11 March 2020

A very clear downtrend was evident in the monthly figures of both the number and value of home loan commitments through late-2017 to mid-2019. Then the RBA began to reduce its cash rate target in a series of cuts and both the number and value of mortgage approvals began to noticeably increase.

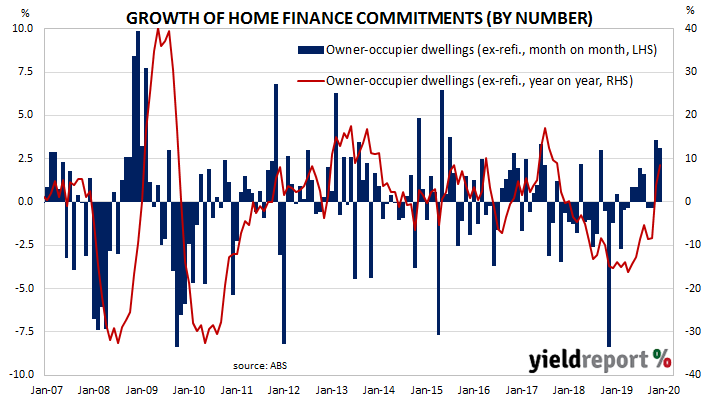

January’s housing finance commitment figures have now been released and the total number of loan commitments (excluding refinancing loans) to owner-occupiers increased by 3.1%, a slight slowing on December’s revised figure of +3.6%. On an annual basis, the growth rate accelerated from December’s revised figure of +3.9% to +8.4%.

Westpac senior economist Matthew Hassan said the number of approvals for construction-related projects suggests a turnaround had begun. “Overall, the picture continues to point to a clear turning point in non-high-rise building activity. The lift in purchases of newly-built dwellings will also help high-rise developers clear unsold stock but is less likely to drive a lift in new projects.”

Local Treasury bond yields finished considerably lower, ignoring unusually large increases in US yields in overnight trading. By the end of the day, the 3-year ACGB yield had lost 9bps to 0.39%, the 10-year yield had fallen by 12bps to 0.67% while the 20-year yield finished just 5bps lower at 1.14%.

Local Treasury bond yields finished considerably lower, ignoring unusually large increases in US yields in overnight trading. By the end of the day, the 3-year ACGB yield had lost 9bps to 0.39%, the 10-year yield had fallen by 12bps to 0.67% while the 20-year yield finished just 5bps lower at 1.14%.

Prices of cash futures contracts moved to reflect a slight firming of rate-cut expectations but only in a theoretical sense. The April contract still implied a 25bps cut to be fully factored in, the same as at the end of the previous day’s trade. Further rate cuts were seen as not particularly likely as the cash rate target would already be at what the RBA considers to be the effective lower bound of 0.25%.

11 March 2020

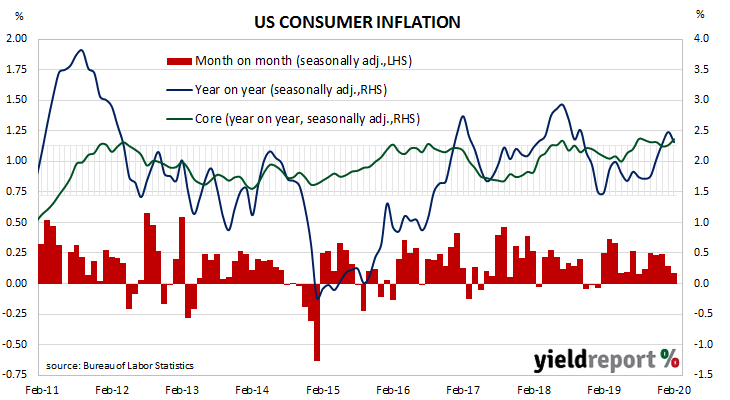

The annual rate of US consumer inflation halved from nearly 3% in the period from July 2018 to February 2019. It then fluctuated in a range from 1.5% to 2.0% through 2019 before rising above 2.0% in the final months of that year. “Headline” inflation is known to be volatile and so references are often made to “core” inflation for analytical purposes. This measure has mostly ranged between 1.7% and 2.3% in recent years.

