29 November 2018

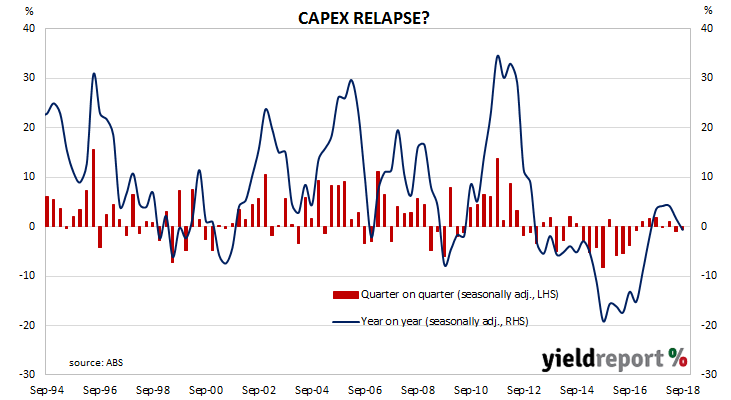

After the March report, Australia’s capital expenditure (capex) slump appeared to have come to an end. Mining investment had increased as a proportion of GDP for the first time since June 2014 and total investment had grown at an annual pace above 4% for a second consecutive quarter. June figures then created some doubt regarding the sustainability of such a recovery when they recorded a fall for the quarter.

According to the latest ABS figures, seasonally-adjusted private sector capex in the September quarter contracted by 0.5%, an improvement on the revised 0.9% fall recorded in the June quarter but lower than the 1.0% increase which was expected. On a year-on-year basis, the growth rate dropped to -0.6% after recording +1.7% in the June quarter after revisions.

Local financial markets reacted in a mixed fashion. By the end of the Australian trading day, 3-year and 10-year Treasury bond yields were both 2bps lower at 2.09% and 2.61% respectively. The Aussie dollar drifted lower after the report but it was largely unaffected and actually ended the afternoon session about 0.2 US cents higher at 73.20 US cents.

Local financial markets reacted in a mixed fashion. By the end of the Australian trading day, 3-year and 10-year Treasury bond yields were both 2bps lower at 2.09% and 2.61% respectively. The Aussie dollar drifted lower after the report but it was largely unaffected and actually ended the afternoon session about 0.2 US cents higher at 73.20 US cents.

28 November 2018

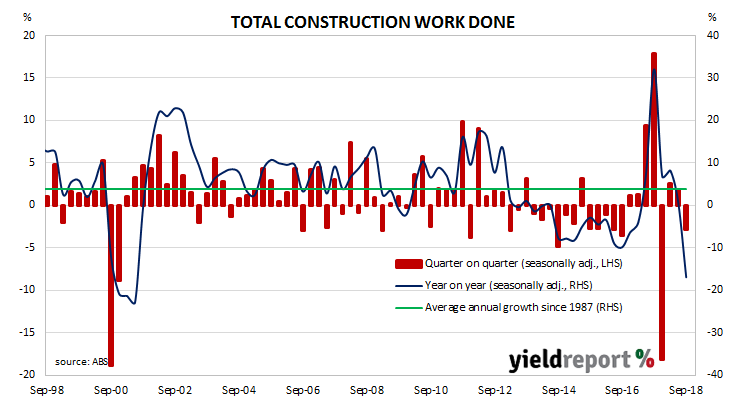

Quarterly construction data compiled and released by the ABS are not considered to be of a “primary” nature in the same way as unemployment (Labour Force) and inflation (CPI) figures. However, the figures are viewed by economists and analysts with interest as they directly feed into quarterly GDP figures.

According to the latest construction figures published by the ABS, the value of construction work has been dragged lower in the September quarter as industrial projects come to an end. Total construction in the September quarter fell by 2.8%, which is lower than the 1.0% increase expected and less than the revised +1.8% increase in the June quarter. On an annual basis, the growth rate dropped back from June’s revised figure of +0.8% to -16.9% as the September 2017 spike forms the base for annual calculations.

Australian Government bond yields had a quiet day. Offshore yields were slightly higher overnight and the construction figures provided little pressure to move yields one way or another. The yield on 3-year Australian Government bonds remained unchanged at 2.11% while the 10-year yield slipped 1bp to 2.63%. The Aussie dollar was also largely unaffected and it finished the afternoon session around 0.1 US cents higher at 72.40 US cents.

