19 March 2019

The RBA held the official cash rate steady at its board meeting in March, as it had for every meeting since the cash rate was reduced to 1.50% in August 2016. Statements from RBA officials through 2018 had indicated the next move was “more likely to be an increase” until February of this year. Then, the RBA changed its tune and stated “the probabilities around these scenarios were now more evenly balanced than they had been over the preceding year…”

The release of any RBA meeting’s minutes is not expected to provide much excitement and only rarely does anything of interest emerge. Most of the time, the minutes are used to clarify statements made by RBA officials or to pinpoint the issues which the RBA has a current focus.

In this case, the minutes highlighted the RBA’s attention on the mismatch between recent weak or softening data reports and the labour market. As ANZ head of Australian Economics David Plank put it, “The dominant theme of the minutes of the RBA’s Board meeting in March is the tension between the activity and employment data.”

Locally, bond yields ignored small rises in bond yields offshore and, by the end of the day, had fallen noticeably. 3-year, 10-year and 20-year yields all shed 5bps to 1.45%, 1.99% and 2.39% respectively. However, in the cash futures market, prices barely changed and contracts continued to imply one rate cut by the end of August, with another cut in November viewed as a 44% chance.

15 March 2019

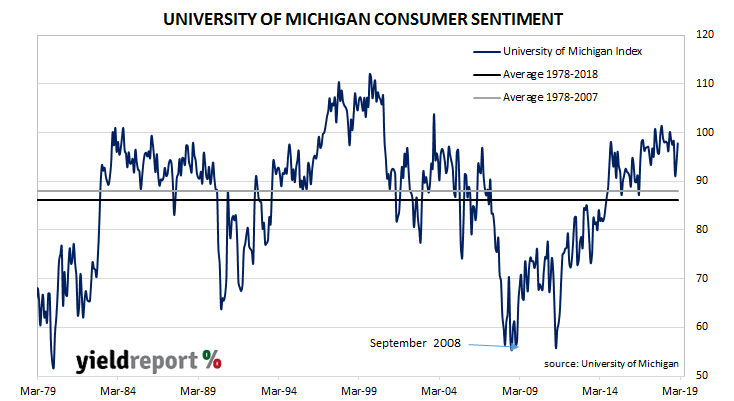

US consumer confidence had been under pressure in recent months and less-confident households are generally inclined to spend less and save more. As private consumption accounts for a majority of GDP growth in advanced economies, household spending is a major determinant of a country’s overall expenditure. However, the latest survey indicates household confidence has bounced back after a sharp drop at the very start of the year.

The latest survey conducted by the University of Michigan indicates confidence levels of US households have recovered back to pre-Christmas levels before the federal shutdown and trade disputes took the spotlight. The University’s Index of Consumer Sentiment result bounced from February’s revised figure of 93.8 to 97.8 in March, more than the market estimate of 95.8.

Richard Curtin, the chief economist of the University’s Survey of Consumers unit, said the higher reading “entirely due” to lower and middle-income households. Sentiment among higher-income households fell.

The University of Michigan’s index is one of two monthly US consumer sentiment indices, the other being the Conference Board’s Consumer Confidence Survey. The University’s survey covers personal finances, business conditions and buying conditions.

15 March 2019

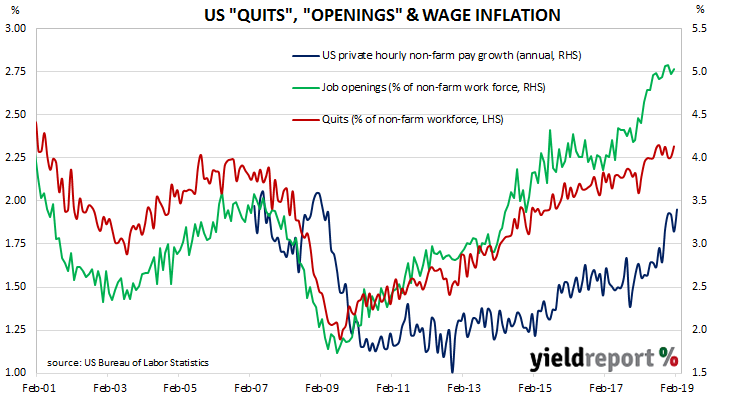

The quit rate as a percentage of total US non-farm employment has been rising slowly but steadily since the end of the GFC. It is now close to its peak reading.

Figures released as part of the most recent JOLTS report show the quit rate has remained stable for a fourth consecutive month. During January, 2.3% of the non-farm workforce left their jobs voluntarily, the same rate as in December, November and October after rounding to one decimal place. Quit rates were highest in the accommodation/food service and in the professional/business services sectors while the finance/insurance and health care sectors recorded the largest falls. Overall, the total number of quits increased from December’s revised figure of 3.39 million to 3.49 million. 8

8

Job openings increased as well. Total vacancies during January increased from December’s revised figure of 7.48 million to 7.58 million, led by increased openings in the wholesale trade and real estate sectors. Openings in the “other services” (maintenance and servicing), retail trade sectors, professional/business services and art/entertainment sectors all fell.

