14 January 2019

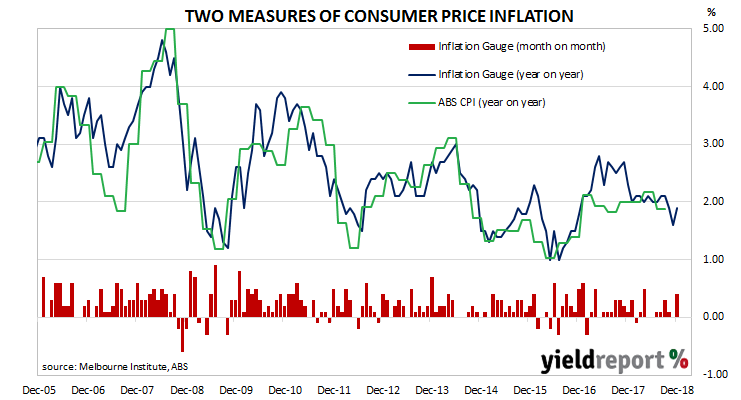

The Melbourne Institute’s Inflation Gauge is an attempt to replicate the ABS consumer price index (CPI) on a monthly basis instead of a quarterly one. In the last few years, it has suggested higher inflation rates were to come, only to reverse course and fall back in line with official figures.

The Inflation Gauge increased by 0.4% during December after a flat result in November and a 0.10% increase in October. On an annual basis, the index increased by 1.9%, a rate which is a considerable jump from November’s 1.6%.

Bond yields finished the day lower, almost in line with leads from overnight US markets. Yields on 3-year, 10-year and 20-year ACGBs all fell by 3bps to 1.77%, 2.28% and 2.66% respectively. The Aussie dollar moved a little lower during the day and finished at 72.00 US cents.

11 January 2019

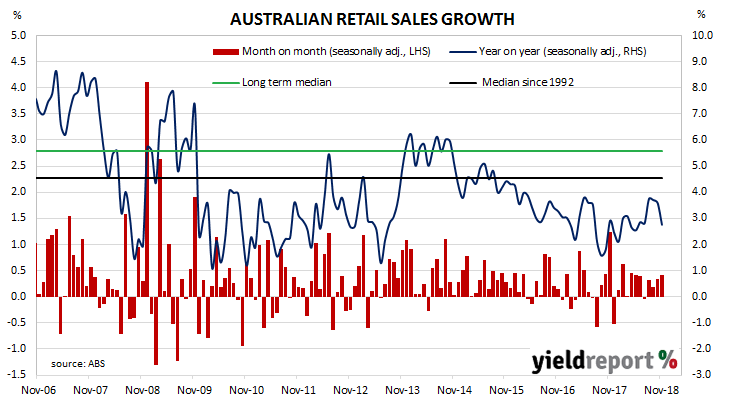

Retail sales figures have been lacklustre for the past couple of years but in 2018 the annual growth rate showed some signs of stabilising, albeit at a low rate. Recent months’ figures have been generally in line with or above market expectations. However, they have not been high enough to change a common view amongst economists of a household sector under pressure from high debt levels and low rates of income growth.

According to the latest ABS figures, total retail sales increased by +0.4% over November on a seasonally-adjusted basis, in line with the expected figure and an increase from October’s +0.3%. However, on an annual basis, retail sales increased by only 2.8%, a lower figure than the 3.6% annual rate recorded for October. Local bond yields finished the day largely unchanged. By the end of the day, the yield on 3-year ACGBs remained unchanged at 1.80%, while 10-year yields had slipped 1bp to 2.31% and 20-year ACGBs had edged up 1bp to 2.69%.

Local bond yields finished the day largely unchanged. By the end of the day, the yield on 3-year ACGBs remained unchanged at 1.80%, while 10-year yields had slipped 1bp to 2.31% and 20-year ACGBs had edged up 1bp to 2.69%.

