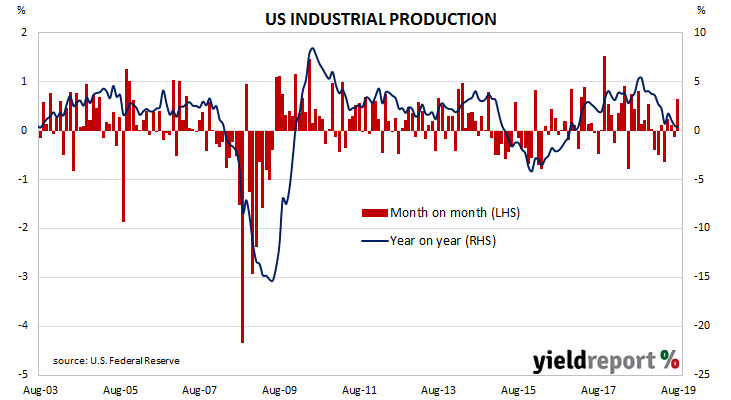

The Federal Reserve’s industrial production index measures real output from manufacturing, mining, electricity and gas company facilities located in the United States. These sectors are thought to be sensitive to consumer demand and so some leading indicators of GDP use industrial production figures as a component. Figures from the latest report suggest some chance of an end to a recent run of months in which US production has gone backwards.

According to the latest figures released by the Fed, US industrial production jumped by 0.6% in August, well in excess of the 0.2% increase which had been expected and a turnaround from July’s 0.1% fall after revisions. However, on an annual basis, growth in industrial production sped up to 0.5% from July’s revised rate of -0.1%.

ANZ economist Adelaide Timbrell said the figures would have some effect on Fed decision-making. “This result was considerably better than expected and will provide the Fed with something to mull over as it discusses rate cuts. Fed Chair Powell previously stated ‘a slowdown in manufacturing did not send a clear signal to the Fed’s rate-setting committee’ but this data does provide further evidence that the Fed doesn’t need to aggressively cut.”

NAB economist Tapas Strickland noted the presence of “one-off factors” which may have bolstered the final figures, such as the 2.6% increase in oil production which occurred during the month. He also pointed to the ISM’s Manufacturing Survey which “continues to point to dire conditions in the manufacturing sector.”

Treasury bond yields finished the day lower, ignoring the superficially strong figures. By the close of business, 2-year US Treasury yields had dropped by 4bps to 1.72% while 10-year and 30-year yields had each shed 5bps to 1.80% and 2.27% respectively.