19 November 2019

The Fed made its first interest rate increase of this cycle in December 2015. It then raised the federal funds target range another eight times over three years before it began making a series of cuts in what Federal Reserve chief Jerome Powell described as a “mid-cycle adjustment”. The most recent of these three rate cuts was at the FOMC’s meeting at the end of October. The publication of the minutes from that meeting suggests the period of rate cuts may have come to an end. “With regard to monetary policy beyond this meeting, most participants judged that the stance of policy, after a 25 basis point reduction at this meeting, would be well calibrated to support the outlook of moderate growth, a strong labor market, and inflation near the Committee’s symmetric 2 percent objective and likely would remain so as long as incoming information about the economy did not result in a material reassessment of the economic outlook.” In other words, current interest rate settings are appropriate in the absence of data which would change the FOMC’s view.

The publication of the minutes from that meeting suggests the period of rate cuts may have come to an end. “With regard to monetary policy beyond this meeting, most participants judged that the stance of policy, after a 25 basis point reduction at this meeting, would be well calibrated to support the outlook of moderate growth, a strong labor market, and inflation near the Committee’s symmetric 2 percent objective and likely would remain so as long as incoming information about the economy did not result in a material reassessment of the economic outlook.” In other words, current interest rate settings are appropriate in the absence of data which would change the FOMC’s view.

ANZ economist Hayden Dimes said the Fed was concerned about economic conditions despite its apparent intention to keep rates unchanged. “Fed officials still viewed downside risks as elevated but signalled that rates would stay on hold until officials see a ‘material change in their economic outlook.’

US Treasury bond yields finished the day lower. By the end of the day, US 2-year Treasury yields had lost 2bps to 1.57% while 10-year and 30-year yields had each fallen by 4bps to 1.75% and 2.21% respectively.

19 November 2019

The RBA kept its official cash rate target steady at its November board meeting, largely as expected. The rate at which the RBA wishes banks to lend to each other in the market for unsecured overnight loans remained unchanged at 0.75%.

Around February of this year, the RBA began to publicly move away from a tightening bias. By April, “there was not a strong case for a near-term adjustment in monetary policy” and, by May, the transformation to an easing bias had been completed. In June, a 25bps rate cut was announced. Additional cuts followed in July and October. The minutes of the November meeting have now been released and the board’s deliberations focussed on the RBA’s economic forecasts as well as past and future rate cuts.

The minutes of the November meeting have now been released and the board’s deliberations focussed on the RBA’s economic forecasts as well as past and future rate cuts.

The RBA’s forecasts for GDP growth, unemployment and inflation took up much of the discussions regarding domestic economic conditions. While some discussion of these topics is hardly unusual, this month’s minutes devoted significantly more time to these topics. The minutes clearly state the Board’s expectations had not been met.

“Over the year since the November 2018 forecasts, GDP growth had been much weaker than expected. Inflation had also been lower than forecast.” The culprit was the “the extent and breadth of the spillovers from the housing downturn…” The RBA admitted it had underestimated the housing downturn’s effects on “consumption, household income, dwelling investment and inflation…” and their flow on effects for growth and inflation. However, employment growth had been strong despite lower-than expected GDP growth and “the unemployment rate had been only marginally higher than forecast.”

15 November 2019

The Federal Reserve’s industrial production (IP) index measures real output from manufacturing, mining, electricity and gas company facilities located in the United States. These sectors are thought to be sensitive to consumer demand and so some leading indicators of GDP use industrial production figures as a component. A month ago, IP figures had suggested some chance of an end to a recent run of months in which US production has gone backwards. Figures from the latest report indicated that view was probably premature.

According to the latest figures released by the Fed, US industrial production dropped by 0.8% in October, less than the 0.3% fall which had been expected and more than double September’s 0.3% fall. On an annual basis, growth in industrial production went further into reverse from September’s rate of -0.1% to -1.1%.

ANZ economist Adelaide Timbrell said, “The GM strike is evident in the data, but the decline was not limited to that auto sector alone. Ex-vehicle and parts-manufacturing production was down 0.2%.”

