16 March 2018

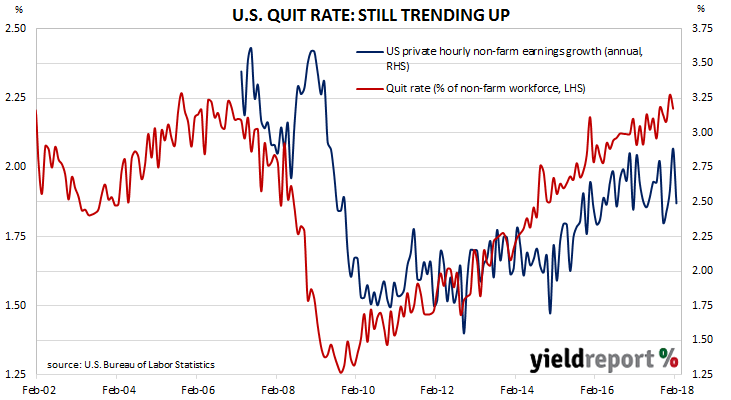

The quit rate time series produced by the Job Openings and Labor Turnover Survey (JOLTS) is a leading indicator of U.S hourly pay. As wages account for around 55% of a product’s or service’s price*, wage inflation and overall inflation rates tend to be closely related. Former Federal Reserve chief Janet Yellen was known to pay close attention to the quit rate but whether new Fed chief Jerome Powell regards the indicator with as much interest is as yet unknown.

Figures released as part of the January JOLTS report show the quit rate slipped back from a revised figure of 2.2% of the non-farm workforce at the end of December to 2.1% at the end of January. The fall was driven by lower quit figures in the professional/business services sector and, to a lesser extent, the healthcare sector.

14 March 2018

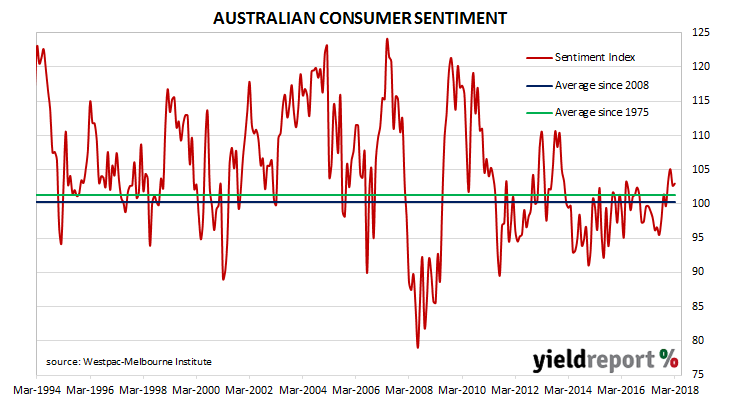

During most of the period between 2014 and 2017, there was a divergence between consumer sentiment and business confidence in Australia. Some economists explained the difference by a lack of wage growth; low wage growth is good for business in keeping costs down and margins up but households’ propensity to spend is hampered. Other explanations, such as households’ debt levels and the threat of higher mortgage rates have also been put forward.

After the Westpac-Melbourne Institute, December consumer survey was released, there was some talk of a possible alignment of the business and household sectors. The January survey provided some support to this line of thinking but recent reports have failed to narrow the gap.

According to the latest Westpac-Melbourne Institute Consumer Sentiment Index, households were slightly more optimistic than a month ago as the Index edged up from 102.7 in February to 103 in March. Any reading above 100 indicates the number of consumers who are optimistic is greater than the number of consumers who are pessimistic. The long-term average reading is just over 101.

14 March 2018

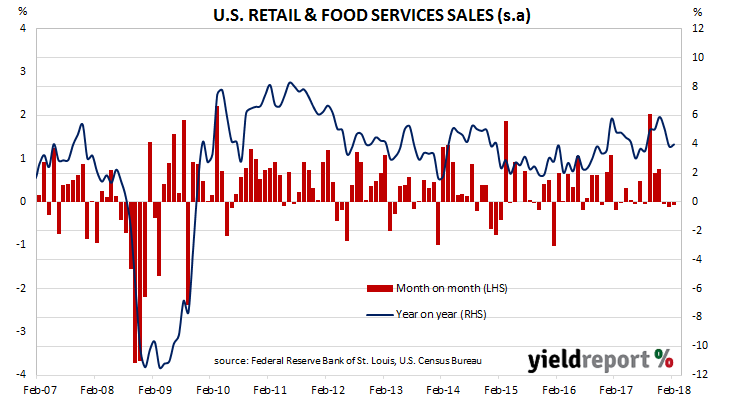

Unemployment may be low in the U.S. but U.S. household spending went backwards again as vehicle sales fell nearly 1%. According to the latest “advance” sales numbers released by the U.S. Census Bureau, February retail sales shrank by 0.1%.

