02 March 2020

The RBA’s stated objective is to achieve an inflation rate of between 2% and 3%, “on average, over time.” Since the GFC, Australia’s inflation rate has been trending lower and lower and it has been below the RBA’s target band for some years now. Despite the RBA’s desire for a higher inflation rate, attempts to accelerate inflation through record-low interest rates have failed to date.

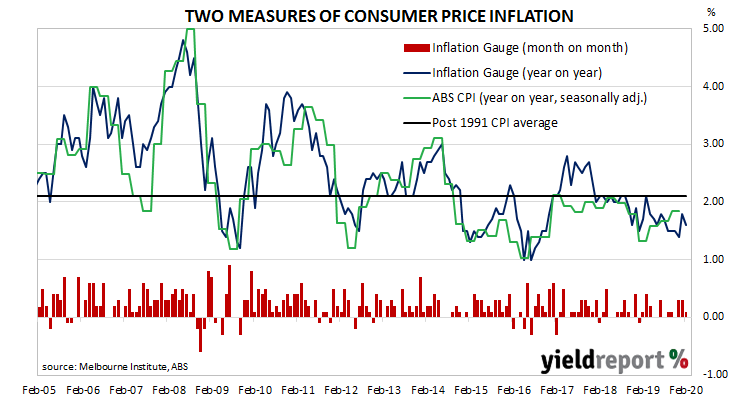

The Melbourne Institute’s latest Inflation Gauge index increased by 0.1% through February following 0.3% increases in December and January. On an annual basis, the index increased by 1.6%, down from January’s comparable rate of 1.8%.

Domestic bond yields at the short end finished lower but, overall, local yields largely discounted significant overnight falls in US markets. By the end of the day, 3-year ACGB yields had shed 5bps to 0.45%, the 10-year yield slipped 1bp to 0.80% while the 20-year yield finished unchanged at 1.22%.

Expectations of another cut in the cash rate target hardened as traders suddenly became convinced the RBA would act in anticipation of a coronavirus-led slowdown. By the end of the day, March contracts implied a 25bps rate cut had been totally priced in, up from the previous day’s 18%. April contracts factored in a March rate cut plus a 76% chance of an additional rate cut at the start of the month. Previously, April contracts had implied a 73% chance of just one rate reduction.

02 March 2020

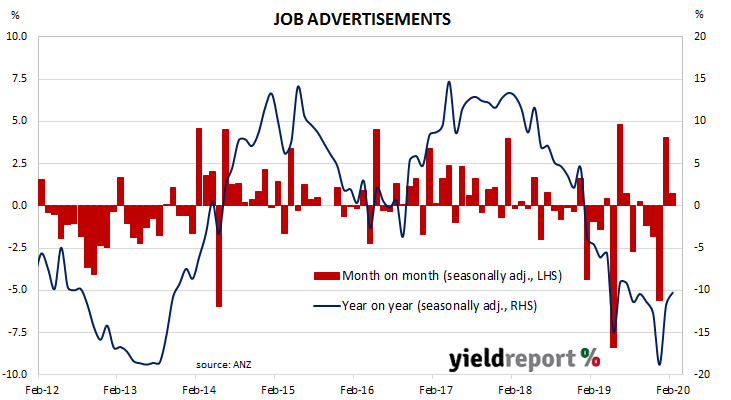

From mid-2017 onwards, year-on-year growth rates in the total number of Australian job advertisements consistently exceeded 10%. That was until mid-2018 when the annual growth rate fell back markedly. 2019 was notable for its reduced employment advertising, along with a reversal of the gains in 2017 and 2018. Despite, the first two surveys of 2020 providing a positive note, economists are doubtful.

According to the latest ANZ figures, total advertisements increased by 0.7% in February on a seasonally-adjusted basis, following a 4.0% rise in January after that month’s figures were revised up. However, on a 12-month basis, total job advertisements were 10.2% lower than the same month last year, a modest improvement from January’s comparable figure of -11.7% after revisions.

