11 February 2020

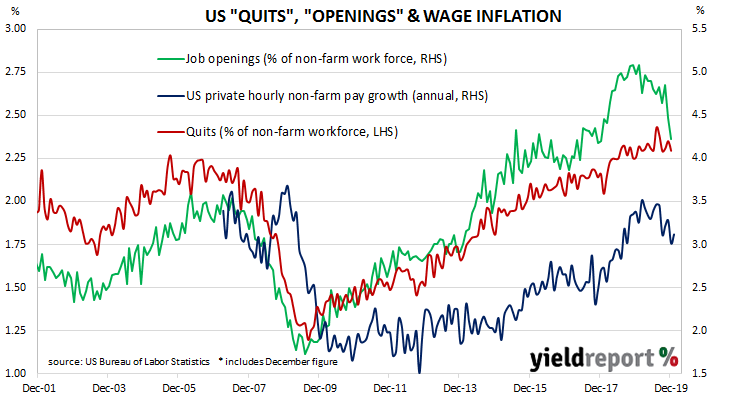

The number of US employees who quit their jobs as a percentage of total employment increased slowly but steadily after the GFC. It peaked in August 2018, stabilised and then remained largely unchanged through the remainder of 2018 before it hit a new peak in July 2019. It has tracked sideways since then.

Figures released as part of the most recent JOLTS report show the quit rate has been maintained at just under the record levels reached in July and August. 2.3% of the non-farm workforce left their jobs voluntarily in December, down from November revised figure of 2.4% but the same rate as in pretty much all of 2019.

Quit numbers were highest in the accommodation/food services sector while the retail trade sector recorded the largest fall, dwarfing changes in other sectors. Overall, the total number of quits for the month decreased from November’s revised figure of 3.568 million to 3.488 million in December.

Total job openings fell noticeably for a second consecutive month. Total vacancies during December fell by 364,000 from November’s revised figure of 6.787 million to 6.423 million, driven by reductions in the “Transportation, warehousing and utilities” and “Health care/social assistance” sectors. The majority of sectors experienced a contraction but the “arts/entertainment” and construction sectors provided a modest offsetting effect. Overall, 13 out of 19 sectors experienced fewer job openings than in the previous month.

NAB Head of FX strategy Ray Attrill said the total was less than expected and the fall suggests “a significantly slower monthly payroll gains down the not-too-distant track.” However, ANZ economist suggested “job openings are falling because the participation rate is rising” while admitting “it could also reflect weakening hiring demand.”

07 February 2020

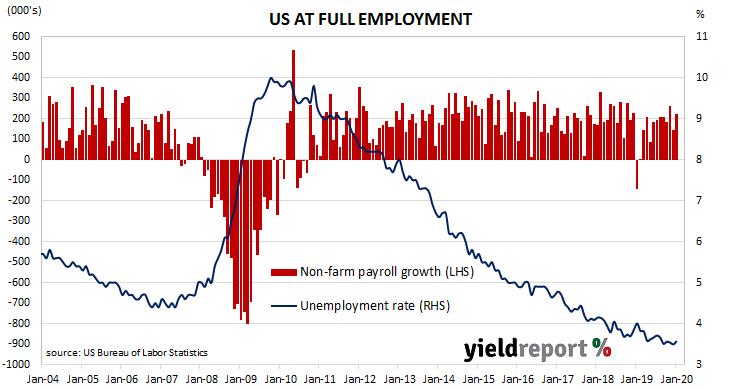

The US economy continues to produce more jobs despite being close to full employment. The unemployment rate has remained at or under 4% since April 2018 and the underemployment rate has been falling in trend terms. The latest employment report indicates the US economy is still producing jobs and drawing Americans back into the workforce.

According to the US Bureau of Labor Statistics, the US economy created an additional 225,000 jobs in the non-farm sector in January, more than December’s revised increase of 147,000 and more than the 160,000 increase which had been expected. Employment figures for December and November were revised up by a total of 7,000.

January’s unemployment rate ticked up from December’s rate of 3.5% to 3.6%. The total number of unemployed increased by 139,000 to 5.892 million while the total number of people who are either employed or looking for work increased by 50,000 to 164.606 million. The increase in the number of people in the labour force helped drive the participation rate from 63.2% to 63.4%.

NAB economist Tapas Strickland described the result as “strong” but noted the report “had little impact on markets, suggesting the coronavirus was the predominant force on markets.” US Treasury yields fell uniformly across the curve. By the close of business, 2-year, 10-year and 30-year Treasury yields had all lost 6bps to 1.40%, 1.58% and 2.05% respectively.

