28 February 2019

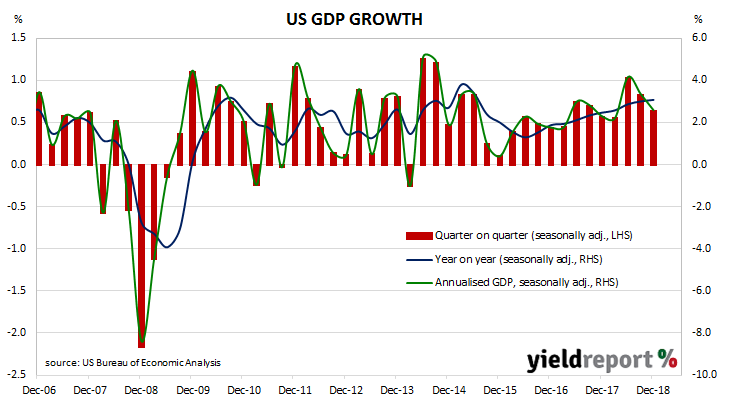

US consumer sentiment figures from December and January have painted a less-than-bright picture of US economic prospects in the near term. Accordingly, bond yields have fallen and the official rate rises are off the table. However, the latest US GDP figures for the December quarter don’t appear to be quite so bleak.

The US Commerce Department has released December quarter “advance” GDP estimates and they indicate the US economy grew at an annualised growth rate of 2.6%. (Due to the US federal shutdown, this report for the December quarter replaced the “advance” estimate originally scheduled for the end of January as well as the second estimate.)

The growth figure was just above the 2.2% median of market estimates but markedly lower than the revised September quarter figure of 3.4%. Westpac’s AM Finance team described the figures as “surprisingly resilient… despite the steep slowing in activity implied by partial data, especially in the month of December.”

ANZ senior economist Cherelle Murphy pointed to the growth of various GDP components and said they “helped soothe concerns about a broad-based slowdown in Q4”. However, she also said first quarter data to date suggest “growth may have a little more momentum to shed yet.”

27 February 2019

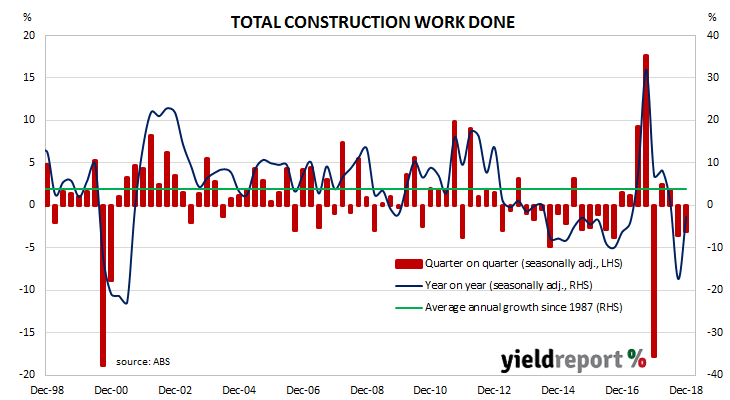

Quarterly construction data compiled and released by the ABS are not considered to be of a “primary” nature in the same way as unemployment (Labour Force) and inflation (CPI) figures. However, the figures are viewed by economists and analysts with interest as they directly feed into quarterly GDP figures.

According to the latest construction figures published by the ABS, the value of construction work has been dragged lower again. Total construction in the December quarter fell by 3.1%, which is less than the 0.5% increase expected but not as low as the revised 3.6% fall in the September quarter. On an annual basis, the growth rate recovered from September’s revised figure of -17.4% to -2.6% as the 2017 construction spike (see below) dropped out of annual calculations. Commsec chief economist Craig James said the weather played a part. “A raft of major companies have highlighted that wet and stormy weather affected activity in the quarter.”

Commsec chief economist Craig James said the weather played a part. “A raft of major companies have highlighted that wet and stormy weather affected activity in the quarter.”

The construction figures presented little in the way of pressure to move local bond yields, which had an unremarkable day as they generally followed US Treasury bonds. By the end of the day, the yield on 3-year and 10-year Australian Government bonds had each shed 2bps to 1.64% and 2.07% respectively while the 20-year yield remained unchanged at 2.46%.

