08 November 2019

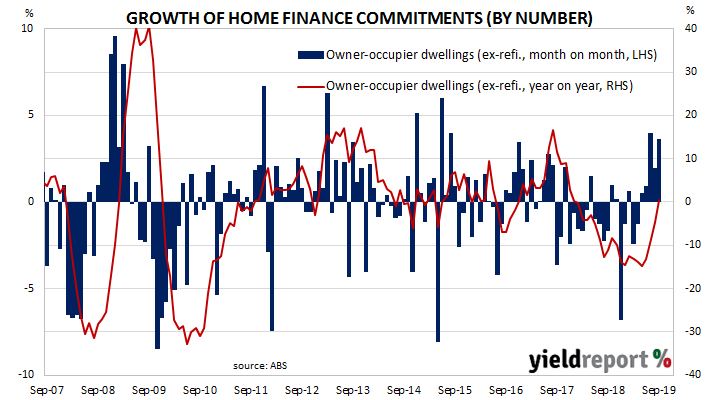

Since late 2017/early 2018, a very clear downtrend has been evident in the monthly figures of both the number and value of home loan commitments. This downtrend lasted through to June 2019 when the RBA cut its cash rate target from 1.50% to 1.25%. The RBA then reduced its target again in July and the number of approvals figures began to recover.

September’s housing finance commitment figures have now been released and the total number of loan commitments to owner-occupiers increased by 1.4%, more than the expected 1.1% increase but less than August’s revised figure of +2.7%. On an annual basis, the growth rate of loan commitments improved for a fourth consecutive month, from August’s revised figure of -3.4% to -0.4%. When “re-financings” are removed, the number of loan commitments increased by 3.6% over the month and by 0.5% when compared to September 2018’s figure.

Westpac senior economist Matthew Hassan said, “The September housing finance approvals showed a much stronger-than-expected rise in owner-occupier loans but a pull-back in the value of investor loan approvals leaving the total value of approvals broadly in line with expectations.”

US Treasury bond yields increased noticeably overnight and Australian Commonwealth Government bond yields followed. By the end of the day, the yield on 3-year ACGBs had gained 4bps to 0.89%, the 10-year yield had jumped up by 8bps to 1.30% and the 20-year yield finished 9bps higher at 1.70%.

05 November 2019

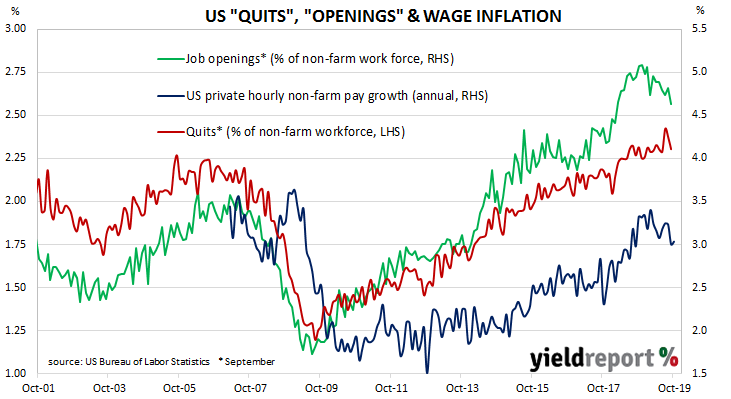

The quit rate as a percentage of total US non-farm employment increased slowly but steadily from the end of the GFC. It peaked in August 2018, stabilised and then remained largely unchanged through the remainder of 2018 before it hit a new peak in July 2019.

Figures released as part of the most recent JOLTS report show the quit rate has slowed from the record levels reached in July and August. 2.3% of the non-farm workforce left their jobs voluntarily in September, down from August’s revised figure of 2.4%. The slightly-lower rate marked a return the same 2.3% growth rate which was present in each of the months from June 2018 through to June 2019.

Quit numbers were highest in the professional/business services, durable goods and non-durable goods sectors while the accommodation/food services, retail trade and real estate/rental/leasing sectors recorded the largest falls. Overall, the total number of quits for the month decreased from August’s revised figure of 3.601 million to 3.498 million in September. August’s total quits were revised up by 75,000.