U.S. financial markets reacted by sending bond yields lower at the long end. By the end of the day, 2 year yields were 1bp higher at 2.26% while 10 year yields were 2bps lower at 2.82% and 30 year yields were 4bps lower at 3.06%. The U.S. currency was stronger against the euro, steady against the pound and weaker against the yen and Aussie.

The fall in total retail sales makes February the third month in a row of lower retail sales after the previous two months’ figures were revised. The decline is well below the market’s expectation of +0.3% and in line with January’s revised -0.1%. However, as sales figures fell heavily in February 2017, the 12-month growth rate actually increased from 3.9% to 4.0%.

13 March 2018

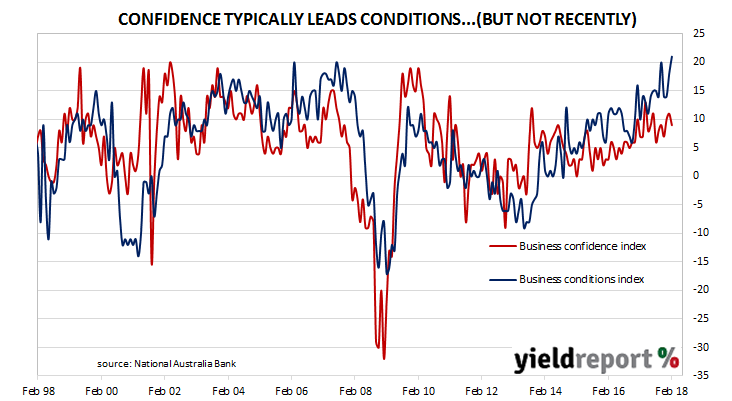

Over the last few months, the adjectives used by NAB economists to describe business conditions have strengthened from “solid” to “elevated”. “Record high” is the current description. According to NAB’s latest monthly business survey of 400 firms conducted in the middle of February, its Business Conditions Index increased to 21, the highest reading on record since the survey began.

Typically, NAB’s confidence index leads the conditions index by approximately one month, although in recent months the two surveys have diverged and the condition index has led the confidence index higher in trend terms since late 2014. The latest figures have not changed this situation. The confidence index slipped from a revised figure of 11 in January to 9 in February, a figure which is just within the “normal” bound above the long term average reading of 6.

The capacity utilisation rate, generally accepted as an indicator of future investment expenditure, slipped back from 82.7% to 82.5%, but it is still well above its long-term average reading. All but the “Transport & Utilities” sector were reported to be operating at or above their long-run averages.

ANZ senior economist, Daniel Gradwell summed up the report. “Australian business conditions pushed higher in February, reaching a new peak. The improvement was broad based across the states, and the underlying details were positive. Businesses appear to be in a purple patch at present, and forward-looking indicators suggest this will continue to translate into a strong labour market.”

13 March 2018

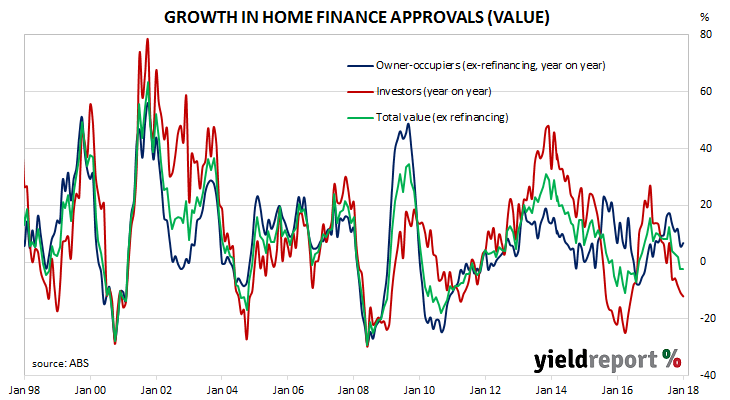

The Australian Bureau of Statistics (ABS) collects data on housing finance commitments made by significant lenders and their figures include secured (mortgage) finance commitments for the construction or purchase of owner-occupied dwellings and investment properties. It has some overlap with the RBA’s monthly private sector credit statistics which also includes investor lending and owner-occupier lending.