ANZ senior economist Catherine Birch said, “This has been a surprise to the positive side; a welcome relief from the more negative data from the private sector on construction work done, capital expenditure, business conditions and confidence.” Domestic bond yields at the short end finished lower but, overall, local yields largely discounted significant overnight falls in US markets. By the end of the day, 3-year ACGB yields had shed 5bps to 0.45%, the 10-year yield slipped 1bp to 0.80% while the 20-year yield finished unchanged at 1.22%.

Domestic bond yields at the short end finished lower but, overall, local yields largely discounted significant overnight falls in US markets. By the end of the day, 3-year ACGB yields had shed 5bps to 0.45%, the 10-year yield slipped 1bp to 0.80% while the 20-year yield finished unchanged at 1.22%.

Expectations of another cut in the cash rate target hardened as traders suddenly became convinced the RBA would act in anticipation of a coronavirus-led slowdown. By the end of the day, March contracts implied a 25bps rate cut had been totally priced in, up from the previous day’s 18%. April contracts factored in a March rate cut plus a 76% chance of an additional rate cut at the start of the month. Previously, April contracts had implied a 73% chance of just one rate reduction.

28 February 2020

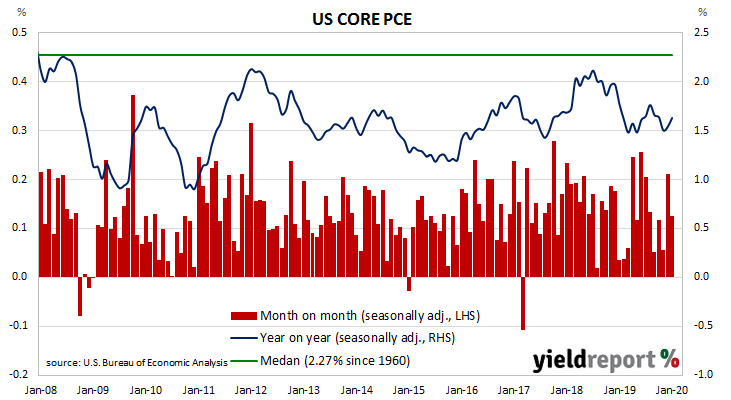

One of the US Fed’s favoured measures of inflation is the change in the core personal consumption expenditures (PCE) price index. After hitting the Fed’s target at 2.0% in mid-2018, the annual rate then hovered in a range between 1.8% and 2.0% through to the end of 2018 before dropping in the first quarter of 2019 to around 1.5%. It has ranged between 1.5% and 1.8% since then.

The latest figures have now been published by the Bureau of Economic Analysis as part of the January personal income and expenditures report. Core PCE prices increased by 0.1% for the month, below the +0.2% increase which had been expected and below December’s 0.2% increase. However, on a 12-month basis, the core PCE inflation rate ticked up from 1.5% to 1.6%.

US Treasury yields finished considerably lower as equity markets sold off amid COVID-19 fears and investors switched to lower-risk assets. By the end of the day, the 2-year Treasury yield had plunged 14bps to 0.92%, the 10-year yield had dropped by 11bps to 1.15% while 30-year yields finished 8bps lower at 1.68%.

In terms of likely US monetary policy, according to federal funds futures contracts the likelihood of another official rate cut jumped dramatically, although the change was not really linked to the report. The probability of a 25bps cut at the March meeting of the FOMC increased from 58% to being fully priced in. Another cut later in the year also became much more likely according to prices of federal funds futures at the end of the day.

