in line with US Treasury movements. By the end of the day, the 3-year ACGB yield had ticked up 1bp to 0.25% while 10-year and 20-year yields had each gained 5bps to 0.91% and 1.53% respectively.

The report came out on the same day as March retail sales figures and Commonwealth bond yields moved higher, largely in line with US Treasury movements. By the end of the day, the 3-year ACGB yield had ticked up 1bp to 0.25% while 10-year and 20-year yields had each gained 5bps to 0.91% and 1.53% respectively.

In the cash futures market, expectations of a rate cut softened a little. By the end of the day, June contracts implied a rate cut down to zero as a 51% chance, down from the previous day’s 54%. July contracts implied a 65% chance of such a move in that month, down from 67%. Contract prices of months in the remainder of 2020 and through to mid-2021 implied similar probabilities, ranging between 43% and 60%.

05 May 2020

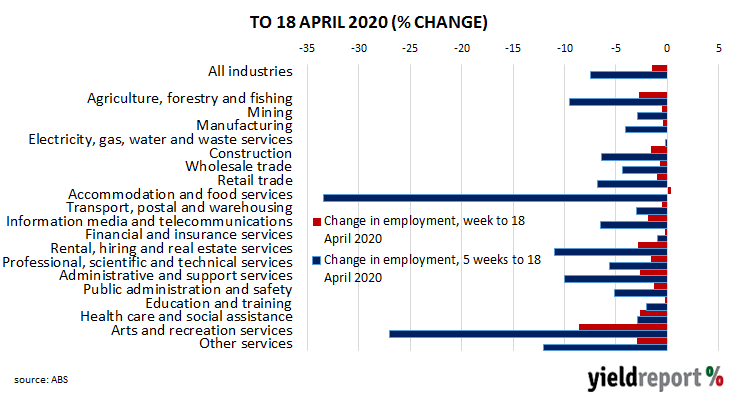

Summary: Job losses continue to mount through April; some people hold multiple jobs; unemployment rate will rise but not by as much as figures suggest.

The ABS has released its second payroll report containing new statistics on jobs and wages based on Single Touch Payroll data provided by the ATO. Job losses do not directly translate into additional unemployment; some people hold more than one job and the report’s figures are not seasonally adjusted.

Between the week ending 14 March 2020 and the week ending 18 April 2000, the total number of work positions in Australia contracted by 7.5%. Total wages fell by 8.2% over the same five-week period.

The rate of weekly job losses slowed when compared with losses in the week ending 4 April. Total jobs fell by 1.5%, a substantial “improvement” when compared with the 5.5% fall in the week ending 4 April. The arts/entertainment sector continued to suffer heavily.

ANZ senior economist Catherine Birch said the numbers “show a decline in the number of jobs rather than the number of workers, and more than 15% of employed workers are estimated to hold multiple jobs.” She noted other differences between the payroll report and Labour Force statistics which would mean the expected rise in unemployment “will likely be smaller than the payroll figures suggest.”

The figures came out on the same day as the RBA Board meeting and domestic Treasury bond yields moved a little higher, largely following US Treasury bond movements overnight. By the end of the day, 90-day bank bills and the 3-year ACGB yield were both unchanged at 0.10% and 0.24% respectively while the 10-year yield finished 3bps higher at 0.86% and the 20-year yield finished 2bps higher at 1.48%.

04 May 2020

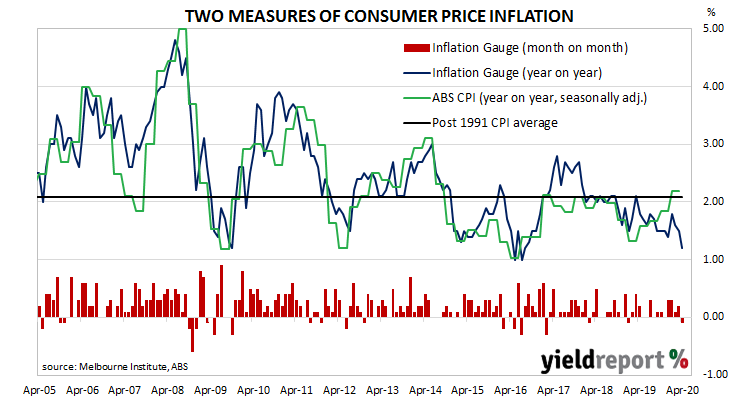

The RBA’s stated objective is to achieve an inflation rate of between 2% and 3%, “on average, over time.” Since the GFC, Australia’s inflation rate has been trending lower and lower and it has been below the RBA’s target band for some years now. Despite the RBA’s desire for a higher inflation rate, attempts to accelerate inflation through record-low interest rates have failed to date.

