21 August 2018

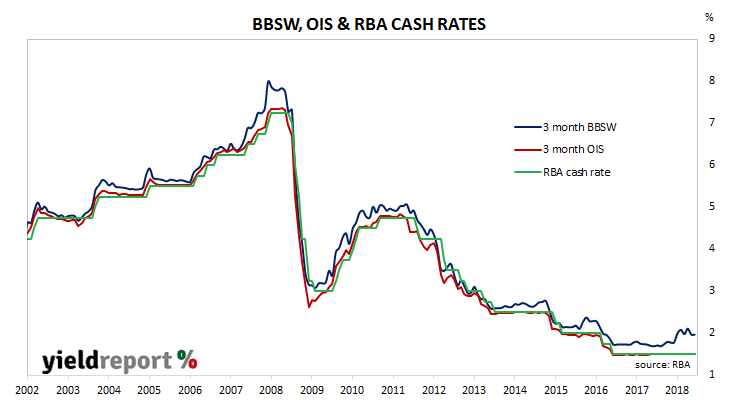

Economists employed by the major banks, along with economists in general, have been steadily pushing their cash rate change forecasts out. The cash rate, the rate at which banks can borrow from and lend to each other in the overnight market, has not been raised since November 2010. It was reduced twelve times since then, beginning in October 2011 and as recently as August 2016.

A year ago, many were of the view the RBA would begin the rate increase as part of the cycle in 2018. As time passed and economic data failed to be of a type which would encourage official rate increases, dates began to be pushed back, initially in late 2018 and then into 2019.

NAB was the last of the major banks to materially change its cash rate forecasts. In May, NAB joined the other majors when it pushed back its timing for a 25bps rate rise from “late 2018” to 2019. After NAB made its change, none of the major banks forecasts a rate rise in 2018.

Westpac and its chief economist Bill Evans have been among the least “hawkish” of economists in the last year or two. For some time, he had expressed the view the data the RBA has seen would not give it the confidence needed to raise the cash rate. He acknowledged at some time those figures would come, but so far they had not and until they had, the RBA was likely to do little.

17 August 2018

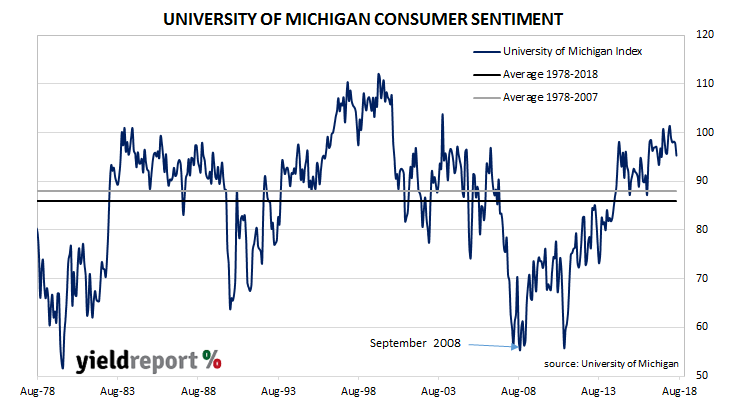

The University of Michigan’s Index of Consumer Sentiment is one of two monthly US consumer sentiment indices, the other being the Conference Board’s Consumer Confidence Survey. It covers personal finances, business conditions and buying conditions. As private consumption accounts for a majority of GDP growth in advanced economies, consumer sentiment surveys present a picture of the economy well in advance of official reports. However, as leading indicators, they are only as useful as other widely available data.

The latest survey conducted by the university indicates US consumers, especially those with incomes in the lowest segment, have become more sensitive to price rises of consumer goods. The economist in charge of the survey, Richard Curtin, described recent changes in consumers’ views as “extraordinary shifts in price perceptions” which indicated little tolerance for price rises above a fairly low rate.

The result was a fall in the index from July’s revised reading of 97.9 to 95.3 in August, which is about the same reading as at the start of 2018. This reading is still in the range which could be considered as elevated and it is considerably more optimistic than the long-term average (see chart above).

15 August 2018

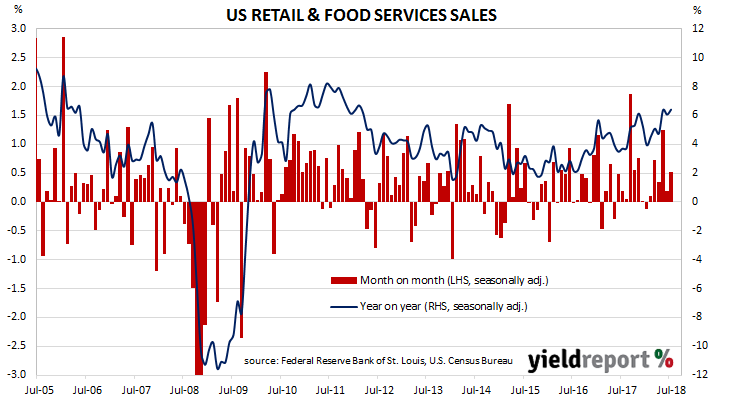

Retail sales account for a large part of consumer spending, which itself is typically the largest segment of GDP in an advanced economy. Changes in retail sales have a large effect on GDP growth rates and thus they are of great interest to economists, policy makers and financial markets.

