23 March 2020

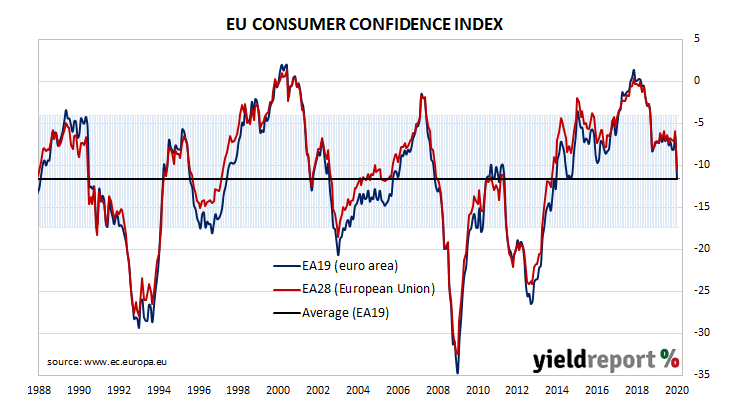

EU consumer confidence plunged during the GFC and again in 2011/12 during the European debt crisis. Since early 2014, it has been at average or above-average levels, rising to a cyclical peak at the beginning of 2018. Even after it dropped back significantly in late 2018, the index remained at a level which corresponds to significant optimism among households. However, the latest reading indicates a significant change has taken place.

The March survey conducted by the European Commission indicated household confidence deteriorated noticeably, albeit from elevated levels. The latest published reading of its Consumer Confidence index recorded a figure of -11.6, above the -14 which had been expected but considerably lower than February’s final figure of -6.6. The average reading since the beginning of 1985 has been -11.6.

The report came out on the same day as the US Fed announced additional measures to support various sectors of the US economy, including the re-establishment of facilities which buy securities backed by consumer and student debt. By the end of the day, yields on German 10 year bunds had lost 6bps to -0.38% while French 10-year OATs had crept up 1bp to 0.11%.

19 March 2020

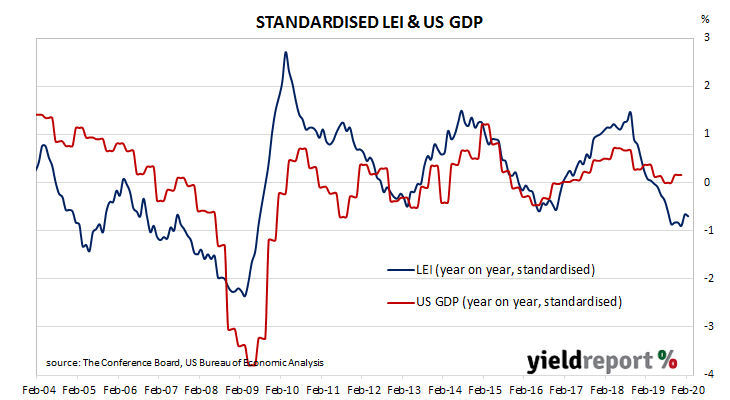

The Conference Board Leading Economic Index (LEI) is a composite index which is composed of ten indices which are thought to be sensitive to changes in the US economy. The Conference Board describes it as an index which attempts to signal peaks and troughs, as turning points in the index have historically occurred prior to changes in aggregate economic activity. While the first two months of 2020 appeared to have represented a break from the downtrend of the second half of 2019, recent events have made the most recent figures obsolete.

The Leading Economic Index increased by just 0.1% during February, in line with expectations but quite a large decline from January’s +0.7% after revisions. On an annual basis, the LEI slowed from January’s revised growth rate of 0.9% to 0.8% in February.

The Conference Board’s Senior Director of Economic Research, Ataman Ozyildirim, said the latest reading “doesn’t reflect the impact of the COVID-19 pandemic which began to hit the US economy in full by early March.” He said “the economy may already be entering into a period of contraction.”

