30 May 2019

Australia’s capital expenditure (capex) slump was thought to have come to an end in 2018 as investment in the mining sector reverted back to its long-term mean after a spike early in the decade. Total investment had begun to grow again, driven by investment in the services sector. Even so, two of the quarters in calendar 2018 still had small contractions.

According to the latest ABS figures, seasonally-adjusted private sector capex in the March quarter of 2019 contracted by 1.7%, a deterioration from the December quarter’s +1.3% after revisions and considerably less than the 0.5% increase which had been expected. On a year-on-year basis, the growth rate fell back into the red at -1.9% after recording a revised rate of +1.0% in the December quarter.

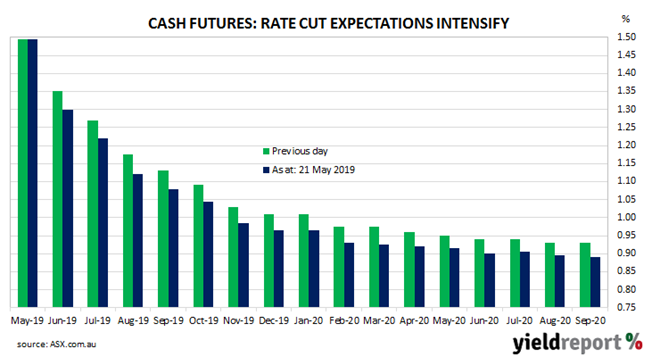

Local financial markets reacted by sending bond yields higher while cutting back the likelihood of looser monetary policy, although the April dwelling approvals report may have had something to do with it. By the end of the Australian trading day, 3-year Treasury bond yields were 4bps higher at 1.13%, 10-year yields had gained 5bps to 1.55% and 20-year yields had increased by 4bps to 2.00%. Cash futures prices mostly moved in a direction which implied a lower likelihood of rate cuts in 2019 and 2020 but not in any meaningful way; rate cuts are still the expected outcome. June cash contracts still priced in a 25bps reduction as an 88% chance while August contracts have a cut fully priced in, along with 72% chance of a second, additional cut. November contracts have two rate cuts fully factored in.

28 May 2019

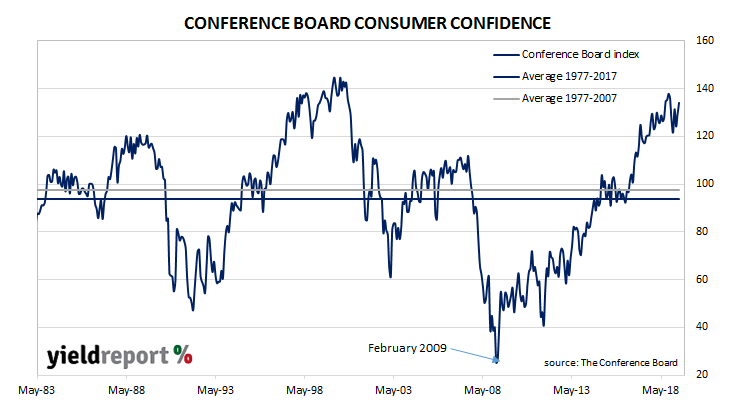

US consumer confidence collapsed in late 2007 as the US housing bubble burst and the US economy went into recession. By 2016, it had clawed its way back to neutral and then went from strength to strength until late 2018. After a dramatic drop through December and January and a couple of months of volatility, recent index values appear to have stabilised at historically high levels.

The latest Conference Board survey indicates US consumers recovered their elevated sense of optimism which existed before a two-month dip around the new-year period. The latest reading came in at 134.1, up from April’s final figure of 129.2, not far away from this cycle’s peak reading of 137.9. From a historical perspective, May’s reading is in the highest 10%.

Lynn Franco, The Conference Board’s Director of Economic said, “The increase in the Present Situation Index was driven primarily by employment gains. Expectations regarding the short-term outlook for business conditions and employment improved, but consumers’ sentiment regarding their income prospects was mixed.”

