11 September 2018

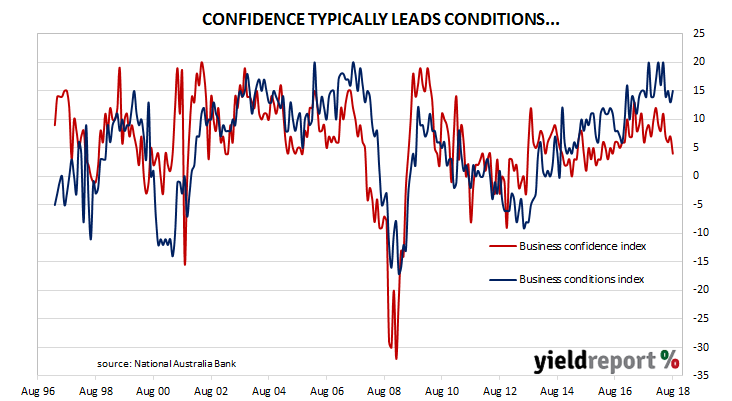

Australian business conditions were robust in the first half of 2018 and hit a record high in April. The latest readings may be lower than those in the first six months of 2018 but they still remain at historically elevated levels. According to some observers, the business conditions index is a good guide to GDP growth. Thus, the current spate of high readings bodes well for Australia’s GDP outlook.

According to NAB’s latest monthly business survey of 400 firms conducted in the last week of August, business conditions remained at a very healthy level. After revisions, the index inched up from 13 at the end of July to 15 in August. NAB chief economist Alan Oster said, “This is a welcome sign of a stabilisation in business conditions”.

Typically, NAB’s confidence index leads the conditions index by approximately one month, although in recent months the two surveys have diverged and the condition index has led the confidence index higher in trend terms since late 2014. The confidence index lost 3 points to register 4 on the index in August, which is below the long-term average reading of 6 and back to levels last seen in July 2016. Westpac senior economist Andrew Hanlon referred to the change of prime minister as a source of uncertainty for the business sector. “The change of prime minister on August 24 and the associated uncertainty around public policy, likely dented business sentiment. This is something to watch; will sentiment snap back in September or will uncertainty around policy remain a concern?”

Westpac senior economist Andrew Hanlon referred to the change of prime minister as a source of uncertainty for the business sector. “The change of prime minister on August 24 and the associated uncertainty around public policy, likely dented business sentiment. This is something to watch; will sentiment snap back in September or will uncertainty around policy remain a concern?”

07 September 2018

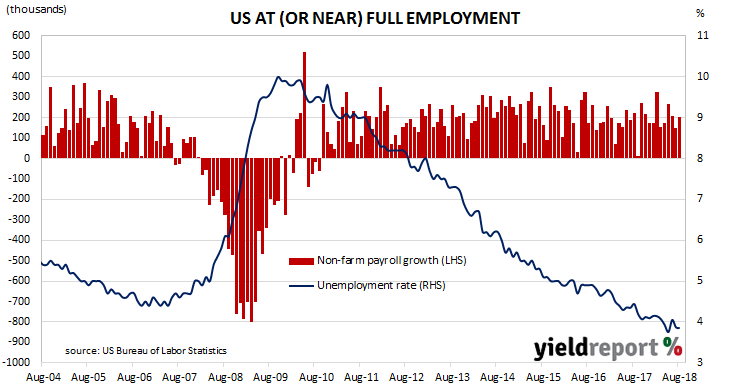

Amongst all the concern regarding potential damage to global trade from the imposition of additional tariffs by the US, China and the EU, the US economy has continued to produce jobs at a robust pace, reducing the number of Americans who wish to work more hours than they do at the moment and adding to the pressure for pay increases.

According to the US Bureau of Labor Statistics, the US economy created 201,000 jobs in the non-farm sector in August. However, the latest figures also include downward revisions to previous employment numbers and figures for June and July were revised down by a total of 50,000.

ANZ senior economist Cherelle Murphy said the figures, particularly the hourly pay numbers, added pressure for the US Fed to keep raising its federal funds rate. “The US labour market report came in better than expected with average hourly earnings growing at 2.9%, the quickest pace since May 2009. Headline non-farm payrolls rose 201,000 and the unemployment rate was steady at 3.9% with under-employment at 7.4%. All of this is consistent with the Fed tightening rates further, with the next hike expected in September.”