27 November 2018

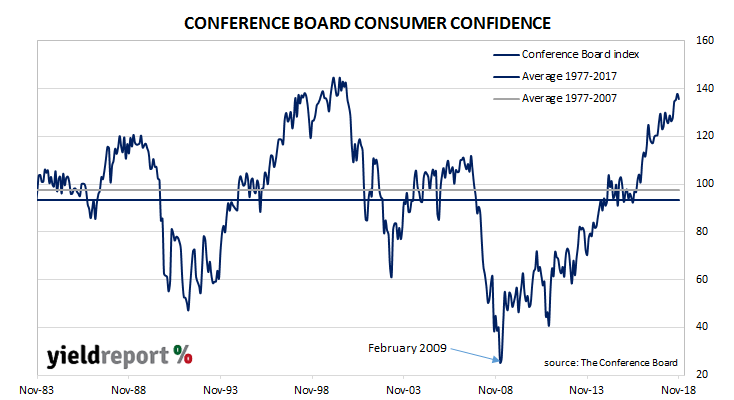

US consumer confidence collapsed in late 2007 as the US housing bubble burst and the US economy went into recession. Only in 2016, eight years later, did it claw its way back to neutral. Since then, US household confidence has trended higher and higher.

The latest Conference Board survey indicates US consumers remain very optimistic. The reading came in at 135.7, down from October’s reading of 137.9 but still well up on September 2017’s comparable figure of 129.5. It is still among the highest readings produced since the survey began in the 1960s.

US bond yields finished the day a touch higher. 2-year, 10-year and 30-year Treasury bond yields all added 1bp to 2.84%, 3.06% and 3.32% respectively.

21 November 2018

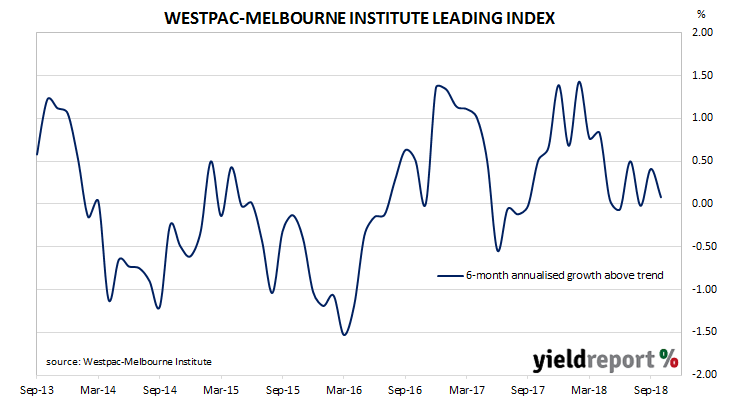

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of economic activity relative to trend in Australia. The index combines certain economic variables which are thought to lead changes in economic growth into a single variable. This variable is claimed to be a reliable cyclical indicator for the Australian economy and an indicator of swings in Australia’s overall economic activity.

The six-month annualised growth rate of the indicator fell back from a revised September figure of +0.41% to 0.08% in October. These figures represent rates relative to trend-GDP growth, which is generally thought to be around 2.75% per annum for Australia. The Index is said to lead GDP by 3 months to 6 months, so theoretically the current reading represents an annualised GDP growth rate of just above 2.75% in the December and/or March quarters.

Westpac chief economist Bill Evans said, “With this latest slowdown, the Index growth rate continues to point to slowing momentum into the new year.”

20 November 2018

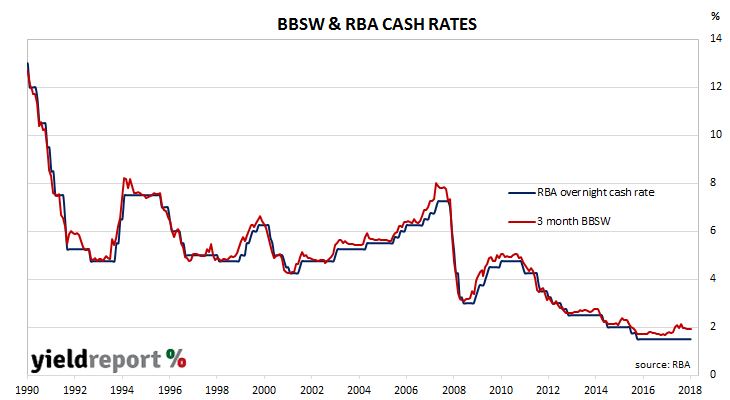

The RBA held the official cash rate steady at its board meeting in November, as it had for every meeting since the cash rate was reduced to 1.50% in August 2016. Statements from RBA officials in the last two years indicate the next move is likely to be up but, at the same time, those statements do not hint at the timing of any such move. Minutes of the November meeting indicate there is little reason to expect any change soon.