The ABS has released housing finance figures for January and the figures indicate the number of owner-occupier approvals were 1.1% lower over the month and 1.9% lower than January 2017. Excluding refinancing, the number of approvals declined by 1.8% for the month but they increased by just +0.2% on a yearly basis.

In dollar terms, owner-occupier loan approvals excluding refinancing increased by 0.3% in January, a sharp turn-around from December’s -2.5% and 6.7% higher than in January 2017. Investor loans grew by 1.1%, which is also a marked reversal of December’s 2.9% fall but they are still 12.1% less than investor loans from the previous January. The total value of loan approvals (ex-refi) increased by 0.7% for the month but it was -2.6% on a year-on-year basis.

Kristina Clifton, a senior economist at CBA said property investors had been a major part of January’s increase. “The rise this month was driven by investors, with the value of loans to owner-occupiers posting a small fall due to a drop in loans to first home buyers. Lending to investors has cooled but remains at a high level despite higher interest rates for investors, particularly those with interest only loans.”

13 March 2018

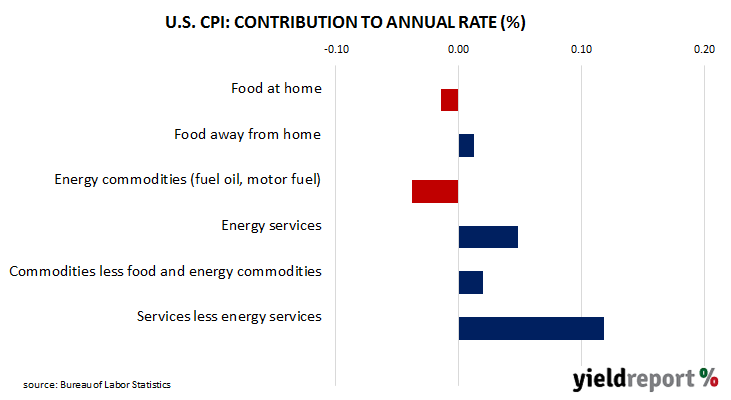

U.S. consumer inflation fell back in February as lower fuel and food prices largely offset increases in implied rents and clothing prices. Consumer price index (CPI) figures released by the Bureau of Labor Statistics indicated seasonally-adjusted consumer prices rose by 0.2% in February, in line with expectations but lower than January’s comparable figure of 0.5%. However, on a 12-month basis, the consumer inflation rate increased from 2.1% to 2.3% (seasonally adjusted).

Financial markets reacted by sending bond yields and the USD lower, although Rex Tillerson’s dismissal as U.S. Secretary of State via Twitter was thought to have had some effect. 2 year bond yields fell by 2bps to 2.25% while 10 year and 30 year yields dropped by 3bps each to 2.84% and 3.10% respectively. The new figures did not change the likelihood of a rate increase at the next FOMC meeting and, according to federal funds futures, the probability of a March rate rise remained just under 90%.

09 March 2018

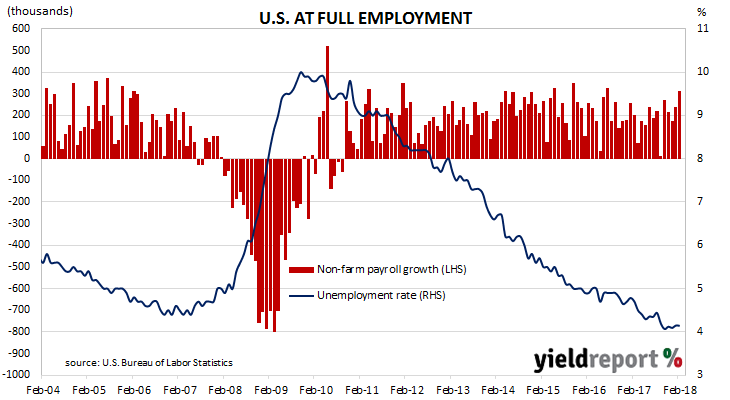

The U.S. economy has produced a bumper month of job creation and kept the U.S un-employment rate at its lowest level since February 2001. According to the U.S. Bureau of Labor Statistics, the U.S. economy created 313,000 jobs in the non-farm sector in February.

The latest figures also include upward revisions to previous employment numbers. January’s figure was revised up from +200,000 to +239,000 and the December number was revised up from +160,000 to +175,000.