26 February 2019

US consumer confidence collapsed in late 2007 as the US housing bubble burst and the US economy went into recession. By 2016, it had clawed its way back to neutral and then went from strength to strength over the next two years. After a dramatic fall in December and January, confidence levels of US households appears to have bounced back after a series of temporary factors faded from view.

The latest Conference Board survey indicates US consumers have shaken off their worries from December and January. The latest reading came in at 131.4, up from January’s revised reading of 121.7 and back to a historically high level.

The consensus expectation prior to the report was for a reading of around 124. However, despite a considerably-higher result, US bond yields still finished the day lower. 2-year, 10-year and 30-year Treasury bond yields all shed 2bps to 2.48%, 2.64% and 3.07% respectively.

A month ago, Lynn Franco, The Conference Board’s Director of Economic Indicators, had said January’s figures were likely to be affected by temporary factors. At the time, the federal shutdown had yet to be resolved and the Federal Reserve’s position on future rate rises was still a concern.

20 February 2019

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of economic activity relative to trend in Australia. The index combines certain economic variables which are thought to lead changes in economic growth into a single variable. Westpac views this variable as a reliable cyclical indicator for the Australian economy and an indicator of swings in Australia’s overall economic activity.

The six-month annualised growth rate of the indicator fell back from a revised December figure of -0.29% to -0.43% in January. These figures represent rates relative to trend-GDP growth, which is generally thought to be around 2.75% per annum. The Index is said to lead GDP by 3 months to 6 months, so theoretically the current reading represents an annualised GDP growth rate of around 2.30% in March and/or June quarters.

The major negative influences on the Index in February came from a fall in the local share market, fewer applications for home construction and lower US industrial production. Higher commodity prices and a fall in unemployment expectations amongst employees provided some offset.

Westpac chief economist Bill Evans noted the difference between the current reading and those from the middle of 2018. “The Index growth rate has shown a significant deterioration over the last six months, declining from +0.17% in August to –0.43% in January.”

19 February 2019

The RBA held the official cash rate steady at its board meeting in February, as it had for every meeting since the cash rate was reduced to 1.50% in August 2016. Statements from RBA officials in the last two years had indicated the next move was “more likely to be an increase”. However, RBA officials have made statements recently which have put that likelihood into doubt.

The release of the meeting’s minutes was not expected to provide anything particularly new. RBA chief Philip Lowe had already given an update which had provided some excitement in his speech to the National Press Club on the day after the RBA board met. The February Statement on Monetary Policy (SoMP) had then formalised the downgraded growth forecasts a few days later.

When the minutes were released, they were pretty much as anticipated. The minutes included statements very similar to Lowe’s Press Club speech regarding the importance of movements in the unemployment rate and inflation, as well as a reference to the RBA’s switch to a neutral bias.

18 February 2019

Insurance Australia Group (IAG) has all but confirmed it will issue a new security before the end of June. It also strongly hinted its RES would not be reset at the end of the year.

In its first-half report, IAG noted the December 2019 reset date and the consequent loss of regulatory capital eligibility. In the report, IAG stated, “In addition, the $550m Reset Exchangeable Securities (RES) issue has a reset date in December 2019, after which it ceases to be eligible for regulatory capital purposes. IAG may seek to issue a new Tier 2 instrument prior to 30 June 2019, subject to market conditions, to assist in refinancing the RES.”

Certainly, the intentional insertion of this paragraph is a large hint a new Tier 2 security is coming, although IAG allows itself some wriggle room with the use of the word “may” rather than the word “will”. However, it also clearly implies the RES will be redeemed. After all, the RES will lose their regulatory capital eligibility and “refinancing the RES” reads as if it is a done deal.

While assuming redemption on a call date or reset date may be a little presumptuous, convention dictates an issuer do so unless it is willing to have its reputation dented, a la the recent Banco Santander deferral. However, the Santander case itself illustrates the necessity of some caution; the very fact the issuer has an option to defer redemption should always be present in investors’ minds.

