16 July 2018

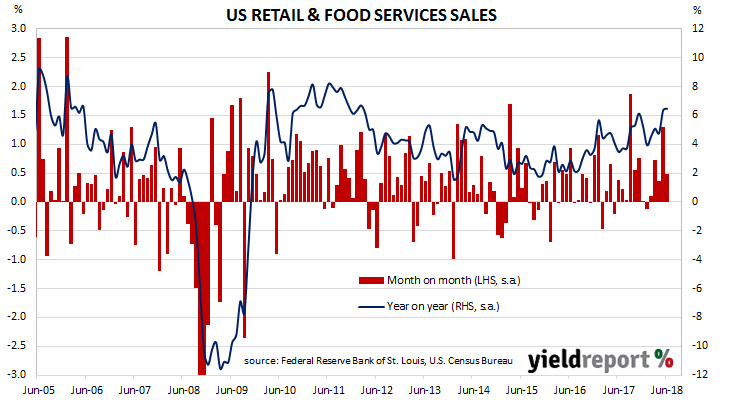

Retail sales account for a large part of consumer spending, which itself is typically the largest segment of GDP in an advanced economy. Changes in retail sales have a large effect on GDP growth rates and thus they are of great interest to economists, policy makers and financial markets.

US retail sales had been weak through the Christmas period and into the first couple of months in 2018 but then figures from March onwards marked a divergence from this trend. The last four months, including the latest June figures, paint a picture of a robust consumer sector.

According to the latest “advance” sales numbers released by the US Census Bureau, retail sales grew by 0.5% over the month and by 6.5% when compared with the same period last year. The figures were less than the 0.6% increase expected and down from May’s comparable figure after it had been revised up from +0.8% to +1.3%.

13 July 2018

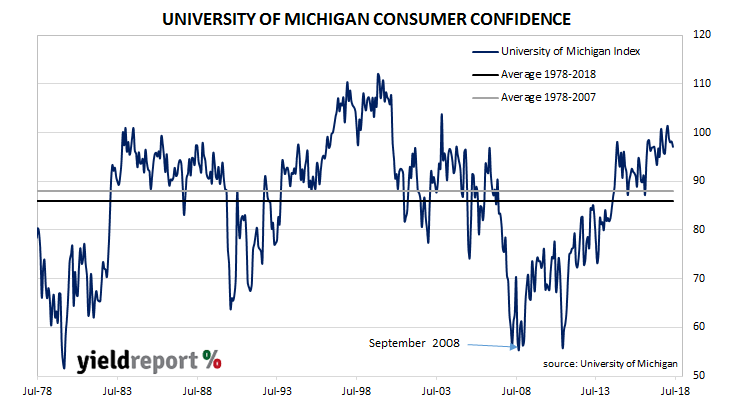

The University of Michigan’s Index of Consumer Sentiment is one of two monthly US consumer sentiment indices, the other being the Conference Board’s Consumer Confidence Survey. It covers personal finances, business conditions and buying conditions. As private consumption accounts for a majority of GDP growth in advanced economies, consumer sentiment surveys present a picture of the economy well in advance of official reports.

However, as leading indicators, they are only as useful as other widely available data.

The latest survey conducted by the university indicates US consumers think employment and pay prospects look favourable but, at the same time, various trade disputes present a potential drag on the US economy and the possibility of higher inflation. The net result was a fall in the index from 98.2 in June to 97.1 in July, which is about the same as the average of the previous twelve months and considerably more optimistic than the long-term average (see chart below).

12 July 2018

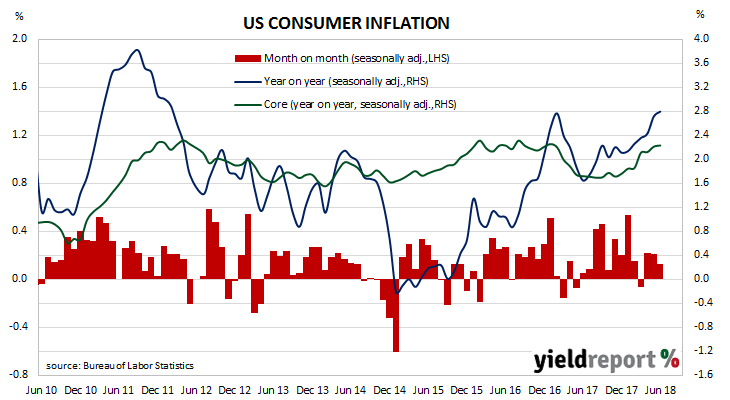

The annual rate of US consumer inflation has increased for the sixth consecutive month in June, driven by higher oil and fuel prices and shelter costs. Consumer price index (CPI) figures released by the Bureau of Labor Statistics indicated seasonally-adjusted consumer prices increased by +0.1%, which was under economists’ expectations and lower than May’s +0.2%. However, on a 12-month basis, the consumer inflation rate increased from May’s 2.7% to 2.8%.