US Treasury yields fell uniformly across the curve. By the close of business, 2-year, 10-year and 30-year Treasury yields had all lost 6bps to 1.40%, 1.58% and 2.05% respectively.

In terms of likely US monetary policy, according to federal funds futures contracts the probability of a rate cut in the first half of 2020 remained small, although price changes did imply some small increases. The implied likelihood of a 25bps cut at the March meeting of the FOMC increased from 9% to 11% while a Fed move in June rose from 36% to 46%. A Fed cut in July looked more likely as prices at the end of the day implied traders had increased the chances of a rate cut in that month from 49% to 57%.

06 February 2020

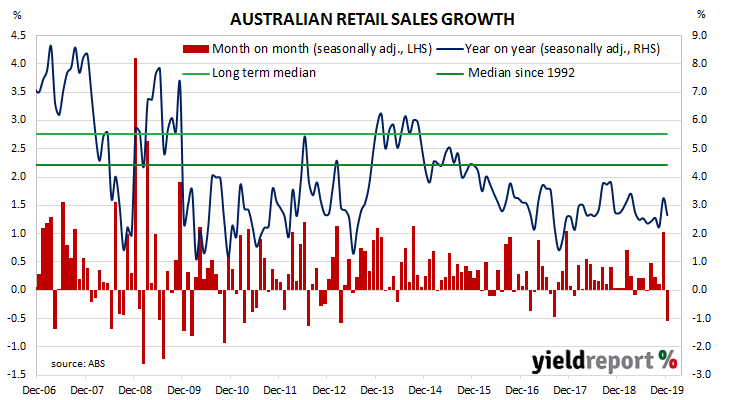

Growth figures of domestic retail sales have been declining since 2014 and they reached a low-point in September 2017 when they registered an annual growth rate of just 1.5%. They then began increasing for about a year, only to stabilise at around 3.0% to 3.5% through late 2018 before trending lower through 2019. November’s figures were boosted by Australia’s recent embrace of “Black Friday” sales and economists were expecting some pullback in December as a result.

According to the latest ABS figures, total retail sales fell by 0.5% in December on a seasonally-adjusted basis, a larger decline than the 0.2% fall which had been expected and well below November’s 1.0% increase after it was revised up from 0.9%. On an annual basis, retail sales increased by just 2.7%, as compared to November’s revised figure of 3.3%.

Bell Potter retail analyst Sam Haddad summed the report up. “The soft December data was expected and reflects the pull-forward of sales into November due to the Black Friday/Cyber Monday promotion and a consumer bias towards such promotions.”

US Treasury yields had increased by modest amounts overnight but bond yields in the domestic market moved a little harder. By the end of the day, the 3-year ACGB yield had gained 5bps to 0.76%, the 10-year yield had increased by 6bps to 1.11% while the 20-year yield finished 7bps higher at 1.51%.

Prices of cash futures contracts moved to soften expectations of a rate cut in the first half of 2020, although the perceived likelihood of a July cut still remained high. March contracts implied a 9% chance of a 25bps rate cut, down from the previous day’s 13% while April contracts implied a 26% chance of another cut, down from 42%. May contracts implied a 41% chance but July contracts still implied an 82% likelihood.

05 February 2020

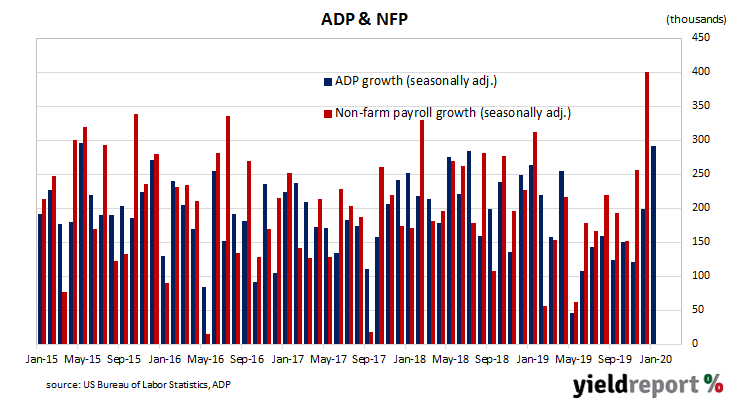

The ADP National Employment Report is a monthly report which provides an estimate of US non-farm employment in the private sector. Since the report began to be published in 2006, its employment figures have exhibited a high correlation with official non-farm payroll figures, although a large difference can arise in any individual month. Even so, the latest report has provided another strong increase.

January’s report indicates private sector employment grew by 291,000, almost double the expected figure of 150,000 and a good deal more than December’s revised increase of 199,000.

