03 April 2019

Retail sales figures have been lacklustre for the past couple of years but in 2018 the annual growth rate showed some signs of stabilising, albeit at a low rate. Annual growth rates started trending up in early 2018 and growth rates of individual months exceeded expectations on several occasions, only to miss market expectations in December and January 2019. However, the latest batch of figures has surprised observers with their strength.

According to the latest ABS figures, total retail sales increased by 0.8% over February on a seasonally-adjusted basis, well above the expected +0.3% increase and a distinct leap from January’s +0.1%. On an annual basis, retail sales increased by 3.2%, up from January’s comparable figure of 2.7%.

Local financial markets reacted by sending bond yields higher. By the end of the day, the yield on 3-year, 10-year and 20-year Treasury bonds had all increased by 3bps to 1.36%, 1.85% and 2.27% respectively. In terms of local monetary policy, expectations of future rate cuts were pared back slightly but not really be enough to materially alter the outlook through 2019 and 2020. August contracts implied a 98% chance of a 25bps rate cut while November contracts implied one cut plus a 44% chance of an additional reduction in the cash rate down to 1.0%.

02 April 2019

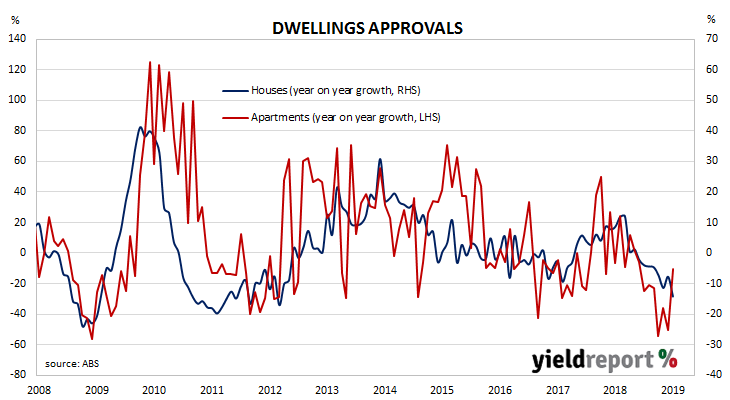

Aside from engineering and architectural design, one of the earliest requirements of a building project is to obtain approval from the relevant statutory body. While not all projects which have been approved are completed, all completed projects have been granted approval. Approvals data thus provides a useful indicator of future construction activity.

The latest building approval figures have been released by the Australian Bureau of Statistics and they indicate the downtrend which started in mid-2018 may have ended. Seasonally-adjusted, total approvals increased by 19.1% in February, which is well over the market consensus figure of -1.8% and a large increase from January’s revised figure of +2.3%. On an annual basis, total approvals fell by 12.5%, as compared to January’s comparable figure of -28.9% after revisions.

Westpac senior economist Matthew Hassan noted a large rise in high-rise approvals among the figures. “The spike is almost certainly a one-off, making the headline result in a misleading ‘rogue’. Indeed, approvals ex high-rise look to have been significantly weaker than expected.”

01 April 2019

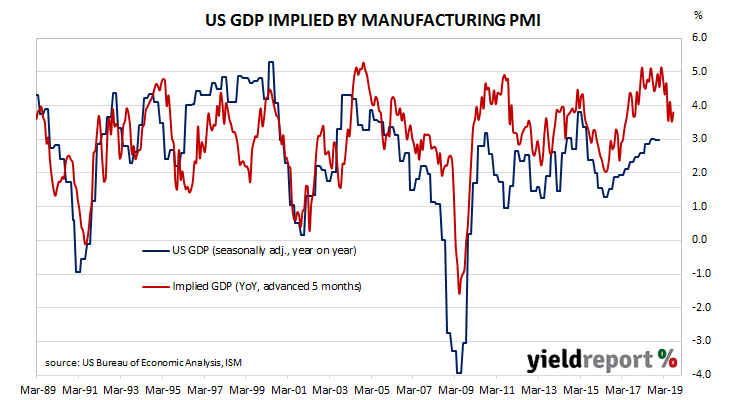

Purchasing managers’ indices (PMIs) have been sliding in recent months, albeit from elevated levels. After reaching a cyclical peak in September 2017, manufacturing PMI readings went sideways for a year before they started a downtrend. The latest reading represents an improvement on the previous month’s figure but this does not necessarily mean the series of lower readings are over.

