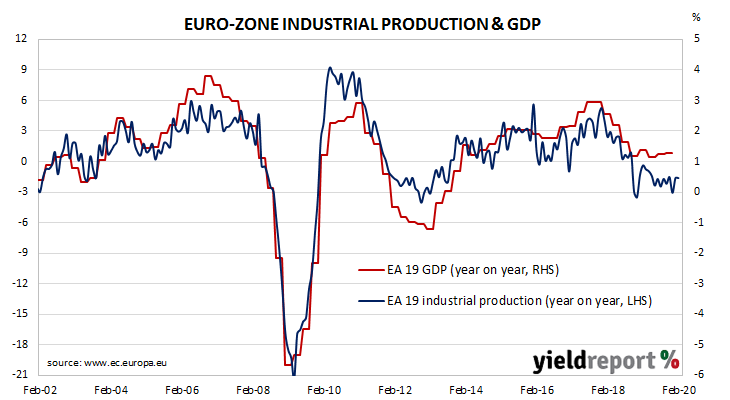

As with other countries’ measures of industrial production, Eurostat’s industrial production index measures the output and activity of industrial sectors in euro-zone countries in aggregate. Following a recession in 2009/2010 and the debt-crisis of 2010-2012 which flowed from it, euro-zone industrial production recovered and then reached a peak four years later in early-2016. Growth rates then fell and recovered through 2016/2017 before beginning a steady and persistent slowdown.

According to the latest figures released by Eurostat, euro-zone industrial production declined by a seasonally-adjusted 0.1% in February, lower than the flat result which had been expected and a significant turnaround from January’s +2.3%. On an annual basis, seasonally-adjusted growth in industrial production remained at January’s revised rate of -1.6%*.

Industrial production increased in the two largest economies of the euro-zone. Germany’s industrial production increased by 0.5% while France’s comparable rate was +0.9%. However, other large economies in the euro-zone, such as Spain and Italy, experienced contractions. Spain’s industrial production shrank by 0.3% and Italy’s shrank by 0.5%.