NAB currency strategist Rodrigo Catril is not a great fan of the predictive powers of the ADP report, saying “this indicator doesn’t have a great track record at predicting US non-farm payrolls…” However, he noted “the strength of ADP was sufficient to offer some offset” to a “disappointing” fall in order backlogs in the ISM non-manufacturing report.

US Treasury yields increased along the curve but more so at the long end. By the end of the day, the 2-year Treasury bond yield had gained 2bps to 1.44% while 10-year and 30-year yields had each increased by 5bps to 1.65% and 2.14% respectively.

In terms of likely US monetary policy, according to federal funds futures contracts the probability of a rate cut in the first half of 2020 remained small. The implied likelihood of a 25bps cut at the March meeting of the FOMC slipped from 9% to 7% while a move in April remained unchanged at 23%. Even a July cut looked less likely; prices at end of the day implied a rate cut at the FOMC’s July meeting had fallen from 55% to 49%.

03 February 2020

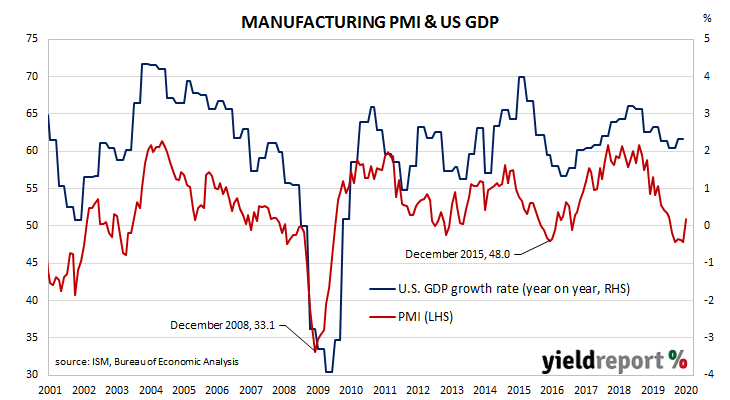

US purchasing managers’ indices (PMIs) have been sliding since August 2018, albeit from elevated levels. After reaching a cyclical peak in September 2017, manufacturing PMI readings went sideways for a year before they started a downtrend. Recent readings appear to have stabilised, albeit at sub-neutral levels. The latest reading marks a return to expansionary levels.

According to the latest Institute of Supply Management (ISM) survey, its Purchasing Managers Index recorded a reading of 50.9 in January, up from December’s final reading of 47.8 and more than the market’s expected figure of 48.4. The average reading since 1948 is 52.9 and any reading below 50 implies a contraction.

The ISM’s Tim Fiore said, “Global trade remains a cross-industry issue, but many respondents were positive for the first time in several months.”

US Treasury yields increased by modest amounts across the curve. By the end of the day, 2-year and 10-year Treasury bond yields had both gained 3bps to 1.35% and 1.53% respectively while the 30-year yield crept up 1bp to 2.01%.

In terms of likely US monetary policy, according to federal funds futures contracts the probability of a rate cut in the first half of 2020 remained small. The implied likelihood of a 25bps cut at the March meeting of the FOMC fell from 27% to 16% while a move in April declined from 44% to 37%. However, the likelihood of a cut jumps in the second half; prices at end of the day implied a rate cut at the FOMC’s July meeting to be 66%.

03 February 2020

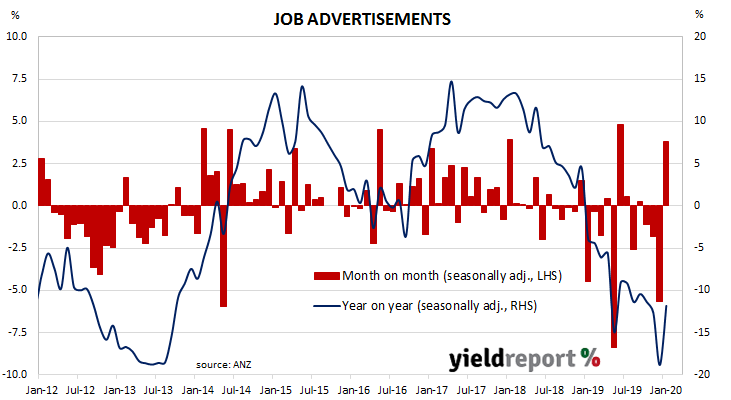

From mid-2017 onwards, year-on-year growth rates in the total number of Australian job advertisements consistently exceeded 10%. That was until mid-2018 when the annual growth rate fell back markedly. 2019 was notable for its reduced employment advertising, along with a reversal of the gains in 2017 and 2018. However, the first survey of 2020 has started on a positive note.