US manufacturing activity accelerated in March, partially recovering February’s fall. According to the Institute of Supply Management (ISM) March survey, its Purchasing Managers Index recorded a reading of 55.3, up from February’s reading of 54.2 and above the market’s expected figure of 54.3.

The average reading since 1948 is 52.9, so the current reading is above the long-term average. US financial markets reacted by sending Treasury bond yields noticeably higher while expectations of looser monetary policy were trimmed a little. By the end of the day, 2-year Treasury bond yields were 7bps higher at 2.33%, 10-year yields had gained 9bps to 2.50% and 30-year yields were 8bps higher at 2.89%. In terms of US monetary policy, according to federal funds futures contracts, the probability of a rate change before the end of 2019 is quite high, unlike a month ago. After the report, futures prices implied a 60% chance of a rate cut at the December meeting of the FOMC, down from 65% at the end of the previous day.

01 April 2019

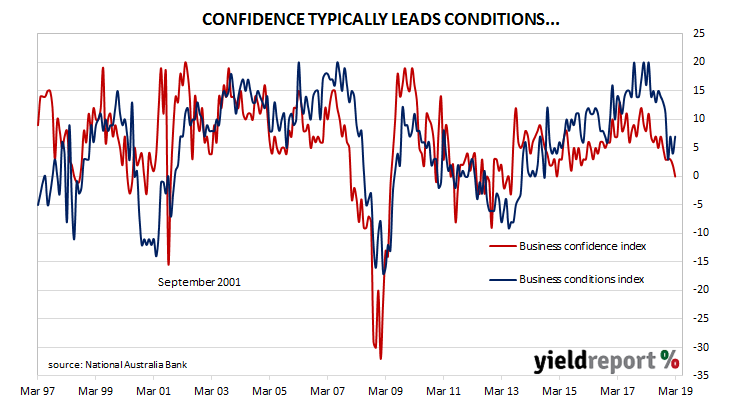

Australian business conditions were robust in the first half of 2018 and a cyclical-peak was reached in April of that year. Although they remained well above average for some months, readings began to slip. By the end of 2018, the readings had plunged to below-average levels and they remained there through the first few months of 2019. At the same time, the confidence index continued to weaken.

According to NAB’s latest monthly business survey of 400 firms conducted in the middle of March, business conditions continued to bounce up and down. After several months of consecutive falls in the latter part of 2018, NAB’s conditions index bounced to 7 in January and then fell back to 4 in February, only to bounce back to 7 again in March. NAB chief economist Alan Oster said, “Business conditions saw a welcome increase to above-average levels with each subcomponent of the index rising. The employment index itself remains well above average, suggesting that for now, survey indicators of labour demand remain favourable. Against this, business confidence…weakened further in the month and continued the below-average run.” The latest reading of the confidence index fell again, this time from 2 to 0, a reading which is statistically well below the long-term average reading of 6. Typically, NAB’s confidence index leads the conditions index by approximately one month, although some divergences appear from time to time. After converging recently, the confidence index has once again diverged from the conditions index.

The latest reading of the confidence index fell again, this time from 2 to 0, a reading which is statistically well below the long-term average reading of 6. Typically, NAB’s confidence index leads the conditions index by approximately one month, although some divergences appear from time to time. After converging recently, the confidence index has once again diverged from the conditions index.