Changes over time can be large but once they are standardised, a clearer relationship with GDP emerges. The latest reading implies a year-on-year growth rate of 1.5% at the beginning of the September 2020 quarter.

19 March 2020

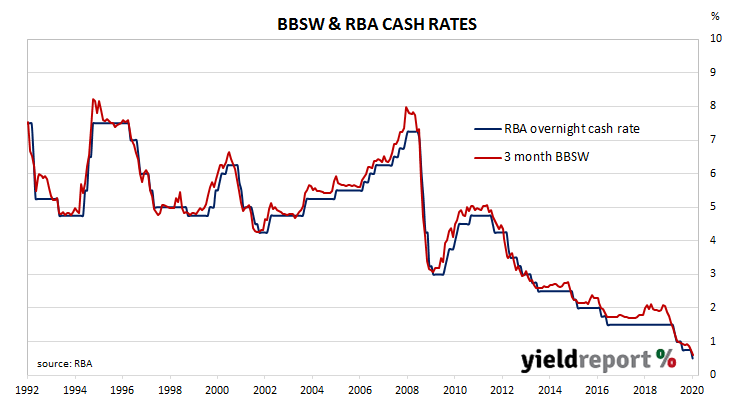

Central banks began unconventional policies in 2001 when the Bank of Japan began buying government bonds. After the GFC, the US Federal Reserve, the European Central Bank and the Bank of England joined in after slashing their official rates down to zero or below. Now the RBA will join the club, buying government bonds in order to hold medium-term bond yields down.

As part of its overall response to the coronavirus and its “very major impact on the economy and the financial system”, the RBA announced a cut to its cash rate target from 0.50% to 0.25% in its first intermeeting rate cut since the mid-1990s. It also announced a suite of three additional policies.

A target of 0.25% has been set for the three-year Australian government bond yield, starting from Friday 20 March. The RBA considers the 3-year rate to be important “as it influences funding rates across much of the Australian economy and is an important rate in financial markets.” RBA chief Philip Lowe said the bank would be “prepared to transact in whatever quantities are necessary to achieve this objective.”

A term-funding facility worth at least $90 billion will be made available to authorised deposit-taking institutions (ADIs) at a fixed rate of 0.25%. ADIs will be able to borrow from the facility amounts equivalent to a maximum of 3% of their existing loans. Additional funding will be made available if lending to business is increased, “especially to small and medium-sized businesses”. The RBA expects to maintain the 0.25% target “until progress is being made towards our goals of full employment and the inflation target.”

18 March 2020

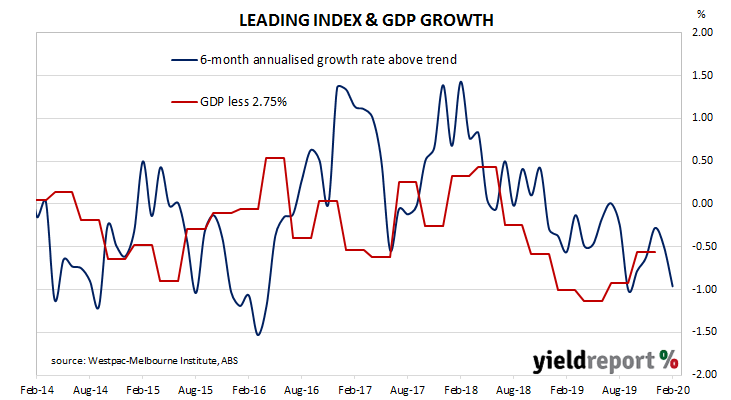

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of Australian economic activity over the next three to six months. After reaching a peak in early 2018, the index trended lower through 2018 and 2019. Readings from the early months of 2020 indicate a continuation of that downtrend.

The latest six month annualised growth rate of the indicator has fallen from January’s revised figure of –0.49% to -0.96% in February. After a brief improvement at the end of 2019, February was the second consecutive month in which readings have deteriorated.

