01 August 2019

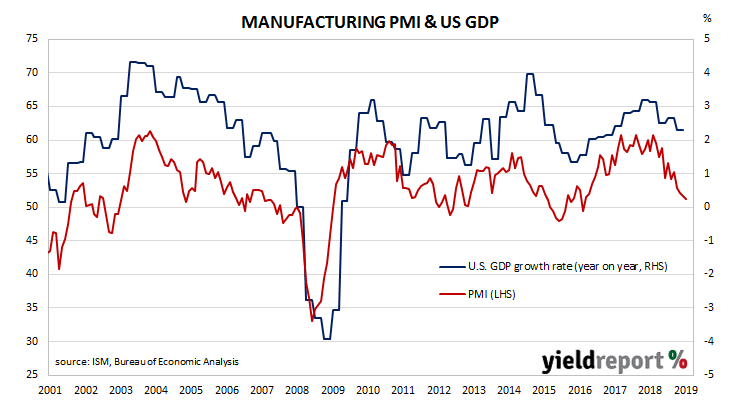

US purchasing managers’ indices (PMIs) have been sliding since August 2018, albeit from elevated levels. After reaching a cyclical peak in September 2017, manufacturing PMI readings went sideways for a year before they started a downtrend. The latest reading has continued this trend.

US manufacturing activity has slowed for a fourth consecutive month. According to the latest Institute of Supply Management (ISM) survey, its Purchasing Managers Index recorded a reading of 51.2, down from June’s reading of 51.7 and less than the market’s expected figure of 52.0. The average reading since 1948 is 52.9, so the latest reading has moved a little further under the long-term average. However, a reading above 50 still implies an expansion.

NAB economist Tapas Strickland noted a lack of consensus among respondents in the report. “Anecdotes in the report highlight very divergent conditions; a number noting ‘business is strong’, while an equal number note ‘weakness in end markets accelerating rapidly. Continuing to reduce production based on weakening demand and declining orders’.”

31 July 2019

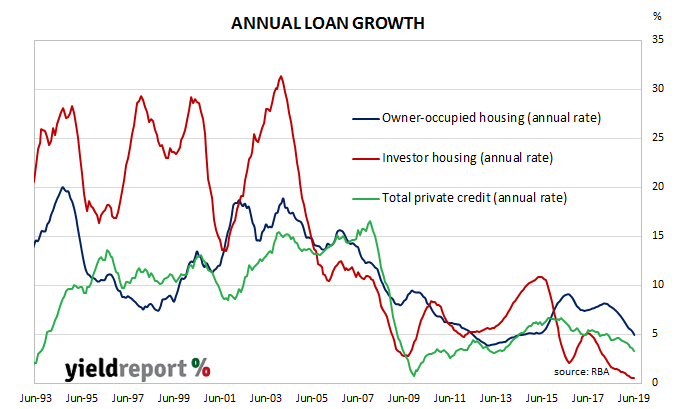

The pace of lending to the non-bank private sector by financial institutions in Australia has been trending down since October 2015. It appeared to have stabilised in the September quarter of 2018 but credit figures in the December quarter put paid to that idea. The latest figures show the pace of lending has continued to slow.

According to the latest RBA figures, private sector credit grew by 0.1% in June, the same rate as in May after revisions but noticeably below the +0.3% consensus estimate. The annual growth rate slipped from May’s figure of 3.6% to 3.3% as lending to business went back into reverse and lending to owner-occupiers slowed.

Andrew Hanlan, a Westpac senior economist, described the growth rate as “anaemic”, a result of a then-weak housing market, a flat business sector and prior to any rate cuts or tax breaks.. Financial markets reacted by sending local bond yields a little lower, although the June quarter CPI report was released at the same time and it would have had some effect. By the end of the day, 3-year ACGB yields had slipped 1bp lower to 0.78% while 10-year and 20-year yields had each lost 2bps to 1.19% and 1.65% respectively. The local currency increased and finished the afternoon session at around 68.90 US cents, having traded at around 68.75 US cents for most of the morning.