The latest consumer price index (CPI) figures released by the Bureau of Labor Statistics indicated seasonally-adjusted consumer prices increased by +0.1% on average in February, more than the flat result which had been expected and the same as January’s +0.1%. However, on a 12-month basis, the inflation rate slowed from January’s annual rate of 2.5% to 2.3%.

Core inflation, a measure of inflation which strips out the volatile food and energy components of the index, increased on a seasonally-adjusted basis by +0.2% for the month, in line with expectations and the same as January’s increase. The annual rate ticked up from January’s 2.3% to 2.4% in February.

ANZ FX strategist John Bromhead said “The data were ignored by the market, which is focussed on the supply and demand shock the world is facing.” He noted “a potentially large deflationary shock hangs over us…” in contrast to the rising inflation rates of the past few months.

US Treasury bond yields mostly increased despite the “flight to safety” attitude present in equity markets. By the close of trade, the 2-year Treasury yield had slipped 1bp lower to 0.52% while the 10-year yield had increased by 8bps to 0.88% and the 30-year yield had gained 10bps to 1.39%.

11 March 2020

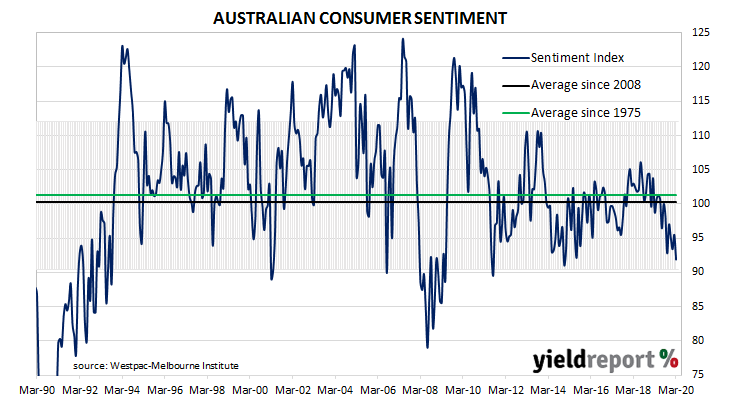

After a lengthy divergence between measures of consumer sentiment and business confidence in Australia which began in 2014, confidence readings of the two sectors converged again around July 2018. Since then, both types of readings have deteriorated, with consumer confidence leading the way. Recent surveys paint a picture of a cautious consumer, indeed a somewhat pessimistic one.

According to the latest Westpac-Melbourne Institute survey conducted in the first week of February, average household optimism has fallen in March after a brief lift occurred in February. The Consumer Sentiment Index declined from 95.5 to 91.9, its lowest reading since December 2014.

Any reading below 100 indicates the number of consumers who are pessimistic is greater than the number of consumers who are optimistic. The latest figure is also very much at the low end of the normal range and well below the long-term average reading of just over 101.

Westpac senior economist Matthew Hassan said, “The worsening coronavirus outbreak and associated rout in financial markets have had a major impact on sentiment this month.”

10 March 2020

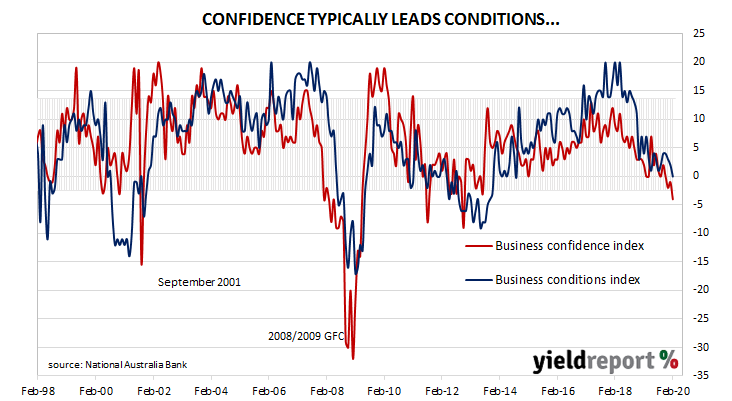

Australian business conditions were robust in the first half of 2018 and a cyclical-peak was reached in April of that year. Readings then began to slip and, by the end of 2018, they had dropped to below-average levels. Forecasts of a slowdown in the domestic economy began to emerge in the first half of 2019 and while conditions remained quite stable at low-growth levels for a period, confidence readings began trending lower.