The Melbourne Institute’s latest Inflation Gauge index decreased by 0.1% through April. The small decline follows a 0.2% increase in March and a 0.1% increase in February. On an annual basis, the index increased by 1.5%, down from March’s comparable rate of 1.6%.

The index came out on the same day as ANZ’s Job Ads report and March’s dwelling approval numbers. Commonwealth bond yields moved lower, although they finished largely in line with US Treasury movements. By the end of the day, the 3-year ACGB yield had slipped 1bp to 0.24%, the 10-year yield had lost 3bps to 0.83% while the 20-year yield finished 4bps lower at 1.46%.

In the cash futures market, expectations of a rate cut softened a touch. By the end of the day, May contracts implied a rate cut down to zero as a 60% chance, down from the previous day’s 62%. June contracts implied a 56% chance of such a move in that month, down from 58%. Contract prices of months in the remainder of 2020 and through to mid-2021 implied similar probabilities, ranging between 45% and 65%.

04 May 2020

Summary: Home approval numbers fall; better than expected; home construction still to slow.

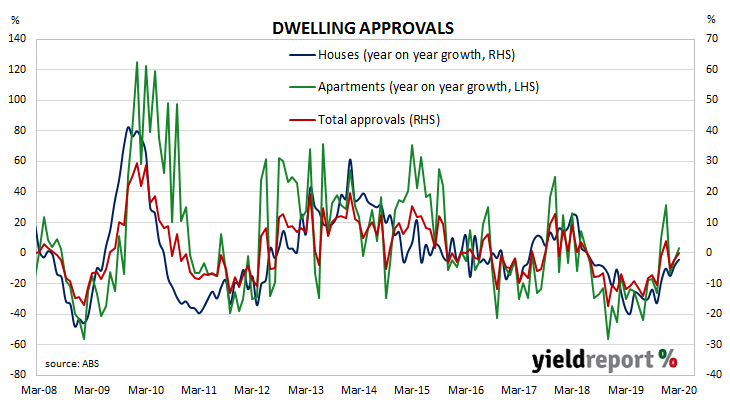

Approvals for dwellings, that is apartments and houses, had been heading south since mid-2018. As an indicator of investor confidence, falling approvals had presented a worrying signal, not just for the building sector but for the overall economy. However, approval figures from late-2019 and early-2020 represented the possibility of a recovery in 2020. Some economists are not convinced.

The Australian Bureau of Statistics has released the latest figures from March and total residential approvals decreased by 4.0% on a seasonally-adjusted basis. The fall over the month was not as bad as the -15% which had been expected but it was still a considerable turnaround from February’s revised figure of +19.4%. Total approvals still increased by 0.2% on an annual basis, an improvement from February’s comparable figure of -4.6% after it was revised up from -5.8%.

ANZ economist Adelaide Timbrell said, “It’s too early to see the impacts of COVID-19 in the building approvals data, since there is a lag between applications and approvals.” Westpac senior economist Matthew Hassan said the fall was “much milder than the expected unwind from a 20% jump the month before.” The figures came out on the same day as the Melbourne Institute’s April Inflation Gauge index and ANZ’s April Job Ads report. Commonwealth bond yields moved lower, although they finished largely in line with US Treasury movements. By the end of the day, the 3-year ACGB yield had slipped 1bp to 0.24%, the 10-year yield had lost 3bps to 0.83% while the 20-year yield finished 4bps lower at 1.46%.

The figures came out on the same day as the Melbourne Institute’s April Inflation Gauge index and ANZ’s April Job Ads report. Commonwealth bond yields moved lower, although they finished largely in line with US Treasury movements. By the end of the day, the 3-year ACGB yield had slipped 1bp to 0.24%, the 10-year yield had lost 3bps to 0.83% while the 20-year yield finished 4bps lower at 1.46%.