13 March 2019

The producer price index (PPI) is a measure of prices charged by producers for domestically produced goods, services, and construction. In the US, it is constructed by the Bureau of Labor Statistics in a fashion similar to the consumer price index (CPI) except it measures prices received from the producer’s perspective. It is another one of the various measures of inflation tracked by the US Fed, along with core personal consumption expenditure (PCE) data.

The latest figures for February have been published by the Bureau and they indicate producer prices crept up by just 0.1% during the month after seasonal adjustments. The result was under the expected 0.2% increase but it marked a turnaround from January’s -0.1%. On a 12-month basis, the rate of producer price inflation after seasonal adjustments slowed to 1.8% after recording 2.0% in January and 2.5% in December.

13 March 2019

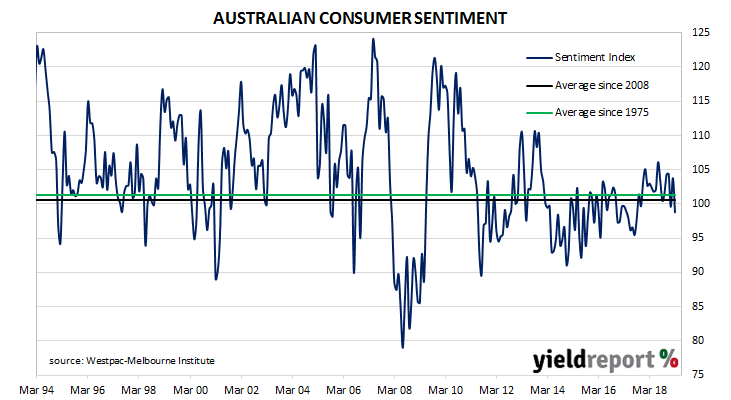

During most of the period between 2014 and 2018 a divergence between consumer sentiment and business confidence in Australia was evident. Normally, the two sectors could be expected to generally track the same path, so an extended difference between the two was somewhat unusual. Around July 2018, the two sectors converged again and they are once again largely in line with each other. Unfortunately, this synchronisation occurred around levels which are neutral to slightly negative.

According to the latest Westpac-Melbourne Institute survey conducted in early-March, average household optimism continued to bounce around neutral levels as the Consumer Sentiment Index retreated under 100 once again, this time from February’s reading of 103.8 to 98.8. Any reading above 100 indicates the number of consumers who are optimistic is greater than the number of consumers who are pessimistic. The long-term average reading is just over 101.

Local bond yields fell considerably, following negative US movements from the previous evening but by a larger magnitude. By the end of the day, 3-year ACGB yields had dropped by 6bps to 1.55%, the 10-year yield was 7bps lower at 1.97% and the 20-year has lost 6bps to 2.36%.

Local bond yields fell considerably, following negative US movements from the previous evening but by a larger magnitude. By the end of the day, 3-year ACGB yields had dropped by 6bps to 1.55%, the 10-year yield was 7bps lower at 1.97% and the 20-year has lost 6bps to 2.36%.

12 March 2019

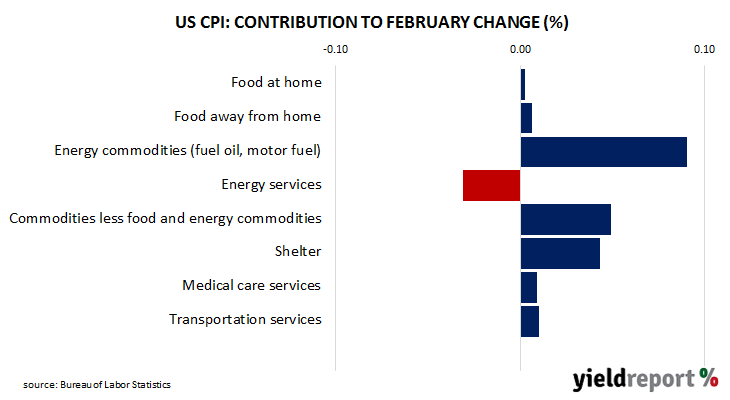

The annual rate of US consumer inflation has dropped from nearly 3% in July 2018 to well below 2% in the first two months of 2019. At the same time, core inflation has been much less volatile and it has ranged between 2.10% and 2.30%. In recent times, differences between the two measures has mostly been caused by changes in gasoline (petrol) prices.