Treasury bond yields barely moved on the day, perhaps supported by October’s retail sales figures which were also published. By the close of business, the 2-year US Treasury yield remained unchanged at 1.61%, the 10-year rate had crept up 1bp to 1.83% and the 30-year yield remained unchanged at 2.31%.

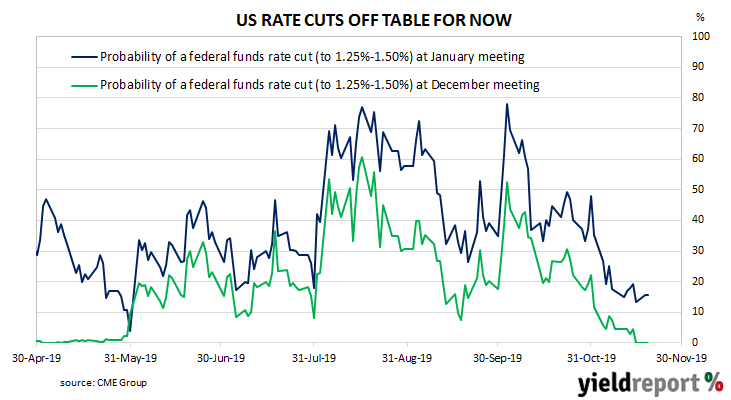

The reaction in the market for federal funds futures was not quite as restrained but it was not dramatic, either. The implied probability of a 25bps rate cut at the FOMC’s December meeting fell from 4% to zero while the likelihood of a January cut fell from 19% to 13%.

15 November 2019

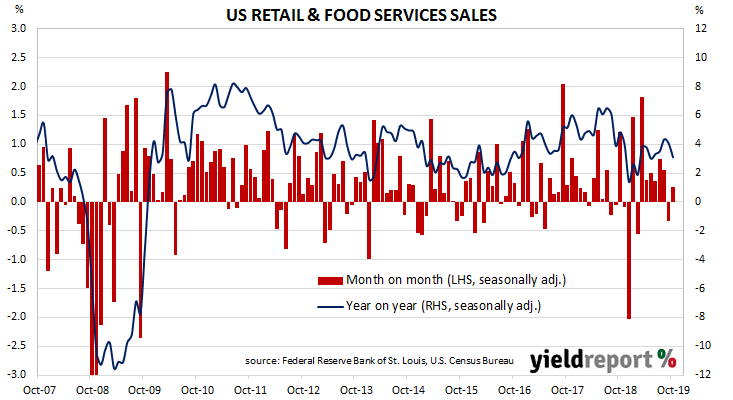

US retail sales had been trending up since late 2015 but, beginning in late 2018, a series of weak or negative monthly results led to a drop-off in the annual growth rate which brought the annual rate below 2.0% by the end of the year. After an unsteady start to 2019, subsequent months’ figures have produced a recovery and expansion which prevailed into the third quarter of the year. However, recent month’s figures have produced some doubts as to the trend’s sustainability.

According to the latest “advance” sales numbers released by the US Census Bureau, total retail sales grew by 0.3% in October, more than the +0.2% increase which had been expected and a marked turnaround from September’s 0.3% contraction. On an annual basis, the growth rate slowed to 3.1% from September’s rate of 4.1%.

Westpac described the sales figures as “relatively solid and close to estimates.”

Treasury bond yields barely moved on the day, although September’s industrial production figures were released by the Federal Reserve on the same day. By the close of business, the 2-year US Treasury yield remained unchanged at 1.61%, the 10-year rate had crept up 1bp to 1.83% and the 30-year yield remained unchanged at 2.31%.

Treasury bond yields barely moved on the day, although September’s industrial production figures were released by the Federal Reserve on the same day. By the close of business, the 2-year US Treasury yield remained unchanged at 1.61%, the 10-year rate had crept up 1bp to 1.83% and the 30-year yield remained unchanged at 2.31%.

The reaction in the market for federal funds futures was also subdued. The implied probability of a 25bps rate cut at the FOMC’s December meeting fell from 4% to zero while the likelihood of a January cut fell from 19% to 13%.

