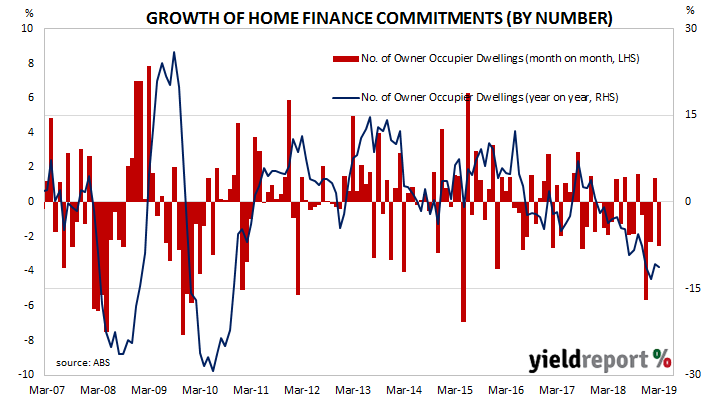

13 May 2019

Since late 2017/early 2018, a very clear downtrend has been evident in the monthly figures of both the number and value of home loan commitments. After the figures from February were released, some economists speculated the worst may have been over. The latest numbers have made that suggestion unlikely.

The ABS has released March’s housing finance commitment figures* and they were less than expected. The total number of loan commitments to owner-occupiers decreased by 2.5%, a larger contraction than the expected -0.5% and a reversal of February’s revised figure of +1.4%. On an annual basis, the growth rate further deteriorated to -11.3% from -10.8% after revisions. When “re-financings” are removed, the number of loan commitments fell by 2.8% over the month and by 13.8% when compared to commitments from March 2018.

ANZ economist Adelaide Timbrell summed up the report in the following way. “All categories of housing finance posted sharp losses and were below market expectations. Owner-occupier finance was hit hardest, although this may be a correction to last month’s spike of owner-occupier finance, which was the highest monthly gain since August 2017.”

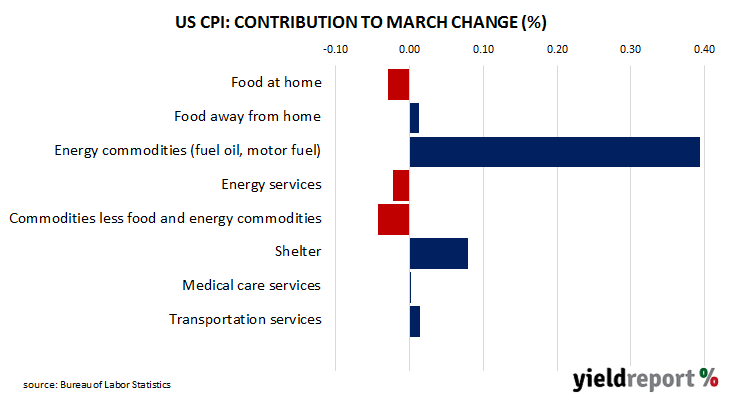

10 May 2019

The annual rate of US consumer inflation halved from nearly 3% in the period from July 2018 to February 2019, before it then quickly increased back to 2%. At the same time, core inflation has been much less volatile and it has mostly ranged between 2.00% and 2.30%. In recent times, differences between the two measures has mostly been caused by changes in gasoline (petrol) prices.

Consumer price index (CPI) figures released by the Bureau of Labor Statistics indicated seasonally-adjusted consumer prices increased on average by 0.3% in April, below the 0.4% consensus figure and lower than March’s 0.4% increase. On a 12-month basis, the inflation rate inched up from March’s annual rate of 1.9% to 2.0%. The primary driver of the increase was another move in gasoline prices but rents also played some part.

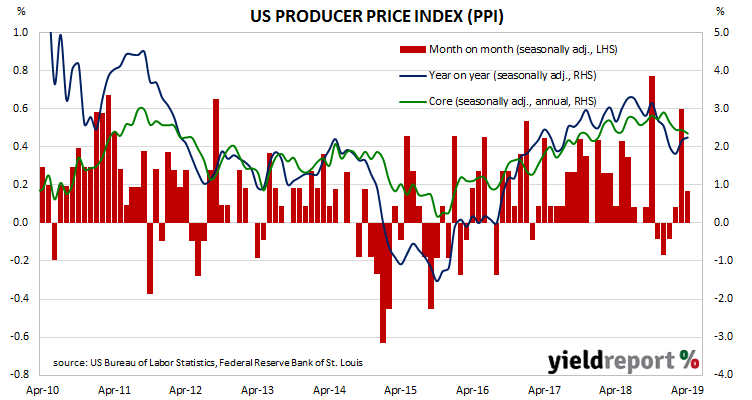

09 May 2019

The producer price index (PPI) is a measure of prices charged by producers for domestically produced goods, services, and construction. In the US, it is constructed by the Bureau of Labor Statistics in a fashion similar to the consumer price index (CPI) except it measures prices received from the producer’s perspective. It is another one of the various measures of inflation tracked by the US Fed, along with core personal consumption expenditure (PCE) data.

