31 May 2018

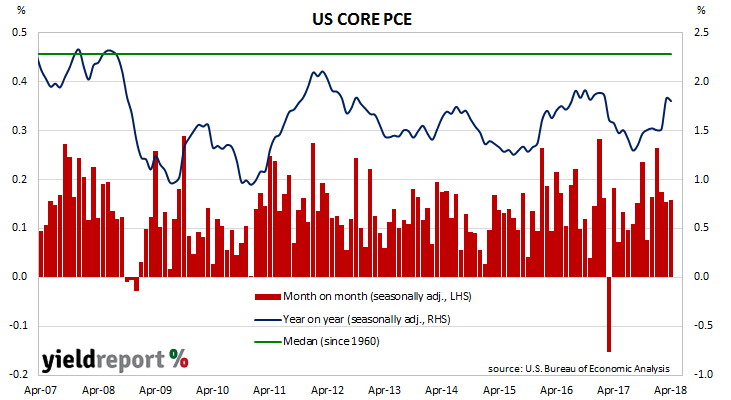

One of the US Fed’s favoured measures of inflation is the change in core personal consumption expenditures (PCE). The core version of consumer spending strips out energy and food components, which are volatile from month to month, in an attempt to identify the prevailing trend. It’s not the only measure of inflation used; the Fed also tracks the Consumer Price Index (CPI) and Producer Price Index (PPI) from the Department of Labor.

The latest PCE figures have been published by the Bureau of Economic Analysis as part of the April figures for personal income and expenditures report. At 0.2% for the month, core PCE inflation was the same as March’s figure but more than the +0.1% which was expected.

On an annual basis, growth of core PCE recorded 1.8% as expected and the same as March’s comparable figure of 1.8% after revisions. Annual core PCE inflation had moved above 1.6% in March after ranging between 1.3% and 1.6% for the previous twelve months. April’s result is the second consecutive month in which the annual rate has remained above the top of this range.

30 May 2018

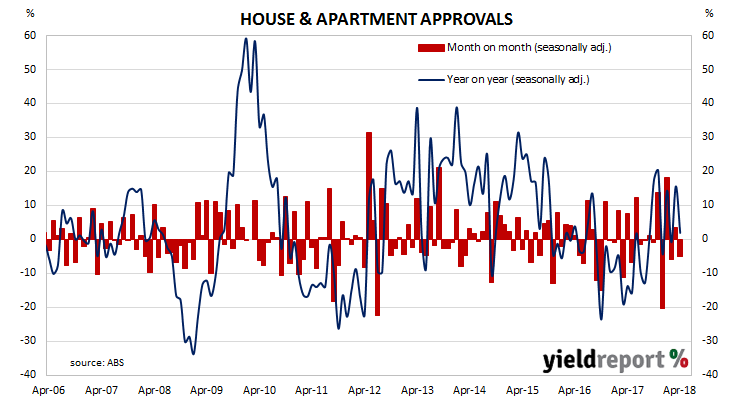

Aside from engineering and architectural design, one of the earliest requirements of a building project is to obtain approval from the relevant statutory body. As a result, building approvals data is a leading economic indicator of future construction. While not all projects which have been approved are completed, all completed projects have been granted approval. Approvals data thus provides a useful indicator of future construction.

The latest building approval figures have been released by the Australian Bureau of Statistics and the month-to-month swings caused by volatile apartment approval numbers have continued. Total April approvals were 5.0% lower than March’s revised total and a little lower than the median forecast of -5.0%. On a 12-month basis and after revisions, total approvals were 1.9% higher.

House approvals increased by +0.7% in April while they were 11.3% higher on a 12-month basis. The corresponding figures for March after revisions were +1.5% for the month and +10.8% for the year. Apartment approvals are a lot more volatile (see chart below) and they dropped by 6.1% in April after a 6.1% increase in March. Compared to March 2017, apartment approvals were 8.2% lower.

