12 February 2019

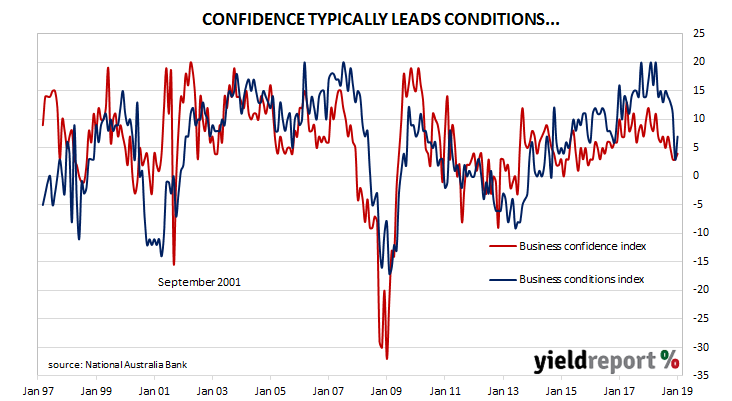

Australian business conditions were robust in the first half of 2018 and a cyclical-peak was reached in April. Then readings began to slip, although they remained well above average for some months. However, by the end of 2018, the readings had plunged to below-average levels. The latest NAB business report suggests conditions over the Christmas/New Year period may have been the result of temporary factors.

According to NAB’s latest monthly business survey of 400 firms conducted in the last week of January, business conditions improved back to above-average levels. After four months of consecutive falls, NAB’s conditions index increased from 3 in December to 7 in January. NAB chief economist Alan Oster said, “Some improvement was likely given the difficulty in addressing seasonality around the Christmas/New year period but even after this partial reversal, conditions and forward orders continue to trend lower and still show a sizeable decline over the past six months.”

ANZ senior economist Felicity Emmett agreed. “The small rebound was evident across most component indexes, although in a worrying sign for the labour market capacity utilisation continued to edge lower. Even taking into account the bounce in January, the drop in business conditions suggests a substantial loss of momentum in the economy.”

12 February 2019

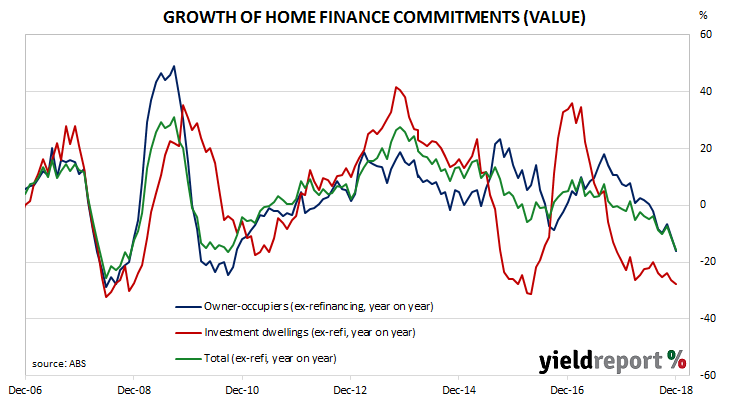

Since late 2017/early 2018, a very clear downtrend has been evident in the monthly figures of both the number and value of home loans commitments. The latest numbers have not done anything to alter this picture.

The ABS has released December housing finance commitment figures* and they were lower than expected. The total number of loan commitments to owner-occupiers fell by 6.1%, less than the expected 2% contraction and lower than November’s figure of -0.90%. On an annual basis, the growth rate deteriorated further to -11.6% after registering -7.2% in November. When “re-financings” are removed, the number of loan commitments fell by 8.2% over the month and by 14.4% when compared to commitments from December 2017.

ANZ economist Jack Chambers said, “The decline in housing finance accelerated in December, with the largest falls seen for owner-occupiers. Finance for first home buyers, which had previously outperformed other segments, fell sharply in December. Total financing is down 20% over the last year and further falls are likely in the near term.”

The report came out on the same day as NAB’s January business survey, so the individual effect of this report is hard to judge. By the close of trade, the yield on 3-year ACGBs had gained 4bps to 1.65% while 10-year and 20-year yields had each increased by 5bps to 2.11% and 2.49% respectively. In the cash futures market, the reaction was modest and contract prices moved in a direction which indicates a lower likelihood of a rate cut later this year or in the first half of 2020.