Westpac chief economist Bill Evans said, “The Index growth rate has been running consistently below trend for fifteen months. That signal is indicative that the Australian economy is entering this extremely difficult coronavirus period with insipid momentum and is therefore more vulnerable to the shock.” Index figures represent rates relative to trend-GDP growth, which is generally thought to be around 2.75% per annum. The index is said to lead GDP by three to six months, so theoretically the current reading represents an annualised GDP growth rate of around 1.75% in the middle of 2020.

Index figures represent rates relative to trend-GDP growth, which is generally thought to be around 2.75% per annum. The index is said to lead GDP by three to six months, so theoretically the current reading represents an annualised GDP growth rate of around 1.75% in the middle of 2020.

17 March 2020

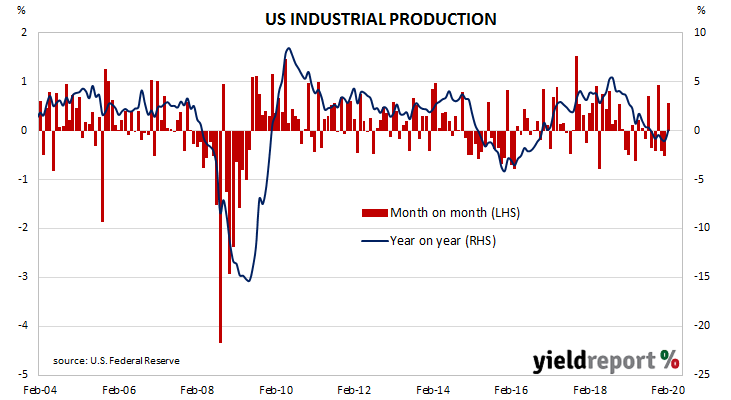

The Federal Reserve’s industrial production (IP) index measures real output from manufacturing, mining, electricity and gas company facilities located in the United States. These sectors are thought to be sensitive to consumer demand and so some leading indicators of GDP use industrial production figures as a component. Had the coronavirus not emerged early in 2020, the latest figures would have added some weight to the argument the downtrend which began in late-2018 was over.

According to February’s figures released by the Federal Reserve, US industrial production increased by +0.6%, higher than the +0.4% increase which had been expected and a complete reversal of January’s revised figure of -0.5%. On an annual basis, the growth rate improved from January’s revised figure of -1.0% to 0.0%.

National Australia Bank Head of FX Strategy Ray Attrill said, “Economic data remains a second-order concern for markets and there wasn’t much reaction to…stronger-than-expected US industrial production…”

The report came on the same day as January’s JOLTS report and February’s retail sales figures were released. Bond yields jumped across the curve but probably more as a result of a general move in financial markets. By the close of trade, the 2-year Treasury yield had gained 13bps to 0.49%, the 10-year had jumped a massive 35bps to 1.08% while the 30-year yield finished 36bps higher at 1.68%.

17 March 2020

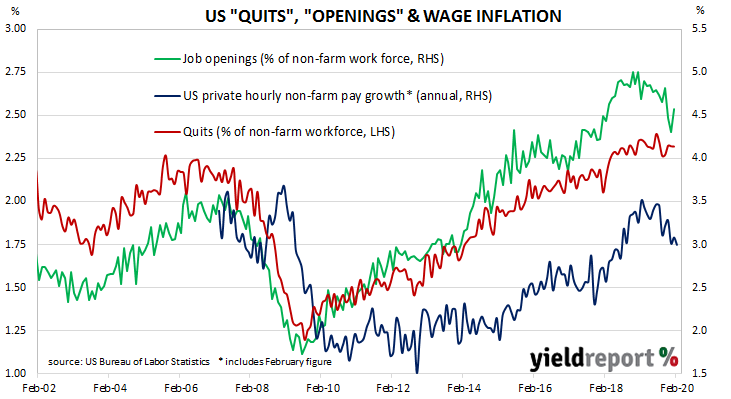

The number of US employees who quit their jobs as a percentage of total employment increased slowly but steadily after the GFC. It peaked in August 2018, stabilised and then remained largely unchanged through the remainder of 2018 before it hit a new peak in July 2019. It has since tracked sideways.