Total job openings fell, even before August’s figure was revised up by 250,000. Total vacancies during September decreased by 277,000 from August’s revised figure of 7.301 million to 7.024 million, driven by large reductions in the “health care/social assistance” and retail trade sectors. Additional openings in the transportation, warehousing and utilities sector and information sectors provided some modest offsetting effects. Overall, 10 out of 19 sectors experienced fewer job openings than in the previous month.

04 November 2019

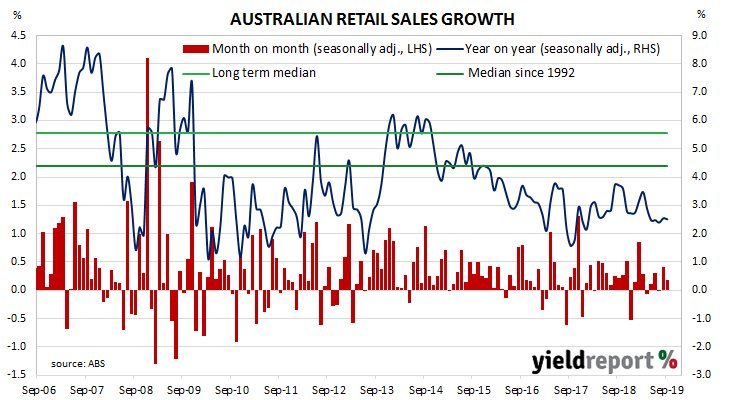

Growth figures of domestic retail sales have been declining since 2014 and they reached a low-point in September 2017 when they registered a growth rate of just 1.5%. They then began increasing for about a year, only to stabilise at around 3.0% to 3.5% through late 2018. 2019 has produced a number of low-growth months along with the odd surprisingly strong result, lowering the annual growth rate further.

According to the latest ABS figures, total retail sales increased by +0.2% in September on a seasonally-adjusted basis, half the expected increase of +0.4% and less than August’s 0.4% increase. On an annual basis, retail sales increased by 2.5%, the same as August’s comparable figure after it was revised down from 2.6%.

ANZ economist Adelaide Timbrell said, “Tax cuts and rate cuts were no match for household challenges such as high household debt, rising cost of living…and pessimism about the economy.” Westpac senior economist Matthew Hassan was equally gloomy, saying the report “disappointed in every respect…”

US Treasury yields had increased on Friday night, lending support for higher yields in the domestic market on Monday when the Inflation Gauge figures came out. However, September’s retail sales report was also released on the same day and so the individual effect of each report is difficult to ascertain. By the end of the day, 3-year, 10-year and 20-year ACGB yields had all increased by 3bps to 0.86%, 1.21% and 1.61% respectively.

04 November 2019

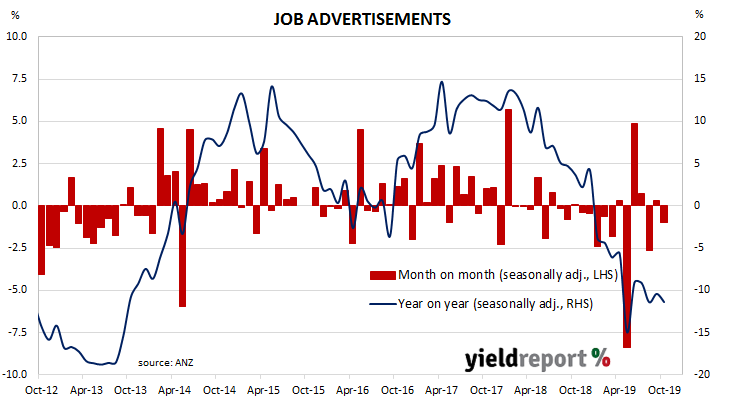

From mid-2017 onwards, year-on-year growth rates in the total number of Australian job advertisements consistently exceeded 10%. That was until mid-2018 when the annual growth rate fell back markedly and then continued to deteriorate for the remainder of 2018 and through 2019.

According to the latest ANZ figures, total advertisements fell by 1.0% in October on a seasonally-adjusted basis, an unfortunate turnaround from September’s modest 0.3% increase. On a 12-month basis, total job advertisements were 11.4% lower than the same month last year, undoing the small improvement which had taken place in September when the comparable annual figure had improved to -10.4%.

