17 January 2020

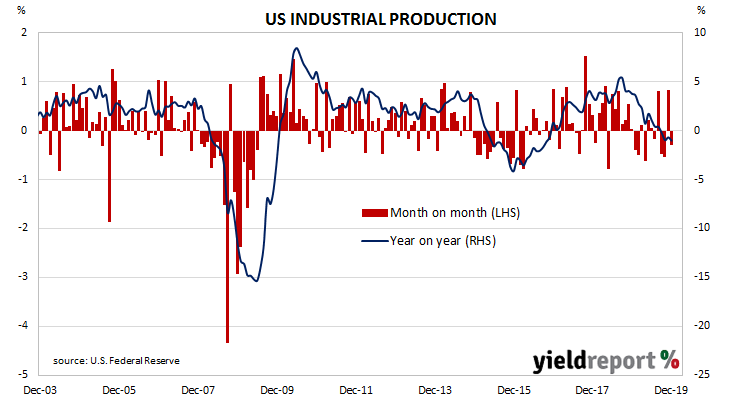

The Federal Reserve’s industrial production (IP) index measures real output from manufacturing, mining, electricity and gas company facilities located in the United States. These sectors are thought to be sensitive to consumer demand and so some leading indicators of GDP use industrial production figures as a component.

The latest figures indicate a downtrend which began in late 2018 has continued.

According to December’s figures released by the Federal Reserve, US industrial production fell by 0.3%, less than the flat result which had been expected and a distinct drop from Novembers 0.8% increase. On an annual basis, the growth rate returned to -1.0% after having increased to -0.7% in November.

According to Westpac macro strategist Tim Riddell, “the tail end of auto-sector strikes impacted activity.” The report came on the same day as JOLTS figures and consumer sentiment figures were released and bond yields eased at the short end. By the close of trade, the 2-year Treasury yield was 2bps lower at 1.56% while the 10-year yield had inched up 1bp to 1.82% and the 30-year yield had gained 2bps to 2.28%.

The report came on the same day as JOLTS figures and consumer sentiment figures were released and bond yields eased at the short end. By the close of trade, the 2-year Treasury yield was 2bps lower at 1.56% while the 10-year yield had inched up 1bp to 1.82% and the 30-year yield had gained 2bps to 2.28%.

In terms of US Fed policy, expectations of another rate change in the next few months remained soft. According to end-of-day prices of federal funds futures, the implied probability of a 25bps rate cut at either of the FOMC’s January or March meetings remained at zero, while the likelihood of a rate cut by or at July’s meeting fell from 29% to 25%.

16 January 2020

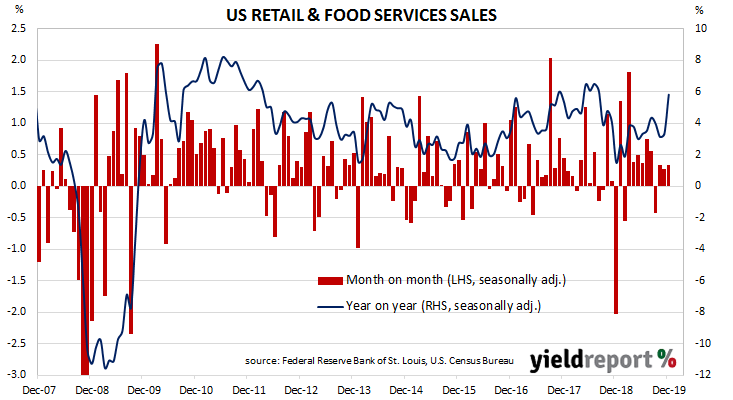

US retail sales had been trending up since late 2015 but, beginning in late 2018, a series of weak or negative monthly results led to a drop-off in the annual growth rate which brought the annual rate below 2.0% by the end of the year. After an unsteady start to 2019, subsequent months’ figures have been consistently positive. Apart from February, just one other month in 2019, September, recorded a decline.

According to the latest “advance” sales numbers released by the US Census Bureau, total retail sales grew by 0.3% in December, in line with expectations and the same rate as in November. On an annual basis, the growth rate jumped to 5.8% from November’s rate of 3.3%.

ANZ FX strategist John Bromhead said, “The data show strong momentum in private consumption at year-end and the early evidence for 2020 is that the pace is spilling into the New Year.”