According to the latest ANZ figures, total advertisements increased by 3.8% in January on a seasonally-adjusted basis, following a 5.7% fall in December after it was revised up. On a 12-month basis, total job advertisements were 11.8% lower than the same month last year, a sharp reversal from December’s comparable figure of -18.8%.

ANZ senior economist Catherine Birch said, “Job ads recovered some ground in January but not enough to fully offset the upwardly-revised 5.7% drop in December.”

03 February 2020

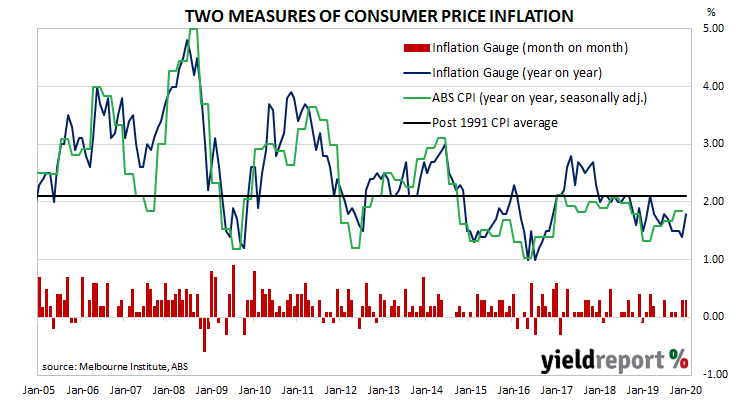

The RBA’s stated objective is to achieve an inflation rate of between 2% and 3%, “on average, over time.” Since the GFC, Australia’s inflation rate has been trending lower and lower and it has been below the RBA’s target band for some years now. Despite the RBA’s desire for a higher inflation rate, attempts to accelerate inflation through record-low interest rates have failed so far.

The Melbourne Institute’s latest Inflation Gauge index increased by 0.3% during January following a 0.3% increase in December and a flat result in November. On an annual basis, the index increased by 1.8%, up from December’s 1.4%.

Domestic bond yields finished a little lower, largely ignoring significant overnight falls in US markets. By the end of the day, 3-year and 10-year ACGB yields had each lost 3bps to 0.58% and 0.94% respectively while the 20-year yield had shed 2bps to 1.33%.

Expectations of another cut in the cash rate target hardened. By the end of the day, February contracts implied a 28% chance of a 25bps rate cut, up from the previous day’s 14% while March contracts implied a 62% chance of a cut, up from 44%. Prices of April contracts had a rate cut fully built-in.

03 February 2020

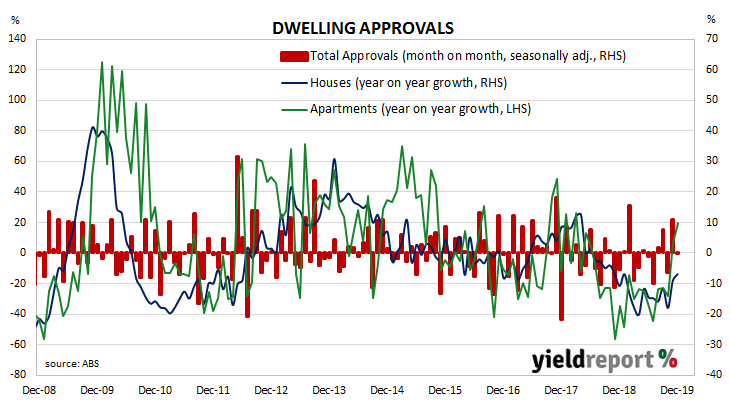

Approvals for dwellings, that is apartments and houses, had been heading south since mid-2018. As an indicator of investor confidence, falling approvals represent a worrying signal, not just for the building sector but for the overall economy. November’s figures represented a substantial turnaround and now December’s figures have lent weight to some economists’ forecasts of a recovery in 2020.

The Australian Bureau of Statistics has released the latest figures from December and total residential approvals fell by 0.2% on a seasonally-adjusted basis, a smaller fall than the 5% contraction which had been expected but a noticeable turnaround from November’s revised figure of +10.9%. However, on an annual basis, total approvals increased by 2.7%, an improvement on November’s comparable figure of -2.8% after revisions.

Westpac senior economist Matthew Hassan said one-off factors may have padded the figures to some extent. However, he also noted the report did contain “some hints of firming elsewhere.”