01 April 2019

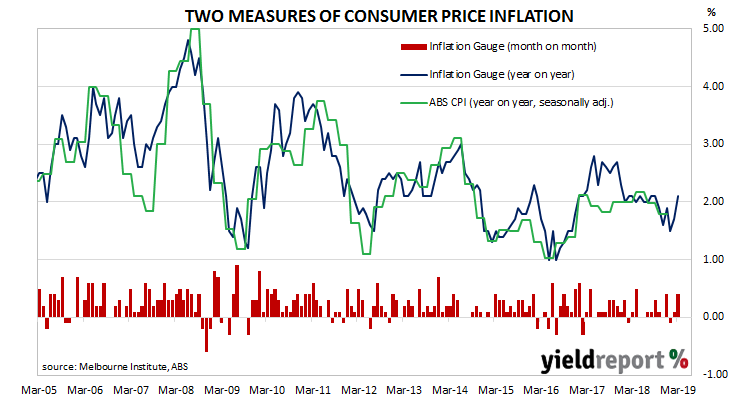

The Melbourne Institute’s Inflation Gauge is an attempt to replicate the ABS consumer price index (CPI) on a monthly basis. It has turned out to be a reliable leading indicator of the CPI, although there are periods in which the Inflation Gauge and the CPI have diverged for as long as twelve months. On average, the Inflation Gauge’s annual rate tends to overestimate changes in CPI inflation by an average of about 0.10% in any given quarter.

The Inflation Gauge increased by 0.40% during March after a 0.10% increase in February and a 0.10% fall in January. On an annual basis, the index increased by 2.10%, up from February’s comparable rate of 1.70%.

Given the Inflation Gauge’s tendency to overestimate, the latest figures imply an official CPI reading of 0.6% (seasonally adjusted) for the March quarter and 2.0% in annual terms.

01 April 2019

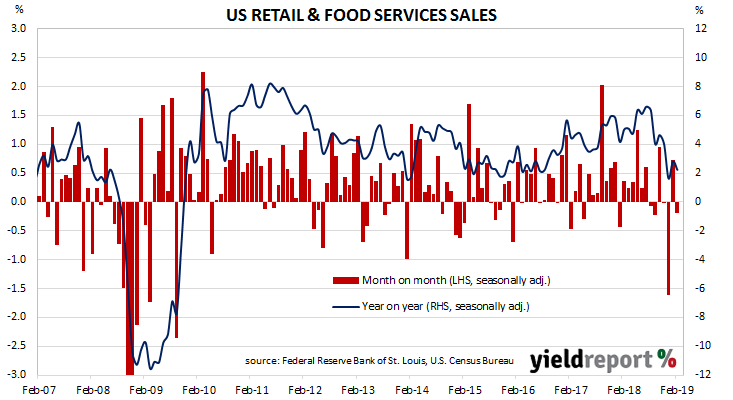

US retail sales have been trending up since late 2015. While there have been patches of weakness along the way, later months’ figures have rebounded to higher levels. After reaching an annual growth rate of 6.6% in July 2018, subsequent sales figures formed a downtrend which brought the annual rate below 2.0% by the end of the year. After a rebound in January, February’s figures may mark a return of this downtrend.

According to the latest “advance” numbers released by the US Census Bureau, total retail sales contracted by 0.2% in February, noticeably below the 0.3% increase which had been expected and a large fall from January’s revised figure of +0.7%. On an annual basis, the growth rate fell back to 2.2% after recording 2.8% in January after revisions. The ISM’s manufacturing PMI report was released almost at the same time and thus the effect of the sales figures was hard to determine. However, by the end of the day, 2-year Treasury bond yields were 7bps higher at 2.33%, 10-year yields had gained 9bps to 2.50% and 30-year yields were 8bps higher at 2.89%. In terms of US monetary policy, according to federal funds futures contracts the probability of a rate change before the end of 2019 is quite high, unlike a month ago. Futures prices implied a 60% chance of a rate cut at the December meeting of the FOMC, down from 65% at the end of the previous day.