11 January 2019

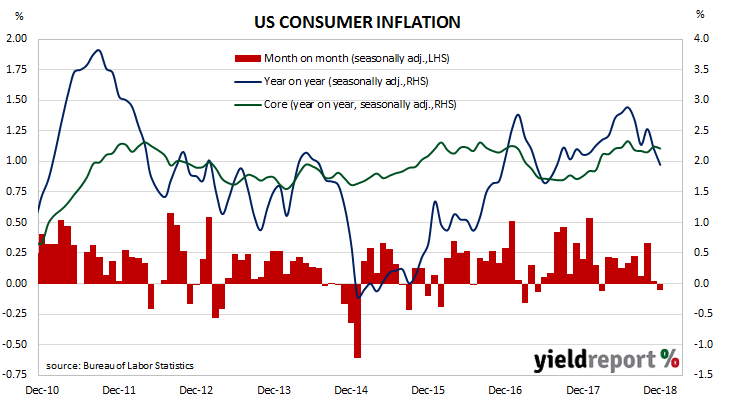

The annual rate of US consumer inflation has dropped below 2% for the first time since July 2017. While the annual inflation rate had trended higher through the 2018 financial year, a string of soft inflation results from July onwards has brought the consumer inflation rate from close to 3% to back below 2% in less than six months.

Consumer price index (CPI) figures released by the Bureau of Labor Statistics indicated seasonally-adjusted consumer prices fell by 0.1% in December, down from November’s flat result but in line with consensus expectations. On a 12-month basis, the consumer inflation rate slowed to 1.9% after falling to 2.2% in November. The primary driver of the fall was a substantial fall in gasoline prices.

09 January 2019

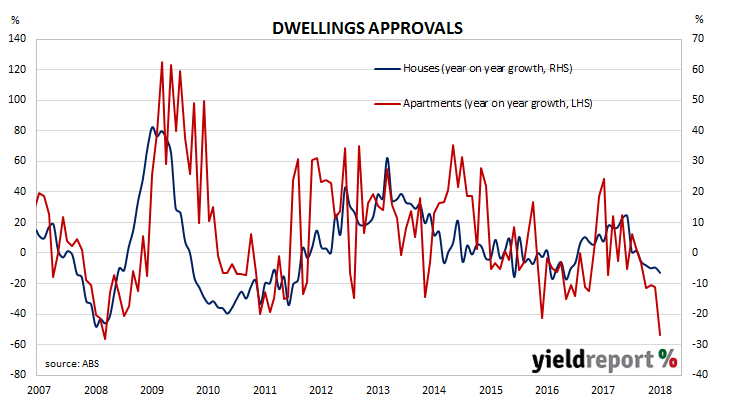

Aside from engineering and architectural design, one of the earliest requirements of a building project is to obtain approval from the relevant statutory body. As a result, building approvals data is a leading economic indicator of future construction. While not all projects which have been approved are completed, all completed projects have been granted approval. Approvals data thus provides a useful indicator of future construction activity.

The latest building approval figures have been released for November by the Australian Bureau of Statistics and they indicate the downtrend which started in July had continued. Seasonally-adjusted, total approvals fell by 9.1% in November, which is well under the market consensus figure of -0.3% and substantially below October’s 1.4% fall. On an annual basis, total approvals fell by 32.8%, a substantial deterioration from October’s comparable figure of -13.0% after revisions.

08 January 2019

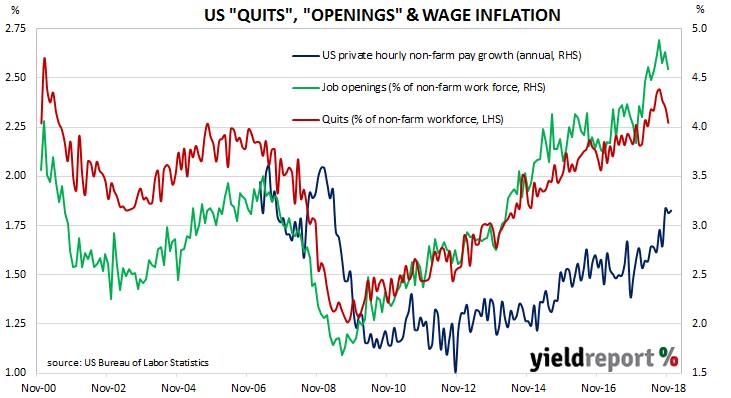

The “quits” rate time series produced by the Job Openings and Labor Turnover Survey (JOLTS) is a leading indicator of US hourly pay. As wages account for around 55% of a product’s or service’s price in the US, wage inflation and overall inflation rates tend to be closely related. Former Federal Reserve chief Janet Yellen was known to pay close attention to the quit rate.

Figures released as part of the most recent JOLTS report show the quit rate fell for a third consecutive month. During November, 2.3% of the non-farm workforce left their jobs voluntarily, the same rate as in October but only after rounding to one decimal place. Quit rates were highest in the health care and construction sectors while the professional/business services and accommodation/food services sectors recorded the largest falls. Overall, the total number of quits fell from October’s revised figure of 3.52 million to 3.41 million.