22 May 2019

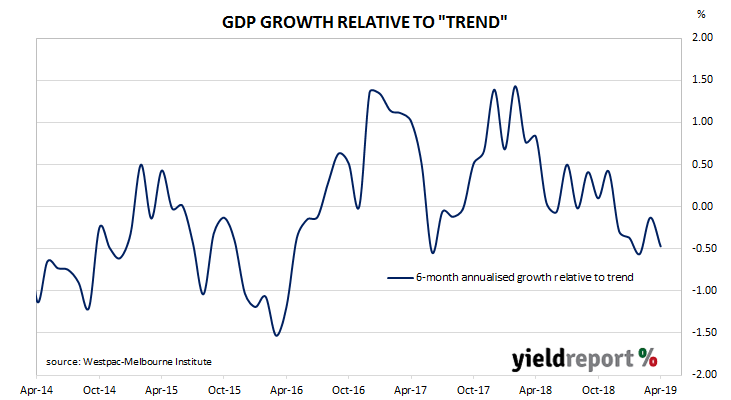

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of Australian economic activity relative to trend over the next three to six months. Since its peak in early 2018, the index had progressively headed lower through 2018 and into 2019. The latest figures have not deteriorated any further but they indicate GDP is likely to remain below trend in coming quarters.

The six-month annualised growth rate of the indicator fell back from March’s revised figure of -0.13% to -0.47% in April. These figures represent rates relative to trend-GDP growth, which is generally thought to be around 2.75% per annum. The Index is said to lead GDP by 3 months to 6 months, so theoretically the current reading represents an annualised GDP growth rate of around 2.25% in late-2019.

The index combines certain economic variables which are thought to lead changes in economic growth into a single variable. Westpac views this variable as a reliable cyclical indicator for the Australian economy and an indicator of swings in Australia’s overall economic activity.

Westpac chief economist Bill Evans re-iterated his comments in recent months regarding the likely rate of GDP growth in 2019. “The Index growth rate has been consistently negative over the last five months, a clear signal that economic growth through the three quarters of 2019 is likely to be below trend.” He is expecting just 2.2% GDP growth for the 2019 calendar year.

22 May 2019

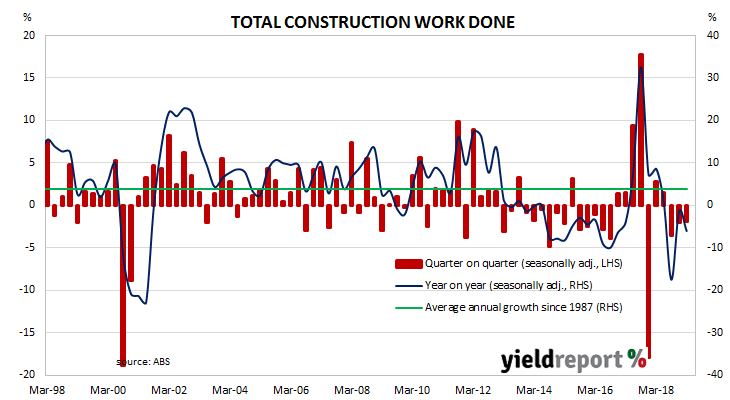

Quarterly construction data compiled and released by the ABS are not considered to be of a “primary” nature in the same way as unemployment (Labour Force) and inflation (CPI) figures. However, the figures are viewed by economists and analysts with interest as they directly feed into quarterly GDP figures.

According to the latest construction figures published by the ABS, the value of construction work has fallen for a third consecutive quarter. Total construction in the March quarter fell by 1.9%, which is less than the flat result expected and slightly less than the revised 2.1% fall in the December quarter. On an annual basis, the growth rate deteriorated from December’s revised figure of -1.5% to -6.0%.

ANZ senior economist Catherine Birch said, “The weakness in residential activity was not a surprise, but public engineering construction contracted for the third consecutive quarter, which is surprising given the large pipeline of public infrastructure spending.

