25 June 2018

National Australia Bank’s income securities were among the first of the floating rate hybrids to be issued in the late 1990s. Adelaide Bank, Macquarie Bank and a few others, including NAB, issued securities with $100 face values and floating-rate coupons. Prior to the issue of these securities which became known as income securities, hybrids in the 1990s had been issued as fixed-rate converting preference shares. Before converting preference shares, hybrids had been mostly, if not entirely, limited to convertible bonds which have existed since the 18th century.

Over the years, some investors have been buying NAB’s income securities on the premise they would be redeemed at $100 “soon”. The problem with this idea was the NAB securities traded at a large discount to face value and they had done so for the last decade. Why would NAB redeem them at $100 when they could do what Bendigo Bank did with its income securities? That is, announce an offer to buy them back at a premium to the market value but at a (sizable) discount to face value.

In December 2010, Bendigo Bank made an offer to repurchase its floating rate subordinated notes (ASX code: BENHB, issued by Adelaide Bank in 1998) at $80 or a 13% premium to the price when the offer was made in November 2010. In that offer, 54% of the outstanding notes were repurchased, leaving around 400,000 notes listed. Six months later, another offer was made at $80 or at an 18% premium to the price. This second offer left just over 210,000 notes on issue and they are still listed on the ASX, currently trading at around $76.50.

Bendigo Bank gave no hint of its buy-back plans, so it would be foolish to think NAB would flag such a plan, either. However, there may be a reason to think a buy-back may be forthcoming.

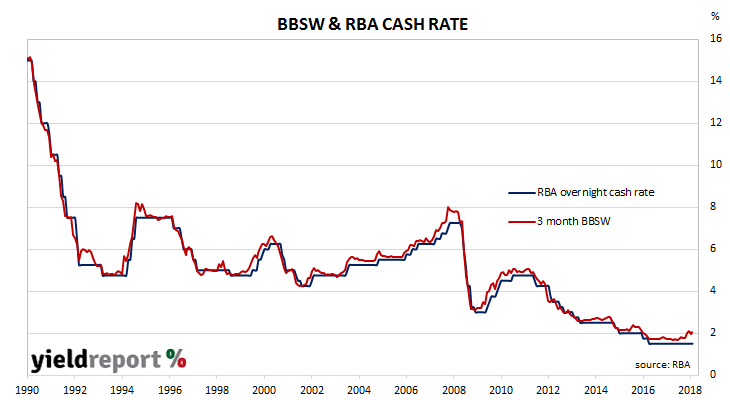

Christopher Joye, economist, fund manager and ex-RBA board member recently wrote how he thinks some interesting times are coming for NAB’s Income Securities (ASX code: NABHA). His team calculated the appropriate trading margin above BBSW for the NAB securities is currently around 360bps. However, as they lose progressively their status as Additional Tier 1 (AT1) securities and become more and more like debt securities, he thinks the appropriate trading margin should drop, and by 2022 the appropriate margin should be around 180bps.

21 June 2018

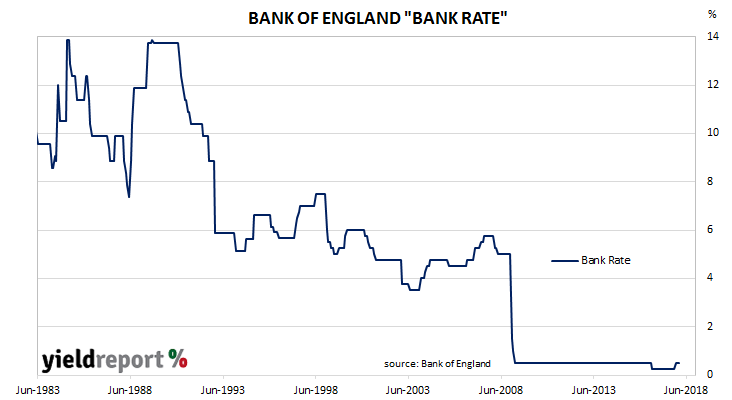

At its June meeting held on Thursday, the Bank of England’s Monetary Policy Committee (MPC) held its official rate, known as Bank Rate, steady at 0.50%. Normally, a decision to do nothing would pass without much comment but, in this case, a couple of interesting developments have taken place

Firstly, the number of members who voted in favour of a rate rise changed from two to three as the BoE’s chief economist moved to increase. Andrew Haldane joined the MPC in 2014 and he has voted in line with the majority view each time until now. He joins known monetary policy “hawks”, Ian McCafferty and Michael Saunders, as dissenters to the decision to hold Bank Rate steady.