Economists were expecting around 191,000 additional positions and US bond markets reacted in a curious fashion. At the close of business, US 2-year bond yields were 3bps lower at 2.66% but 10-year yields had increased by 6bps to 2.94% and the yield on 30-year Treasury bonds had gained 5bps to 3.10%. The US currency was a little stronger against the euro and yen but steady against sterling. According to cash futures prices, the implied probability of a rate rise by the US FOMC at its September meeting remained just short of 100% while the probability of an additional rate rise in December jumped from a little under 70% to almost 80%.

07 September 2018

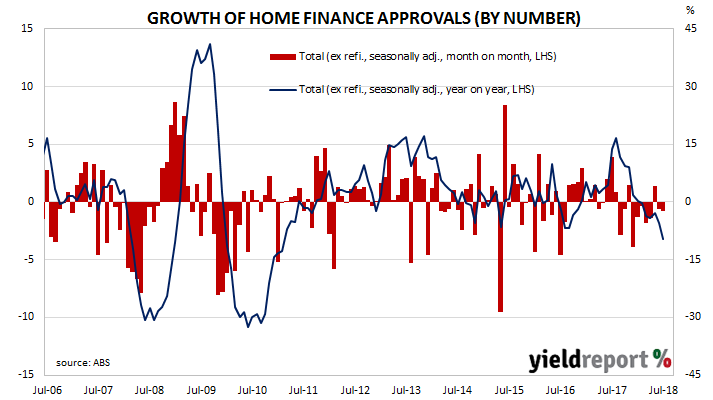

The Australian Bureau of Statistics (ABS) collects data on housing finance commitments made by significant lenders and their figures include secured (mortgage) finance commitments for the construction or purchase of owner-occupied dwellings and investment properties. It has some overlap with the RBA’s monthly private sector credit statistics which also includes investor lending and owner-occupier lending.

The ABS has released housing finance figures for July and they were higher than the consensus expectation. Total approvals in July increased by 0.4%, which is more than the expected -0.1% figure and up from June’s revised figure of -0.8%. However, on an annual basis, the growth rate slowed even further, from a revised figure of -4.5% in June to -6.2% in July. When refinancing approvals are removed, approvals fell by 0.8% over the month and by 9.6% over the year.

In dollar terms, total loan approvals excluding refinancing fell by 1.3% for the month, a slightly greater fall than in June when approvals fell by 1.1% after revisions. On a year-on-year basis, total approvals excluding refinancing fell by 9.0%.

In dollar terms, total loan approvals excluding refinancing fell by 1.3% for the month, a slightly greater fall than in June when approvals fell by 1.1% after revisions. On a year-on-year basis, total approvals excluding refinancing fell by 9.0%.

Westpac senior economist Matt Hassan said, “Overall, the finance data is consistent with the continued slowing in market conditions evident in auction markets and prices.”

04 September 2018

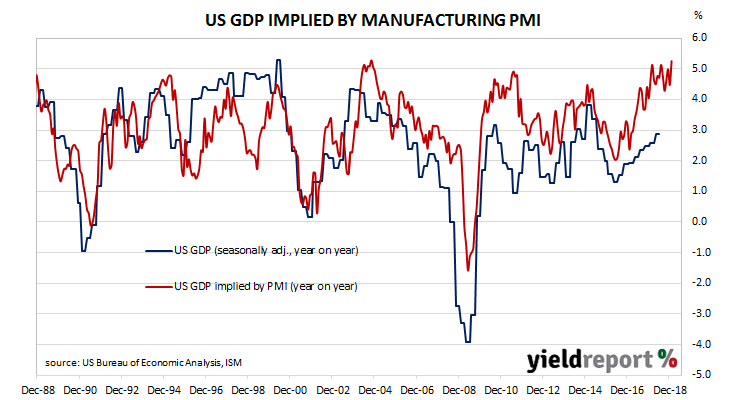

Purchasing Managers’ Indices (PMIs) are economic indicators derived from monthly surveys of purchasing and supply executives in private sector companies. They are diffusion indices, which means a reading of 50% represents no change from the previous period, while a reading under 50% implies respondents on average reported a deterioration. Their usefulness lay in being a leading indicator of GDP.

US manufacturing activity rebounded more than expected in August and the latest figure is very much at elevated levels. According to the Institute of Supply Management (ISM) August survey, its Purchasing Managers Index recorded a reading of 61.3, up from July’s reading of 58.1 and more than the expected figure of 59.2.