ANZ senior economist Catherine Birch contrasted the survey which “has been pointing to a material slowdown in employment growth for some time” with “remarkably resilient” employment growth. US Treasury yields had increased on Friday night, lending support for higher yields in the domestic market on Monday when the figures came out. However, September’s retail sales report was also released on the same day and so the individual effect of each report is difficult to ascertain. By the end of the day, 3-year, 10-year and 20-year ACGB yields had all increased by 3bps to 0.86%, 1.21% and 1.61% respectively.

US Treasury yields had increased on Friday night, lending support for higher yields in the domestic market on Monday when the figures came out. However, September’s retail sales report was also released on the same day and so the individual effect of each report is difficult to ascertain. By the end of the day, 3-year, 10-year and 20-year ACGB yields had all increased by 3bps to 0.86%, 1.21% and 1.61% respectively.

04 November 2019

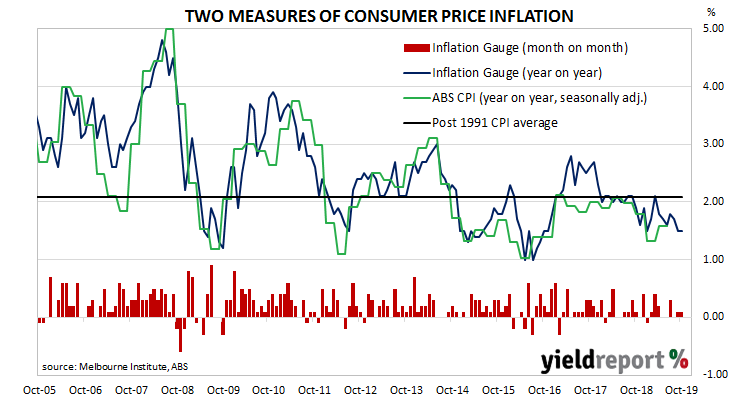

The RBA’s stated objective is to achieve an inflation rate of between 2% and 3%, “on average, over time.” Since the GFC, Australia’s inflation rate has been trending lower and lower and it has been below the RBA’s target band for some years now. Despite the RBA’s desire for a higher inflation rate, attempts to accelerate inflation through record-low interest rates have failed so far. The latest unofficial measurement of consumer inflation has provided any indication that story has changed.

The Melbourne Institute’s latest Inflation Gauge index increased by 0.1% in October following a 0.1% increase in September and a flat result in August. On an annual basis, the index increased by 1.5%, the same rate as in September.

US Treasury yields had increased on Friday night, lending support for higher yields in the domestic market on Monday when the Inflation Gauge figures came out. However, September retail sales and the ANZ’s Job Ads figures were also released on the same day and so the individual effect of each report is difficult to ascertain. By the end of the day, 3-year, 10-year and 20-year ACGB yields had all increased by 3bps to 0.86%, 1.21% and 1.61% respectively.

01 November 2019

US purchasing managers’ indices (PMIs) have been sliding since August 2018, albeit from elevated levels. After reaching a cyclical peak in September 2017, manufacturing PMI readings went sideways for a year before they started a downtrend. The latest reading represents a turnaround but calling an end may be premature.

US manufacturing activity rebounded to some extent after having slowed for six consecutive months. According to the latest Institute of Supply Management (ISM) survey, its Purchasing Managers Index recorded a reading of 48.3, up from September’s reading of 47.8 but less than the market’s expected figure of 49.0. The average reading since 1948 is 52.9 and any reading below 50 implies a contraction.

The ISM’s Tim Fiore said, “Overall, sentiment this month remains cautious regarding near-term growth.” Westpac’s Finance AM team described the report as “disappointing”, noting falls in the “prices paid” and “production” sub-indices. US Treasury yields increased along the curve but more so at the short end. By the end of the day, 2-year Treasury bond yields had gained 4bps to 1.56%, the 10-year yield had increased by 2bps to 1.71% and the 30-year yield finished 1bp higher at 2.19%.

US Treasury yields increased along the curve but more so at the short end. By the end of the day, 2-year Treasury bond yields had gained 4bps to 1.56%, the 10-year yield had increased by 2bps to 1.71% and the 30-year yield finished 1bp higher at 2.19%.