12 February 2019

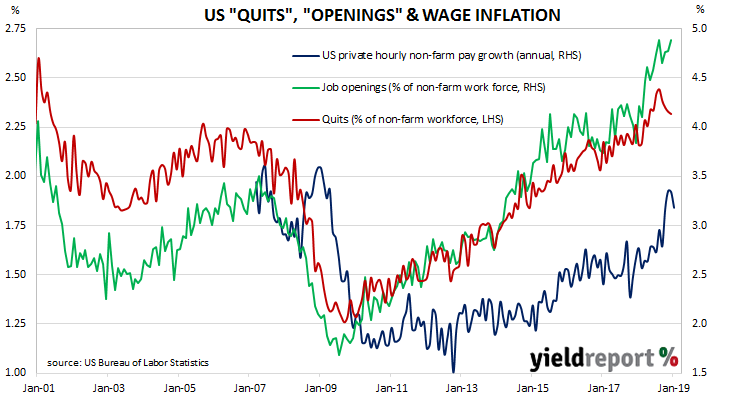

In August 2018, the quit rate as a percentage of total US non-farm employment reached a new series-high. Since then, it has fallen back, although by not enough to break the trend.

Figures released as part of the most recent JOLTS report show the quit rate has remained stable for a third consecutive month. During December, 2.3% of the non-farm workforce left their jobs voluntarily, the same rate as in November and October after rounding to one decimal place. Quit rates were highest in the professional/business services and health care sectors while the “other services”, (maintenance and servicing) and retail sectors recorded the largest falls. Overall, the total number of quits slipped from November’s revised figure of 3.49 million to 3.48 million.

Job openings moved in the other direction. Total vacancies during December increased from November’s revised figure of 7.17 million to 7.34 million, led by increased openings in the construction and accommodation/food services sectors. Openings in the retail, manufacturing and federal government sectors were all noticeably lower.

Job openings moved in the other direction. Total vacancies during December increased from November’s revised figure of 7.17 million to 7.34 million, led by increased openings in the construction and accommodation/food services sectors. Openings in the retail, manufacturing and federal government sectors were all noticeably lower.

Treasury bond yields mostly increased. By the end of the day, the yield on US 2-year Treasury bonds were unchanged at 2.50% while the 10-year yield had increased by 3bps to 2.68% and the 30-year yield finished up 2bps at 3.02%. According to federal funds futures prices, the probability of a rate rise before the December FOMC meeting remained under 5%.

06 February 2019

RBA chief Philip Lowe gave a speech with the title “The Year Ahead” to the National Press Club of Australia in Sydney on Wednesday. Most of it was similar to a cut-down version of the minutes of any RBA Board meeting. However, there were two sentences which had quite an effect on yields in local bond and cash markets.

“Looking forward, there are scenarios where the next move in the cash rate is up and other scenarios where it is down.” This sentence itself was unremarkable; of course, there are small and unlikely possibilities. However, for some time the RBA had held a bias towards higher official rates.

Close to the end of January, RBA Board member Ian Harper had said he personally viewed the next move of the cash rate as likely to be an increase. The minutes of recent Board meetings had been a little less assertive but there was not a great deal of difference. According to the minutes of the December meeting, “…the next move in the cash rate was more likely to be an increase than a decrease, but that there was no strong case for a near-term adjustment in monetary policy.”

05 February 2019

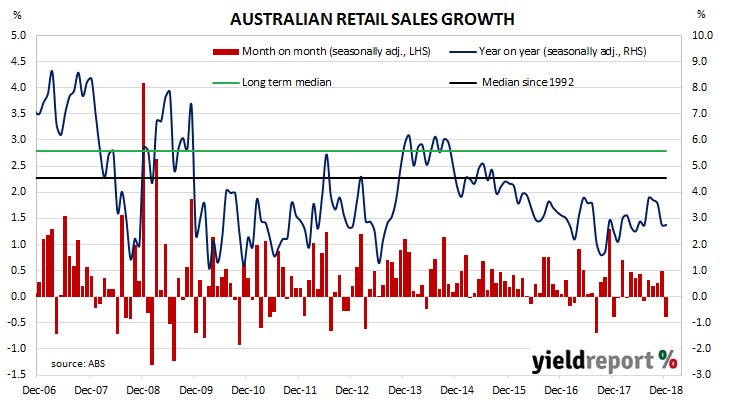

Retail sales figures have been lacklustre for the past couple of years but in 2018 the annual growth rate showed some signs of stabilising, albeit at a low rate. While recent months’ figures have been generally in line with or above market expectations, the latest month’s figures have come as a negative surprise.