21 May 2019

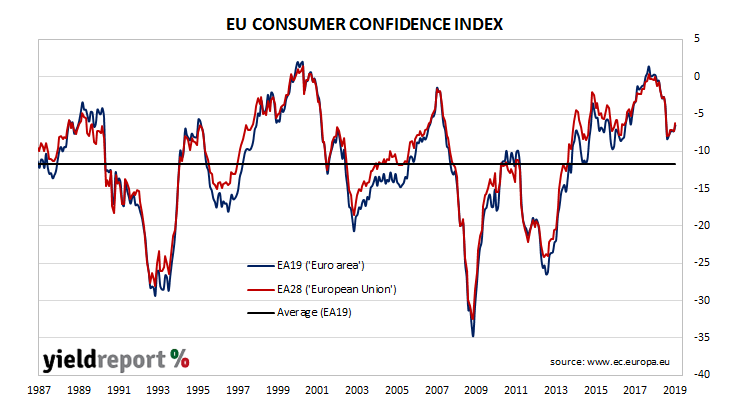

EU consumer confidence plunged during the GFC and again in 2011/12 during the European debt crisis. Since early 2014 it has been at an average of above levels, rising to a cyclical peak at the beginning of 2018. It then dropped back significantly in December 2018, albeit to still-elevated levels, at about the same time as doubts emerged over the US economy’s robustness. Since then, it has slowly been recovering.

The latest survey conducted by the European Commission indicates EU households have continued to remain quite optimistic in the face of low GDP growth rates and high unemployment rates in some large EU countries such as France, Spain and Italy. The latest reading produced a small gain in the EC’s Consumer Confidence indicator as it increased from April’s revised figure of -7.3 in April to -6.5.

21 May 2019

The RBA held the official cash rate steady at its board meeting in May, as it had for every meeting since the cash rate was reduced to 1.50% in August 2016. Statements from RBA officials through 2018 had indicated the next move was “more likely to be an increase” until February of this year. The RBA then changed its tune and stated “the probabilities around these scenarios were now more evenly balanced than they had been over the preceding year…” Two months later, the RBA’s April minutes stated nothing was likely in the foreseeable future. “Given this outlook for further progress towards the Bank’s goals, members agreed that there was not a strong case for a near-term adjustment in monetary policy.” However, the minutes also stated a cut in the cash rate would be appropriate “where inflation did not move any higher and unemployment trended up…” Note the use of the word “trend”.

The minutes of the RBA Board’s May meeting have now been released and the contents complete the shift which started in late 2018 of the RBA’s outlook from “hawkish” to “dovish”.

Local bond yields fell across the curve despite higher yields in offshore markets. By the end of the day, 3-year, 10-year and 20-year ACGB yields had each shed 4bps to 1.18%, 1.65% and 2.09% respectively.

17 May 2019

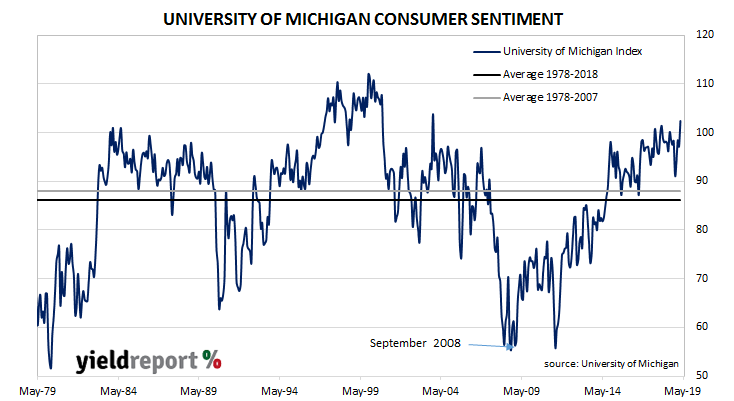

US consumer confidence had started 2019 at well-above-average levels in a longer-term context, although it was markedly lower than the more buoyant readings which typified most of 2018. Less-confident households are generally inclined to spend less and save more and some drop off in household consumption, especially on discretionary spending, could have been expected to follow. As private consumption expenditures account for a majority of GDP in advanced economies, a lower rate of household spending growth would flow through to lower GDP growth if other GDP components did not compensate. However, the latest consumer survey suggests this is currently not the case in the US.

The latest survey conducted by the University of Michigan indicates the average confidence level of US households has moved from an elevated level to one which is bordering on exuberant. The University’s Index of Consumer Sentiment result jumped from April’s revised figure of 97.2 to 102.4 in May, significantly more than the market estimate of 97.9. Westpac’s Finance AM team explained the increase in terms of “a solid jobs market outweighing skittish markets and rising trade tensions.”

15 May 2019

After a lengthy divergence between consumer sentiment and business confidence in Australia which began in 2014, the two sectors converged again around July 2018. Currently, both measures are around neutral or slightly negative levels. The latest reading of consumer sentiment may have moved to a slightly optimistic level but it is still only at the long-term average.