Treasury bond yields increased on the day, with larger movements at the front of the curve. By the close of business, the 2-year US Treasury yield had increased by 4bps to 1.58%, the 10-year rate had gained 3bps to 1.81% while the 30-year yield finished 2bps higher at 2.26%.

Expectations of a change in the federal funds rate in the next few months remained low. According to end-of-day prices of federal funds futures, the implied probability of a 25bps rate cut at either of the FOMC’s January or March meetings remained at zero.

16 January 2020

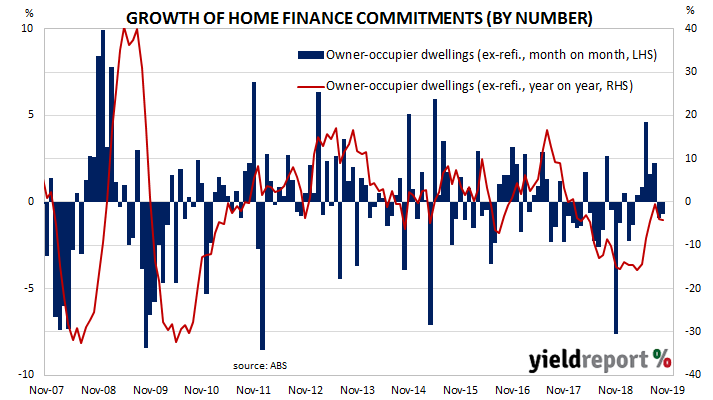

A very clear downtrend was evident in the monthly figures of both the number and value of home loan commitments through late 2017 to June 2019. Then the RBA began to reduce its cash rate target in a series of cuts. Both the number and value of mortgage approvals began to noticeably increase during that time.

November’s housing finance commitment figures have now been released and the total number of loan commitments (excluding refinancing loans) to owner-occupiers fell by 0.7%, a small improvement on October’s revised figure of -0.9%. However, on an annual basis, the growth rate deteriorated for a second consecutive month, from October’s revised figure of -4.0% to -4.2%.

Australian Commonwealth Government bond yields fell on the day, although the falls were largely in line with moves in US Treasury bond markets. By the end of the day, the yield on 3-year, 10-year and 20-year ACGBs had all lost 3bps to 0.77%, 1.20% and 1.61% respectively.

Expectations of future rate cuts hardened in the cash futures market. At the close of trade, February contracts implied another 25bps rate cut was a 56% chance, up from the previous day’s 51%. The likelihood of a rate cut at the RBA’s March meeting was 73%, up from 68% while April contracts implied a rate cut was fully priced in.

15 January 2020

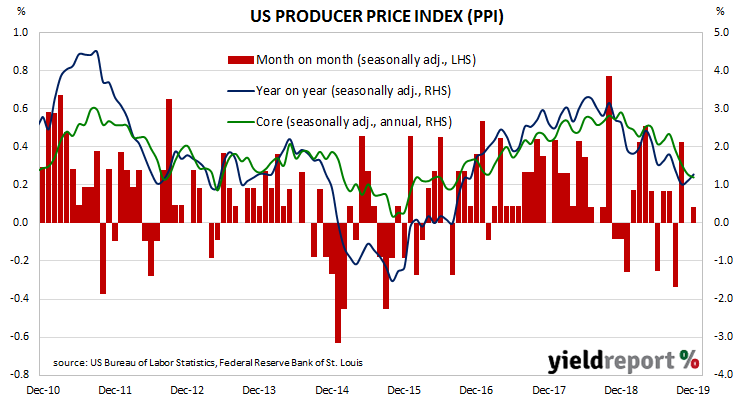

Around the end of 2018, the annual rate of prices received by producers began a downtrend which then continued through 2019. Months in which prices picked up suggested the trend may have been coming to an end but, so far, the down trend has continued.

The figures from December have been published by the Bureau of Labor Statistics and they indicate producer prices increased by just 0.1% after seasonal adjustments, less than the 0.2% which had been expected but an increase from November’s flat result. On a 12-month basis, the rate of producer price inflation after seasonal adjustments accelerated to 1.3% after recording 1.1% in November and 1.0% in September.