14 November 2019

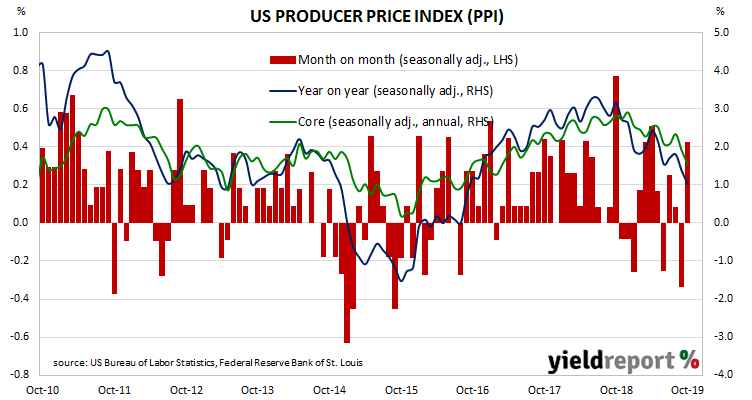

Around the end of 2018, the annual rate of prices received by producers began a downtrend which then continued through 2019. Recent figures had suggested this trend may have finished, although the latest figures have retained some ambiguity in this regard.

The figures from October have been published by the Bureau of Labor Statistics and they indicate producer prices increased by 0.4% after seasonal adjustments. The result was above the 0.3% increase which had been expected and a noticeable turnaround from September’s -0.3%. However, on a 12-month basis, the rate of producer price inflation after seasonal adjustments slowed to 1.0% after recording 1.4% in September and 1.8% in August.

“Core” PPI inflation increased by 0.3%, which is a marked turnaround from September’s comparable figure of -0.3%. Its annual rate dropped for a second consecutive month, this time from 1.9% to 1.5%.

US Treasury bond yields finished lower. By the end of the day, US 2-year Treasury yields had lost 3bps to 1.61%, the 10-year yield had fallen by 7bps to 1.82% and the 30-year yield finished 6bps lower at 2.31%.

13 November 2019

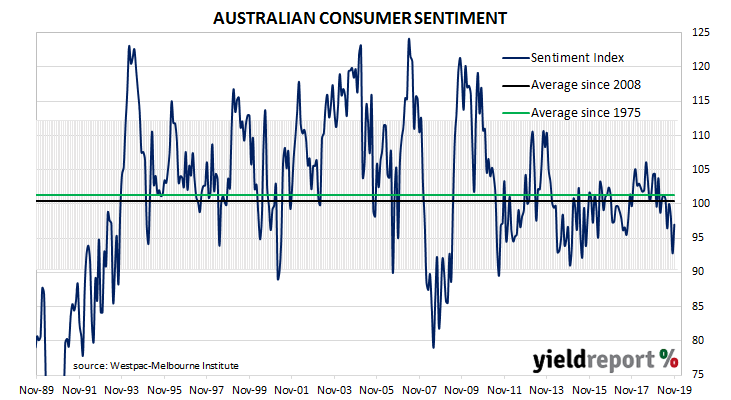

After a lengthy divergence between consumer sentiment and business confidence in Australia which began in 2014, the two sectors converged again around July 2018. Since then, confidence has deteriorated and both measures have been around or under neutral levels in recent months. The prospect of reduced international trade and high household debt levels have compelled both the business and household sectors to act cautiously.

According to the latest Westpac-Melbourne Institute survey conducted in early November, average household optimism has recovered back to almost-neutral levels. The Consumer Sentiment Index rebounded from 92.8 to 97.0, almost completely reversing the previous survey’s plunge and recovering back to just a little below the long-term average reading of just over 101. Any reading above 100 indicates the number of consumers who are optimistic is greater than the number of consumers who are pessimistic.

Westpac chief economist Bill Evans said, “The pattern of confidence falling in response to a rate cut and recovering when the RBA remains on hold repeats what we saw earlier in the year…” He said the bounce supported the view households tend to be “somewhat unnerved by the announcement of low rates and media controversy around the banks’ responses.”