Figures released as part of the most recent JOLTS report show the quit rate has been maintained at just under the record levels reached in July and August. 2.3% of the non-farm workforce left their jobs voluntarily in January, the same rate as December’s revised figure of 2.3% and the same rate as in pretty much all of 2019.

Quit numbers were highest in the retail trade sector while the “Other services” sector recorded the largest fall, with the change in each sector considerably larger than those of other sectors. Overall, the total number of quits for the month increased ever-so-slightly from December’s revised figure of 3.528 million to 3.532 million in January.

Total job openings bounced after two months of falls. Total vacancies during January rose by 411,000 from December’s revised figure of 6.552 million to 6.963 million, driven by increases in the “Health care/social assistance” and “Finance & insurance” sectors. Nearly all sectors experienced increases and only job openings in the “Accommodation & food services” and wholesale trade sectors contracted. Overall, 17 out of 19 sectors experienced more job openings than in the previous month.

National Australia Bank Head of FX Strategy Ray Attrill said the day’s US data remained “a second-order concern for markets”.

17 March 2020

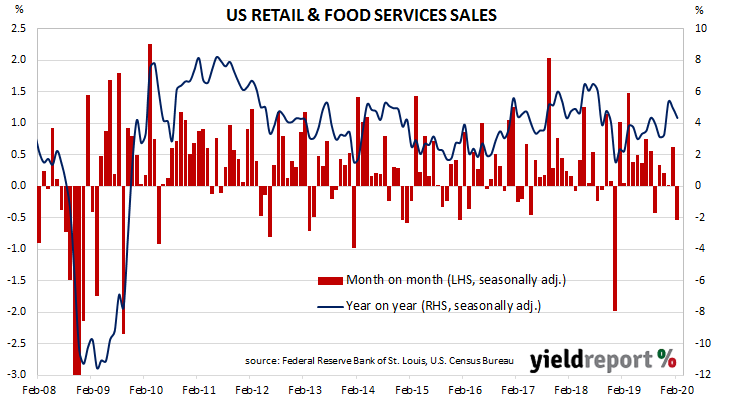

US retail sales had been trending up since late 2015 but, beginning in late 2018, a series of weak or negative monthly results led to a drop-off in the annual growth rate which brought the annual rate below 2.0% by the end of the year. Growth rates then increased in trend terms through 2019 into early 2020.

According to the latest “advance” sales numbers released by the US Census Bureau, total retail sales shrank by 0.5% in February, well under the +0.2% which had been expected and less than January’s revised increase of +0.6%. On an annual basis, the growth rate fell for a second consecutive month, this time to 4.3% from January’s revised rate of 5.0%.

The report came on the same day as January’s JOLTS report and February’s industrial production figures were released. Bond yields jumped across the curve but probably more as a result of a general move in financial markets. By the close of trade, the 2-year Treasury yield had gained 13bps to 0.49%, the 10-year had jumped a massive 35bps to 1.08% while the 30-year yield finished 36bps higher at 1.68%.

In terms of US Fed policy, a rate change of any sort remained unlikely given the federal funds rate has been at the effective lower bound since the US Fed made its second emergency cut for the month on Sunday 15 March.

17 March 2020

The RBA cut its official cash rate target from 0.75% to 0.50% at its March meeting. The idea the RBA would move at its March meeting took a hold of traders in the domestic cash market at the end of the previous week. At that time, March contracts had implied only an 18% chance of a rate move but a day before that, it had been zero. After the weekend, on the day before the RBA meeting, this probability moved to 100%.

The minutes of the March meeting have now been released and the board’s deliberations focussed on the novel coronavirus, its effects on markets in the latter part of February and the responses of central banks. They noted “it was becoming increasingly clear that COVID-19 would cause major disruption to economic activity around the world.” While the minutes went through its familiar format of discussing international and domestic economic conditions, there was little discussion in these sections without some reference to the economic impact of the coronavirus. The RBA Board concluded “the outbreak would have a significant effect on the Australian economy.”