Financial markets reacted by sending local bond yields a little lower, although the June quarter CPI report was released at the same time and it would have had some effect. By the end of the day, 3-year ACGB yields had slipped 1bp lower to 0.78% while 10-year and 20-year yields had each lost 2bps to 1.19% and 1.65% respectively. The local currency increased and finished the afternoon session at around 68.90 US cents, having traded at around 68.75 US cents for most of the morning.

31 July 2019

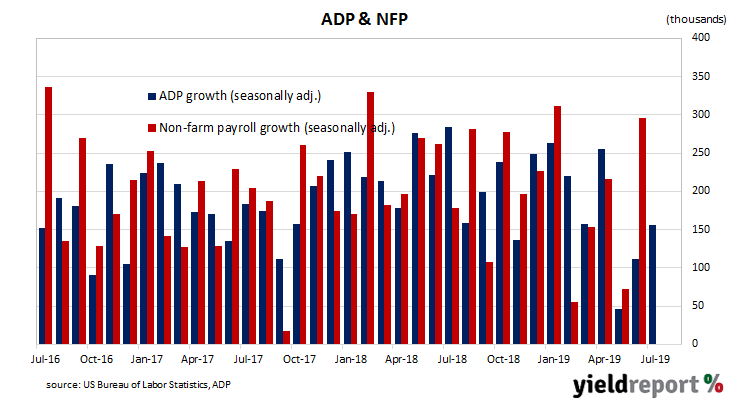

The ADP National Employment Report is published monthly by the ADP Research Institute. The report provides an estimate of US non-farm employment based in the private sector. Since the report began to be published in 2006, its total private sector non-farm employment figures have exhibited a high correlation with the Bureau of Labor Statistics (BLS) non-farm payroll figures.

The latest July figures indicate private sector employment grew by 155,600, just above the expected figure of 150,000 and an improvement on June’s revised increase of 111,900.

ANZ senior economist Felicity Emmett described the result as “reasonably strong”, indicative of “ongoing momentum in the labour market…” Westpac’s Finance AM team said the report cemented “expectations for a decent payrolls report later this week.”