Apart from a weak January, US retail sales have been robust from September 2017 onwards when annual growth rates started exceeding 5%. Since March, growth rates have picked up even further and the latest July figures suggest recent strength in consumer spending has continued into the September quarter.

According to the latest “advance” sales numbers released by the US Census Bureau, retail sales grew by 0.5% over the month and by 6.4% when compared with the same period last year. The increase was considerably higher than the 0.1% increase expected and up from June’s revised figure of +0.2%.

The increase was primarily driven by restaurants, bars and take-away sales, as well as online (“non-store”) retailing.

15 August 2018

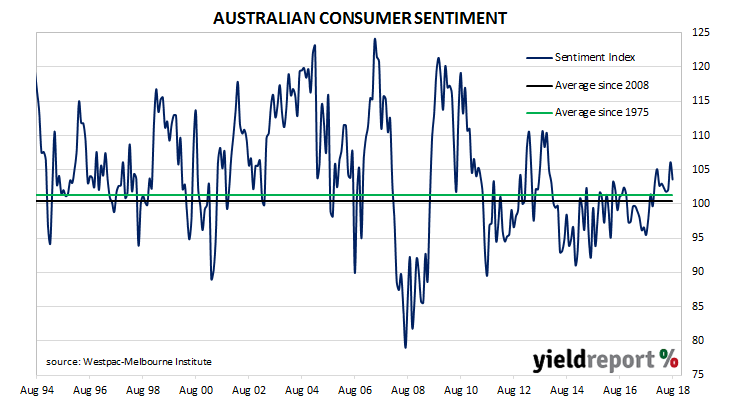

During most of the period between 2014 and 2018 there has been a divergence between consumer sentiment and business confidence in Australia. The latest consumer survey may mark the beginning of a convergence of the two sectors. Although one month’s reading is hardly enough to rely on, perhaps Westpac chief economist Bill Evans knew something when he referred to “a clear improvement” in consumer sentiment after last month’s report.

According to the latest Westpac-Melbourne Institute survey conducted early in August, households’ levels of optimism slipped as the Consumer Sentiment Index fell back from July’s reading of 106.1 to 103.6. Any reading above 100 indicates the number of consumers who are optimistic is greater than the number of consumers who are pessimistic. The long-term average reading is just over 101.

14 August 2018

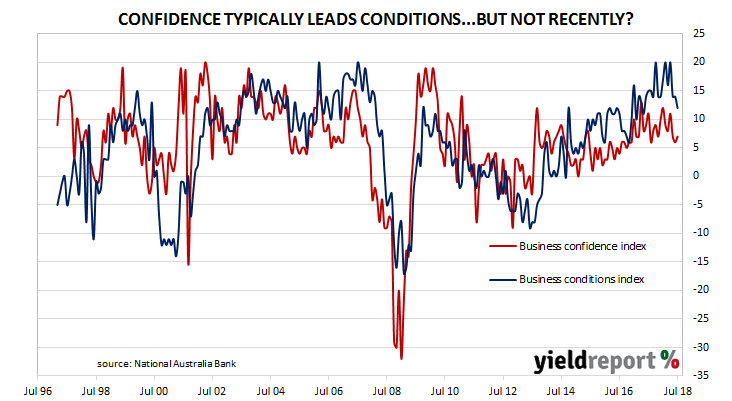

Australian business conditions have been more than just solid in the first half of 2018, having hit a record high in April. The latest readings may be lower than those in the first six months of 2018 but they still remain at historically elevated levels. The conditions index is of a certain importance. According to Westpac currency strategists Imre Speizer and Sean Callow, it “is usually the best guide to GDP growth…”

According to NAB’s latest monthly business survey of 400 firms conducted in the last week of July, business conditions deteriorated, albeit from an extremely-healthy level. After revisions, the index slipped from 14 at the end of June to 12 in July. NAB chief economist Alan Oster said, “While forward orders remain around average, which still implies growth in the sector, the declines over recent months suggest that there is some risk of a pull-back in business activity that warrants close watching over coming months.”