Expectations prior to the document’s release were minimal. Rate changes are not expected until mid-to-late 2019 at the earliest and minutes of previous meetings have repeatedly stated a lack of “strong case for a near-term adjustment in monetary policy”. However, economists and other observers view RBA board meetings as a chance for the RBA to signal changes in the path of the overnight cash rate.

While the minutes did not provide any surprises, they did indicate the RBA is confident of its forecasts for employment, GDP growth and inflation. There has been a marked difference between the RBA’s forecasts and those of private sector economists in recent times; the RBA’s forecasts have generally been more optimistic than the forecasts from economists from local banks and other financial institutions. To date, both sides have stuck to their respective positions and neither side appears to be budging.

15 November 2018

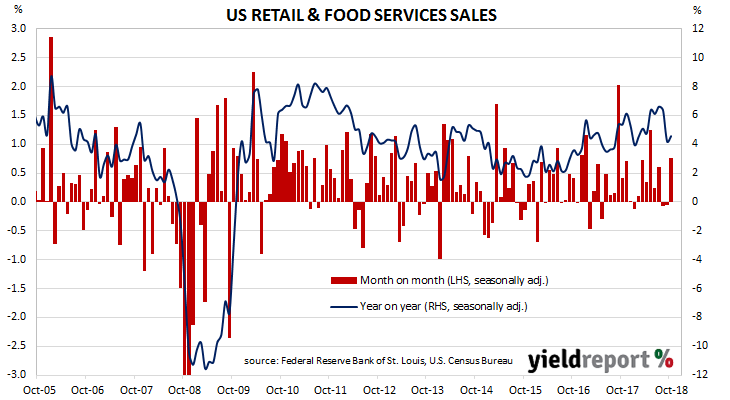

Retail sales account for a large part of consumer spending, which itself is typically the largest segment of GDP in an advanced economy. Changes in retail sales have a large effect on GDP growth rates and thus they are of great interest to economists, policy makers and financial markets.

US retail sales have been trending up since late 2015. While there have been patches of weakness along the way, later months’ figures have rebounded to higher levels. After reaching an annual growth rate of 6.6% in July, sales figures from August and September brought the annual rate back to 4.2%, a rate just above those during a similar trough at the start of the year.

According to the latest “advance” sales numbers released by the US Census Bureau, total retail sales grew by 0.8% over the month, which is more than the +0.5% expected and well up from September’s revised figure of -0.1%. On an annual basis, the growth rate increased from September’s revised figure of 4.2% to 4.6% in October.

14 November 2018

During most of the period between 2014 and 2018 there has been a divergence between consumer sentiment and business confidence in Australia. The two sectors appeared to have converged again in July but then September’s survey indicated consumer sentiment had deteriorated while business sentiment had recovered slightly. This latest survey suggests the two sectors may have once again synchronised with each other.

According to the latest Westpac-Melbourne Institute survey conducted early in October, households’ levels of optimism increased as the Consumer Sentiment Index moved up from October’s reading of 101.5 to 104.3. Any reading above 100 indicates the number of consumers who are optimistic is greater than the number of consumers who are pessimistic. The long-term average reading is just over 101.

Westpac’s chief economist Bill Evans initially seemed perplexed. “This is a surprisingly strong result. In particular, respondents are much more positive about their own finances. That is despite consistent reports around weakness in the housing markets in the major capitals and the sharp falls in the equity market through October. However, there may be an explanation. “Low interest rates and their prospect of being sustained for some time are clearly supporting confidence. For example, the confidence of those respondents with a mortgage increased by 4.3%.”

14 November 2018

Not all that long after the AOFM got out of the RMBS market, the Commonwealth appears ready to return. The Federal Government has announced it will establish a $2 billion fund to purchase securities backed by loans to small and medium-sized enterprises (SMEs).

The new fund, known as the Australian Business Securitisation Fund, will be created to increase the ease at which lenders to SMEs can finance loans of this type. In effect, it will add to demand these sorts of securities, thus allowing issuers to increase the supply without driving the price down (and the yield up). Alternatively, if the supply of securities from issuers does not increase, the additional demand will drive the price up, thus reducing the cost (yield) to issuers. In any event, lenders will have an incentive to increase lending to SMEs.

While the Federal Government’s sentiment is noble, anyone with a knowledge of the Tricontinental and State Bank of South Australia debacles in the late 1980s will be concerned. Non-performing loans provided by government-owned institutions to the business sector were behind the demise of each and eventually, tax-payers footed the bill. A less-generous interpretation of the government’s proposal is that it is just another version of a price-support scheme for holders of securities backed by loans to SMEs.