30 July 2019

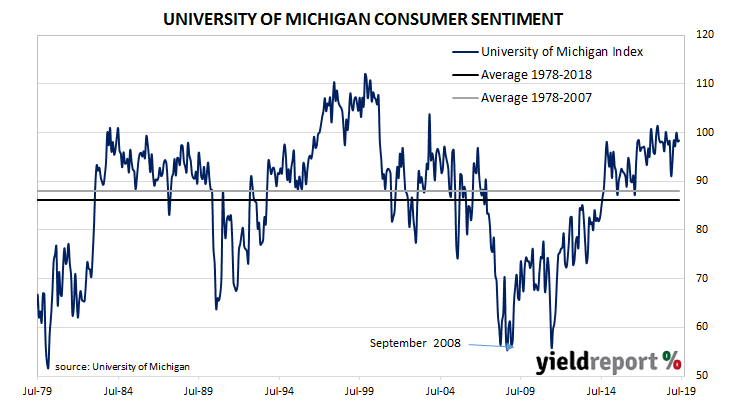

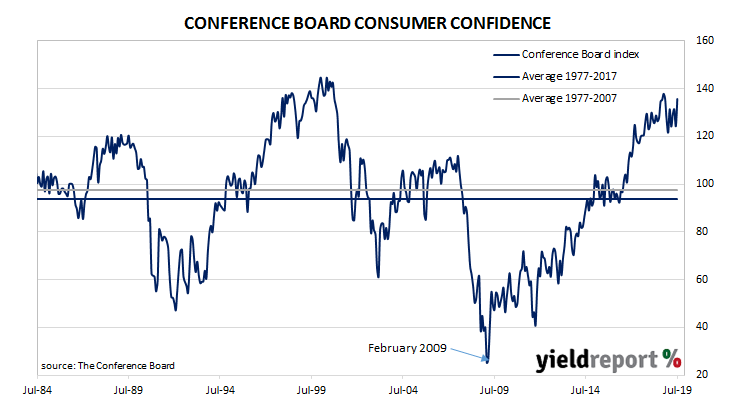

US consumer confidence collapsed in late 2007 as the US housing bubble burst and the US economy went into recession. By 2016, it had clawed its way back to neutral and then went from strength to strength until late 2018. Since then, measures of consumer confidence have oscillated within a fairly narrow band at historically high levels. This latest report had continued this pattern.

The latest Conference Board survey indicates US consumers have remained quite optimistic as trade and geo-political tensions have emerged and then dissipated. July’s reading came in at 135.7, a large increase above June’s final figure of 124.3 and not that far from its all-time high. Consumers’ views of present conditions and the short-term outlook with regards to the business environment and the labour market all improved.

A month ago, Lynn Franco, The Conference Board’s Director of Economic, had noted the effect of trade and tariff tensions and suggested any continuation was likely to “diminish consumers’ confidence”. In July, those fears faded. “Consumers are once again optimistic about current and prospective business and labour market conditions. In addition, their expectations regarding their financial outlook also improved.”

30 July 2019

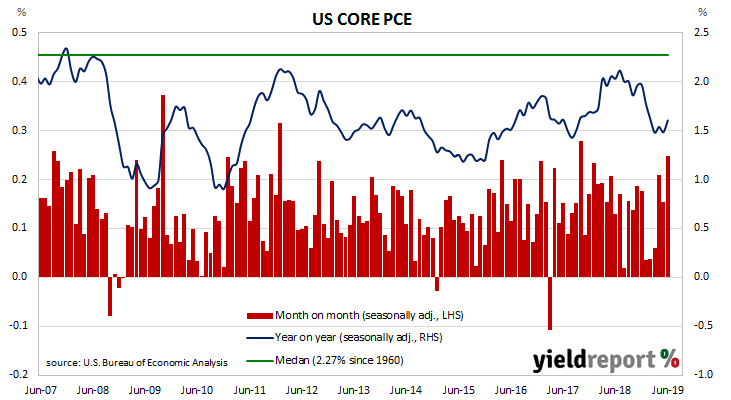

One of the US Fed’s favoured measures of inflation is the change in the core personal consumption expenditures (PCE) price index. After hitting the Fed’s target at 2.0% in mid-2018, the annual rate then hovered in a range between 1.8% and 2.0% through to the end of 2018 before dropping in the first quarter of 2019. Since then, the annual rate has stayed around 1.5%.

The latest figures have now been published by the Bureau of Economic Analysis as part of the June personal income and expenditures report. Core PCE inflation was +0.2% for the month, the same rate as in May and April but less than the 0.3% increase which had been expected. On a 12-month basis, the core PCE inflation rate ticked up to 1.6% after May’s annual rate was revised down to 1.5%.

ANZ economist Jack Chambers said, “The three-month annualised rate of core PCE is 2.4%, up from 0.6% in Q1 (the March quarter), signalling that the period of low inflation at the start of the year has passed.”

30 July 2019

Approvals figures for dwellings, that is apartments and houses, have been heading south since mid-2018. As an indicator of investor confidence, falling approval figures represent a worrying signal, not just for the building sector but for the overall economy. May’s figures offered some hope of a recovery and some economists thought at the time the bottom of the cycle may be approaching.

The Australian Bureau of Statistics has now released the latest building approval figures and they indicate any such recovery has not arrived just yet. Seasonally-adjusted, total approvals decreased by 1.2% in June, which is less than the market consensus figure of +0.2% and a deterioration from May’s revised figure of +0.3%. On an annual basis, total approvals fell by 25.6%, as compared to May’s comparable figure of -19.2% after revisions. ANZ economist Adelaide Timbrell expects a recovery to come. “The sentiment effects from the election, APRA credit easing and rate cuts are yet to flow through to building approvals data, but we still expect a recovery as a result of these changes.”