28 February 2020

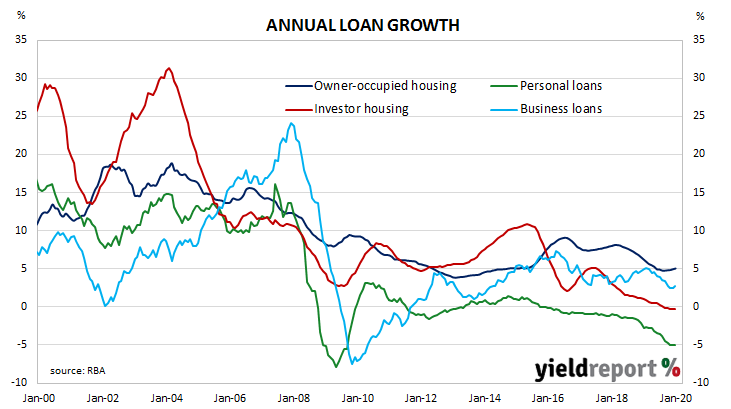

The pace of lending to the non-bank private sector by financial institutions in Australia has been trending down since October 2015. It appeared to have stabilised in the September quarter of 2018 but the annual growth rate then continued to deteriorate through 2019, despite some optimism emerging in the housing market following the re-election of the Coalition Government in May of that year.

While senior RBA officials would like business lending to increase, those same officials would also like households to reduce debt. Recently, RBA Governor Philip Lowe publicly stated the cash rate has been reduced in part to assist households to set aside funds to repay debt.

According to the latest RBA figures, private sector credit grew by +0.3% in January, just above the +0.2% increase which had been expected as well as December’s +0.2% increase. The annual growth rate ticked up from 2.4% to 2.5%.

The increase over the month was predominantly driven by increased business lending, with real estate investors also playing a significant part. Personal lending contracted again while lending to owner-occupiers increased modestly. Westpac senior economist Andrew Hanlan said, “Credit began 2020 on a slightly better note, expanding by 0.33% in January; while not strong, that is the best monthly outcome since October 2018.” He noted a “turnaround in the housing sector is evident.”

Westpac senior economist Andrew Hanlan said, “Credit began 2020 on a slightly better note, expanding by 0.33% in January; while not strong, that is the best monthly outcome since October 2018.” He noted a “turnaround in the housing sector is evident.”

Local financial markets reacted by sending bond yields lower, although demand for bonds was almost certainly driven by a rush to safe assets as equity markets were hit by COVID-19 fears. By the end of the Australian trading day, the 3-year Treasury bond yield had lost 6bps to 0.50%, the 10-year yield had shed 4bps to 0.81% while the 20-year yield finished 3bps lower at 1.22%.

27 February 2020

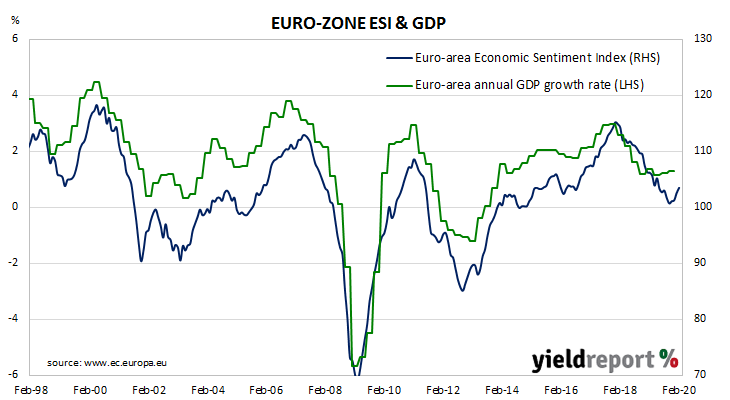

The European Commission’s Economic Sentiment Indicator (ESI) is a composite index comprised of five differently-weighted sectoral confidence indicators. It is heavily weighted towards confidence surveys from the business sector; the consumer confidence sub-index only accounts for 20% of the ESI. However, it has a good relationship with euro-area GDP, although not as a leading indicator.

The ESI recorded a reading of 103.5 in February, above the market’s expected figure of 101.5 and up from January’s reading of 102.6. The average reading since 1985 has been 101. Overall sentiment in the euro-zone improved as three of the five confidence sub-indices showed gains. The Industry, Services and Consumer sub-indices increased while the Retail and Construction sub-indices deteriorated. On a geographical basis, the ESI rose in France, Germany and Spain but remained unchanged in Italy.