29 May 2018

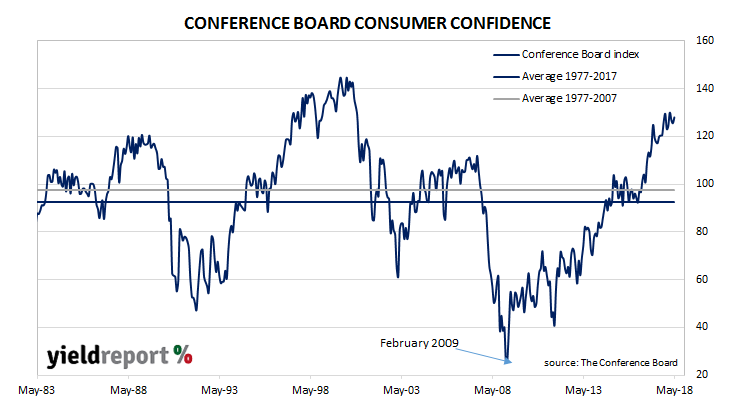

The University of Michigan’s Index of Consumer Sentiment is one of two monthly US consumer sentiment indices, the other being The Conference Board’s Consumer Confidence Survey. It covers personal finances, business conditions and buying conditions.

The latest May survey includes responses up to 16 May and it indicates US consumers consider current conditions to be more favourable while their views regarding prospective conditions are described as having “improved modestly.” The net result was an increase in the index from a revised 125.6 in April to 128.0 in May.

Lynn Franco, Director of Economic Indicators at The Conference Board said, “Overall, confidence levels remain at historically strong levels and should continue to support solid consumer spending in the near-term.” However, readings regarding consumers’ expectations suggest “the pace of growth over the coming months is not likely to gain any significant momentum.”

23 May 2018

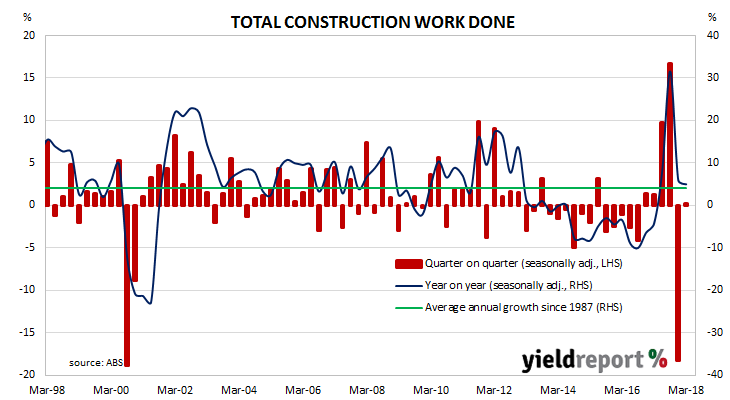

Quarterly construction data compiled and released by the ABS are not considered to be of a “primary” nature in the same way as unemployment (Labour Force) and inflation (CPI) figures. However, the figures are viewed by economists and analysts with interest as they directly feed into quarterly GDP figures which come out two weeks later.

According to the latest construction figures published by the ABS, the value of construction work stabilised in the March quarter after a spike and subsequent reversal in the September and December quarters. Total construction in the March quarter increased by 0.2%, which is less than the 1.3% increase expected and in stark contrast to the 18.3% fall previously recorded. On an annual basis, the growth rate dropped back from December’s revised figure of +6.0% to +5.0% in the March quarter. ANZ senior economist Daniel Gradwell described the figures underlying the construction report as “solid” even though the headline figures were below expectations. “Work continues to steam ahead in the public sector, while the housing sector still has some life left. Despite some emerging weakness in the non-residential segment, we expect private construction will make a modest contribution to Q1 (March quarter) GDP growth.”

ANZ senior economist Daniel Gradwell described the figures underlying the construction report as “solid” even though the headline figures were below expectations. “Work continues to steam ahead in the public sector, while the housing sector still has some life left. Despite some emerging weakness in the non-residential segment, we expect private construction will make a modest contribution to Q1 (March quarter) GDP growth.”

23 May 2018

Next month, the Federal Open Market Committee (FOMC) is expected to raise the US Fed’s target range for the federal funds rate by 25bps. Currently, the band sits at 1.50% to 1.75% and the increase will move it to 1.75% to 2.00%. It would be the US central bank’s second increase of the year in which three, possibly four, increases are expected.

The minutes of the FOMC’s latest meeting in early May gave no reason for a change in this view. However, there were one or two sections which gave economists and other observers something to chew on.

The main point of interest was the comment the Fed is happy to let inflation overshoot. ANZ economist Jack Chambers pointed to a section in the minutes discussing this possibility and they “noted that a modest inflation overshoot ‘could be helpful’ ”. He interpreted this statement as a “dovish” sign; that is, even if inflation were to move higher than its 2% target, the statement suggests the FOMC would not necessarily raise the federal funds rate. He also noted the discussion of the yield curve and its predictive powers with regards to recessions. In spite of these points, “the Federal Reserve remains on track to increase rates in June” and once again later in the year. “Overall, the minutes are consistent with a total of three, rather than four, rate hikes this year.”