August’s figure is the highest in this cycle so far after readings of 60.8 recorded in September 2017 and February 2018 were exceeded and US bond yields across the curve finished the day higher. 2 year yields increased by 2bps to 2.65% and 10 year yields increased by 4bps to 2.90%.

04 September 2018

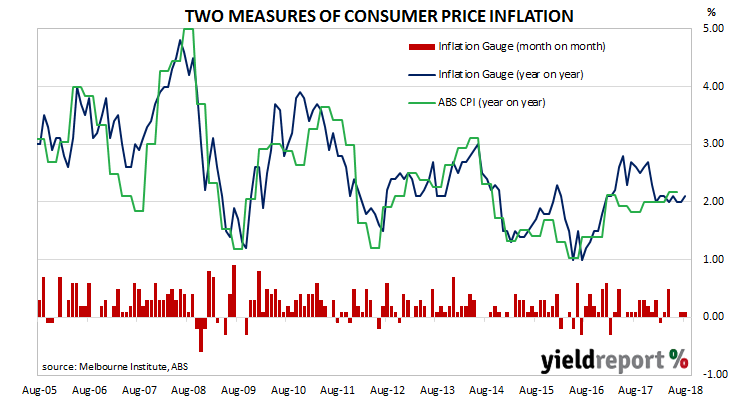

The Melbourne Institute’s Inflation Gauge is an attempt to replicate the ABS consumer price index (CPI) on a monthly basis instead of quarterly. It has turned out to be a reliable leading indicator of the CPI, although there are periods in which the Inflation Gauge and the CPI have diverged for periods of up to six-to-twelve months. On average, the Inflation Gauge’s annual rate tends to overestimate changes in the CPI inflation by an average of about 0.10% in any given quarter.

The Inflation Gauge increased by 0.1% during August after a similar increase in July and flat results in June and May. On an annual basis, the index increased by 2.1%, a rate which is higher than June and July’s 2.0% but the same as recorded in May.

Bond yields were largely unaffected while the local currency went a little higher. The yield on 3-year ACGBs slipped by 1bp to 1.99% while 10-year and 20-year ACGBs remained unchanged at 2.52% and 2.86% respectively. The Aussie dollar finished the day around 0.2 US cents higher at 72.10 US cents.

30 August 2018

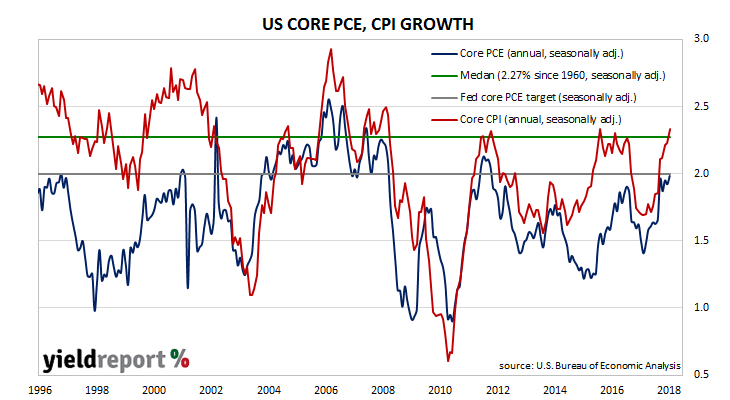

One of the US Fed’s favoured measures of inflation is the change in the core personal consumption expenditures (PCE) price index. The core version strips out energy and food components, which are volatile from month to month, in an attempt to identify the prevailing trend. It’s not the only measure of inflation used; the Fed also tracks the Consumer Price Index (CPI) and Producer Price Index (PPI) from the Department of Labor.

The latest figures have been published by the Bureau of Economic Analysis as part of the July personal income and expenditures report. At +0.2% for the month, core PCE inflation was up from June’s +0.1% and in line with expectations.

US financial markets were largely focussed on emerging market disarray and trade issues when the report was released and investors had already shifted to a “risk-off” setting. Bond yields finished the day a little lower while the US dollar was stronger against the euro but weaker against the yen and steady against sterling. 2-year, 10-year and 30-year yields each eased by 2bps to 2.65%, 2.86% and 3.00% respectively.

US financial markets were largely focussed on emerging market disarray and trade issues when the report was released and investors had already shifted to a “risk-off” setting. Bond yields finished the day a little lower while the US dollar was stronger against the euro but weaker against the yen and steady against sterling. 2-year, 10-year and 30-year yields each eased by 2bps to 2.65%, 2.86% and 3.00% respectively.