Consumer price index (CPI) figures released by the Bureau of Labor Statistics indicated seasonally-adjusted consumer prices increased on average by 0.2% in February, in line with the consensus figure but higher than January’s flat result. On a 12-month basis, the inflation rate remained at January’s annual rate of 1.5%. The primary driver of the increase was another move in gasoline prices.

“Core” inflation, a measure of inflation which strips out the volatile food and energy components of the index, increased on a seasonally-adjusted basis by +0.1% for the month, in line with expectations. The annual rate remained unchanged at 2.1% after January’s reading was revised down a little.

“Core” inflation, a measure of inflation which strips out the volatile food and energy components of the index, increased on a seasonally-adjusted basis by +0.1% for the month, in line with expectations. The annual rate remained unchanged at 2.1% after January’s reading was revised down a little.

12 March 2019

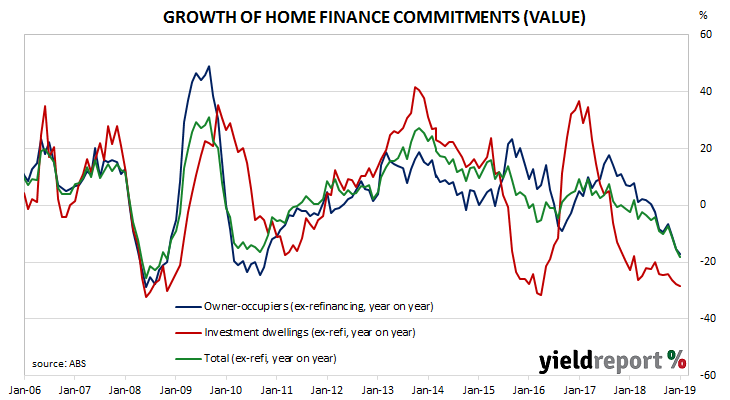

Since late 2017/early 2018, a very clear downtrend has been evident in the monthly figures of both the number and value of home loan commitments. The latest numbers have not done anything to alter this picture.

The ABS has released January’s housing finance commitment figures* and they were large as expected. The total number of loan commitments to owner-occupiers fell by 2.6%, broadly in line with the expected 2% contraction but also an improvement on December’s figure of -6.1%. On an annual basis, the growth rate deteriorated further to -13.6% after registering -11.4% in December. When “re-financings” are removed, the number of loan commitments fell by 1.2% over the month and by 14.8% when compared to commitments from January 2018.

Westpac senior economist Matthew Hassan said, “Overall, the January update was soft but not quite as soft as expected for owner-occupier activity. However, given the less reliable nature of January housing data, this is not enough evidence to signal a shift in the clear weakening trend over the second half of 2018.”

Westpac senior economist Matthew Hassan said, “Overall, the January update was soft but not quite as soft as expected for owner-occupier activity. However, given the less reliable nature of January housing data, this is not enough evidence to signal a shift in the clear weakening trend over the second half of 2018.”

The report often comes out on the same day as NAB’s business survey, a report which also has enough importance to move markets and so the individual effect of either report is hard to judge. However, bonds yields were almost unchanged by the end of the day. The yield on 3-year ACGBs was steady at 1.61%, 10-year yields gained 1bp to 2.04% and 20-year yields remained unchanged at 2.42%.

12 March 2019

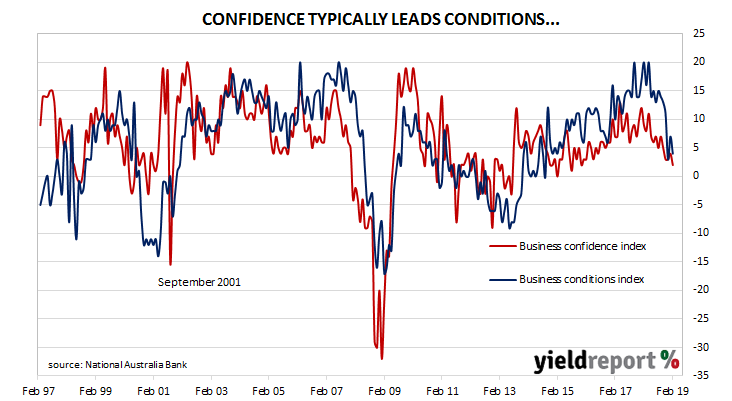

Australian business conditions were robust in the first half of 2018 and a cyclical-peak was reached in April. Then readings began to slip, although they remained well above average for some months. However, by the end of 2018, the readings had plunged to below-average levels. There was some suggestion conditions over the Christmas/New Year period may have been the result of temporary factors but the latest report puts that idea in doubt.