01 November 2019

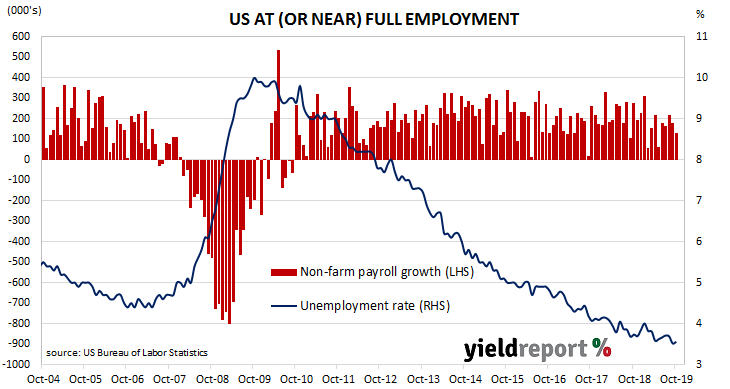

The US economy continues to produce more jobs despite being close to full employment. The unemployment rate has remained at or under 4% since April 2018 and the underemployment rate has been falling in trend terms. The latest employment report indicates the US economy is still producing jobs and luring people back in the workforce.

According to the US Bureau of Labor Statistics, the US economy created an additional 128,000 jobs in the non-farm sector in October, significantly fewer than September’s revised increase of 180,000 but more than the 90,000 increase which had been expected. Employment figures for August and September were also revised up by a total of 95,000.

The unemployment rate increased from September’s rate of 3.5% to 3.6% in October as the total number of unemployed increased by 86,000 to 5.855 million while the total number of people who are either employed or looking for work increased by 327,000 to 164.365 million.

According to NAB currency strategist Rodrigo Catril, the report was a ”good one, allaying fears of potential weakness emanating from US-China trade tensions and its impact on the US manufacturing sector.” He pointed to the strike by GM workers and other factors as having temporary effect on the employment figures and noted the increase in the participation rate as another factor which raised October’s unemployment rate.

31 October 2019

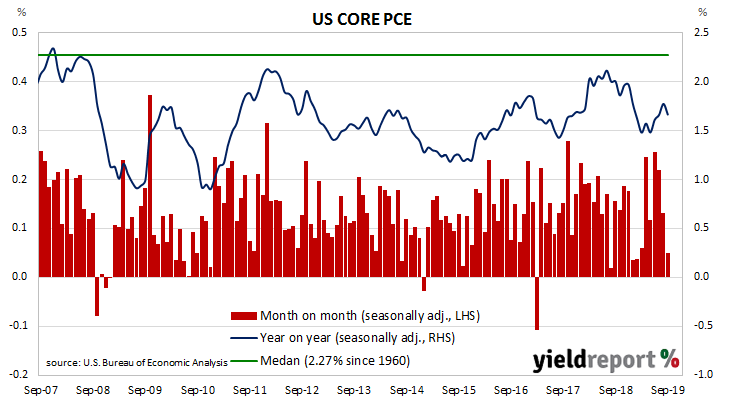

One of the US Fed’s favoured measures of inflation is the change in the core personal consumption expenditures (PCE) price index. After hitting the Fed’s target at 2.0% in mid-2018, the annual rate then hovered in a range between 1.8% and 2.0% through to the end of 2018 before dropping in the first quarter of 2019. It then hovered around 1.5% or just above it for some months before moving higher in the last few months.

The latest figures have now been published by the Bureau of Economic Analysis as part of the September personal income and expenditures report. Core PCE inflation was flat for the month, largely in line with expectations but less than August’s +0.1%. On a 12-month basis, the core PCE inflation rate slipped back from August’s 1.8% to 1.7%.

US Treasury yields finished the day a little higher and more so at the front of the curve. By the end of the day, 2-year yields had gained 4bps to 1.56%, 10-year yields had increased by 2bps to 1.71% and 30-year yields finished 1bp higher at 2.19%.