On an annual basis, the index grew by 2.0%, up from June’s 1.9% after revisions. Annual core PCE inflation has been moving higher since March after ranging between 1.3% and 1.6% for around a year. It is now at the Fed’s target.

30 August 2018

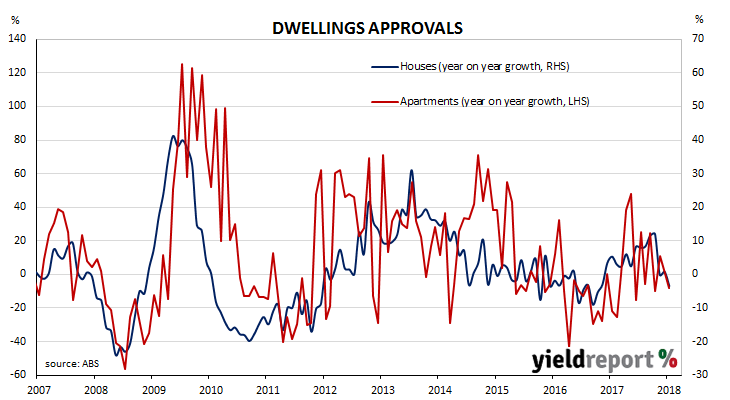

Aside from engineering and architectural design, one of the earliest requirements of a building project is to obtain approval from the relevant statutory body. As a result, building approvals data is a leading economic indicator of future construction. While not all projects which have been approved are completed, all completed projects have been granted approval. Approvals data thus provides a useful indicator of future construction.

The latest building approval figures have been released by the Australian Bureau of Statistics and figures for July reversed most of the gains from June. Seasonally-adjusted, total approvals fell by 5.2% in July, which is a larger fall than the expected 2.0% and a large drop from June’s revised growth rate of +6.8%. On an annual basis, total approvals fell by 5.6%, which is down from June’s comparable figure of 1.8% after revisions and less than the expected 2.5% contraction.

Westpac, senior economist Matthew Hassan said this latest report may be indicative of what is to come. “Overall…the July report is a weak one for a new building with the detail starting to move more in line with our expectation of a renewed decline in this segment.”

Westpac, senior economist Matthew Hassan said this latest report may be indicative of what is to come. “Overall…the July report is a weak one for a new building with the detail starting to move more in line with our expectation of a renewed decline in this segment.”

Reactions of local financial markets were mixed but as economists and commentators were more interested in the capex data released by the ABS at the same time, it is difficult to separate out the effect of one report as opposed to another. By the end of the Australian trading day, 3-year yields were 1bp higher at 2.03%, 10-year yields had increased by 2bps to 2.57% but the local currency was 0.25 US cents lower at 72.80 US cents.

30 August 2018

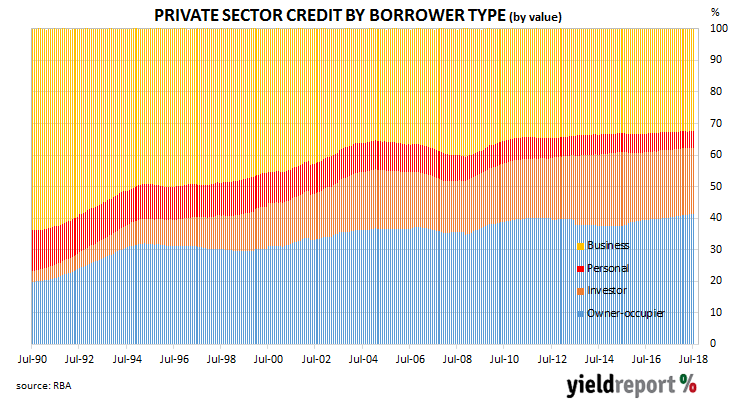

The pace of lending to the non-bank private sector by financial institutions in Australia stabilised in July. However, it may be just a pause in its descent of the past three-years after reaching a post-GFC peak in October 2015.

According to the latest RBA figures, private sector credit grew by 0.4% in July, up from the 0.3% growth rate in June and above the 0.3% consensus estimate. The year-to-July growth rate remained unchanged at 4.4% after revisions as personal loans and lending to investors stagnated.

Westpac senior economist Andrew Hanlon’s view was the month-on-month increase is likely to be short-lived. “This better outcome for total credit is likely to be a temporary respite from the current slowdown. Tighter lending conditions and rising funding costs will continue to weigh on the housing sector over coming months. House prices have turned, following a strong run, and dwelling approvals are down from the 2016 peak and are likely to move lower still after an extended upswing, to bring them more in line with underlying requirements.”