15 February 2019

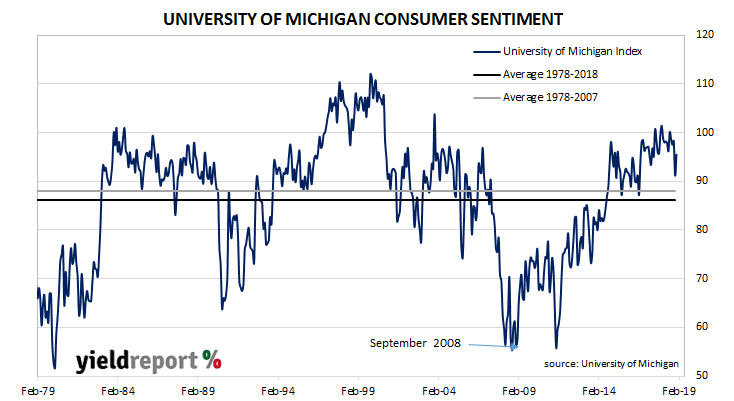

US consumer confidence has been under pressure in recent months and less-confident households are generally inclined to spend less and save more. As private consumption accounts for a majority of GDP growth in advanced economies, household spending is a major determinant of a country’s overall expenditure. Hence the concern generated by these reports.

The latest survey conducted by the University of Michigan indicates US consumers have been somewhat reassured by the end of the US federal shutdown and a likely pause in the raising of official interest rates. The result was a rebound in the University’s Index of Consumer Sentiment from a revised 91.2 in January to 95.5 in February.

The University of Michigan’s index is one of two monthly US consumer sentiment indices, the other being the Conference Board’s Consumer Confidence Survey. The University’s survey covers personal finances, business conditions and buying conditions.

The bounce was a little more than expected but bond and currency markets treated it with a degree of indifference. By the end of the day, 2-year US Treasury yields had gained 2bps to 2.52%, the 10-year yield was 1bp higher at 2.66% while 30-year yields slipped 1bp to 2.99%. The US dollar was largely unchanged against all other major currencies.

15 February 2019

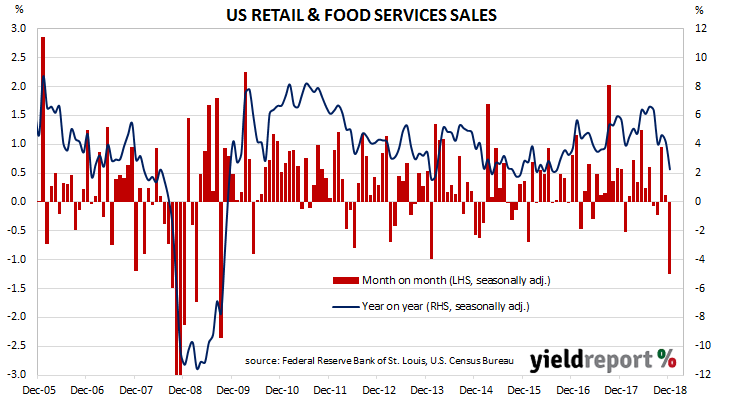

US retail sales have been trending up since late 2015. While there have been patches of weakness along the way, later months’ figures have rebounded to higher levels. After reaching an annual growth rate of 6.6% in July 2018, sales figures from the following months brought the annual rate back to a little above 4% by November, or roughly where it was at the start of that year. The latest December report has brought the annual rate even lower.

According to the latest “advance” sales numbers released by the US Census Bureau, total retail sales contracted by 1.2% in December, which is much less than the +0.1% expected and substantially lower than November’s revised figure of +0.1%. On an annual basis, the growth rate fell back to 2.3% after recording 4.1% in November after revisions.

Financial markets reacted by sending Treasury yields lower across the curve. By the end of the day, the yield on 2-year Treasury bonds had fallen 3bps to 2.50%, 10-year yields were 5bps lower at 2.65% and 30-year bond yields had lost 5bps lower to 3.00%. However, prices in the futures market for federal funds were largely unmoved. Contracts implied no chance of a rate change at the upcoming March FOMC meeting and only a slim chance of a 25bps rise at either the June or September meetings.

Financial markets reacted by sending Treasury yields lower across the curve. By the end of the day, the yield on 2-year Treasury bonds had fallen 3bps to 2.50%, 10-year yields were 5bps lower at 2.65% and 30-year bond yields had lost 5bps lower to 3.00%. However, prices in the futures market for federal funds were largely unmoved. Contracts implied no chance of a rate change at the upcoming March FOMC meeting and only a slim chance of a 25bps rise at either the June or September meetings.