The latest figures for April have been published by the Bureau and they indicate producer prices increased by 0.2% during the month after seasonal adjustments. The result was in line with the expected figure but considerably less than March’s +0.6%. On a 12-month basis, the rate of producer price inflation after seasonal adjustments accelerated to 2.3% after recording 2.2% in March and 1.8% in February. “Core” PPI inflation fell back from March’s 0.3% to 0.1% in April but the rate of annual increase remained at 2.4%.

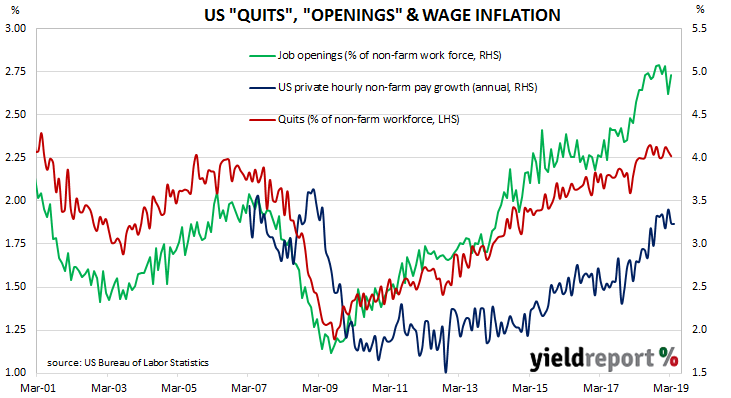

07 May 2019

The quit rate as a percentage of total US non-farm employment had been rising slowly but steadily since the end of the GFC. It made a series peak in August 2018 and then stabilised, with total quits roughly increasing at the same rate as non-farm employment.

Figures released as part of the most recent JOLTS report show the quit rate remained unchanged at a historically high level. During March, 2.3% of the non-farm workforce left their jobs voluntarily, the same rate as it has been since July after revisions to estimates of the total non-farm workforce. Quit numbers were highest in wholesale trade, “other services” and real estate rental/leasing sectors while the construction and accommodation/food services sectors recorded the largest falls. Overall, the total number of quits slipped from February’s revised figure of 3.447 million to 3.409 million.

Job openings rebounded from February’s noticeable drop. Total vacancies during March jumped from February’s revised figure of 7.142 million to 7.488 million, driven by additional openings in the transportation, warehousing/utilities, health care/social assistance and construction sectors. The finance/ insurance and non-durable goods manufacturing sectors recorded significantly reduced openings.

07 May 2019

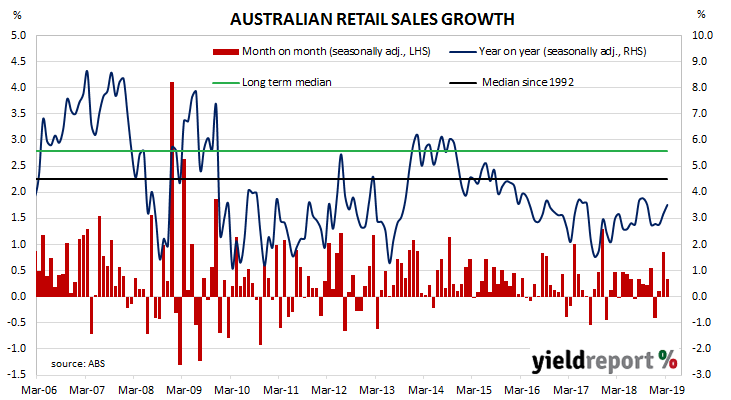

Growth figures for domestic retail sales have been declining since 2014 and they hit a low point in September 2017. Annual growth rates then began increasing for about a year, only to stabilise at around 3.0% to 3.5% through late-2018 and early-2019. The last few months’ reports have provided some encouraging figures but they are far from a state which could be accurately described as buoyant, strong or robust.