11 July 2018

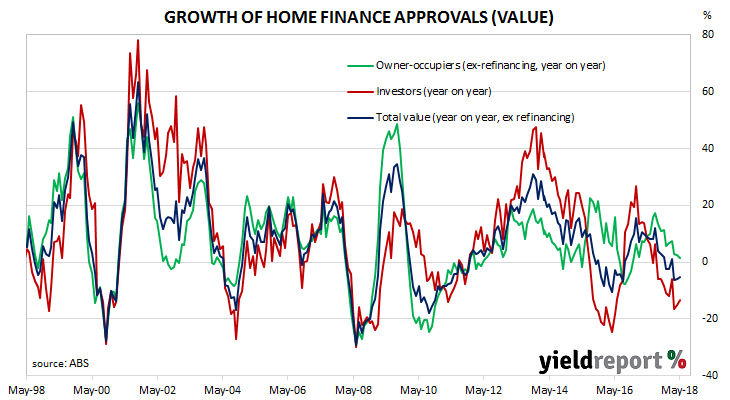

The Australian Bureau of Statistics (ABS) collects data on housing finance commitments made by significant lenders and their figures include secured (mortgage) finance commitments for the construction or purchase of owner-occupied dwellings and investment properties. It has some overlap with the RBA’s monthly private sector credit statistics which also includes investor lending and owner-occupier lending.

The ABS has released housing finance figures for May and they were higher than market expectations. However, bond yields finished the day lower despite higher US yields in overnight markets. 3 year bond yields fell by 4bps to 2.06% and 10 year yields lost 3bps to 2.61%.

The number of owner-occupier approvals increased by 1.1% compared to April, which was higher than the 2% fall expected. Excluding refinancing, the number of approvals increased by 1.8%. On a year-on-year basis, owner-occupier approvals fell by 2.5% and after excluding refinancing, the value of approvals fell by 2.8%.

In dollar terms, the total value of loan approvals, excluding refinancing, increased by 0.4% for the month. On a year-on-year basis, the total value fell by 5.3%.

Finance approvals for owner-occupiers have slowed but by nearly as much as the investor segment. The total value of owner-occupier loan approvals, excluding refinancing, increased by 0.8% in May, following a revised 0.3% increase in April. On an annual basis, May owner-occupier loan approvals increased by 1.6%, down from April’s comparable figure of 2.4%.

11 July 2018

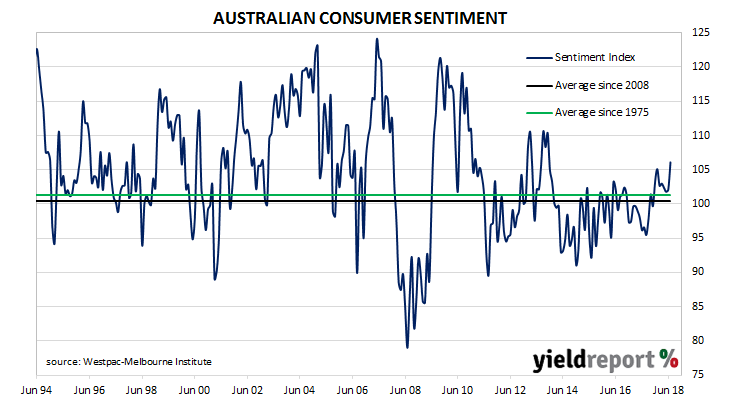

During most of the period between 2014 and 2018 there has been a divergence between consumer sentiment and business confidence in Australia. The latest consumer survey may mark the beginning of a convergence of the two sectors. Although one month’s reading is hardly enough to rely on, perhaps Westpac chief economist Bill Evans knew something when he referred to “a clear improvement” in consumer sentiment after last month’s report.

According to the latest Westpac-Melbourne Institute survey conducted in the first week of July, households’ levels of optimism improved markedly as the Consumer Sentiment Index inched up from June’s reading of 102.1 to 106.1. Any reading above 100 indicates the number of consumers who are optimistic is greater than the number of consumers who are pessimistic. The long-term average reading is just over 101.

While significantly higher than readings over the last five years or so, Westpac senior economist Matthew Hassan was quick to point out it was “not that strong” and still below the average of readings in the ten years prior to the GFC. On the plus side, he noted “a more balanced growth profile across states” along with a mining-led recovery in Queensland and Western Australia. All the same, “a lift in consumer demand still looks unlikely near term.”