13 February 2019

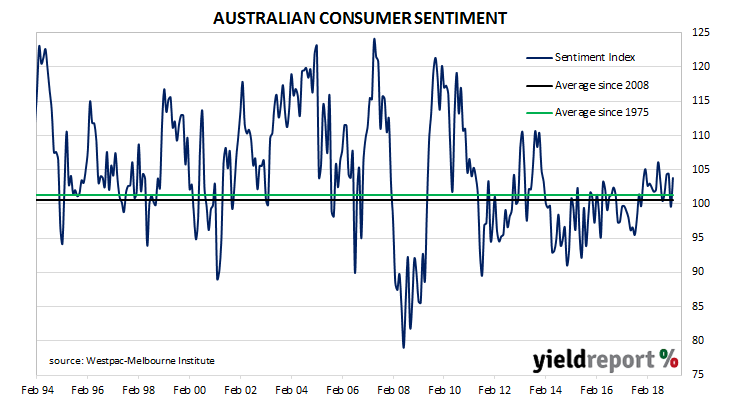

During most of the period between 2014 and 2018, a divergence between consumer sentiment and business confidence in Australia was evident. Normally, the two sectors could be expected to generally track the same path, so an extended difference between the two was somewhat unusual. Around July 2018, the two sectors converged again and, since then, they have generally been moving in line with each other.

According to the latest Westpac-Melbourne Institute survey conducted in the first week of February, average household optimism increased as the Consumer Sentiment Index recovered from January’s reading of 99.6 to 103.8. Any reading above 100 indicates the number of consumers who are optimistic is greater than the number of consumers who are pessimistic. The long-term average reading is just over 101.

Local bond yields reacted by moving higher, although how much of the change was due to the report and how much was due to higher US bond yields is debatable. By the end of the day, the yield on 3-year Treasury bonds was 3bps higher at 1.68% while 10-year and 20-year yields each increased by 4bps to 2.15% and 2.53% respectively.

13 February 2019

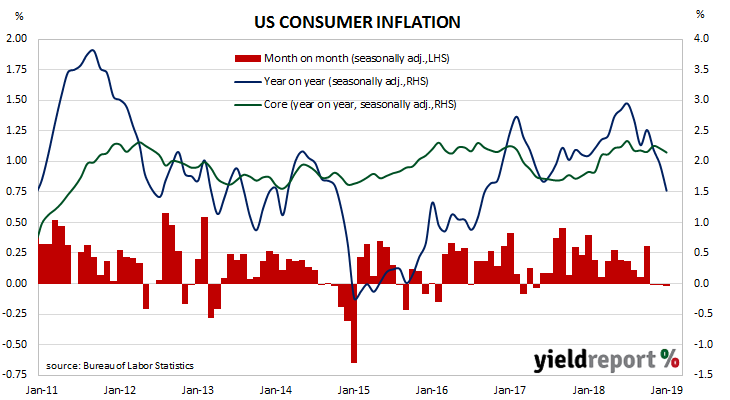

The annual rate of US consumer inflation has dropped from nearly 3% in July 2018 to well below 2% over the last couple of months. At the same time, core inflation has been much less volatile and it has ranged between 2.10% and 2.30%. In recent times, differences between the two have mostly been caused by changes in gasoline (petrol) prices.

Consumer price index (CPI) figures released by the Bureau of Labor Statistics indicated seasonally-adjusted consumer prices remained unchanged in January, less than the consensus figure of +0.1 but the same as December’s revised figure. On a 12-month basis, the consumer inflation rate slowed to 1.5% after recording 1.9% in December. The primary driver of the fall was another substantial fall in gasoline prices.

“Core” inflation, a measure of inflation which strips out the volatile food and energy components of the index, increased on a seasonally-adjusted basis by +0.2% for the month, in line with expectations. The annual rate remained unchanged at 2.2%.

Markets reacted by sending US bond yields higher. By the end of the day, 2-year Treasury yields had ticked up 1bp to 2.53%, 10-year yields had increased by 2bps to 2.70% and 30-year yields had gained 1bp to 3.03%.