Overall sentiment in the euro-zone improved as three of the five confidence sub-indices showed gains. The Industry, Services and Consumer sub-indices increased while the Retail and Construction sub-indices deteriorated. On a geographical basis, the ESI rose in France, Germany and Spain but remained unchanged in Italy.

27 February 2020

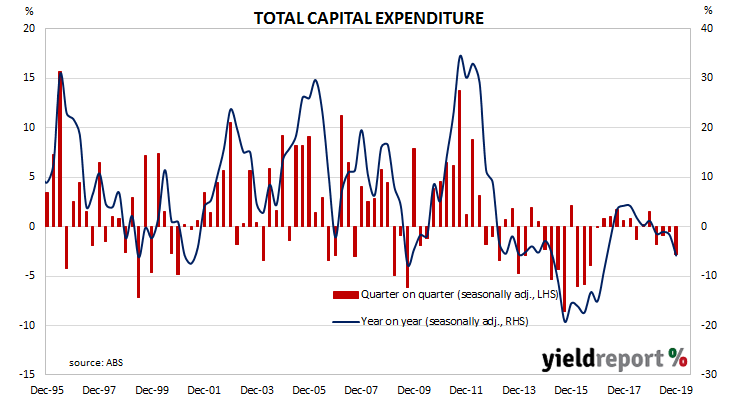

Australia’s capital expenditure (capex) slump was thought to be coming to an end as investment in the mining sector reverted back to its long-term mean after a spike early in the decade. Total investment had begun to grow again, driven by investment in the services sector. However, contractions in recent quarters have become the norm.

According to the latest ABS figures, seasonally-adjusted private sector capex in the December quarter contracted by 2.8%, well below the +0.5% increase which had been expected and under the September quarter’s revised figure of -0.4%. On a year-on-year basis, total capex contracted by 5.8% after recording an annual rate of -1.6% in the September quarter.

ANZ senior economist Catherine Birch said, “The weakness in Q4 was broad-based across mining, manufacturing and other industries.” Local financial markets reacted by sending bond yields lower. By the end of the Australian trading day, the 3-year Treasury bond yield had lost 5bps to 0.56%, the 10-year yield had dropped by 7bps to 0.85% while the 20-year yield finished 4bps lower at 1.25%.

Local financial markets reacted by sending bond yields lower. By the end of the Australian trading day, the 3-year Treasury bond yield had lost 5bps to 0.56%, the 10-year yield had dropped by 7bps to 0.85% while the 20-year yield finished 4bps lower at 1.25%.

In the cash futures market, traders reacted by hardening their expectations of further official rate cuts in 2020, although a March rate cut was still viewed as quite unlikely. The implied probability of a 25bps cut at the RBA’s March meeting remained unchanged at 11% while April contracts implied a 55% chance of a cut, up from the previous day’s 47%. May 2020 contracts implied another cut in the cash rate target had increased from 76% to 83%. Prices of July contracts continued to have a rate cut fully priced in.

26 February 2020

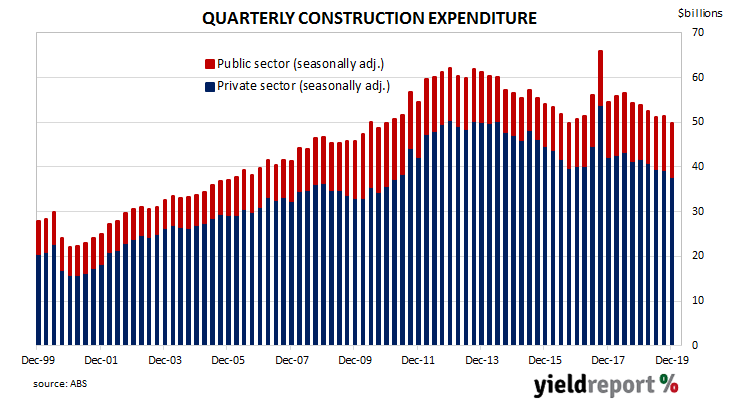

Construction expenditure increased substantially in Australia in the early part of this decade following a more-steady expansion through the 2000s. A large portion of the increase came from the commissioning of new liquid natural gas projects and the expansion of existing mining projects to exploit a tripling in price of Australia’s mining exports in the previous decade. The return to “normal” investment levels is still continuing.