According to NAB’s latest monthly business survey of 400 firms conducted in the second half of February, business conditions continued to bump along at below-average levels. The NAB’s conditions index has registered 0, down from January’s revised reading of 2.

Business confidence continued its recent downward slide. NAB’s confidence index fell from -1 to -4, further below its long-term average reading of 6. Typically, NAB’s confidence index leads the conditions index by approximately one month, although some divergences appear from time to time.

Alan Oster, NAB’s chief economist, said the survey suggests “ongoing softness in the business sector with conditions and confidence having tracked below average for some time and capacity utilisation hovering around average in recent months.”

US Treasury bond yields had jumped significantly in overnight trading after expectations were raised of a large US fiscal package to cushion the US economy. Local yields largely followed and, by the end of the day, the 3-year ACGB yield had increased by 10bps to 0.48%, the 10-year yield had jumped by 18bps to 0.79% while the 20-year yield finished 20bps higher at 1.19%.

Prices of cash futures contracts moved to reflect a slight softening of rate-cut expectations but only in a technical sense. The April contract still implied a 25bps cut to be fully factored in, the same as at the end of the previous day’s trade. However, further rate cuts were seen as not particularly likely as the cash rate target would already be at what the RBA considers to be the effective lower bound of 0.25%.

06 March 2020

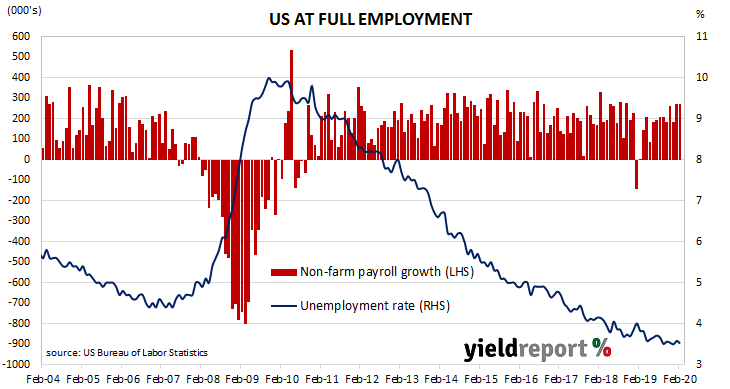

The US economy continues to produce more jobs despite being close to full employment. The US unemployment rate has remained near 3.5% since September 2019 and nearly 1.5 million positions have been created over the past year. The latest employment report indicates the US economy was still producing jobs in February but expectations of further US employment growth have dimmed recently.

According to the US Bureau of Labor Statistics, the US economy created an additional 273,000 jobs in the non-farm sector in February, coincidentally the same number as in January’s revised increase and more than the 195,000 increase which had been expected. Employment figures for November and January were revised up by a total of 85,000.

February’s unemployment rate ticked down from January’s rate of 3.6% to 3.5%. The total number of unemployed shrank by 105,000 to 5.787 million while the total number of people who are either employed or looking for work decreased by 60,000 to 164.546 million. The fall in the number of people in the labour force was not enough to alter the participation rate from 63.4%.

ANZ economist Hayden Dimes said the report was ignored as investors focussed on the likely fallout of more coronavirus infections in the US.

US Treasury yields fell heavily as investors fled equity markets and sought the safety of government bonds. By the close of business, the US Treasury 2-year bond yield had lost 12bps to 0.39%, the 10-year yield had dropped by 20bps to 0.57% and the 30-year Treasury yield plunged by 27bps to 1.02%.

In terms of likely US monetary policy, according to federal funds futures contracts at least another 50bps reduction is expected at the next FOMC meeting, coming on top of the emergency cut made on Tuesday. The implied likelihood of a 50bps cut at the FOMC’s March meeting increased from 51% to 72% while the likelihood of a 75bps reduction increased from zero to 28%.