In the cash futures market, expectations of a rate cut softened a touch. By the end of the day, May contracts implied a rate cut down to zero as a 60% chance, down from the previous day’s 62%. June contracts implied a 56% chance of such a move in that month, down from 58%. Contract prices of months in the remainder of 2020 and through to mid-2021 implied similar probabilities, ranging between 45% and 65%.

04 May 2020

Summary: ANZ’s job ads index dives in April; five times worse than previous record fall; a bad sign for employment in coming months.

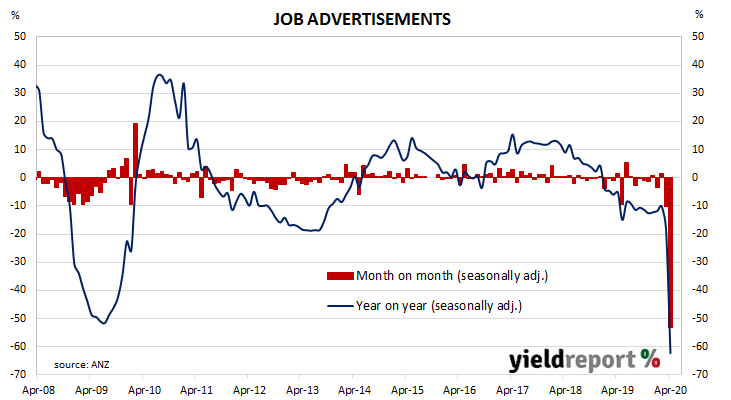

From mid-2017 onwards, year-on-year growth rates in the total number of Australian job advertisements consistently exceeded 10%. That was until mid-2018 when the annual growth rate fell back markedly. 2019 was notable for its reduced employment advertising, along with a reversal of the gains in 2017 and 2018. Figures from the first quarter of 2020 were already troubling before Australian labour demand stepped over March’s cliff edge.

According to the latest ANZ figures, total advertisements plunged by 53.1% in April on a seasonally-adjusted basis. The staggering drop followed a 10% fall in March and a 1.5% rise in February after revisions. On a 12-month basis, total job advertisements were 62.2% lower than in April of last year, representing a massive drop from March’s comparable figure of -18.3%.

ANZ senior economist Catherine Birch said the drop “was almost five times the previous record monthly fall of 11.3% in January 2009, which was during the GFC.” The figures came out on the same day as the Melbourne Institute’s April Inflation Gauge index and March’s dwelling approval numbers. Commonwealth bond yields moved lower, although they finished largely in line with US Treasury movements. By the end of the day, the 3-year ACGB yield had slipped 1bp to 0.24%, the 10-year yield had lost 3bps to 0.83% while the 20-year yield finished 4bps lower at 1.46%.

The figures came out on the same day as the Melbourne Institute’s April Inflation Gauge index and March’s dwelling approval numbers. Commonwealth bond yields moved lower, although they finished largely in line with US Treasury movements. By the end of the day, the 3-year ACGB yield had slipped 1bp to 0.24%, the 10-year yield had lost 3bps to 0.83% while the 20-year yield finished 4bps lower at 1.46%.

In the cash futures market, expectations of a rate cut softened a touch. By the end of the day, May contracts implied a rate cut down to zero as a 60% chance, down from the previous day’s 62%. June contracts implied a 56% chance of such a move in that month, down from 58%. Contract prices of months in the remainder of 2020 and through to mid-2021 implied similar probabilities, ranging between 45% and 65%.

01 May 2020

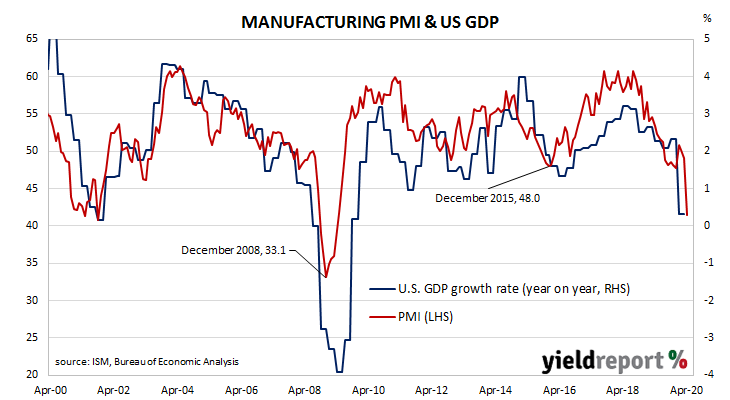

US purchasing managers’ indices (PMIs) have been sliding since August 2018, albeit from elevated levels. After reaching a cyclical peak in September 2017, manufacturing PMI readings went sideways for a year before they started a downtrend. Readings stabilised in late 2019 after a truce of sorts was made with the Chinese regarding trade. However, the March 2020 report implied US manufacturing activity had begun contracting and the latest reading has all but confirmed it.