20 June 2018

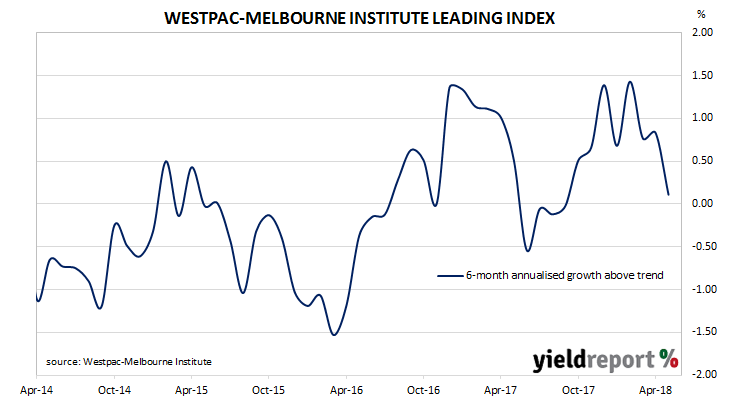

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of economic activity relative to trend in Australia. The index combines certain economic variables which are thought to lead changes in economic growth into a single variable. This variable is claimed to be a reliable cyclical indicator for the Australian economy and an indicator of swings in Australia’s overall economic activity.

The six month annualised growth rate of the indicator fell from a revised +0.83% in April to +0.11% in May. These figures represent growth rates relative to trend-GDP growth, which is generally thought to be around 2.75% per annum for Australia. The Index is said to lead GDP by 3 months to 6 months, so theoretically the current reading represents an annualised GDP growth rate of a little under 3% in the September or December quarters.

Since October, the Leading Index has returned values which implied above-trend growth in the near future. The series “yo-yoed” to some degree in the first quarter of 2018 but, since then, it has slid back to just above zero, the point which represents “at trend” growth.

20 June 2018

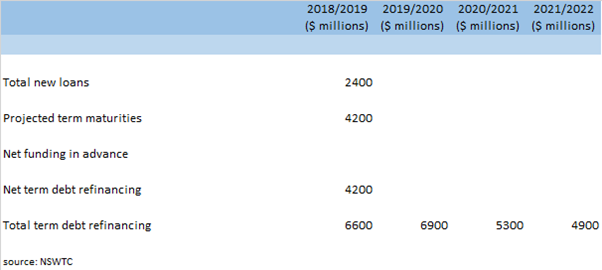

The New South Wales Government recently released its 2018/2019 budget and as a result, New South Wales Treasury Corporation (NSWTC) estimates it will borrow $6.6 billion in 2018/2019. This figure is about $3.5 billion less than forecast in NSWTC’s 2017/2018 funding requirement and it is the result of what NSWTC referred to as “surplus financial assets”.

Around two-thirds of NSWTC’s bond issues scheduled for the 2018/2019 year will be used to finance $4.2 billion of NSWTC bonds due to mature during the year. The balance of the $6.6 billion to be borrowed will be for new expenditures.

19 June 2018

The RBA held the official cash rate steady at its board meeting in June, as it had for every meeting since the cash rate was reduced in August 2016. The US Fed may be well into its rate rising cycle but so far the RBA has not shown any indication it is about to take the same path.

The minutes from the RBA’s latest meeting have now been released and analysts and economists did not find anything particularly controversial. As AMP Capital’s Shane Oliver put it, there were “no surprises”.

The RBA board covered the usual areas; global conditions, “had strengthened over the prior year”, local employment growth “had grown strongly” while inflation “remained low and was likely to remain so for some time.” The property market was less of a concern as APRA regulations, lower loan demand and tighter credit standards “had been helpful” in containing the build-up of household debt. Interest rates were “continuing to support the Australian economy.”