06 March 2020

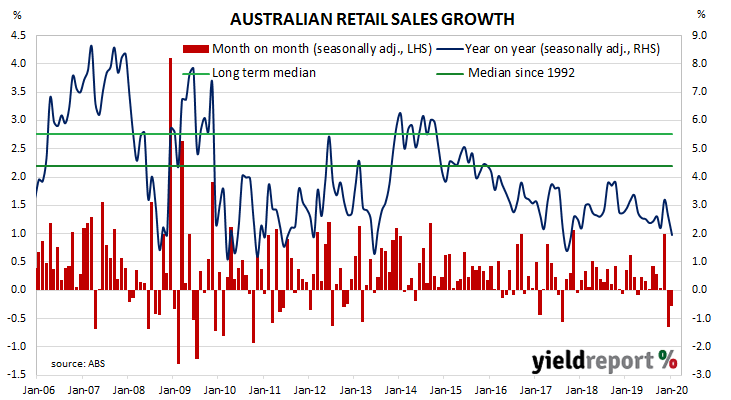

Growth figures of domestic retail sales have been declining since 2014 and they reached a low-point in September 2017 when they registered an annual growth rate of just 1.5%. They then began increasing for about a year, only to stabilise at around 3.0% to 3.5% through late 2018 before trending lower through 2019. January’s figures have continued that trend and economists do not see signs of a turnaround any time soon.

According to the latest ABS figures, total retail sales fell by 0.3% in January on a seasonally-adjusted basis, a larger decline than the flat result which had been expected but not as negative as December’s -0.7% after it was revised down from -0.5%. On an annual basis, retail sales increased by only 2.0%, as compared to December’s comparable figure of 2.6% after revisions.

Westpac senior economist Matthew Hassan said, “Overall, looking through monthly sales-related volatility and temporary bushfire effects, the underlying trend is still clearly weak.”

US Treasury yields had fallen heavily overnight and domestic bond yields followed to some extent except at the short end where yields increased surprisingly. By the end of the day, the 3-year ACGB yield had gained 2bps to 0.38% while the 10-year yield had lost 6bps to 0.61% and the 20-year yield had dropped by 11bps to 0.99%.

Expectations of another cut in the cash rate target in the next month or two firmed up even further. By the end of the day, April contracts implied a rate cut had been fully built in, the same as at the end of the previous day’s trade. However, further rate cuts were seen as not particularly likely and contracts out to December 2020 typically implied a 20%-25% chance of a rate cut down to zero.

ANZ economist Adelaide Timbrell described the fall as “much sharper decline than expected” and the coronavirus “may have been behind part of January’s weakness, along with the bushfires.” She expects the retail sector to be hit “substantially” in coming months.

04 March 2020

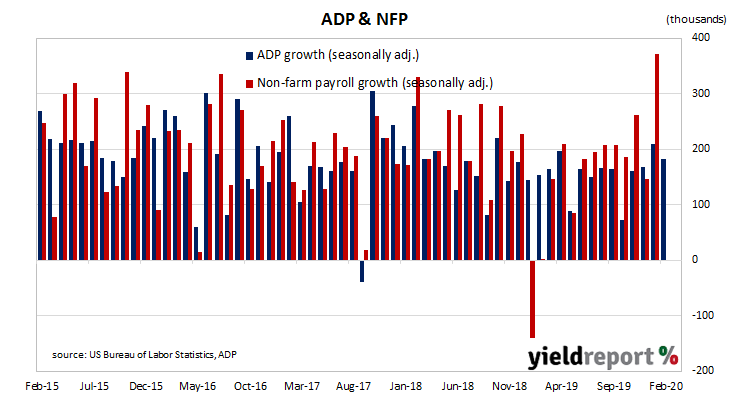

The ADP National Employment Report is a monthly report which provides an estimate of US non-farm employment in the private sector. Since the report began to be published in 2006, its employment figures have exhibited a high correlation with official non-farm payroll figures, although a large difference can arise in any individual month. Even so, the latest report has provided another robust increase.

February’s report indicates private sector employment grew by 183,000, more than the 170,000 which had been expected but less than January’s revised figure of 209,000.

US Treasury yields increased at the long end of the curve while shorter-dated yield remained unmoved as US markets were perceived to welcome a lower likelihood of a Bernie Sanders nomination. By the end of the day, the 2-year Treasury bond yield remained unchanged at 0.69% while the 10-year yield had gained 6bps to 1.06% and the 30-year yield had jumped by 10bps to 1.71%.