11 July 2018

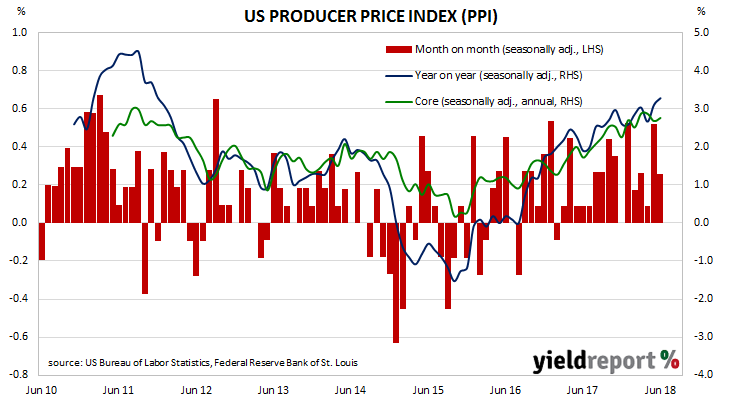

The producer price index (PPI) is a measure of prices charged by producers for domestically produced goods, services, and construction. It is constructed by the US Bureau of Labor Statistics in a fashion similar to the consumer price index (CPI) except it measures prices received from the producer’s perspective. It is another one of the various measures of inflation tracked by the US Fed, along with the CPI and core personal consumption expenditure (PCE).

The latest figures for June have been published by the Bureau and they indicate producer prices increased by +0.3% across the month. The increase was more than the +0.2% expected but lower than May’s +0.5%. On a 12-month basis, the rate of producer price inflation increased to 3.3% after recording 3.1% in May and 2.7% in April.

10 July 2018

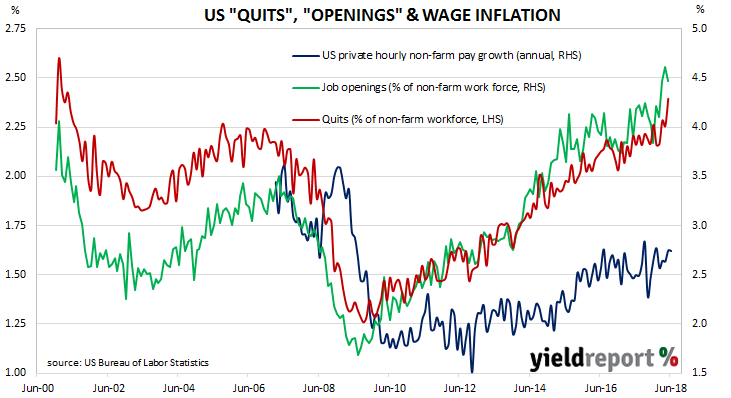

The “quits” rate time series produced by the Job Openings and Labor Turnover Survey (JOLTS) is a leading indicator of US hourly pay. As wages account for around 55% of a product’s or service’s price*, wage inflation and overall inflation rates tend to be closely related. Former Federal Reserve chief Janet Yellen was known to pay close attention to the quit rate but whether new Fed chief Jerome Powell regards the indicator with as much interest is as yet unknown.

Figures released as part of the most recent JOLTS report show the quit rate moved up from 2.3% to 2.4% of the non-farm workforce at the end of May. Quit rates were highest in the “Trade, transportation and utilities” and “Health care and social assistance” sectors while the only sector to record a fall was the “Manufacturing” sector.

Reactions by financial markets were muted. The yield on US 2 year Treasury bonds edged up 1bp to 2.57% while 10 year yields remained unchanged at 2.86%. According to cash futures prices, the probability of a rate rise at the September FOMC meeting moved a little higher to 85.4%. The US dollar was up marginally against the yen, down a little against sterling and roughly unchanged against the euro.

10 July 2018

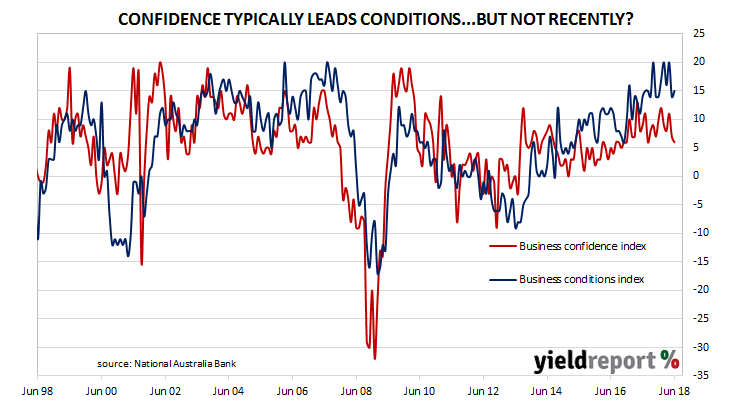

Australian business conditions have been more than just solid in the first half of 2018, having hit a record high in April. The latest readings have done nothing to alter this picture.