According to the latest ABS figures, total retail sales fell by 0.4% over December on a seasonally-adjusted basis, below the expected flat result and a marked drop from November’s revised figure of +0.5%. On an annual basis, retail sales increased by 2.8%, the same as November’s comparable figure.

Westpac senior economist Matthew Hassan said, “Overall, this was a weak update, slightly weaker than we had been anticipating and highlighting downside risks to the December quarter GDP.”

Despite the report’s “miss”, reactions in local financial markets was unremarkable. By the end of the day, the yield on 3-year and 20-year ACGBs had both crept up 1bp to 1.75% and 2.61% respectively while 10-year yields had gained 2bps to 2.25%.

Despite the report’s “miss”, reactions in local financial markets was unremarkable. By the end of the day, the yield on 3-year and 20-year ACGBs had both crept up 1bp to 1.75% and 2.61% respectively while 10-year yields had gained 2bps to 2.25%.

In the forex market, the Aussie dollar dropped by around 0.15 US cents immediately upon the release of the report and then slowly recovered back to 72.10 US cents. It jumped by around 0.5 US cents after the RBA meeting to finish the afternoon session at close to 72.65 US cents.

In terms of local monetary policy, prices of cash futures contracts were largely unchanged from the previous day. May contracts implied a 12% chance of a rate cut, August contracts implied a 28% chance and November contracts implied a 48% chance.

04 February 2019

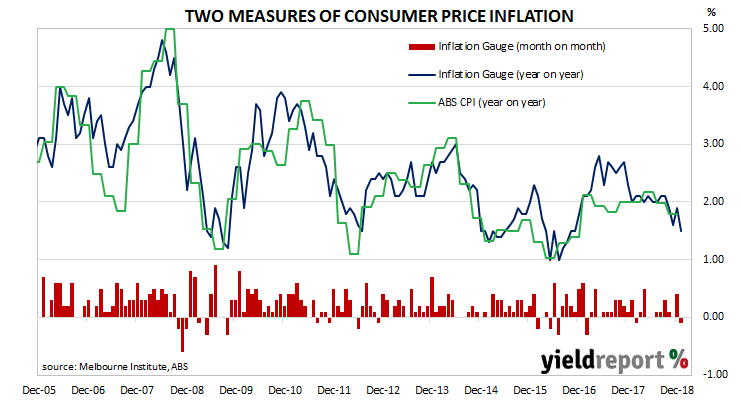

The Melbourne Institute’s Inflation Gauge is an attempt to replicate the ABS consumer price index (CPI) on a monthly basis. It has turned out to be a reliable leading indicator of the CPI, although there are periods in which the Inflation Gauge and the CPI have diverged for as long as twelve months. On average, the Inflation Gauge’s annual rate tends to overestimate changes in CPI inflation by an average of about 0.10% in any given quarter.

The Inflation Gauge slipped back by 0.1% during January after a 0.40% increase in December and a flat result in November. On an annual basis, the index increased by 1.5%.

04 February 2019

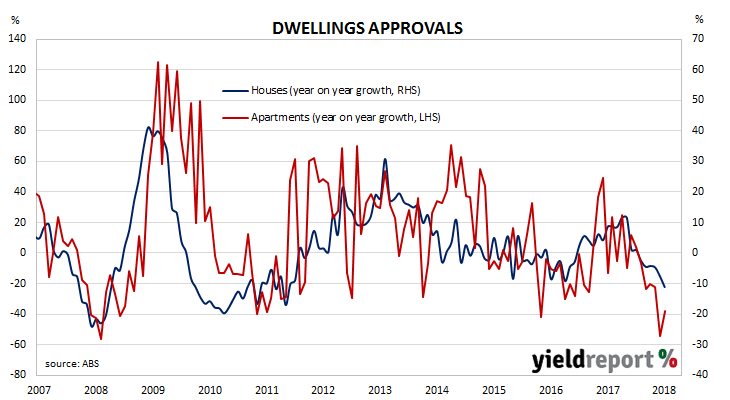

Aside from engineering and architectural design, one of the earliest requirements of a building project is to obtain approval from the relevant statutory body. While not all projects which have been approved are completed, all completed projects have been granted approval. Approvals data thus provides a useful indicator of future construction activity.