ANZ economist Adelaide Timbrell expects a recovery to come. “The sentiment effects from the election, APRA credit easing and rate cuts are yet to flow through to building approvals data, but we still expect a recovery as a result of these changes.”

30 July 2019

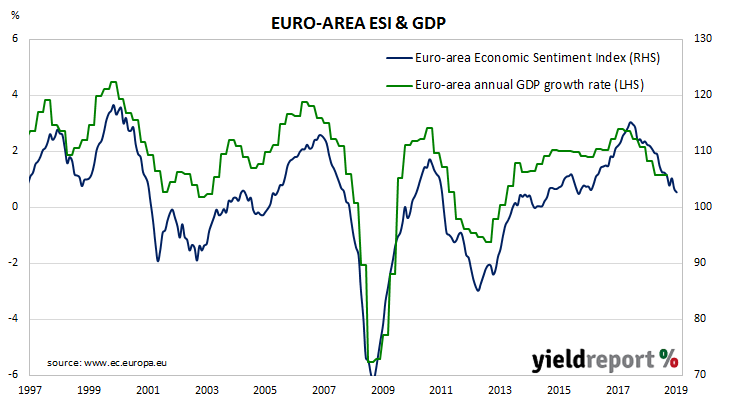

The European Commission’s Economic Sentiment Indicator (ESI) is a composite index comprised of five differently-weighted sectoral confidence indicators. It is heavily weighted towards confidence surveys from the business sector; the consumer confidence sub-index only accounts for 20% of the ESI. However, it has a good relationship with euro-area GDP, although not in the sense of a leading indicator.

The ESI recorded a reading of 102.7, down from June’s reading of 103.3 but above the market’s expected figure of 103.0. The average reading is 100, so the latest reading can be described as being just above average.

Overall sentiment in the euro-area deteriorated as four of the five sub-indices faltered and only the consumer confidence sub-index improved. On a geographical basis, the ESI rose in Italy and Spain, remained unchanged in France but it decreased noticeably in Germany.

26 July 2019

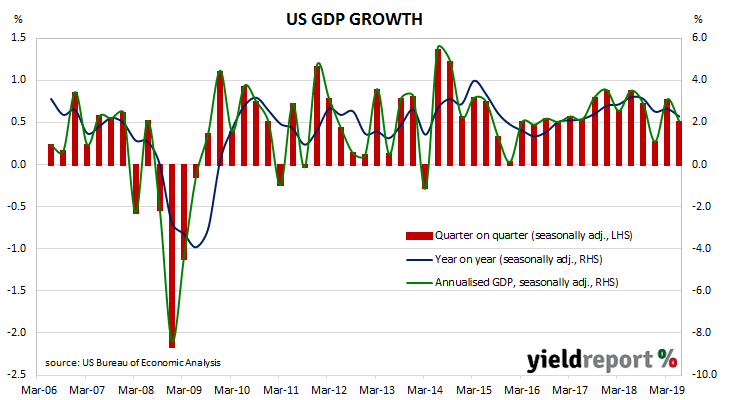

While the US has a historically low unemployment rate and strong GDP growth, bond yields suggest growth in the future will be less than what it is now. A rate cut is expected shortly as “insurance” against a softening external sector and the yield curve is flat or inverted depending on which measure one uses. However, quarterly US GDP figures have held up so far.

The US Commerce Department has now released June quarter “advance” GDP estimates and they indicate the US economy grew at an annualised rate of 2.1%. The growth figure was more than the 1.8% median of market estimates but a drop from the March quarter’s revised figure of 3.1%.

US Treasury bond yields slipped a little lower while the odds of a rate cut at the FOMC’s upcoming July meeting did not alter significantly. By the end of the day, 2-year, 10-year and 30-year yields had all slipped 1bp lower to 1.85%, 2.07% and 2.60% respectively. Federal funds futures still implied at least one 25bps rate reduction was coming, with a 25bps cut viewed as a 78% chance and a 50bps cut as a 22% chance.