The figures came out on the same day as the latest wage price index report but neither one made much of an impact on local Treasury bond yields. By the end of the day, the yield on 3-year ACGBs had lost 2bps to 0.83%, the 10-year yield had slipped 1bp to 1.28% while the 20-year yield finished unchanged at 1.69%.

13 November 2019

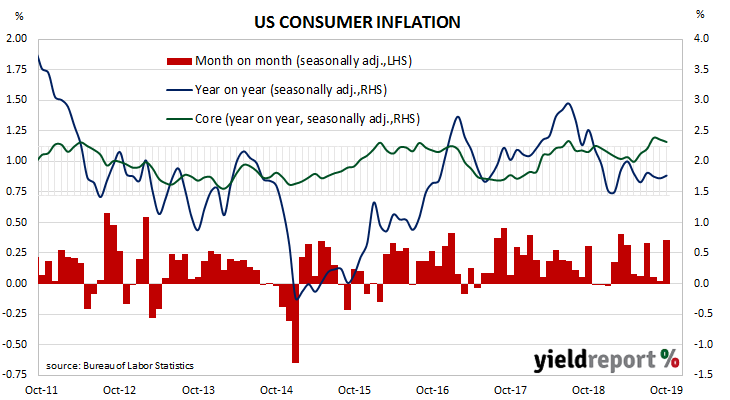

The annual rate of US consumer inflation halved from nearly 3% in the period from July 2018 to February 2019 and then subsequently fluctuated in a range from 1.5% to 2.0%. However, “headline” inflation is known to be volatile and so references are often made to “core” inflation figures for purposes of analysis. This measure has mostly ranged between 1.7% and 2.3% in recent years and it has not been below 2.0% since early 2018.

The latest consumer price index (CPI) figures released by the Bureau of Labor Statistics indicated seasonally-adjusted consumer prices increased by +0.4% on average in October, more than the +0.3% increase which had been expected and well in excess of September’s flat result. On a 12-month basis, the inflation rate ticked up from September’s annual rate of 1.7% to 1.8%.

NAB economist NAB Tapas Strickland said the report “suggests core inflation in the US remains contained” while ANZ Head of Australian Economics David Plank said, “There is no compelling evidence that tariff rises have been passed on to consumers.”

Core inflation, a measure of inflation which strips out the volatile food and energy components of the index, increased on a seasonally-adjusted basis by +0.2% for the month, in line with expectations and more than September’s +0.1% increase. However, the annual rate slipped from 2.4% to 2.3%.

13 November 2019

As with other countries’ measures of industrial production, Eurostat’s industrial production index measures the output and activity of industrial sectors in euro-zone countries in aggregate. Following a recession in 2009/2010 and the resultant European debt-crisis of 2010-2012, euro-zone industrial production began to recover until a peak was reached four years later in early-2016. Growth rates then slowed through the rest of 2016, accelerated during 2017 and then began a steady slowing which has lasted through to late-2019.

According to the latest figures released by Eurostat, euro-zone industrial production increased by a seasonally-adjusted 0.1% in September, higher than the 0.3% fall which had been expected but also noticeably lower than August’s +0.4%. On an annual basis, seasonally-adjusted growth in industrial production improved from August’s revised rate of -2.6% to -1.9%* in September.

ANZ Head of Australian Economics David Plank said, “The weakness was in intermediate goods production, suggesting that the pipeline of demand remains soft.”

Industrial production growth rates varied significantly from country to country but it contracted in three of the euro-zone’s four largest economies. German industrial production contracted by 1.0% while in Spain and Italy the comparable figures were -0.9% and -0.4% respectively. French industrial production expanded by +0.3%.