31 October 2019

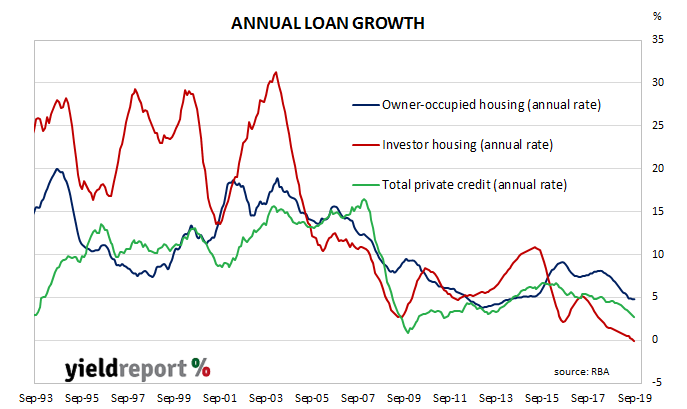

The pace of lending to the non-bank private sector by financial institutions in Australia has been trending down since October 2015. It appeared to have stabilised in the September quarter of 2018 but then subsequent credit figures put paid to that idea. Despite some optimism emerging in the housing market following the re-election of the Coalition Government in May, lending figures have continued to slow.

According to the latest RBA figures, private sector credit grew by 0.2% in September, in line with the expected figure and the same as August’s number. The annual growth rate continued its downward slide as, this time from August’s figure of 2.9% to 2.7% in September. Lending to business picked up a little but the owner-occupier segment remained subdued and investor lending moved into negative territory.

Westpac senior economist Andrew Hanlon said, “Housing finance is rising but housing credit growth has yet to stir, held back by the investor segment.” Local bond yields ignored largish falls of US Treasury yields in overnight trading and yields at the short end moved a little higher, although the latest home approvals report would have had some effect as well. By the end of the day, 3-year ACGB yields had gained 3bps to 0.81% while the 10-year yield remained unchanged at 1.14% and the 20-year yield had crept up 1bp to 1.54%.

Local bond yields ignored largish falls of US Treasury yields in overnight trading and yields at the short end moved a little higher, although the latest home approvals report would have had some effect as well. By the end of the day, 3-year ACGB yields had gained 3bps to 0.81% while the 10-year yield remained unchanged at 1.14% and the 20-year yield had crept up 1bp to 1.54%.

Prices of cash futures contracts moved to dampen expectations of another cut in the cash rate. By the end of the day, November contracts implied just a 5% chance of another 25bps rate cut, down from the previous day’s 7%. December contracts implied a 24% chance of a cut, down from 35% while February contracts implied another cut as a 49% likelihood, down from the previous day’s 65%.

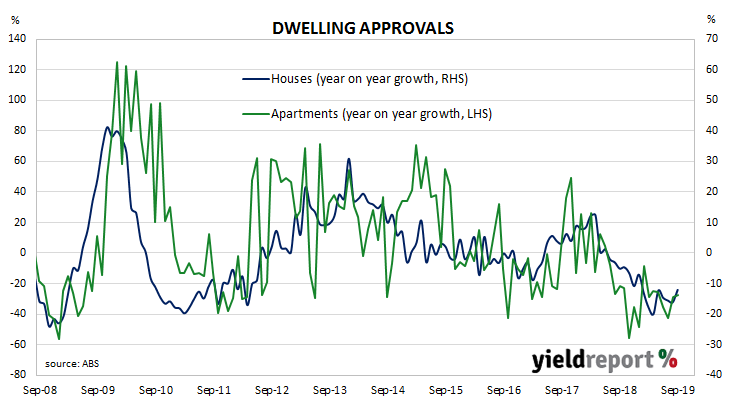

31 October 2019

Approvals figures for dwellings, that is, apartments and houses, have been heading south since mid-2018. As an indicator of investor confidence, falling approval figures represent a worrying signal, not just for the building sector but for the overall economy. There had been some expectation of a recovery in recent months and now that recovery may have arrived.

The Australian Bureau of Statistics has now released the latest figures from September and total residential approvals jumped by 7.6% on a seasonally-adjusted basis, more than the flat result which had been expected and a substantial improvement on August’s revised figure of -0.6%. However, on an annual basis, total approvals fell by 19.0%, although this annual figure is also an improvement on August’s comparable figure of -21.1% after revisions.

ANZ economist Hayden Dimes said, “Housing approvals surged in September following a sharp rise in approvals for units and decent pick up for houses. The rise in approvals for units was primarily in Queensland, ACT and South Australia.”

Local bond yields ignored largish falls of US Treasury yields in overnight trading and yields at the short end moved a little higher, although the latest private credit figures may have had some effect. By the end of the day, 3-year ACGB yields had gained 3bps to 0.81% while the 10-year yield remained unchanged at 1.14% and the 20-year yield had crept up 1bp to 1.54%.