15 June 2018

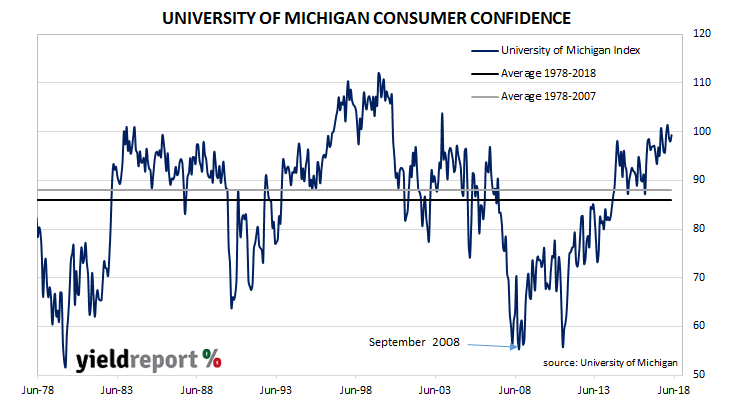

The University of Michigan’s Index of Consumer Sentiment is one of two monthly US consumer sentiment indices, the other being the Conference Board’s Consumer Confidence Survey. It covers personal finances, business conditions and buying conditions.

The latest survey conducted by the university indicates US consumers think current conditions are favourable but they are worried about the overall economy. The net result was an increase in the index from 98.0 in May to 99.3 in June. However, on the whole, survey respondents indicated they were still considerably more optimistic than the long-term average (see chart below).

14 June 2018

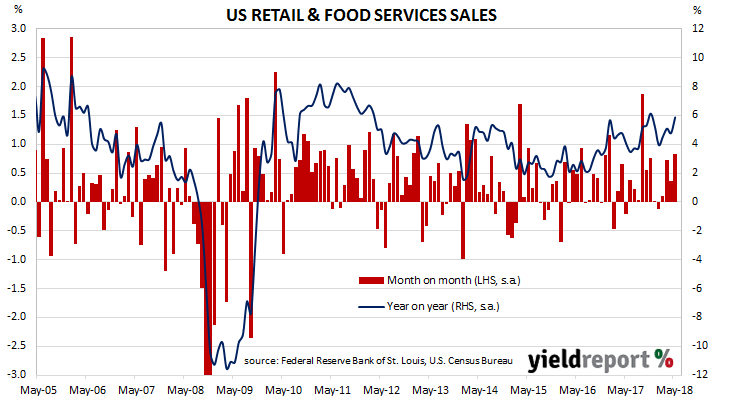

Retail sales account for a large part of consumer spending, which itself is typically the largest segment of GDP in an advanced economy. Changes in retail sales have a large effect on GDP growth rates and thus they are of great interest to economists, policy makers and financial markets.

US retail sales had been weak through the Christmas period and into the first couple of months in 2018 but then figures for March and April marked a departure from this trend. The latest May figures have added further evidence of buoyant consumer spending.

According to the latest “advance” sales numbers released by the US Census Bureau, retail sales grew by 0.8% over the month and by 5.9% when compared with the same period last year. The figures were twice as much as the expected figure as well as April’s comparable figure after it had been revised up from +0.3% to +0.4%.