23 May 2018

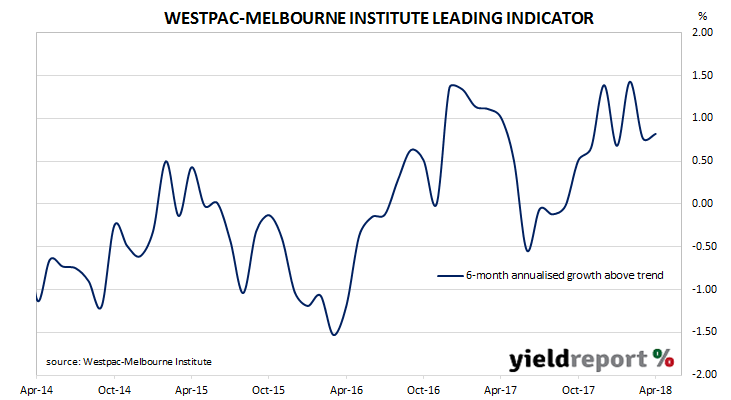

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of economic activity relative to trend in Australia. The index combines certain economic variables which are thought to lead changes in economic growth into a single variable. This variable is claimed to be a reliable cyclical indicator for the Australian economy and an indicator of swings in Australia’s overall economic activity.

Since October, the Leading Index has returned values which implied above-trend growth in the near future. The series has continued its yoyo-like behaviours in the first quarter of 2018 but the index is still in positive territory, which indicates above-trend economic growth. The six month annualised growth rate of the indicator increased from a revised +0.77% to +0.82%. These figures represent growth rates relative to trend-GDP growth, which is generally thought to be around 2.75% per annum for Australia.

21 May 2018

Back in February, NAB said it expected just one rate rise in 2018. It said its previous forecast of an August increase had been pushed out to “late 2018”, based on the data available at that time. Given most RBA rate changes have been in either February, May, August or November, “late 2018” was likely to have meant November.

Now, NAB expects no rate increases in 2018 at all. It was the last of the major banks to change its view to the “no rate increases in 2018” scenario, Commonwealth Bank having done so in the first week of this month.

NAB has joined Westpac, ANZ and Commonwealth, all of whom expect the first official rate increase by the RBA in 2019. Commonwealth expects a rate rise in February, while Westpac and ANZ expect the first increase to be more in the middle of the year.

The triggers for NAB’s change came just over a week ago after the release of March quarter wage price index and April Labour Force figures.

NAB’s view of economic growth, employment growth and wages has not changed. “In particular, our view has been that economic growth will strengthen over the coming year and that, with the pace of jobs growth already solid, this would lead to a declining unemployment rate and as a result upwards pressure on wages growth and inflation.”

After last week’s reports, NAB came to the conclusion a rate rise in November “is too early and we now expect the RBA to be on hold through the rest of this year.” NAB cannot see the RBA moving while wages grow at 2% or thereabouts. “Quite reasonably, the RBA does not see 2% wages growth as consistent with 2.5% inflation over time and wants to see some pick-up in wages before lifting rates.”

16 May 2018

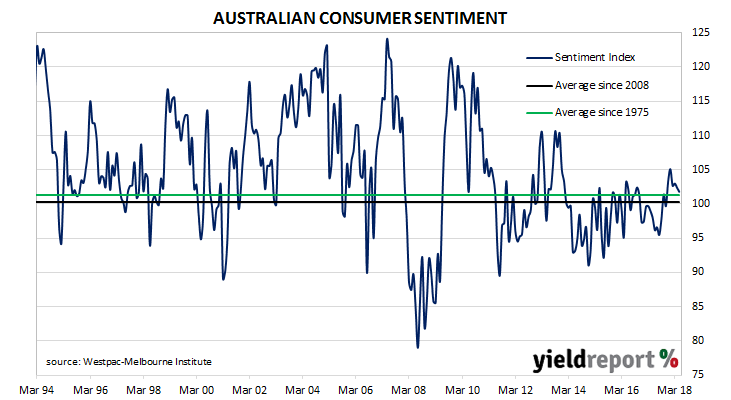

During most of the period between 2014 and 2017 there was a divergence between consumer sentiment and business confidence in Australia. Some economists explained the difference by a lack of wage growth; low wage growth is good for business in keeping costs down and margins up but households’ propensity to spend is hampered. Other explanations, such as households’ debt levels and the threat of higher mortgage rates have also been put forward.