22 August 2018

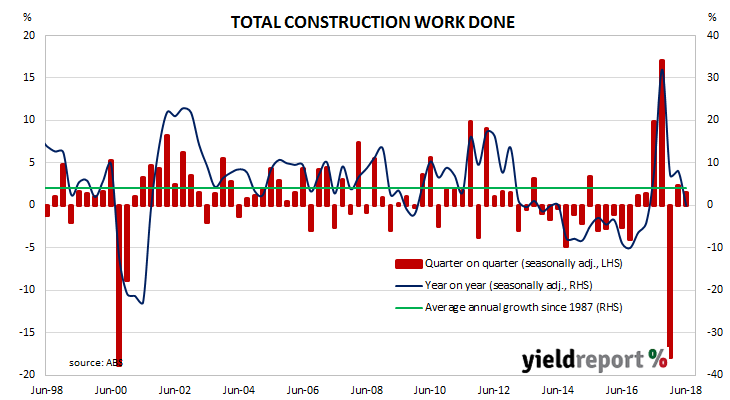

Quarterly construction data compiled and released by the ABS are not considered to be of a “primary” nature in the same way as unemployment (Labour Force) and inflation (CPI) figures. However, the figures are viewed by economists and analysts with interest as they directly feed into quarterly GDP figures.

According to the latest construction figures published by the ABS, the value of construction work increased by a very modest amount in the June quarter after a similar-sized increase in the previous period. Total construction in the June quarter increased by 1.6%, which is more than the 0.8% increase expected but less than the revised +2.4% increase in the March quarter. On an annual basis, the growth rate dropped back from March’s revised figure of +8.1% to -0.1% in the June quarter.

ANZ senior economist Daniel Gradwell viewed the figures with some enthusiasm. “Both the headline result and the details were strong for Q2 (June quarter) construction, while upward revisions to the Q1 (March quarter) result mean momentum has been better than previously thought. Work done in Q2 was up across both the public and private sectors and across most industries and [it] is expected to make a solid contribution to Q2 GDP growth.”

ANZ senior economist Daniel Gradwell viewed the figures with some enthusiasm. “Both the headline result and the details were strong for Q2 (June quarter) construction, while upward revisions to the Q1 (March quarter) result mean momentum has been better than previously thought. Work done in Q2 was up across both the public and private sectors and across most industries and [it] is expected to make a solid contribution to Q2 GDP growth.”

22 August 2018

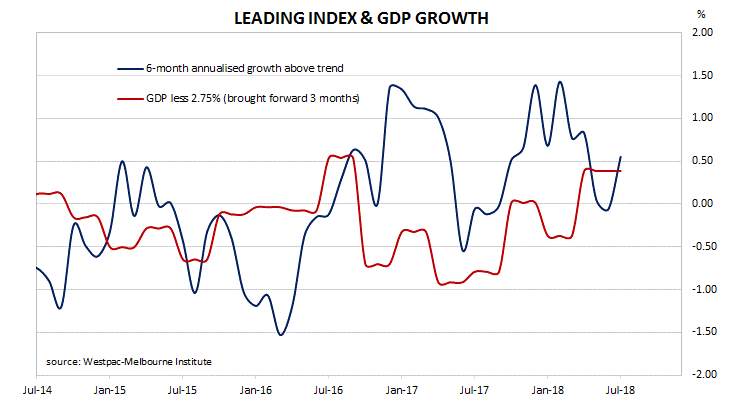

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of economic activity relative to trend in Australia. The index combines certain economic variables which are thought to lead changes in economic growth into a single variable. This variable is claimed to be a reliable cyclical indicator for the Australian economy and an indicator of swings in Australia’s overall economic activity.

The six-month annualised growth rate of the indicator increased from a revised -0.06% in June to +0.55% in July. These figures represent growth rates relative to trend-GDP growth, which is generally thought to be around 2.75% per annum for Australia. The Index is said to lead GDP by 3 months to 6 months, so theoretically the current reading represents an annualised GDP growth rate of around 3.25% in the September or December quarters.

According to Westpac chief economist Bill Evans, the largest negative influences over the previous six months included Australians higher expectations of becoming unemployed, lower commodity prices and a flatter yield curve. An increase in the total number of hours worked by Australians provided some offsetting effects.