13 June 2018

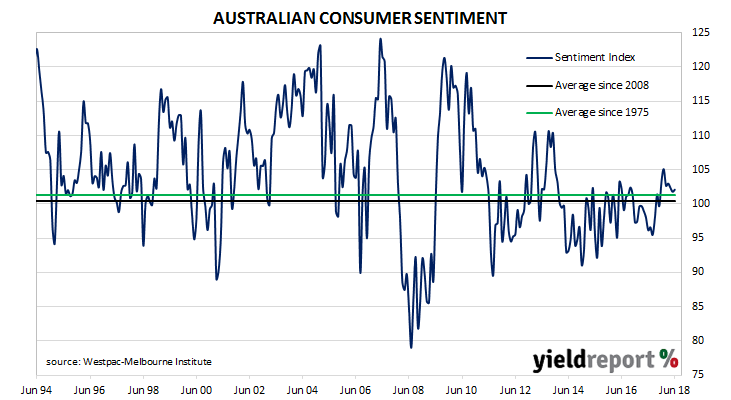

During most of the period between 2014 and 2017 there was a divergence between consumer sentiment and business confidence in Australia. Some economists explained the difference by a lack of wage growth; low wage growth is good for business in keeping costs down and margins up but households’ propensity to spend is hampered. Other explanations, such as households’ debt levels and the threat of higher mortgage rates have also been put forward.

According to the latest Westpac-Melbourne Institute Consumer Sentiment Index, households’ levels of optimism improved slightly as the Index inched up from May’s reading of 101.8 to 102.1 in June. Any reading above 100 indicates the number of consumers who are optimistic is greater than the number of consumers who are pessimistic. The long-term average reading is just over 101.

13 June 2018

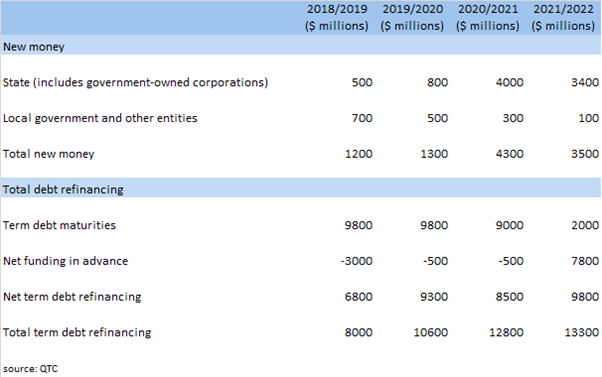

The Queensland Government has released its 2018/2019 budget and as a result, Queensland Treasury Corporation (QTC) estimates it will borrow $8 billion in 2018/2019. This figure is about $1.8 billion less than forecast in QTC’s 2017/2018 funding requirement and it is the result of QTC pre-funding transactions. Pre-funding is the term used to describe the sale of bonds in excess of what is required for the current year.

Nearly 90% of QTC’s bond issues scheduled for the 2018/2019 year will be used to finance the $9.8 billion of QTC bonds due to mature during the year. Only $1.2 billion will be raised for new expenditure. $3 billion has already been raised in pre-funding during 2017/2018, leaving another $8 billion to be borrowed.

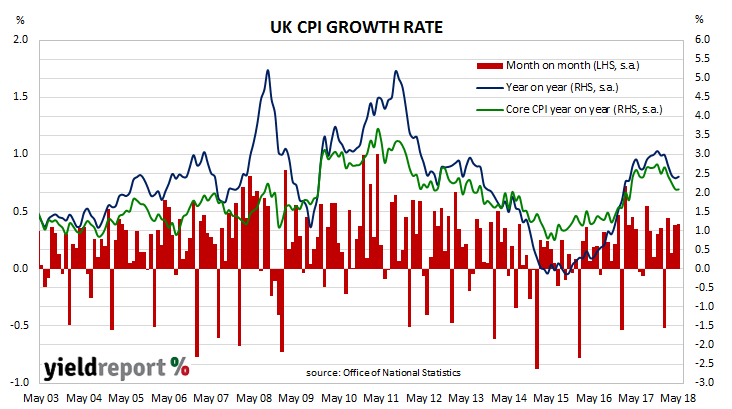

13 June 2018

The UK economy is unlike most European economies. It has an unemployment rate which is only bettered by Germany and it has no problem with deflation. It was also one of the first countries to get inflation back to within its central bank’s stated target range of 2%-3%.

The annual rate of UK consumer inflation stabilised in May, maintained predominantly by higher fuel prices and other transport costs. Consumer price index (CPI) figures released by the Office of National Statistics (ONS) indicated seasonally-adjusted consumer prices increased by 0.4% over the month, which is more than markets expected but the same as March’s comparable figure. On a 12-month basis, the consumer inflation rate remained unchanged at 2.4% (seasonally adjusted).