According to the latest Westpac-Melbourne Institute Consumer Sentiment Index, households’ levels of optimism slipped again as the Index dropped back from April’s reading of 102.4 to 101.8 in May. Any reading above 100 indicates the number of consumers who are optimistic is greater than the number of consumers who are pessimistic. The long-term average reading is just over 101.

The survey was held in the second week of May, a week which contained the Federal Budget. Westpac chief economist Bill Evans said half the survey had been conducted before the budget and half had been conducted afterwards. He had noticed a clear distinction between results of the two groups; households which had been surveyed after the budget were more optimistic.

15 May 2018

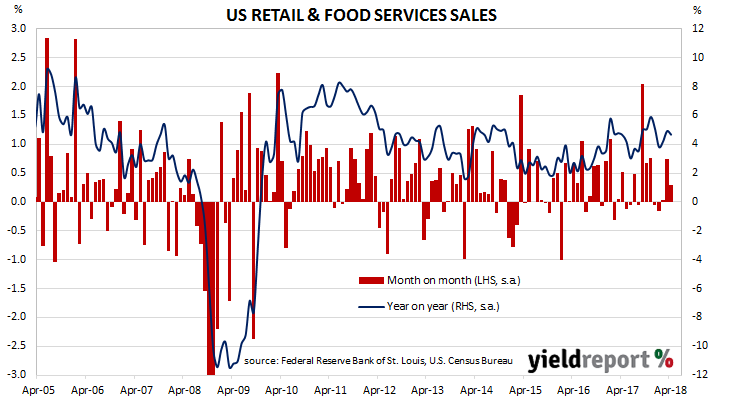

Retail sales account for a large part of consumer spending, which itself is typically the largest segment of GDP in an advanced economy. Changes in retail sales have a large effect on GDP growth rates and thus they are of great interest to economists, policy makers and financial markets.

US retail sales had been weak through the Christmas period and into the first couple of months in 2018 but then figures for March seemed to mark a departure from this trend. The latest April figures have added further evidence of some strength in consumer spending.

According to the latest “advance” sales numbers released by the US Census Bureau, retail sales grew by 0.3% over the month and by 4.7% when compared with the same period last year. The figures were in line with the +0.3% median expectation but lower than March’s comparable figures which were revised up from +0.6% to +0.8%.

15 May 2018

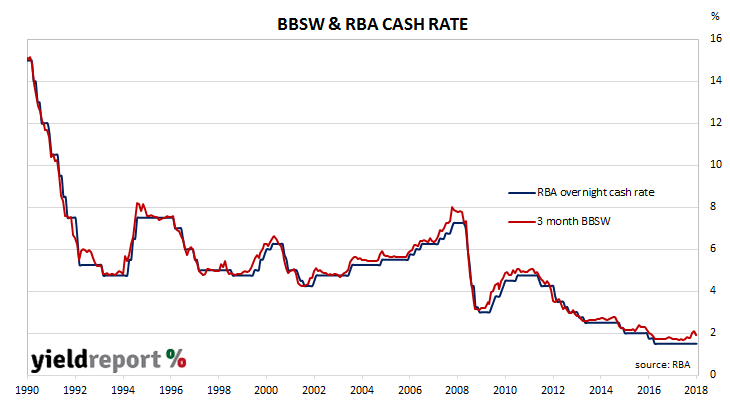

The RBA held the official cash rate steady at its board meeting in May, a decision which surprised very few people. Given the current state of prices in the cash futures market, there is no material expectation of any rate rises this year and well into 2019.

The minutes from that meeting have now been released and, as Commonwealth Bank’s Kristina Clifton said, there were “no surprises”. In fact, there is very little indication of any change on the horizon. As Bill Evans, Westpac’s chief economist put it, “If anything, these minutes seem to imply even greater patience with the current policy of steady rates. In describing the current policy as ‘a source of stability and confidence’, the Bank is clearly contrasting its policy with the Federal Reserve’s ongoing tightening cycle, but feels no embarrassment with its stance.”

There was also some discussion by the RBA of movements in BBSW which had created some unease recently. It explained a higher BBSW in terms of a flow-on effect of “higher cost of borrowing in US dollar short-term money markets” into other markets “including Australia.” Unfortunately, the board could not provide much guidance as to whether it was a short-term aberration or something else. “It is not clear how much of the rise in LIBOR and hence BBSW is due to structural changes in money markets and how much is temporary. In the last couple of weeks, these money market rates have declined noticeably from their peaks. We will continue to monitor how this unfolds in the period ahead.”