According to NAB’s latest monthly business survey of 400 firms conducted in the last week of February, business conditions dropped back below average after January’s bounce proved to be temporary. After several months of consecutive falls in the latter part of 2019, NAB’s conditions index bounced to 7 in January and then fell back to 4 in February. NAB chief economist Alan Oster said, “The decline in conditions was relatively broad-based in the month and continues a relatively sharp decline over the previous six months. The decline in confidence was more modest but the series has now been below average for some time. Forward orders fell to below average levels in the month, and capacity utilisation declined further suggesting that conditions are unlikely to regain much ground.”

The latest reading for the confidence index fell back from 4 to 2, a level which could be described as significantly below the long-term average reading of 6. Typically, NAB’s confidence index leads the conditions index by approximately one month, although some divergences appear from time to time. Now the two series have converged again, with the conditions index catching up to the confidence index after an eighteen-month gap.

11 March 2019

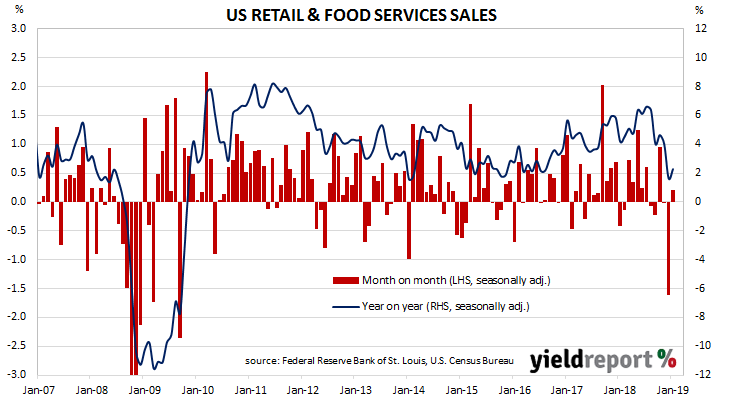

US retail sales have been trending up since late 2015. While there have been patches of weakness along the way, later months’ figures have rebounded to higher levels. After reaching an annual growth rate of 6.6% in July 2018, subsequent sales figures formed a downtrend which brought the annual rate below 2.0% by the end of the year. The latest January report has provided a rebound of sorts.

According to the latest “advance” sales numbers released by the US Census Bureau, total retail sales increased by 0.2% in January, or slightly higher than the flat result which had been expected and a good deal higher than December’s revised figure of -1.6%. On an annual basis, the growth rate increased to 2.3% after recording 1.6% in December after revisions.

ANZ senior economist Felicity Emmett said, “Markets will be looking for January’s lift to be sustained, with strength in the labour market and rising real wages expected to support consumption. Rates are close to neutral and the Fed has made it clear they do not want to quash the expansion, with cycles often ending on the back of aggressive tightening. Until they feel comfortable with the domestic and international environment, on-hold guidance will remain in place.”

ANZ senior economist Felicity Emmett said, “Markets will be looking for January’s lift to be sustained, with strength in the labour market and rising real wages expected to support consumption. Rates are close to neutral and the Fed has made it clear they do not want to quash the expansion, with cycles often ending on the back of aggressive tightening. Until they feel comfortable with the domestic and international environment, on-hold guidance will remain in place.”

08 March 2019

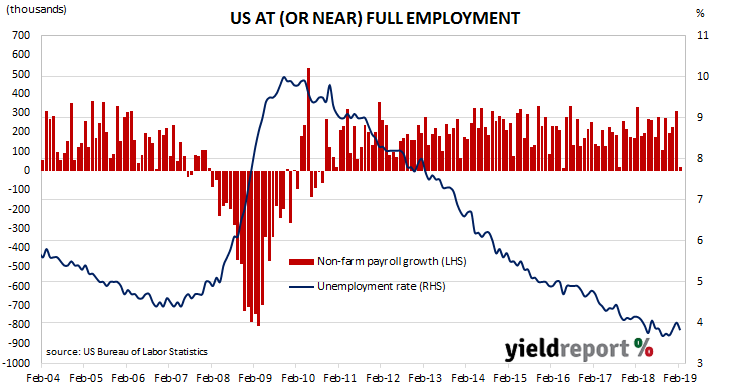

The US economy continues to produce more jobs despite the being close to full employment. The buoyant conditions have eaten into the under-employment rate and annual increases in hourly pay have hit a new post-GFC high.

According to the US Bureau of Labor Statistics, the US economy created 20,000 jobs in the non-farm sector in February. Economists had been expecting around 180,000 additional positions.

US bond yields finished the day slightly lower across the curve while the US dollar was weaker against other major currencies except for sterling. 2-year, 10-year and 30-year Treasury bond yields all slipped 1bp to 2.46%, 2.63% and 3.02% respectively.

The figures had little impact on expected Federal Reserve policy and the current expectation is of no change in the federal funds rate during 2019. However, a small probability has been assigned to a rate cut at the FOMC’s December meeting, although this possibility has been around since late last year.