31 January 2020

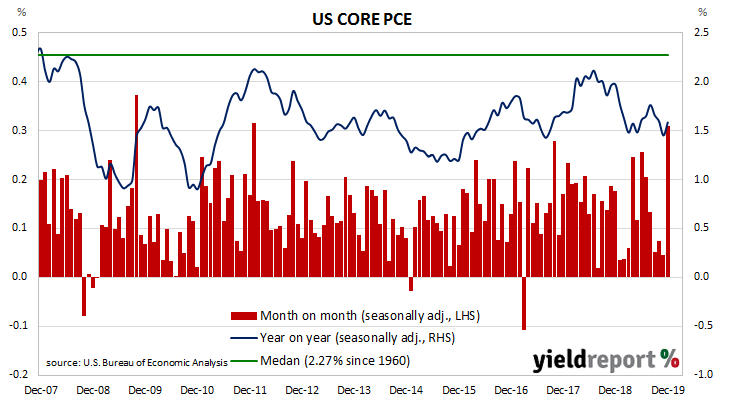

One of the US Fed’s favoured measures of inflation is the change in the core personal consumption expenditures (PCE) price index. After hitting the Fed’s target at 2.0% in mid-2018, the annual rate then hovered in a range between 1.8% and 2.0% through to the end of 2018 before dropping in the first quarter of 2019 to around 1.5%. It then ranged between 1.5% and 1.8% for the rest of the year.

The latest figures have now been published by the Bureau of Economic Analysis as part of the December personal income and expenditures report. Core PCE prices increased by 0.3% for the month, above expectations and a jump from November’s flat result. On a 12-month basis, the core PCE inflation rate rebounded to 1.6% after slipping to 1.5% in November.

ANZ economist Daniel Been said, “This is encouraging but will not alter the Fed’s accommodative bias, which aims to lift actual and expected inflation.”

US Treasury yields finished the day considerably lower as markets factored in potentially less economic activity from a coronavirus-related slowdown in trade and tourism. By the end of the day, 2-year yields had dropped by 10bps to 1.32%, 10-year yields had shed 9bps to 1.50% while 30-year yields finished 5bps lower at 2.00%.

31 January 2020

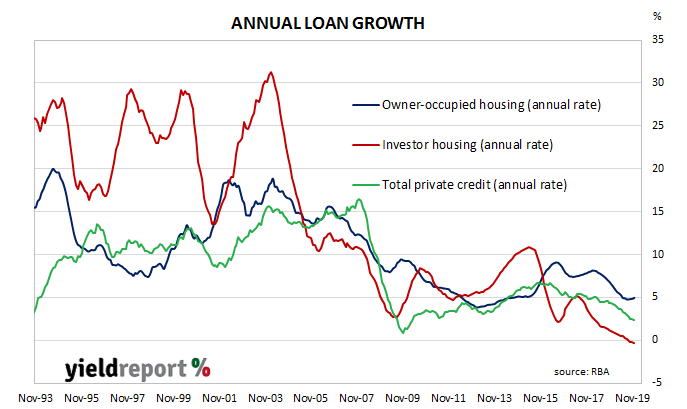

The pace of lending to the non-bank private sector by financial institutions in Australia has been trending down since October 2015. It appeared to have stabilised in the September quarter of 2018 but the annual growth rate then continued to deteriorate through 2019, despite some optimism emerging in the housing market following the re-election of the Coalition Government in May of that year.

According to the latest RBA figures, private sector credit grew by +0.2% in December, in line with expectations as well as November’s +0.2% increase. The annual growth rate remained unchanged at 2.4%, with the increase spread almost evenly between lending to owner-occupiers, investors and business.

Westpac senior economist Andrew Hanlan put the figures into a broader context. “Currently, credit growth is around historic lows and compares with the cycle lows of 0.8% in November 2009, associated with the GST, and -1.8% in April 1992, associated with the recession of the early 1990s.” Local financial markets reacted by sending bond yields lower, ignoring slightly higher US bond yields in overnight trading. By the end of the Australian trading day, the 3-year Treasury bond yield had slipped 1bp to 0.61%, the 10-year yield remained unchanged at 0.97% while the 20-year yield finished 3bps lower at 1.35%.

Local financial markets reacted by sending bond yields lower, ignoring slightly higher US bond yields in overnight trading. By the end of the Australian trading day, the 3-year Treasury bond yield had slipped 1bp to 0.61%, the 10-year yield remained unchanged at 0.97% while the 20-year yield finished 3bps lower at 1.35%.

Despite generally lower yields in the bond market, prices of cash futures contracts moved to lower expectations of another rate cut. By the end of the day, February contracts implied a 14% chance of a 25bps rate cut, down from the previous day’s 16%. March contracts implied a 44% chance of a cut, down from 47%. However, April contracts implied an 81% likelihood while May contracts continued to imply another cut as a certainty.