According to the latest construction figures published by the ABS, the value of construction work has continued the downtrend which began in the September quarter of 2018. Total construction in the December quarter fell by 3.0%, a smaller fall than the 1.0% contraction which had been expected and less than the revised 0.4% increase of the September quarter. On an annual basis, the growth rate deteriorated from September’s revised figure of -5.6% to -7.4%.

ANZ senior economist Catherine Birch said, “The downturn in residential activity accelerated but it was private-sector non-residential construction work done that surprised to the downside. Public sector work done provided a small offset.” Commonwealth Government bond yields finished the day a little lower, somewhat in line with lower US Treasury yields. By the end of the day, the 3-year ACGB yield had lost 3bps to 0.61%, the 10-year yields remained unchanged at 0.92% while the 20-year yield finished 2bps lower at 1.29%.

Commonwealth Government bond yields finished the day a little lower, somewhat in line with lower US Treasury yields. By the end of the day, the 3-year ACGB yield had lost 3bps to 0.61%, the 10-year yields remained unchanged at 0.92% while the 20-year yield finished 2bps lower at 1.29%.

In the cash futures market, traders reacted by hardening their expectations of further official rate cuts in 2020, although a March rate cut was still viewed as quite unlikely. The implied probability of a 25bps cut at the RBA’s March meeting increased from 9% to 11% while April contracts implied a 47% chance of a cut, up from the previous day’s 39%. May 2020 contracts implied another cut in the cash rate target had increased from 69% to 76%. Prices of July contracts continued to have a rate cut fully priced in.

26 February 2020

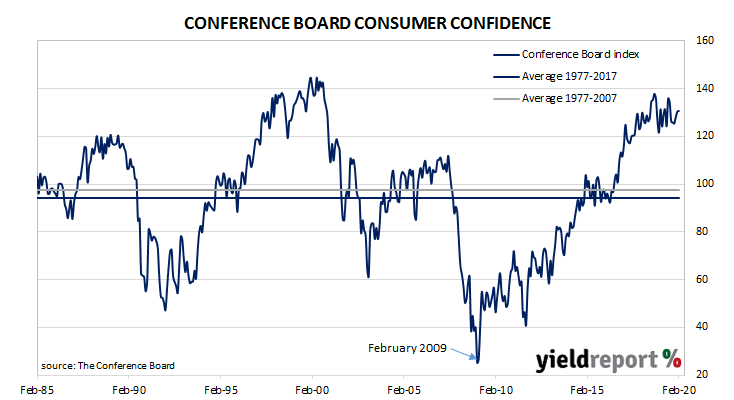

US consumer confidence collapsed in late 2007 as the US housing bubble burst and the US economy went into recession. By 2016, it had clawed its way back to neutral and then went from strength to strength until late 2018. Since then, measures of consumer confidence have oscillated within a fairly narrow band at historically high levels.

The latest Conference Board survey held during the first half of February indicates US consumers remained very optimistic. February’s Consumer Confidence Index registered 130.7, below the median consensus figure of 132.5 but above January’s final figure of 130.4. Compared to consumers’ views held at the time of the January survey, their views of present conditions deteriorated while their views of future conditions improved.

ANZ senior economist Felicity Emmett said, “Confidence remains elevated and while the dip in the present assessment could reflect some anxiety about COVID-19, the outlook is bright, implying private consumption should hold firm.”

Financial markets largely ignored the report as they were focussed on the possible globalisation of the SARS CoV-2 virus and the economic fallout which would accompany it. By the end of the day, yields on 2-year and 10-year Treasury bonds had each lost 2bps to 1.22% and 1.35% respectively while the 30-year yield had slipped 1bp to 1.82%.