According to the latest ABS figures, total retail sales increased by 0.3% in March on a seasonally-adjusted basis, generally in line with market expectations although a clear drop from February’s revised increase of +0.9%. On an annual basis, retail sales increased by 3.5%, up from February’s comparable figure of 3.2%.

Financial markets responded by sending local bond yields higher although a good amount, if not all of the reaction, arose from the RBA’s decision in the afternoon to not reduce the cash rate as many economists had expected. By the end of the day, the yield on 3-year ACGBs had jumped 8bps to 1.31%, 10-year yields had gained 5bps to 1.80% and 20-year yields were 4bps higher at 2.22%.

07 May 2019

The May board meeting of the RBA is historically one of the four months of the year in which the likelihood of a rate change is highest. February, May, August and November happen to be the four months of the year in which previous rate changes have typically occurred.

At this latest board meeting, the RBA decided to leave Australia’s overnight cash rate unchanged at 1.50%. For most, if not all of the thirty board meetings held since the rate was last changed in August 2016, describing such a decision “as expected” was par for the course. However, in the lead up to this latest meeting, 14 out of 26 economists in a Bloomberg poll had expected the RBA to cut rates by 25bps. Cash futures contracts at the time implied traders were not as confident of a cut; May contracts implied a move by the RBA was viewed as a realistic chance at 38%.

However, in the lead up to this latest meeting, 14 out of 26 economists in a Bloomberg poll had expected the RBA to cut rates by 25bps. Cash futures contracts at the time implied traders were not as confident of a cut; May contracts implied a move by the RBA was viewed as a realistic chance at 38%.

So, once the decision to leave the cash rate unchanged was announced, bond yields moved quickly and significantly. By the end of the day, the yield on 3-year ACGBs had jumped 8bps to 1.31%, 10-year yields had gained 5bps to 1.80% and 20-year yields were 4bps higher at 2.22%.

06 May 2019

From mid-2017 onwards, year-on-year growth rates in the total number of job advertisements consistently exceeded 10%. That was until mid-2018 when the annual growth rate fell back markedly and then tracked lower for the remainder of 2018. Figures in the beginning of 2019 continued that trend and the latest April figures have continued to go backwards, albeit at a slower pace.

April’s figures have now been released by ANZ and, after revisions and seasonal adjustments, total advertisements slipped by 0.1% to 166,464. On a 12-month basis, total job advertisements fell by 5.6%, a slight improvement on March’s comparable figure of -6.2% after revisions.

ANZ’s Head of Australian Economics, David Plank said, “After five successive steep falls, it is pleasing to see a virtually unchanged result in job ads for April.” Financial markets responded by sending local bond yields lower while the expectation of rate cuts through 2019 and 2020 firmed, although some part of the reaction may have been related to the Melbourne Institute’s Inflation Gauge figures which had been released around the same time. By the end of the day, the yield on 3-year ACGBs had lost 4bps to 1.23%, 10-year yields had dropped 6bps to 1.75% and 20-year yields were 4bps lower at 2.18%.

Financial markets responded by sending local bond yields lower while the expectation of rate cuts through 2019 and 2020 firmed, although some part of the reaction may have been related to the Melbourne Institute’s Inflation Gauge figures which had been released around the same time. By the end of the day, the yield on 3-year ACGBs had lost 4bps to 1.23%, 10-year yields had dropped 6bps to 1.75% and 20-year yields were 4bps lower at 2.18%.

06 May 2019

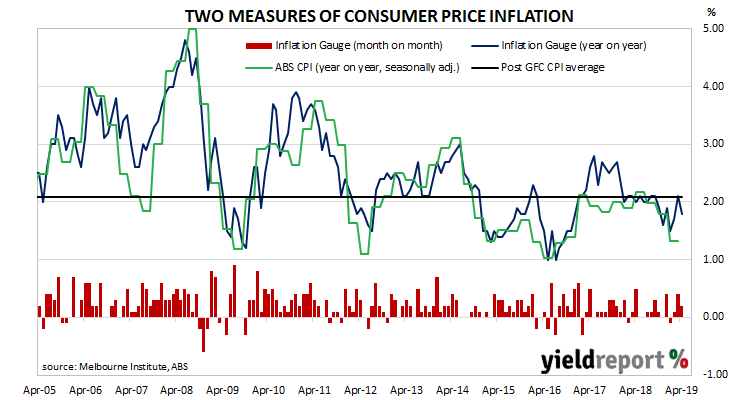

The Melbourne Institute’s Inflation Gauge is an attempt to replicate the ABS consumer price index (CPI) on a monthly basis. It has turned out to be a reliable leading indicator of the CPI, although there are periods in which the Inflation Gauge and the CPI have diverged for as long as twelve months. On average, the Inflation Gauge’s annual rate tends to overestimate changes in CPI inflation by an average of about 0.1% per quarter.