The ISM’s manufacturing PMI report was released almost at the same time and thus the effect of the sales figures was hard to determine. However, by the end of the day, 2-year Treasury bond yields were 7bps higher at 2.33%, 10-year yields had gained 9bps to 2.50% and 30-year yields were 8bps higher at 2.89%. In terms of US monetary policy, according to federal funds futures contracts the probability of a rate change before the end of 2019 is quite high, unlike a month ago. Futures prices implied a 60% chance of a rate cut at the December meeting of the FOMC, down from 65% at the end of the previous day.

29 March 2019

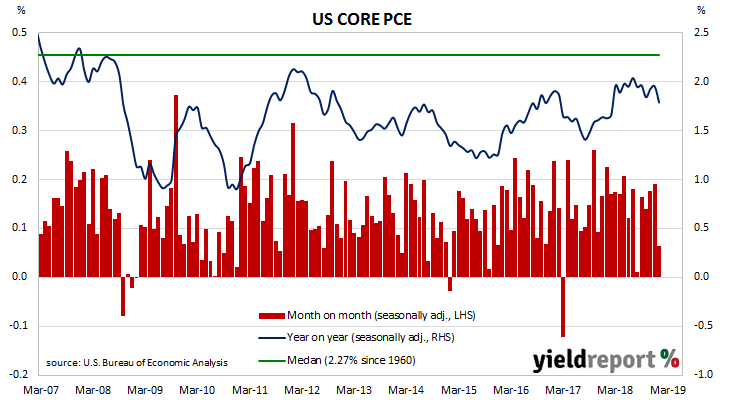

One of the US Fed’s favoured measures of inflation is the change in the core personal consumption expenditures (PCE) price index. After hitting the Fed’s target at 2.0% in July, the annual rate then slipped a little and then hovered in a range between 1.8% and 2.0% through the end of 2018 and into early 2019.

January’s expenditure figures have now been published by the Bureau of Economic Analysis as part of the February personal income and expenditures report (some results have been delayed by the US federal shutdown in late-December and early-January). At +0.1% for the month, core PCE inflation was lower than December’s +0.2% and lower than the expected +0.2% increase. On a 12-month basis, the core PCE inflation rate fell from December’s figure of 2.0% to 1.8%.

29 March 2019

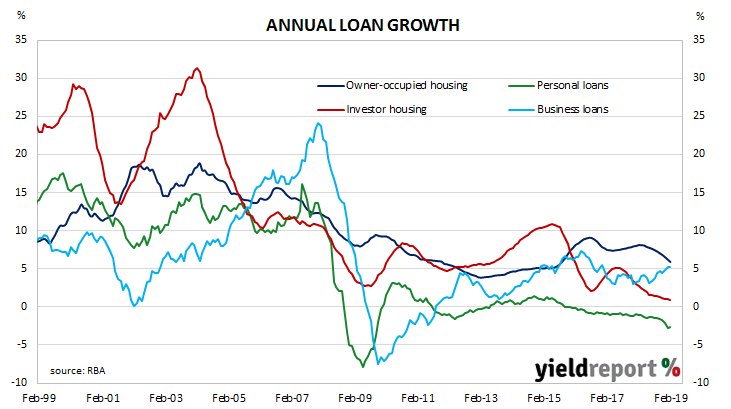

The pace of lending to the non-bank private sector by financial institutions in Australia has been trending down since October 2015. It appeared to have stabilised in the September quarter of 2018 but credit figures in the December quarter put paid to that idea. The first two months of 2019 have provided more of the same and growth rates have further deteriorated.

According to the latest RBA figures, private sector credit grew by 0.3% in February, an increase on January’s figure and more than the 0.2% consensus estimate. However, the annual growth rate slipped from January’s figure of 4.3% to 4.2% as home lending continued to slow.

A month ago, Westpac senior economist Andrew Hanlan said the housing market was the prime determinant and he expanded on this theme after the latest figures. “New lending for housing is contracting, declining by 20% in 2018, with the second half of the year particularly weak, down 15%. Weakness has become more broadly based, including owner-occupiers. Lending to both investors and owner-occupiers fell by around 15% over the second half of 2018.”