US Treasury bond yields slipped a little lower while the odds of a rate cut at the FOMC’s upcoming July meeting did not alter significantly. By the end of the day, 2-year, 10-year and 30-year yields had all slipped 1bp lower to 1.85%, 2.07% and 2.60% respectively. Federal funds futures still implied at least one 25bps rate reduction was coming, with a 25bps cut viewed as a 78% chance and a 50bps cut as a 22% chance.

US GDP numbers are published in a manner which is different to most other countries; quarterly figures are compounded to give an annualised figure. In countries such as Australia and the UK, an annual figure is calculated by taking the latest number and comparing it with a figure from a year ago. The diagram below shows US GDP once it has been expressed in the normal manner, as well as the annualised figure.

23 July 2019

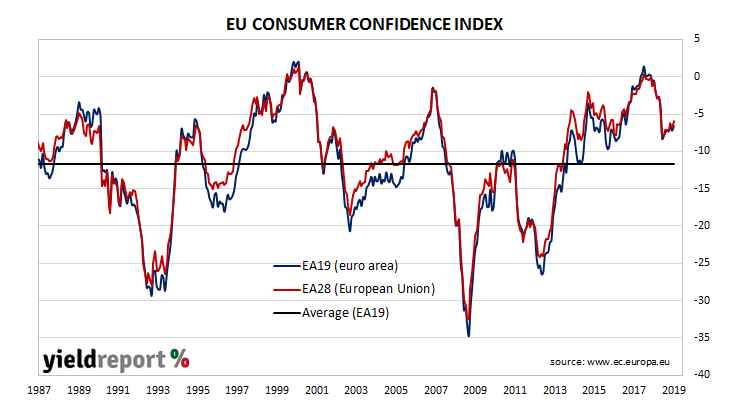

EU consumer confidence plunged during the GFC and again in 2011/12 during the European debt crisis. Since early 2014, it has been at average or above-average levels, rising to a cyclical peak at the beginning of 2018. However, it dropped back significantly in late 2018, albeit to still-elevated levels, at about the same time as doubts emerged over the US economy’s robustness. Since then, it has slowly been recovering and the latest survey of euro-zone households indicates this process has continued despite lower GDP growth forecasts and a relatively high unemployment rate which has been improving only slowly.

The latest survey conducted by the European Commission indicates EU household confidence has recovered from June’s fall. The latest reading produced a small gain in the EC’s Consumer Confidence indicator from June’s figure of -7.2 to -6.6 in July.

The reading easily beat the market’s expected figure of -7.1 but it had little effect on European bond yields. By the end of the day, UK 10-year gilts yields had shed 2bps to 0.69% while German and French 10-year yields had both slipped 1bp to -0.35% and -0.09% respectively.

19 July 2019

US consumer confidence had started 2019 at well above average levels in a longer-term context, although it was markedly lower than the more buoyant readings which typified most of 2018. After rebounding from the falls of January and February, US households have pretty much maintained a historically-high level of confidence.

The latest survey conducted by the University of Michigan indicates the average confidence level of US households remain at an elevated level despite central bank concerns regarding international factors. The University’s preliminary estimate of its Index of Consumer Sentiment moved a little higher from June’s revised figure of 98.2 to 98.4 in July, in line with the market estimate.

The University’s chief economist (Surveys of Consumers), Richard Curtin said one of the components of the index had changed in an interesting fashion. Previous surveys had revealed consumers view higher inflation as a threat to economic growth through rising interest rates and higher unemployment expectations. “Consumers’ views appear to be more consistent with the stagflation thesis, which holds that inflation and unemployment move in the same direction. This thesis is more consistent with how consumers process and organize diverse bits of news about the economy.” He said consumers’ attitudes to inflation are usually based on overall inflation and not wage inflation as per Phillips curve theory.