While the minutes went through its familiar format of discussing international and domestic economic conditions, there was little discussion in these sections without some reference to the economic impact of the coronavirus. The RBA Board concluded “the outbreak would have a significant effect on the Australian economy.”

Bill Evans, Westpac’s chief economist said the minutes had largely been overtaken by events of the past few weeks. “Since the Board meeting, the RBA has announced a series of initiatives to boost liquidity in the financial markets. “ He was referring to an expansion of the RBA’s repurchase facility and its announcement of its intention to enter the secondary market for government bonds should it feel it necessary.

13 March 2020

US consumer confidence started 2019 at well-above-average levels in a longer-term context, although readings were markedly lower than those which had been typical of most of the previous year. During the rest of 2019, US households maintained historically-high levels of confidence except for two short-lived plunges; one at the very start of the year and one in August.

The latest survey conducted by the University of Michigan indicates the average confidence level of US households has dropped significantly. The University’s preliminary reading from its Index of Consumer Sentiment registered 95.9 in March, under the consensus figure of 96.4 and noticeably less than February’s final figure of 101.0.

The University’s Surveys of Consumers chief economist, Richard Curtin, said a drop in share prices and increasing coronavirus infections were behind the decline.

US Treasury bond yields increased, especially at the long end but the moves were more in anticipation of a large fiscal response from the US Government to the economic fallout of the coronavirus pandemic. By the close of trade, the 2-year Treasury yield was 4bps higher at 0.51%, the 10-year yield had jumped by 21bps to 0.99% while the 30-year yield had gained 13bps to 1.55%.

In terms of US Fed policy, expectations of another rate reduction by the end of March remained high. According to end-of-day prices of federal funds futures, the implied likelihood of a 75bps cut at the FOMC’s March meeting fell from 50% to 23% while the likelihood of a 100bps reduction increased from 50% to 77%.

12 March 2020

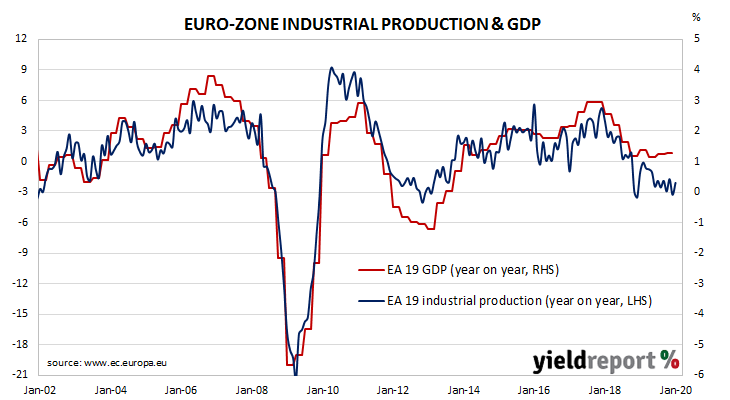

As with other countries’ measures of industrial production, Eurostat’s industrial production index measures the output and activity of industrial sectors in euro-zone countries in aggregate. Following a recession in 2009/2010 and the debt-crisis of 2010-2012 which flowed from it, euro-zone industrial production recovered and then reached a peak four years later in early-2016. Growth rates then slowed through the rest of 2016, accelerated during 2017 and then began another steady and persistent slowdown which has lasted through to the present.

According to the latest figures released by Eurostat, euro-zone industrial production increased by a seasonally-adjusted 2.3% in January, higher than the 1.2% increase which had been expected and also a marked turnaround from December’s -1.8%. On an annual basis, seasonally-adjusted growth in industrial production improved from December’s revised rate of -3.3% to -2.1%* in January.

Industrial production growth rates expanded in all the euro-zone’s four largest economies. Industrial production increased by 2.7% in Germany, in France by 1.2%, in Spain by 0.1% and by 3.7% in Italy.