According to NAB’s latest monthly business survey of 400 firms conducted in the last week of June, its Business Conditions Index steadied after a large fall in May. After revisions, the index crept up from 14 at the end of May to 15 in June. NAB chief economist Alan Oster said, “While forward looking indicators have weakened a little, they still point to favourable business conditions for the rest of 2018.”

Typically, NAB’s confidence index leads the conditions index by approximately one month, although in recent months the two surveys have diverged and the condition index has led the confidence index higher in trend terms since late 2014. The confidence index slipped from a revised reading of 7 in May to 6 in June, which is roughly the same as the long term average reading.

09 July 2018

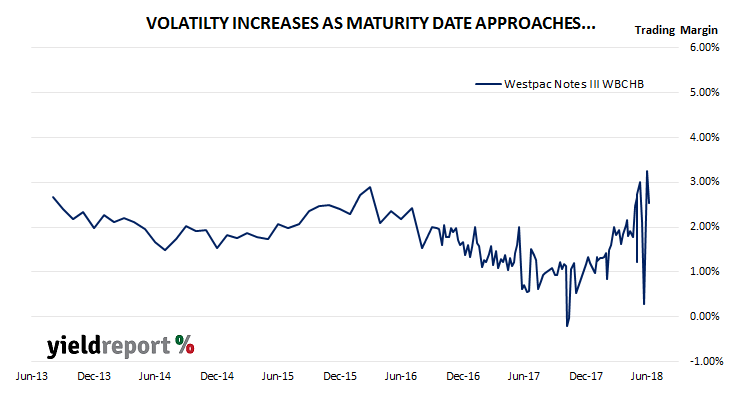

Westpac Subordinated Notes II (ASX code: WBCHB) were issued in August 2013. They pay a floating rate of interest equivalent to 3 month BBSW + 230bps, have a first call date of 22 August 2018 and their final maturity date is on 22 August 2023.

Westpac has recently announced it will redeem all of these notes on the first (call) optional redemption date of 22 August 2018. Holders will receive the final interest payment of $1.07002 in addition to the $100.00 face value.

By the start of 2019, there will be less than ten ASX-listed notes and bonds remaining which have been issued by investment-grade companies. The redemption of Westpac’s notes will be the first of several during the latter part of 2018. Crown Notes (ASX code: CWNHA) are callable in September, Suncorp Notes (ASX code: SUNPD) are callable in November and AMP Notes (ASX code: AMPHA) will mature in December.

04 July 2018

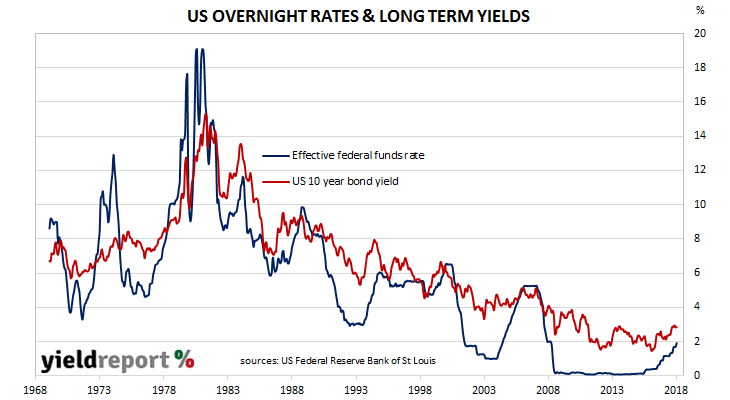

The Federal Open Markets Committee (FOMC) of the US Fed raised the federal funds rate range to 1.75%-2.00% at its last meeting in mid-June. The move was widely expected and another one, possibly two rate increases are expected before the end of 2018.

The minutes of the meeting have now been released and there appears to be no change in the FOMC’s general attitude. The threat of a US-Chinese trade war is noted as a cause for concern but it appears as if members of the FOMC have not given these concerns anywhere near as much weight as they have to the strength of the US economy. The FOMC also noted the current “stance of monetary policy would remain accommodative stance” after the rate increase “supporting strong labor (sic) market conditions and a sustained return to 2% inflation.”

Westpac senior economist Elliot Clarke said the US Fed is likely to maintain its current course of raising rates despite recent uncertainties. “Overall, the FOMC is intent on continuing with its gradual normalisation of policy, believing that the underlying strength of the US economy will win out over global uncertainties, a large portion of which is the result of President Trump’s political agenda.” However, he did remind us a continuation of the normalisation policy would always be “data dependent”.