According to the latest Westpac-Melbourne Institute survey conducted in early May, average household optimism has continued to remain close to neutral levels. The Consumer Sentiment Index moved a little higher, this time from April’s reading of 100.7 to 101.3. Any reading above 100 indicates the number of consumers who are optimistic is greater than the number of consumers who are pessimistic. The long-term average reading is just over 101.

Westpac chief economist Bill Evans said, “Despite the Reserve Bank ultimately deciding not to cut the cash rate at its May Board meeting, it is likely that households are much more confident this month than previously that interest rates are likely to come down further.”

15 May 2019

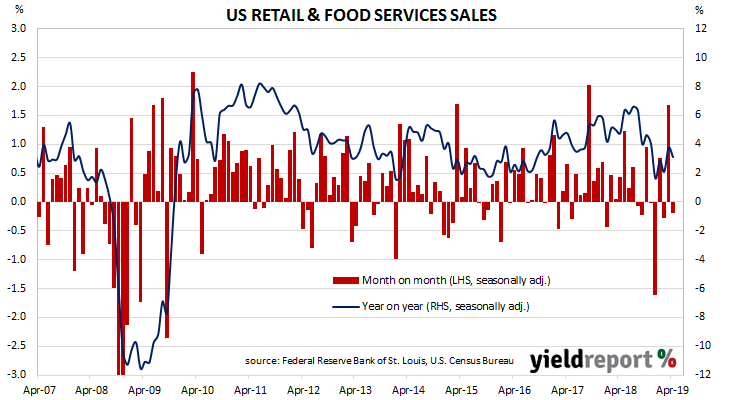

US retail sales had been trending up since late 2015 but, beginning in late-2018, a series of weak or negative monthly results led to a drop-off in the annual growth rate. Subsequent sales figures formed a downtrend which brought the annual rate below 2.0% by the end of the year. Growth in the March quarter was quite strong but the conditions which produced those results may not have spilled into April.

According to the latest “advance” sales numbers released by the US Census Bureau, total retail sales declined by 0.2% in April, well under the +0.2% which had been expected and a marked reversal from March’s revised figure of +1.7%. On an annual basis, the growth rate slowed to 3.1% from March’s revised rate of 3.8%.

Financial markets reacted by sending bond yields lower. By the end of the day, yields on 2-year, 10-year and 30-year Treasury bonds were all 3bps lower at 2.16%, 2.38% and 2.82% respectively. However, prices in the futures market for federal funds reacted in a different manner and the likelihood of a lower rate after the FOMC’s December meeting was trimmed from 75% to 71%.

14 May 2019

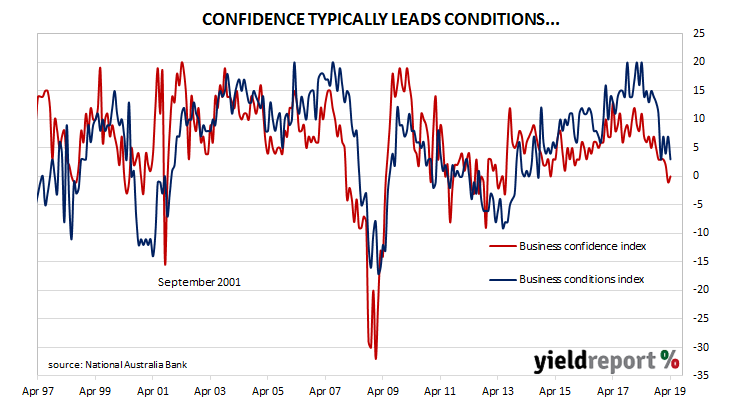

Australian business conditions were robust in the first half of 2018 and a cyclical-peak was reached in April of that year. Although they remained well above average for some months, readings began to slip and by the end of 2018, they had dropped to below-average levels. Readings have now oscillated within a fairly narrow band for the last four months.

According to NAB’s latest monthly business survey of 400 firms conducted in the second half of April, business conditions have continued their swing between the lower side of “normal” and “somewhat on the low side”. Since the latter part of 2018, NAB’s conditions index has bounced between 3, which is on the low side, and 7, which is about average. The latest reading produced by the index is 3.

Westpac senior economist Andrew Hanlan said, “The NAB business survey for April was particularly weak, providing further evidence of the economic slowdown which emerged in mid-2018 and has extended into 2019.”