12 November 2019

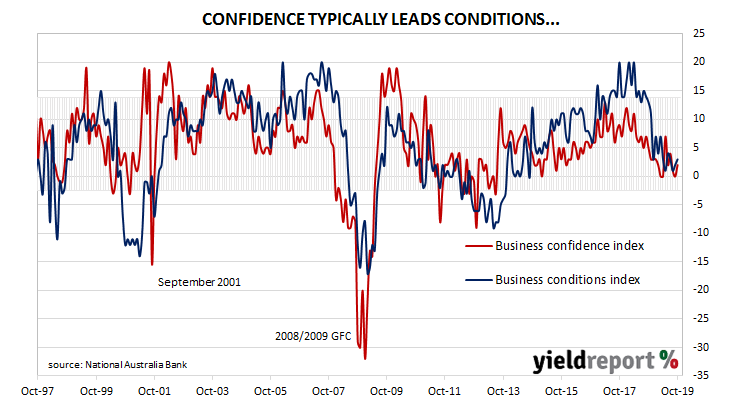

Australian business conditions were robust in the first half of 2018 and a cyclical-peak was reached in April of that year. Although they remained well above average for some months, readings began to slip and by the end of 2018, they had dropped to below-average levels. Forecasts of a slowing domestic economy began to emerge in the first half of 2019 and recent readings from NAB’s monthly surveys have largely been consistent with those forecasts.

According to NAB’s latest monthly business survey of 400 firms conducted in the last week of October, business conditions continued to bump along at below-average levels. Since late 2018, NAB’s conditions index bounced between 3, which is on the low side of normal and 7, which is about average. The index then broke through this lower bound in May 2019. The latest reading registered 3, a modest rise from September’s reading of 2. The latest reading of NAB’s confidence index moved largely in line with its condition index. It improved from September’s reading of 0 to 2 in October, although it is still well below its long-term average reading of 6. Typically, NAB’s confidence index leads the conditions index by approximately one month, although some divergences appear from time to time.

The latest reading of NAB’s confidence index moved largely in line with its condition index. It improved from September’s reading of 0 to 2 in October, although it is still well below its long-term average reading of 6. Typically, NAB’s confidence index leads the conditions index by approximately one month, although some divergences appear from time to time.

ANZ senior economist Catherine Birch said, “While there is still a long way to go before we can consider the private sector in recovery, there were some tentatively positive signs.” However, she also noted “the business sector has not been as responsive to monetary and fiscal stimulus as we would like”, given the capacity utilisation rate was “largely flat”, as was NAB’s employment index.

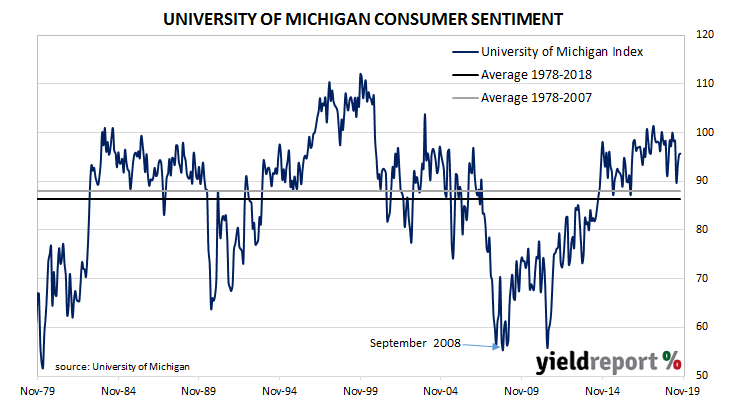

08 November 2019

US consumer confidence started 2019 at well above average levels in a longer-term context, although readings were markedly lower than those which had been typical of most of the previous year. Since then, surveys have generally indicated US households maintained historically-high levels of confidence except for two short-lived plunges; one at the very start of the year and one in August.

The latest survey conducted by the University of Michigan indicates the average confidence level of US households has increased for a third consecutive month, although the improvement was very, very minor. The University’s preliminary reading from its Index of Consumer Sentiment increased from October’s final figure of 95.5 to 95.7 in November, just ahead of the consensus figure of 95.5.

The University’s Surveys of Consumers chief economist, Richard Curtin, said, “Consumers did voice a slightly more positive outlook for the economy, which was offset by a slightly less favourable outlook for their own personal finances.” Tariffs remained a topic on respondents’ minds while impeachment proceedings were irrelevant at this stage.

US Treasury yields finished higher on the day. By the close of business, 2-year Treasury yields were unchanged at 1.67% but 10-year had gained 2bps to 1.94% and 30-year yields had increased by 3bps to 2.43%.