14 December 2018

Retail sales account for a large part of consumer spending, which itself is typically the largest segment of GDP in an advanced economy. Changes in retail sales have a large effect on GDP growth rates and thus they are of great interest to economists, policy makers and financial markets.

US retail sales have been trending up since late 2015. While there have been patches of weakness along the way, later months’ figures have rebounded to higher levels. After reaching an annual growth rate of 6.6% in July, sales figures from the following months have brought the annual rate back to a little above 4%, or roughly where it was at the start of the year.

According to the latest “advance” sales numbers released by the US Census Bureau, total retail sales grew by 0.2% in November, which is more than the +0.1% expected but substantially lower than October’s revised figure of +1.1%. On an annual basis, the growth rate fell back to 4.2% after recording 4.8% in October

12 December 2018

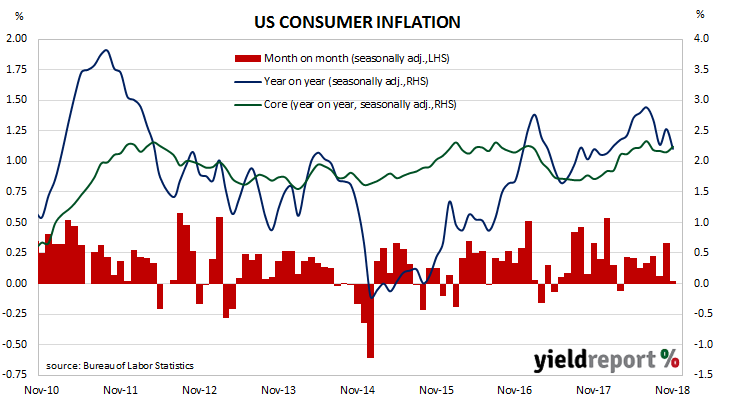

The annual rate of US consumer inflation has fallen back in November after a short-lived bounce in October.

Consumer price index (CPI) figures released by the Bureau of Labor Statistics indicated seasonally-adjusted consumer prices remained unchanged in November, down from October’s +0.3% but in line with consensus expectations. On a 12-month basis, the consumer inflation rate slowed to 2.2% after rebounding to 2.5% in October.

“Core” inflation, a measure of inflation which strips out the volatile food and energy components of the index, increased on a seasonally-adjusted basis by +0.2% for the month, also in line with expectations. The annual rate remained unchanged at 2.2% for a fourth consecutive month.

Westpac senior currency strategist Sean Callow said although the headline rate was above 2%, it was worth being aware “this measure consistently runs higher than the Fed’s preferred inflation measure, the personal consumption expenditure (PCE) deflator.” US PCE inflation has been running at less than 2% on an annual basis consistently since early 2012, although it did hit the US Fed’s 2% target in July.

12 December 2018

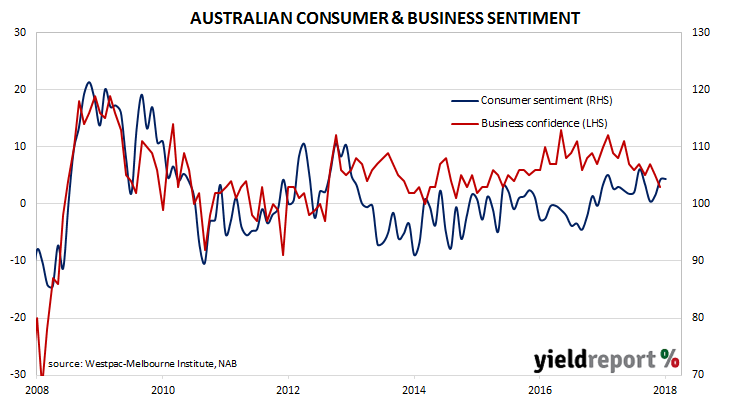

During most of the period between 2014 and 2018 a divergence between consumer sentiment and business confidence in Australia was evident. Normally, the two sectors could be expected to generally track the same path, so an extended difference between the two was somewhat unusual. However, around July 2018, the two sectors converged again only to go their separate ways again in September. This latest survey has the consumer sector holding up while the business sector shows some signs of weakness.

According to the latest Westpac-Melbourne Institute survey conducted early in December, average household optimism fractionally increased as the Consumer Sentiment Index crept up from November’s reading of 104.3 to 104.4. Any reading above 100 indicates the number of consumers who are optimistic is greater than the number of consumers who are pessimistic. The long-term average reading is just over 101.