20 February 2020

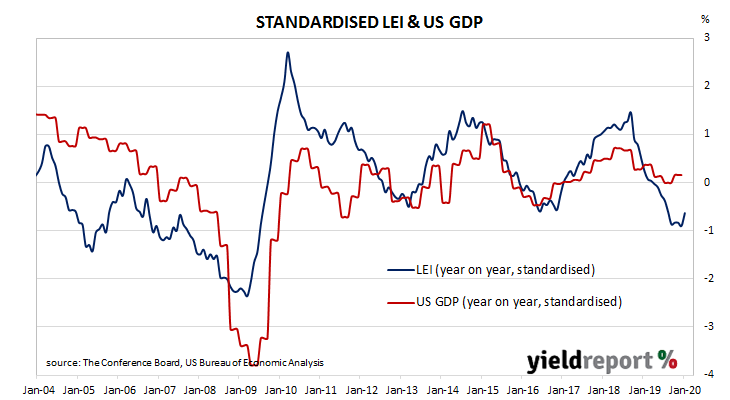

The Conference Board Leading Economic Index (LEI) is a composite index which is composed of ten indices which are thought to be sensitive to changes in the US economy. The Conference Board describes it as an index which attempts to signal peaks and troughs as turning points in the index have historically occurred prior to changes in aggregate economic activity. The second half of 2019 contained a string of negative month-on-month figures and the first result of 2020 may represent a break from this earlier trend.

The Leading Economic Index jumped by 0.8% during January, double the 0.4% which had been expected and representing a large turnaround from December’s -0.3%. On an annual basis, the LEI accelerated from December’s growth rate of 0.2% to 1.0% in January.

The Conference Board’s Senior Director of Economic Research, Ataman Ozyildirim, said the US economy will probably continue to grow at an annualised rate of “about 2%” through early 2020. He also noted “the COVID-19 outbreak may impact manufacturing supply chains in the US in the coming months.”

Changes over time can be large but once they are standardised, a clearer relationship with GDP emerges. The latest reading implies a year-on-year growth rate of 1.5% at the beginning of the June 2020 quarter.

US financial markets reacted by pushing Treasury yields higher but only at the short end. By the end of the day, the yield on 2-year Treasury bonds had increased by 2bps to 1.42%, while 10-year and 30-year yields both remained unchanged at 1.56% and 2.01% respectively.

20 February 2020

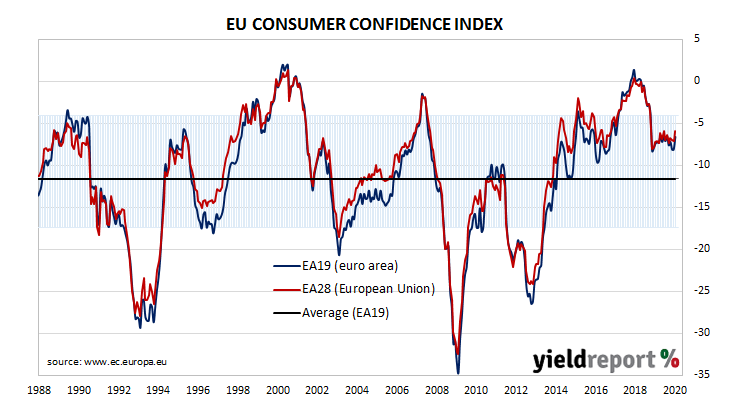

EU consumer confidence plunged during the GFC and again in 2011/12 during the European debt crisis. Since early 2014, it has been at average or above-average levels, rising to a cyclical peak at the beginning of 2018. Even after it dropped back significantly in late 2018 as doubts emerged over the US economy’s robustness, the index remained at a level which corresponds to significant optimism among households.

The February survey conducted by the European Commission indicated household confidence remained at robust levels. The latest published reading of its Consumer Confidence index recorded a figure of -6.6, higher than January’s final figure of -8.1 and well into above-average territory. The average reading since the beginning of 1985 has been -11.6.

ANZ senior economist Catherine Birch said, “The dichotomy between domestic demand and industrial weakness continues.” While measures of consumer confidence have remained elevated, industrial production rates have deteriorated.