Westpac senior economist Andrew Hanlon had an interesting explanation for the softer business conditions which may suggest it is temporary. “Recall that in July, billions of people around the globe were transfixed by the greatest show on earth, the World Cup. No great surprise that the consumer sectors had a soft month…”

Typically, NAB’s confidence index leads the conditions index by approximately one month, although in recent months the two surveys have diverged and the condition index has led the confidence index higher in trend terms since late 2014. The confidence index regained the 1 point it lost in June’s survey to record 7 in July, which is just above the long-term average reading.

10 August 2018

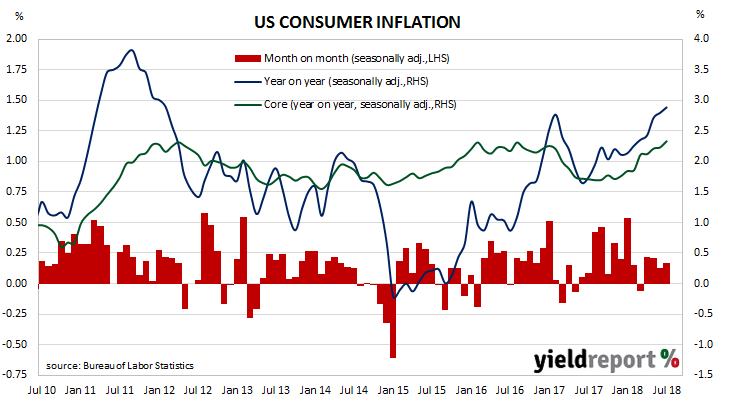

The annual rate of US consumer inflation has increased for the seventh consecutive month in July, again driven by higher oil and fuel prices and shelter costs. Consumer price index (CPI) figures released by the Bureau of Labor Statistics indicated seasonally-adjusted consumer prices increased by +0.2%, in line with economists’ expectations and the same as June’s +0.2%. However, on a 12-month basis, the consumer inflation rate increased from June’s 2.8% to 2.9%.

“Core” inflation, a measure of inflation which strips out the volatile food and energy components of the index, increased on a seasonally-adjusted basis by +0.2% for the month, while the annual rate increased from 2.2% to 2.3%. This is the highest annual rate of underlying consumer inflation since September 2008.

The reaction to the inflation figures was mixed up with concern arising from gyrations in the Turkish currency and a preference by global investors for low-risk assets such as bonds in “safe-haven” countries. 2 year and 10 year bond yields both decreased by 5bps to 2.60% and 2.87% respectively while 30 year yields fell by 4bps to 3.03%. The USD was stronger against the euro and pound but weaker against the yen.

09 August 2018

The producer price index (PPI) is a measure of prices charged by producers for domestically produced goods, services, and construction. In the US it is constructed by the Bureau of Labor Statistics in a fashion similar to the consumer price index (CPI) except it measures prices received from the producer’s perspective. It is another one of the various measures of inflation tracked by the US Fed, along with the CPI and core personal consumption expenditure (PCE).

The latest figures for July have been published by the Bureau and they indicate producer prices were unchanged across the month. The result was less than the expected +0.2% and lower than May’s +0.3%. On a 12-month basis, the rate of producer price inflation dropped back to 3.2% after recording 3.3% in June and 3.1% in May.

ANZ senior economist Joanne Masters said the report suggests “inflation is not getting away from the Fed any time soon.” However, Westpac’s Finance AM team warned against complacency. “Notwithstanding the weaker than expected outcome, upstream input cost pressures are building thanks to the robust US economy, higher energy prices and import tariffs.”

08 August 2018

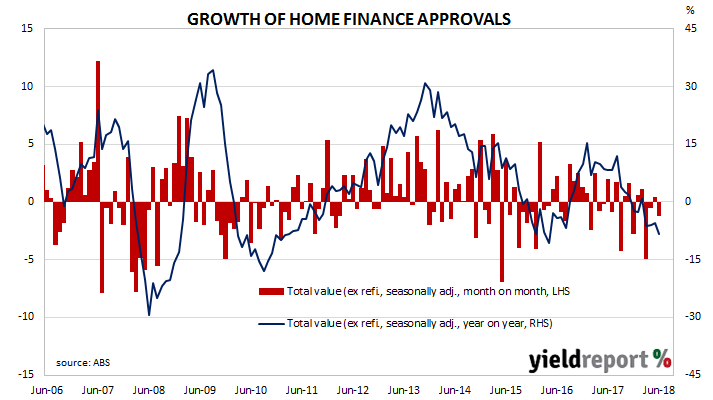

The Australian Bureau of Statistics (ABS) collects data on housing finance commitments made by significant lenders and their figures include secured (mortgage) finance commitments for the construction or purchase of owner-occupied dwellings and investment properties. It has some overlap with the RBA’s monthly private sector credit statistics which also includes investor lending and owner-occupier lending.