13 November 2018

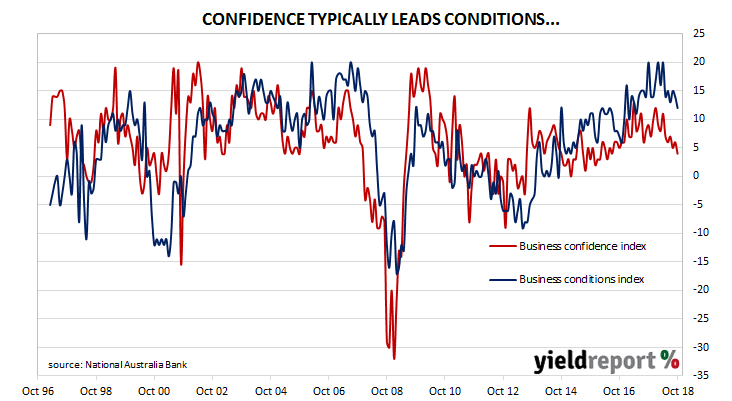

Australian business conditions were robust in the first half of 2018, especially so in April when one index registered an all-time high. Readings then slipped back over the next couple of months but they have still remained at above-average levels to date.

According to NAB’s latest monthly business survey of 400 firms conducted in the last week of October, business conditions have remained at a healthy level despite being lower than in September. After revisions, the index fell from a revised value of 14 in September to 12 at the end of October. NAB chief economist Alan Oster said, “Business conditions have eased back from the high levels seen earlier in the year but remain well above average.”

Typically, NAB’s confidence index leads the conditions index by approximately one month, although in recent months the two surveys have diverged and the condition index has led the confidence index higher in trend terms since late 2014. After revisions, the confidence index fell by 2 points to register 4 on the index in October. A reading at this level suggests business confidence is a touch on the low side but still not far from the long-term average value of 6.

09 November 2018

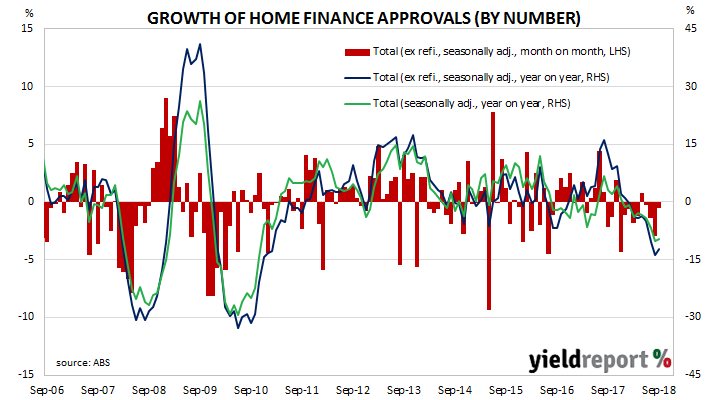

The Australian Bureau of Statistics (ABS) collects data on housing finance commitments made by significant lenders and their figures include secured (mortgage) finance commitments for the construction or purchase of owner-occupied dwellings and investment properties. It has some overlap with the RBA’s monthly private sector credit statistics which also includes investor lending and owner-occupier lending.

The ABS has released housing finance figures for September and they were in line with expectations. Total approvals fell by 1.0%, down from August’s -2.2% after revisions. On an annual basis, the growth rate recovered a touch from a revised figure of -10.2% in August to -9.7% in September. When refinancing approvals are removed, approvals fell by 0.5% over the month and by 12.3% over the past 12 months.

ANZ senior economist Daniel Gradwell said, “Housing finance fell in line with expectations in September, with declines across all segments. The recent fall in owner-occupier finance suggests that weaker sentiment is now also having an impact on the broader market. Importantly, the average loan size has started to pull back. This means that further weakness in house prices is likely, although smaller loans should be considered a positive development from a financial stability point of view.”

Financial markets were largely unresponsive to the figures and they had the RBA’s latest Statement on Monetary Policy to consider as well. By the end of the day, 3-year, 10-year and 20-year bond yields all finished unchanged at 2.19%, 2.77% and 3.11% respectively. However, the cash futures market must think the RBA will move more slowly as prices adjusted to imply a slightly lower probability of a rate rise in any given month from July 2019 to March 2020.

Financial markets were largely unresponsive to the figures and they had the RBA’s latest Statement on Monetary Policy to consider as well. By the end of the day, 3-year, 10-year and 20-year bond yields all finished unchanged at 2.19%, 2.77% and 3.11% respectively. However, the cash futures market must think the RBA will move more slowly as prices adjusted to imply a slightly lower probability of a rate rise in any given month from July 2019 to March 2020.