In terms of likely US monetary policy, according to federal funds futures contracts another rate cut on top of the emergency cut made on Tuesday is a certainty. The implied likelihood of a 25bps cut at the March meeting of the FOMC remained at 100%.

Employment numbers grew in businesses of all sizes, with a majority of the month’s gain in large businesses. Firms with less than 50 employees added a net 24,000 positions, mid-sized firms (50-499 employees) added 26,000 positions and large businesses (500 or more employees) accounted for 133,000 additional positions

03 March 2020

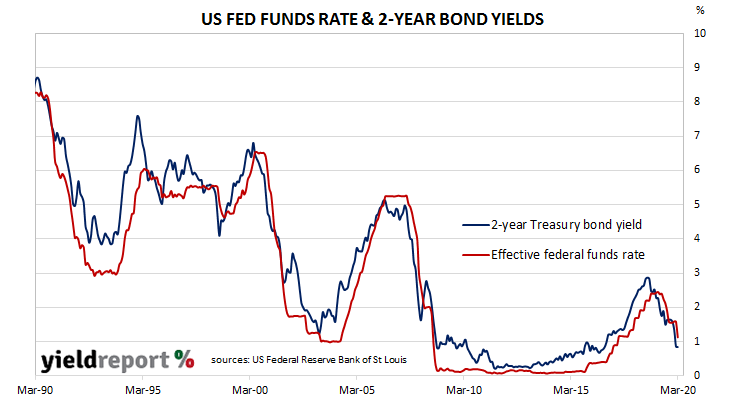

The US was at the heart of what became known as the “Global Financial Crisis” in 2008/2009. As the US economy fell into a deep recession, the Federal Reserve rapidly cut its interbank overnight lending target range to 0%-0.25%. It left this target range close to zero for over seven years until it began to “normalise” interest rates through 2016, 2017 and 2018. However, in early-2019, it was spooked by prospects of a slowing global economy, falling bonds yields and the US-China trade dispute. Shortly thereafter, the Fed began a series of rate cuts, the last of which occurred in October 2019. Up until late last week, the next rate cut was expected in mid-2020.

In a move which would have been a surprise to many up until last Friday, the Federal Reserve cut its overnight interest rate target by 50bps at a meeting of its monetary policy committee. The Fed’s interest rate setting committee, known as the Federal Open Markets Committee (FOMC), reduced its federal funds target range from 1.50%-1.75% to 1.00%-1.25%. The decision came on a day between scheduled meetings, something the FOMC has done in the past only in times of distress, thus prompting the “emergency” description from observers.

The unanimous decision was made despite the committee describing the fundamentals of the US economy as “strong”. The committee’s official statement said “the coronavirus poses evolving risks to economic activity” and, as such, a rate cut would support the Fed’s goals. The statement also stated the Fed will be “closely monitoring developments.”

03 March 2020

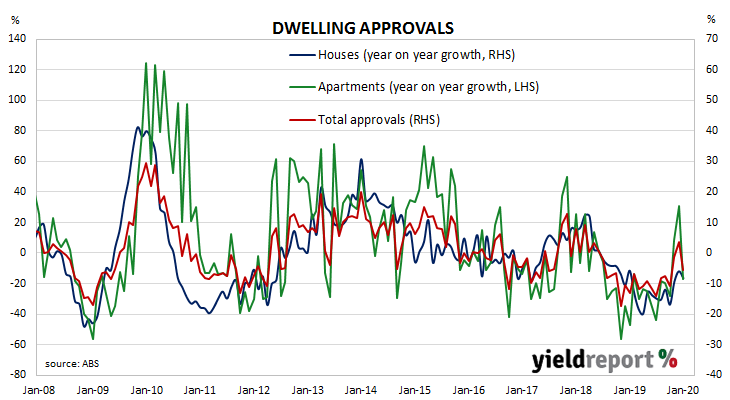

Approvals for dwellings, that is apartments and houses, had been heading south since mid-2018. As an indicator of investor confidence, falling approvals represent a worrying signal, not just for the building sector but for the overall economy. Approval figures from November and December represented a substantial turnaround and the possibility of a recovery in 2020. However, the latest numbers have put the recovery scenario in doubt.