The ABS has released housing finance figures for June and they were lower than market expectations. Longer term bond yields finished the day higher despite slightly lower US yields in overnight markets; 3-year bond yields remained unchanged at 2.11% and 10 year yields added 2bps to 2.68%.

The number of approvals fell by 1.1% over June and by 5.0% on an annual basis. When approvals for refinancing is removed, the number of approvals fell by 0.5% over the month and by 5.6% over the year. In dollar terms, total loan approvals excluding refinancing fell by 1.2% for the month. On a year-on-year basis, the total value fell by 8.4%.

The number of approvals fell by 1.1% over June and by 5.0% on an annual basis. When approvals for refinancing is removed, the number of approvals fell by 0.5% over the month and by 5.6% over the year. In dollar terms, total loan approvals excluding refinancing fell by 1.2% for the month. On a year-on-year basis, the total value fell by 8.4%.

07 August 2018

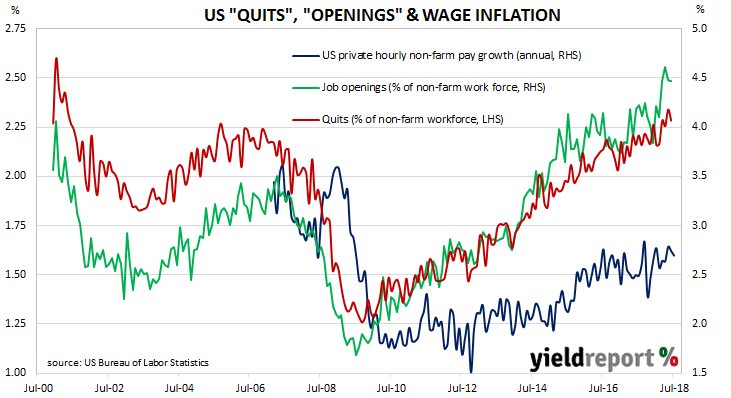

The “quits” rate time series produced by the Job Openings and Labor Turnover Survey (JOLTS) is a leading indicator of US hourly pay. As wages account for around 55% of a product’s or service’s price*, wage inflation and overall inflation rates tend to be closely related. Former Federal Reserve chief Janet Yellen was known to pay close attention to the quit rate but whether new Fed chief Jerome Powell regards the indicator with as much interest is as yet unknown.

Figures released as part of the most recent JOLTS report show the quit rate remained unchanged after revisions at 2.3% of the non-farm workforce at the end of June. Quit rates were highest in the “Real estate, rental and leasing” and “Professional and business services” sectors while the “Other services”, “Education and health services” and “Leisure and hospitality” sectors each recorded noticeable falls. ANZ economist Giulia Specchia described the figures as pointing “to ongoing tightness in the labour market and modest upward wage pressures.”

Reactions by financial markets were subdued. The yield on US 2 year Treasury bonds edged up 1bp to 2.66% while 10 year yields moved up 3bps to 2.97%. According to cash futures prices, the probability of a rate rise at the September FOMC meeting is close to a certainty at 96% while the likelihood of another increase in December moved from 65.8% to 68.4%. The US dollar was essentially unchanged against other major currencies.

07 August 2018

The August board meeting of the RBA is historically one of the four months of the year in which the likelihood of a rate change is highest. February, May, August and November happen to be the four months of the year in which previous rate changes have typically occurred.

As expected, the RBA announced Australia’s overnight cash rate would remain at 1.50%. ANZ senior economist Felicity Emmett said, “The tone of the statement remains broadly positive, with the Bank suggesting no material changes to its forecasts in the upcoming Statement on Monetary Policy due on Friday.”

Market reaction was limited on the day. Cash futures markets were less convinced of the likelihood of an upcoming rate rise and closing prices implied only a 20% chance of a rate rise within the next 12 months. In the bond market, Commonwealth Government yields slipped a couple of basis points across the curve. Yields on 3 year, 10 year and 20 year bonds all ended the day 2bps lower at 2.11%, 2.66% and 2.98% respectively. The local currency fluctuated around 73.95 US cents immediately after the decision but it did not really change until late in the afternoon when it moved up to 74.25 US cents.

Westpac chief economist Bill Evans has been critical of some parts of the RBA’s logic in recent months. After this latest policy meeting, he disagreed with the RBA’s forecast of “some lift in wages growth over time” given the RBA’s forecasts of the unemployment rate. He said the RBA’s expectations was inconsistent with the level of the unemployment rate required to produce wage pressures, which he estimates to be around 5%. “Our view, based on offshore evidence, is that the NAIRU in this cycle is likely to be below 5%, so even with this new lower unemployment forecast, it still seems a big call to expect sustained upward pressures on wages growth.”