The Inflation Gauge index increased by 0.2% during April after a 0.4% increase in March and a 0.1% increase in February. On an annual basis, the index increased by 1.8%, down from March’s comparable rate of 2.1%. For the purposes of comparison, the CPI has grown at a compound rate of 2.1% since the beginning of April 2009.

03 May 2019

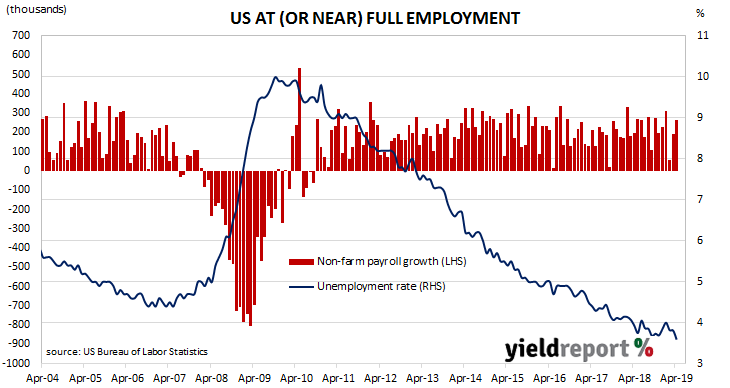

The US economy continues to produce more jobs despite the being close to full employment. The unemployment rate has remained at or under 4% since April 2018 while annual increases in hourly pay have remained above 3% for seven consecutive months. The latest figures indicate the unemployment rate has been pushed even lower.

According to the US Bureau of Labor Statistics, the US economy created 263,000 jobs in the non-farm sector in April. Economists had been expecting around 180,000 additional positions. The unemployment rate fell from 3.8% to 3.6% as the total number of unemployed people fell by 377,000 to 5.834 million while the total number of people employed in both the farm and non-farm sectors fell by 103,000 to 156.645 million.

US bond yields finished slightly lower overall, although yields at the front of the curve did actually increase a little. By the end of the day, 2-year Treasury bond yields had crept up 1bp to 2.34%, 10-year yields had lost 2bps to 2.52% and 30-year yields had slipped 1bp to 2.92%.

03 May 2019

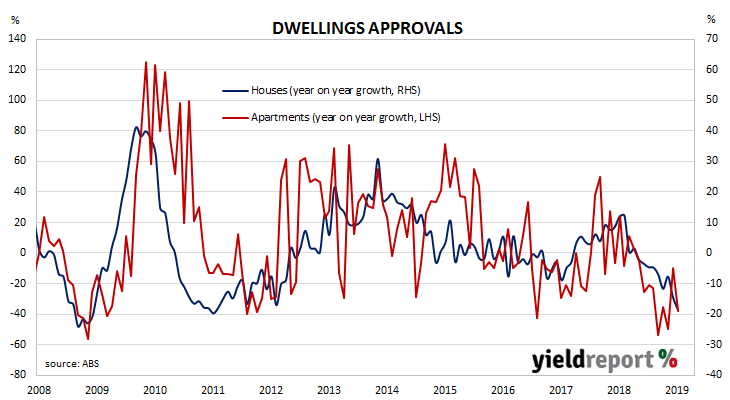

Aside from engineering and architectural design, one of the earliest requirements of a building project is to obtain approval from the relevant statutory body. While not all projects which have been approved are completed, all completed projects have been granted approval. Approvals data thus provides a useful indicator of future construction activity.

The latest building approval figures have been released by the Australian Bureau of Statistics and they indicate the downtrend which started in mid-2018 may not have ended after all. Seasonally-adjusted, total approvals fell by 15.5% in March, which is below the market consensus figure of -12.5% and a marked reversal from February’s revised figure of +19.1%. On an annual basis, total approvals fell by 27.3%, as compared to February’s comparable figure of -12.3% after revisions.

Reactions in local financial markets were minimal. By the end of the Australian trading day, 3-year Treasury bond yields were unchanged at 1.27%, 10-year yields had gained 1bp to 1.81% but 20-year yield slipped 1bp to 2.22%. Cash futures prices mostly moved in a direction which implied a lower likelihood of rate cuts in 2019 and 2020 but only in a technical sense. A rate cut before the end of August is still viewed as a certainty and an additional cut before the end of November has been assigned a 78% probability.