ANZ economist Hayden Dimes said the result was weaker than expected “due to softness in the service sector offsetting higher-priced goods.” However, he also noted some Federal Reserve officials were waiting for the effects of last year’s rate cuts to flow through. “Inflation remains well below the Fed target of 2% but San Francisco Federal Reserve President Daly said the three rate cuts last year put the economy on track to reach that target.”

15 January 2020

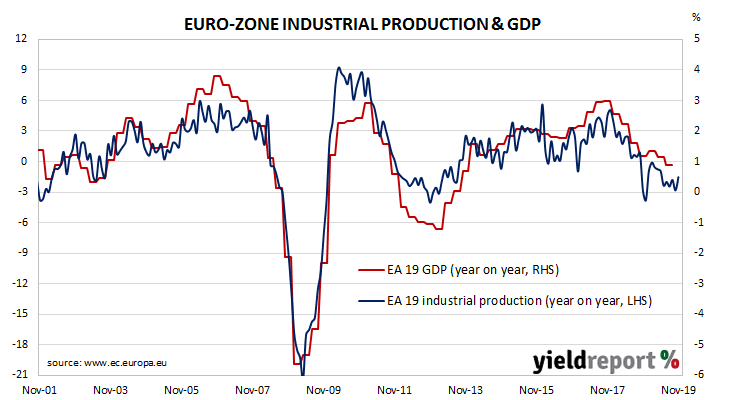

Following the European debt-crisis of 2010-2012, euro-zone industrial production began to recover until a peak was reached four years later in early-2016. Growth rates then slowed through the rest of 2016, accelerated during 2017 and then began a steady slowing which has lasted through to late-2019.

According to the latest figures released by Eurostat, euro-zone industrial production increased by a seasonally-adjusted 0.2% in November, less than the 0.3% increase which had been expected but a marked turnaround from October’s revised figure of -0.9%. On an annual basis, seasonally-adjusted growth in industrial production improved from October’s revised rate of -2.8% to -1.5%* in November.

Westpac macro strategist Tim Riddle said the figures were “a sign of potential bottoming in regional activity” despite the relatively lacklustre growth rate for the month.

14 January 2020

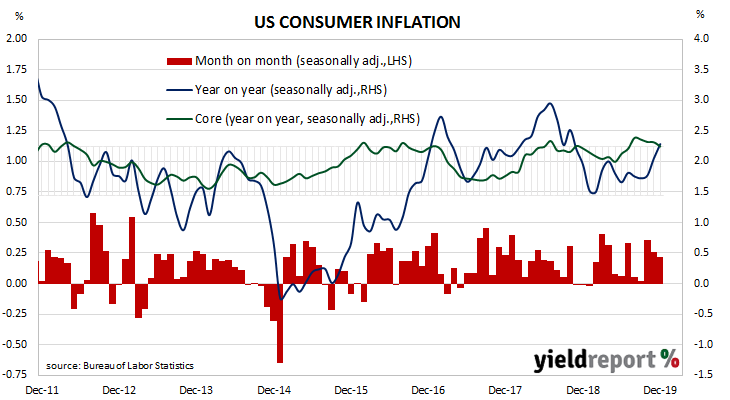

The annual rate of US consumer inflation halved from nearly 3% in the period from July 2018 to February 2019 and then subsequently fluctuated in a range from 1.5% to 2.0%. However, “headline” inflation is known to be volatile and so references are often made to “core” inflation figures for purposes of analysis. This measure has mostly ranged between 1.7% and 2.3% in recent years.

The latest consumer price index (CPI) figures released by the Bureau of Labor Statistics indicated seasonally-adjusted consumer prices increased by +0.2% in December, in line with the +0.2% increase which had been expected but lower than November’s +0.3%. On a 12-month basis, the inflation rate increased from November’s annual rate of 2.1% to 2.3%. Core inflation, a measure of inflation which strips out the volatile food and energy components of the index, increased on a seasonally-adjusted basis by +0.1% for the month, less than the 0.2% which had been expected and less than November’s +0.1% increase. The annual rate slipped from November’s 2.3% to 2.2% in December.

Core inflation, a measure of inflation which strips out the volatile food and energy components of the index, increased on a seasonally-adjusted basis by +0.1% for the month, less than the 0.2% which had been expected and less than November’s +0.1% increase. The annual rate slipped from November’s 2.3% to 2.2% in December.