According to the latest Westpac-Melbourne Institute survey conducted early in December, average household optimism fractionally increased as the Consumer Sentiment Index crept up from November’s reading of 104.3 to 104.4. Any reading above 100 indicates the number of consumers who are optimistic is greater than the number of consumers who are pessimistic. The long-term average reading is just over 101.

11 December 2018

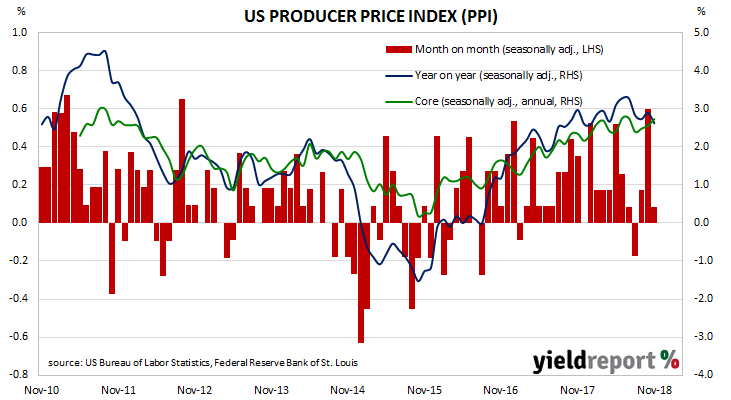

The producer price index (PPI) is a measure of prices charged by producers for domestically produced goods, services, and construction. In the US, it is constructed by the Bureau of Labor Statistics in a fashion similar to the consumer price index (CPI) except it measures prices received from the producer’s perspective. It is another one of the various measures of inflation tracked by the US Fed, along with core personal consumption expenditure (PCE) data.

The latest figures for November have been published by the Bureau and they indicate producer prices increased by 0.1% during the month after seasonal adjustments. The result was above expectations but quite a bit lower than October’s 0.6% increase. On a 12-month basis, the rate of producer price inflation after seasonal adjustments fell back to 2.6% after recording 2.9% in October and 2.7% in September.

“Core” PPI inflation, increased on a seasonally-adjusted basis by +0.3% for the month. On an annual basis, the rate ticked up from October’s revised rate of 2.6% to 2.7% in November.

11 December 2018

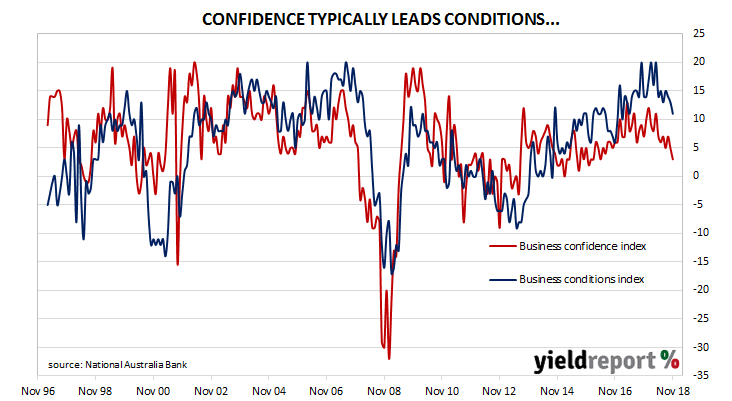

Australian business conditions were robust in the first half of 2018, especially so in April when one index registered an all-time high. Readings then slipped back over the next couple of months but they have still remained at above-average levels to date. On the other hand, business confidence has trended down since mid-2017.

According to NAB’s latest monthly business survey of 400 firms conducted in the last week of November, business conditions have remained at a healthy level despite three months of consecutive falls. After revisions, the index fell from a revised value of 13 in October to 11 at the end of November. NAB chief economist Alan Oster said, “Since around mid-2018 it appears the business sector has lost some momentum…” While he acknowledged current activity levels are “reasonable”, lower confidence index readings suggest “businesses’ outlook is for momentum to ease further.”

Typically, NAB’s confidence index leads the conditions index by approximately one month, although in recent months the two surveys have diverged and the conditions index has led the confidence index higher in trend terms since late 2014. However, the business confidence index peaked in April 2017 and it has since trended lower. The conditions index peaked later in 2017 and did not exceed this reading again. It has since trended lower, indicating the confidence index may have resumed its leading indicator capacity once more. After revisions, the confidence index fell by 2 points to register 3 on the index in November. The long-term average value is 6, so it is not that far below average. However, as ANZ senior economist Daniel Gradwell put it, “ongoing declines of this scale would become a concern.”