According to the latest Institute of Supply Management (ISM) survey, its Purchasing Managers Index recorded a reading of 41.5 in April, higher than the expected figure of 37.5 but much, much lower than March’s final reading of 49.1. The average reading since 1948 is 52.8 and any reading below 50 implies a contraction.

The ISM’s Tim Fiore said, “The coronavirus pandemic and global energy market weakness continue to impact all manufacturing sectors for the second straight month. Among the six big industry sectors, Food, Beverage and Tobacco Products remains the strongest. Transportation Equipment and Fabricated Metal Products are the weakest of the big six sectors.” US Treasury yields fell at the long end of the curve. By the end of the day, the 2-year Treasury bond yield had crept up 1bp to 0.20% while the 10-year yield had gained 2bps to 0.62% and the 30-year yield finished 4bps higher at 1.25%.

US Treasury yields fell at the long end of the curve. By the end of the day, the 2-year Treasury bond yield had crept up 1bp to 0.20% while the 10-year yield had gained 2bps to 0.62% and the 30-year yield finished 4bps higher at 1.25%.

NAB head of FX Strategy within its FICC division Ray Attrill said the index had been “once again held up by the rise in supplier delivery times, a function of the lockdowns and disrupted supply chains [and] not excess demand…” He also noted a fall of the new orders sub-index below the GFC-era record low, as well as falls in other sub-indices to record or near-record lows.

30 April 2020

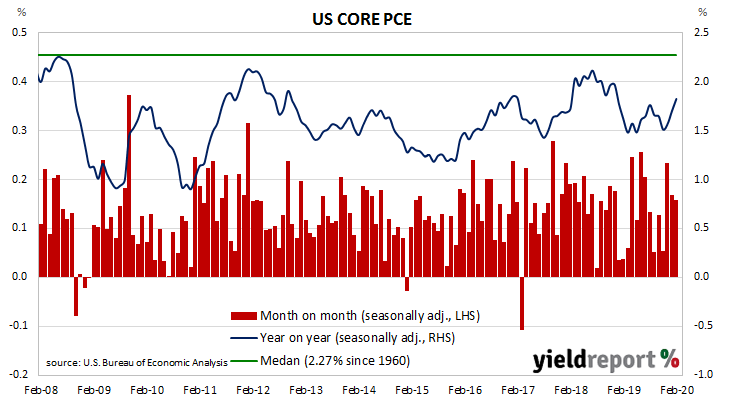

One of the US Fed’s favoured measures of inflation is the change in the core personal consumption expenditures (PCE) price index. After hitting the Fed’s target at 2.0% in mid-2018, the annual rate then hovered in a range between 1.8% and 2.0% through to the end of 2018 before dropping in the first quarter of 2019 to around 1.5%. It has ranged between 1.5% and 1.8% since then.

The latest figures have now been published by the Bureau of Economic Analysis as part of the March personal income and expenditures report. Core PCE prices decreased by 0.1% for the month, in line with a -0.1% which had been expected but lower than February’s 0.2% increase. On a 12-month basis, the core PCE inflation rate ticked down from February’s figure of 1.8% to 1.7%.

ANZ economist Kishti Sen said, “As demand collapses…there will be more deflation to come in the months ahead.”

US Treasury yields finished higher at the long end despite “risk-off” moves by investors away from equity markets. By the end of the day, the 2-year Treasury yield had slipped 1bp to 0.19% while the 10-year yield had inched up 1bp to 0.64% and the 30-year yield had increased by 3bps to 1.28%.

In terms of US Fed policy, a rate change of any sort remained unlikely given the federal funds rate has been at the effective lower bound since the US Fed reduced it on Sunday 15 March. However, contract prices out to March 2021 imply traders think there is a small chance of a 25bps increase in the federal funds rate beginning in December.