ANZ senior economist Felicity Emmett said the report “was viewed as a little disappointing, with markets looking for a bit more life in core CPI.”

US Treasury bond yields fell on the day. By the close of trade, the 2-year Treasury yield had lost 3bps to 1.56%, the 10-year yield had fallen by 4bps to 1.81% and the 30-year yield finished 3bps lower at 2.27%.

In the futures market for federal funds, expectations of further rate changes in the short term remained low. According to end-of-day prices of federal funds futures, the implied probability of a 25bps rate cut at either of the FOMC’s January or March meetings remained at zero. July contracts implied a 30% chance of a rate cut, up from the previous day’s 28%.

13 January 2020

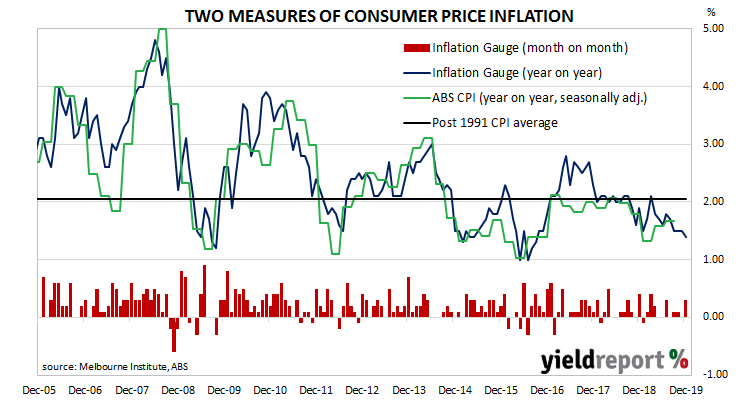

The RBA’s stated objective is to achieve an inflation rate of between 2% and 3%, “on average, over time.” Since the GFC, Australia’s inflation rate has been trending lower and lower and it has been below the RBA’s target band for some years now. Despite the RBA’s desire for a higher inflation rate, attempts to accelerate inflation through record-low interest rates have failed so far. The latest unofficial measure of consumer inflation suggests the annual rate of consumer inflation is likely to fall, at least in the short term.

The Melbourne Institute’s latest Inflation Gauge index increased by 0.3% during December following a flat result in November and a 0.1% increase in October. On an annual basis, the index increased by 1.4%, down from November’s rate of 1.5%.

Domestic bond yields finished the day lower, largely following overnight leads from US Treasury bonds. By the end of the day, 3-year ACGB yields had shed 2bps to 0.79% while 10-year and 20-year yields had each lost 5bps to 1.22% and 1.64% respectively.

Prices of cash futures contracts moved to harden expectations of another cut in the cash rate target. By the end of the day, February contracts implied a 46% chance of a 25bps rate cut, up from the previous day’s 42% while March contracts implied a 60% chance of another cut, up from 55%. May contracts had a 93% likelihood of a rate cut built in.

10 January 2020

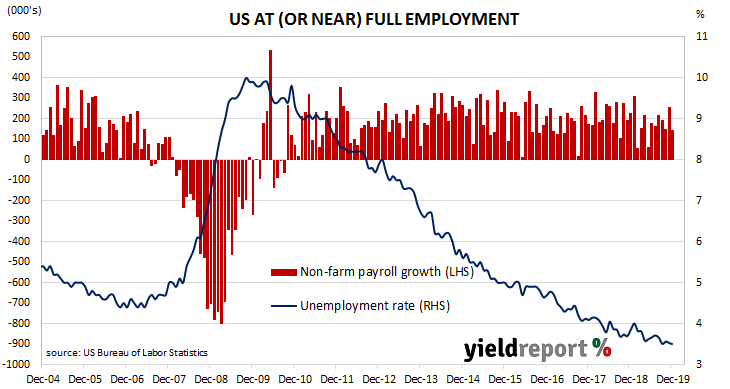

The US economy continues to produce more jobs despite being close to full employment. The unemployment rate has remained at or under 4% since April 2018 and the underemployment rate has been falling in trend terms. The latest employment report indicates the US economy is still producing jobs but not all the figures have been interpreted positively.