The latest building approval figures have been released for December by the Australian Bureau of Statistics and they indicate the downtrend which started in July had continued. Seasonally-adjusted, total approvals fell by 8.4% in December, which is well under the market consensus figure of +2.0% but an improvement on November’s revised figure of -9.8%. On an annual basis, total approvals fell by 22.5%, as compared to November’s comparable figure of -33.5% after revisions.

Local financial markets’ reactions were modest but there was also an ANZ Job Ads report and a Melbourne Institute Inflation Gauge report with which to contend. By the end of the Australian trading day, 3-year, 10-year and 20-year Treasury bond yields were all 2bps higher at 1.74%, 2.23% and 2.60% respectively. Cash futures prices were essentially unchanged and a bias towards a rate cut in late 2019 or early 2020 remained in place. The Aussie dollar finished the afternoon session about 0.2 US cents lower at 72.30 US cents.

04 February 2019

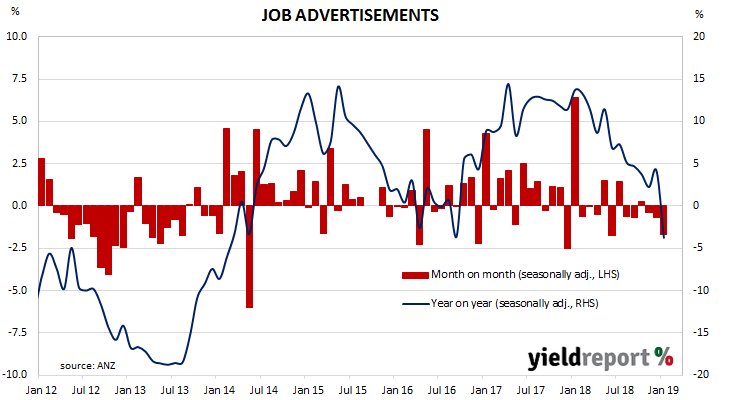

ANZ’s job advertisement survey is well-known as a leading indicator of employment numbers in Australia. As such, it is inversely related to the unemployment rate. ANZ’s survey reflects changes in demand for labour and it provides another measure of activity in the economy. There is also a fairly good inverse relationship between changes in Australia’s unemployment rates and changes in the RBA cash rate. Understanding the path of Australia’s unemployment rate has historically provided a reliable indicator of RBA rate changes.

From mid-2017 onwards, year-on-year growth rates in the total number of advertisements consistently exceeded 10%. That was until mid-2018 when the annual growth rate fell back markedly and then tracked lower for the remainder of 2018.

January’s figures have now been released and, after revisions and seasonal adjustments, total advertisements fell by 1.7% to 171,392. On a 12-month basis, total job advertisements shrank by 3.7%, the first time the annual rate has gone into negative territory since September 2016.

Local financial markets’ reactions were modest but there was also a December dwellings approval report and a Melbourne Institute Inflation Gauge report with which to contend. By the end of the Australian trading day, 3-year, 10-year and 20-year Treasury bond yields were all 2bps higher at 1.74%, 2.23% and 2.60% respectively. Cash futures prices were essentially unchanged; a bias towards a rate cut in late 2019 or early 2020 remained in place. The Aussie dollar finished the afternoon session about 0.2 US cents lower at 72.30 US cents.

Local financial markets’ reactions were modest but there was also a December dwellings approval report and a Melbourne Institute Inflation Gauge report with which to contend. By the end of the Australian trading day, 3-year, 10-year and 20-year Treasury bond yields were all 2bps higher at 1.74%, 2.23% and 2.60% respectively. Cash futures prices were essentially unchanged; a bias towards a rate cut in late 2019 or early 2020 remained in place. The Aussie dollar finished the afternoon session about 0.2 US cents lower at 72.30 US cents.