26 March 2019

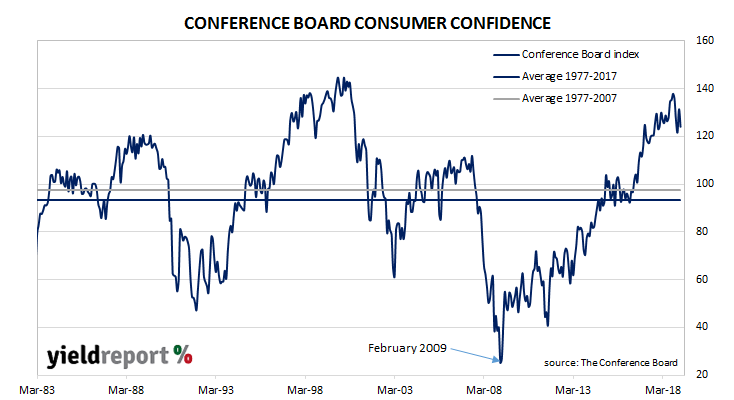

US consumer confidence collapsed in late 2007 as the US housing bubble burst and the US economy went into recession. By 2016, it had clawed its way back to neutral and then went from strength to strength until late 2018. After a dramatic drop through December and January, confidence levels bounced in February. This latest survey has reversed much of that bounce.

The latest Conference Board survey indicates US consumers are not quite as optimistic as February’s survey suggested. The latest reading came in at 124.1, a considerable fall from February’s reading of 131.4 but still at an elevated level in historical terms. Most of the fall was attributable to US households’ views of current business and labour market conditions.

The consensus expectation prior to the report was for a reading of around 132. However, US bond yields still finished the day higher. By this time, 2-year Treasury bond yields had gained 3bps to 2.26% while 10-year and 30-year yields had each increased by 2bps to 2.42% and 2.88% respectively.

20 March 2019

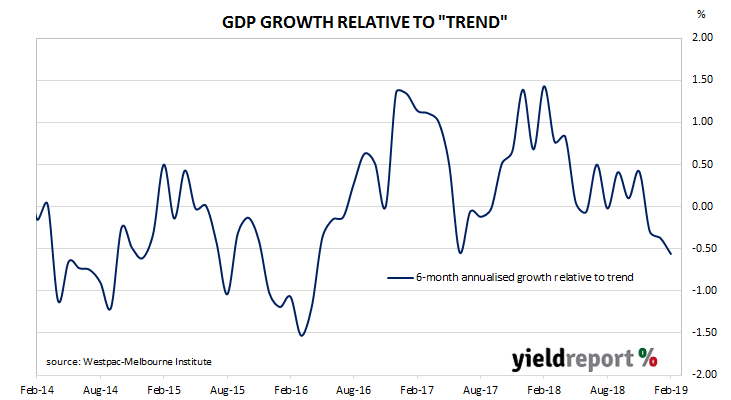

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of economic activity relative to trend in Australia. The index combines certain economic variables which are thought to lead changes in economic growth into a single variable. Westpac views this variable as a reliable cyclical indicator for the Australian economy and an indicator of swings in Australia’s overall economic activity.

The six-month annualised growth rate of the indicator fell back from a revised January figure of -0.37% to -0.56% in February. These figures represent rates relative to trend-GDP growth, which is generally thought to be around 2.75% per annum. The Index is said to lead GDP by 3 months to 6 months, so theoretically the current reading represents an annualised GDP growth rate of around 2.20% in mid-2019.

Westpac chief economist Bill Evans said, “This is a strengthening signal that growth through the first two to three quarters of 2019 is likely to be below trend.” He expects the RBA to ratchet back its 2019 GDP growth forecasts at its May and August meetings and consequently cut the cash rate by 25bps in August and November.