According to the US Bureau of Labor Statistics, the US economy created an additional 145,000 jobs in the non-farm sector in December, less than November’s revised increase of 256,000 and less than the 160,000 increase which had been expected. Employment figures for October and November were revised down by a total of 14,000.

December’s unemployment rate remained at November’s rate of 3.5%. The total number of unemployed decreased by 58,000 to 5.753 million while the total number of people who are either employed or looking for work fell by 211,000 to 164.556 million.

US Treasury yields finished lower on the day. By the close of business, 2-year Treasury yields had slipped 1bp to 1.57%, the 10-year yield had lost 4bps to 1.82% and 30-year yields had shed 5bps to 2.28%.

In terms of likely US monetary policy, according to federal funds futures contracts the probability of a rate cut in the March quarter of 2020 remained slim. The implied likelihood of a 25bps cut at the January meeting of the FOMC remained unchanged at zero while a move in March is also viewed as highly unlikely at just under 4%.

10 January 2020

Growth figures of domestic retail sales have been declining since 2014 and they reached a low-point in September 2017 when they registered an annual growth rate of just 1.5%. They then began increasing for about a year, only to stabilise at around 3.0% to 3.5% through late 2018 before trending lower through 2019. However, the latest figures are not in keeping with recent months.

According to the latest ABS figures, total retail sales jumped by 0.9% in November on a seasonally-adjusted basis, more than double the expected increase of +0.4% and well above October’s 0.1% increase after it was revised up from zero. On an annual basis, retail sales increased by 3.2%, as compared to October’s figure of 2.3%.

Westpac senior economist Matthew Hassan said, “Retail sales came in much stronger than expected in November on what looks to be a combination of ‘Black Friday’ sales and some delayed effect from policy stimulus measures.”

US Treasury yields had had a quiet night and bond yields in the domestic market moved in a similar vein. By the end of the day, 3-year, 10-year and 20-year ACGB yields had all inched up 1bp to 0.81%, 1.27% and 1.69% respectively.

Prices of cash futures contracts moved to soften expectations of a rate cut in the first half of 2020, although the change was minor. February contracts implied a 42% chance of a 25bps rate cut, down from the previous day’s 53% while March contracts implied a 55% chance of another cut, down from 69%. A full 25bps rate cut is now not completely factored in until June.

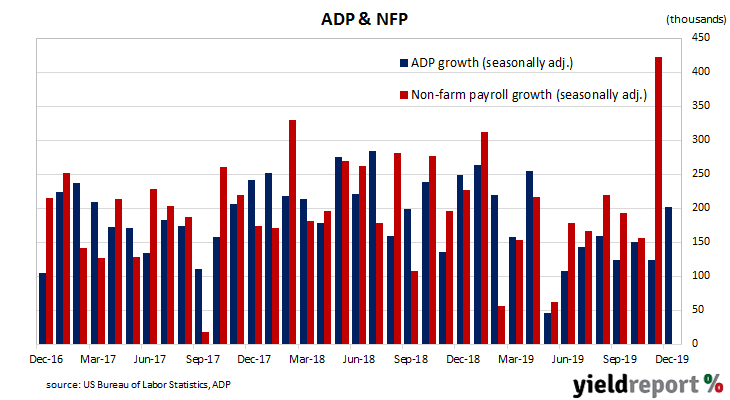

08 January 2020

The ADP National Employment Report is published monthly by the ADP Research Institute. The report provides an estimate of US non-farm employment in the private sector. Since the report began to be published in 2006, its total private sector non-farm employment figures have exhibited a high correlation with the Bureau of Labor Statistics (BLS) non-farm payroll figures which are typically published a day or two later.

The latest figures indicate private sector employment grew by 201,660 in December, well above the expected figure of 160,000 and almost double November’s revised increase of 124,000.

NAB economist Tapas Strickland described the figures as “still suggestive of a robust labour market.”

US Treasury yields increased along the curve. By the end of the day, 2-year Treasury bond yields had gained 3bps to 1.58% while 10-year and 30-year yields had each increased by 5bps to 1.87% and 2.36% respectively.

In terms of likely US monetary policy, according to federal funds futures contracts the probability of another rate cut at January’s FOMC meeting remained at zero. The implied likelihood of a 25bps cut at the March meeting also fell to zero, having been seen as a remote possibility at the end of the previous day.