01 February 2019

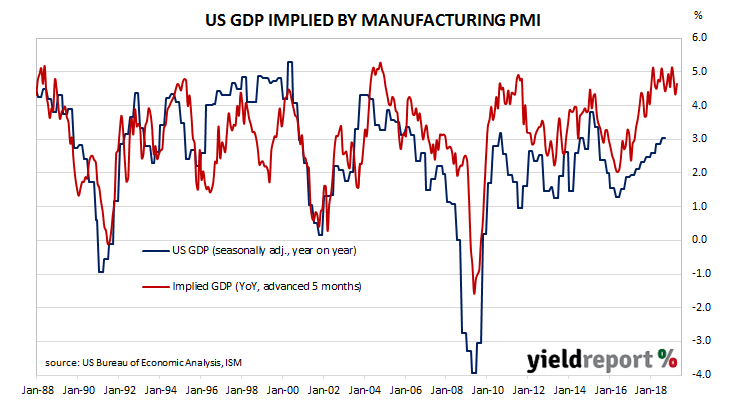

Purchasing Managers’ Indices (PMIs) are economic indicators derived from monthly surveys of purchasing and supply executives in private sector companies. They are diffusion indices, which means a reading of 50% represents no change from the previous period, while a reading under 50% implies respondents on average reported a deterioration. Their usefulness lay in being a leading indicator of GDP.

US manufacturing activity partially recovered in January after a large fall in December. According to the Institute of Supply Management (ISM) January survey, its Purchasing Managers Index recorded a reading of 56.6, up from December’s reading of 54.3 and more than the expected figure, which was also 54.3. The average reading since 1948 is 52.9.

US bond yields finished the day higher while the US dollar was largely unchanged against other major currencies. 2-year Treasury bond yields finished 3bps higher at 2.49%, 10-year yields increased by 5bps to 2.68% and 30-year yields were 3bps higher at 3.03%.

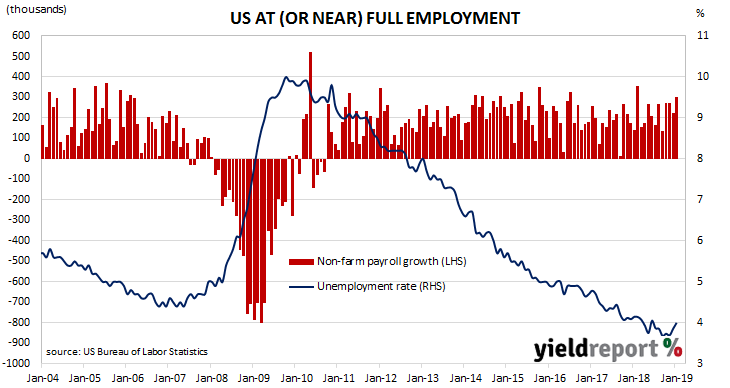

01 February 2019

The US economy continues to produce more jobs despite being close to full employment. However, the buoyant conditions are enticing Americans back into the workforce, which increases the unemployment rate in some months.

According to the US Bureau of Labor Statistics, the US economy created 304,000 jobs in the non-farm sector in January. Economists had been expecting around 165,000 additional positions and US markets reacted by sending bond yields higher.

US bond yields finished the day higher across the curve while the US dollar was largely unchanged against other major currencies. 2-year Treasury bond yields finished 3bps higher at 2.49%, 10-year yields increased by 5bps to 2.68% and 30-year yields were 3bps higher at 3.03%.

US bond yields finished the day higher across the curve while the US dollar was largely unchanged against other major currencies. 2-year Treasury bond yields finished 3bps higher at 2.49%, 10-year yields increased by 5bps to 2.68% and 30-year yields were 3bps higher at 3.03%.

The figures had little impact on expected Federal Reserve policy as the probability of rate rises had already been pruned right back. According to cash futures prices, the implied probability of a rate rise by the US FOMC at its March meeting moved from just 2% to zero while the chance of a June rate rise also moved to zero.