The Australian Bureau of Statistics has released the latest figures from January and total residential approvals fell by 15.3% on a seasonally-adjusted basis, much lower than the +1.0% increase which had been expected and a substantial turnaround from December’s revised figure of +3.9%. On an annual basis, total approvals contracted by 11.3%, a significant deterioration from December’s comparable figure of +7.2% after revisions.

Westpac senior economist Matthew Hassan described the drop as “much sharper than expected”. He put it down to an unwinding of a previous spike in high-rise approvals and bushfire effects.

The report came out before the RBA decided to reduce its cash rate target by 25bps. The reaction in bond markets was subdued in any case and domestic bond yields finished just a touch lower. By the end of the day, the 3-year ACGB yield remained unchanged at 0.45% while 10-year and 20-year yields had each slipped 1bp to 0.79% and 1.21% respectively.

The report came out before the RBA decided to reduce its cash rate target by 25bps. The reaction in bond markets was subdued in any case and domestic bond yields finished just a touch lower. By the end of the day, the 3-year ACGB yield remained unchanged at 0.45% while 10-year and 20-year yields had each slipped 1bp to 0.79% and 1.21% respectively.

Expectations of another cut in the cash rate target remained in place, although they were trimmed just a little. By the end of the day, April contracts implied a 73% chance of a 25bps rate cut, down from the previous day’s 76% while May contracts implied a 95% chance of a cut, down from the previous day’s 100%. Prices of July contracts implied a rate cut had been fully built in.

02 March 2020

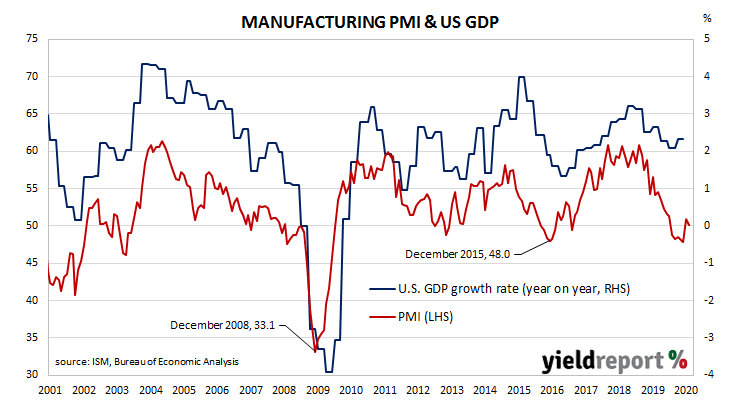

US purchasing managers’ indices (PMIs) have been sliding since August 2018, albeit from elevated levels. After reaching a cyclical peak in September 2017, manufacturing PMI readings went sideways for a year before they started a downtrend. Readings stabilised after a truce of sorts was made with the Chinese regarding trade in late 2019. The latest reading implies US manufacturing activity is still expanding, but only barely.

According to the latest Institute of Supply Management (ISM) survey, its Purchasing Managers Index recorded a reading of 50.1 in February, less than the market’s expected figure of 50.5 and down from January’s final reading of 50.9. The average reading since 1948 is 52.9 and any reading below 50 implies a contraction.

The ISM’s Tim Fiore said, “Comments from the panel were generally positive, with sentiment cautious compared to January. The PMI remained in expansion territory but at a weak level.” US Treasury yields generally increased, although this was likely due to rapidly rising expectations of central banks acting to mitigate the economic fallout from coronavirus infections. By the end of the day, the 2-year Treasury bond yield had slipped 1bp to 0.91%, the 10-year yield had ticked up 1bp to 1.16% while the 30-year yield gained 4bps to 1.72%.

US Treasury yields generally increased, although this was likely due to rapidly rising expectations of central banks acting to mitigate the economic fallout from coronavirus infections. By the end of the day, the 2-year Treasury bond yield had slipped 1bp to 0.91%, the 10-year yield had ticked up 1bp to 1.16% while the 30-year yield gained 4bps to 1.72%.

ANZ economist Adelaide Timbrell noted slowing delivery times posed a concern. “Given COVID-19 disruption only recently became a significant global risk and a headwind to domestic momentum in the US, we’ll likely have to wait for another month of data before we start to see significant impacts.” She said the report indicated delivery times had “slowed owing to delays in receiving inputs.”