The market’s expectation for employment growth during the month was for +200,000 additional positions. U.S. financial markets initially reacted by sending yields higher before they partially slipped back. By the end of the day, 2 year and 10 year yields were 3bps higher at 2.27% and 2.89% respectively while 30 year yields were 4bps higher at 3.16%. The U.S. currency was stronger against the yen, steady against the euro and weaker against the pound and the Aussie. According to cash futures prices, the implied probability of a rate rise by the U.S. FOMC at its upcoming March meeting moved up from 87% to 90%.

07 March 2018

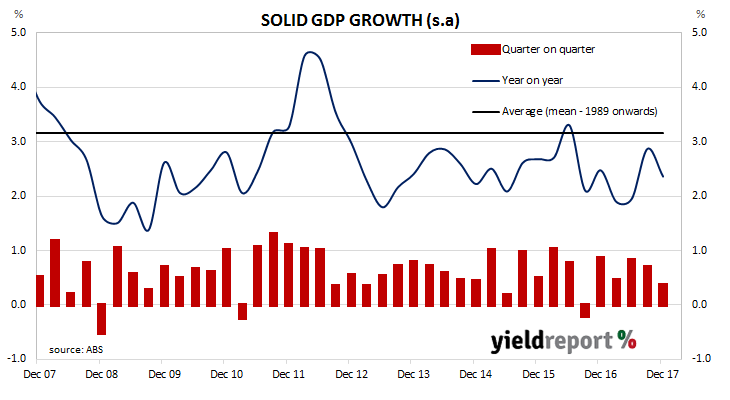

A recession is generally defined by economists as two consecutive quarters of negative GDP, an event which last occurred in Australia in 1991 which became known as “the recession we had to have”. Since that time, Australia has had the odd negative quarter, such as in the September quarter of 2016 and the March quarter of 2011, but not two in a row.

The latest figures released by the ABS indicated December quarter GDP grew by 0.4%, just under the 0.5% expected by economists. Growth in the December quarter was less than September’s 0.7% and the year-on-year growth figure fell from a revised rate of 2.9% to 2.4%.

Markets were largely unperturbed by the figures and bond yields finished the day a little lower while the local currency remained unchanged. 3 year bond yields fell 2bps lower to 2.10%, 10 year yields fell 3bps to 2.78% and the local currency finished at 78.25 U.S. cents.

Growth in the quarterly figures was primarily driven by increased spending on consumables and, to a lesser degree, government investment. Private sector investment and lower exports were the primary drags on growth.

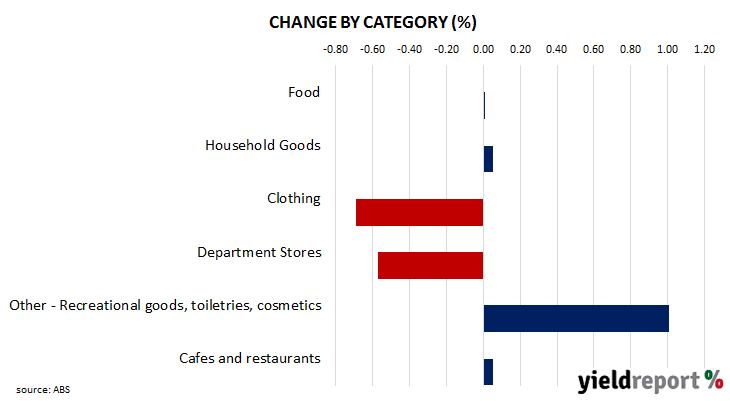

06 March 2018

After a large fall in consumer spending in December, January sales have recovered to some extent but even so, one Westpac economist described the figures as “a fairly bleak read”.

Five out of the six sales categories experienced weak growth or actual contractions and clothing sales and department store sales fared the worst. Only the “Other” category, which includes books, recreational goods, cosmetics and toiletries amongst other things, grew by more than an anaemic rate.

Total retail sales (seasonally adjusted) increased by 0.1% in January, after falling by 0.5% in December. On a year-on-year basis, sales grew by 2.1%, down from the previous month’s 2.5% annual rate.

06 March 2018

The March board meeting of the RBA is historically not one of the four months of the year in which the likelihood of a rate change is highest. February, May, August and November happen to be the four months of the year in which previous rate changes have typically occurred.

As expected, the RBA announced Australia’s overnight cash rate would remain at 1.50%. The RBA Governor had pointed out in his February testimony before the House of Representatives Standing Committee on Economics the Reserve Bank “does not see a strong case for a near-term adjustment of monetary policy.”

However, there was a couple of points of interest to come out of the statement which followed the meeting. Several economist, including Westpac chief economist Bill Evans, observed what appears to be lowering of the RBA’s growth forecasts. He pointed to the RBA’s forecast “for the Australian economy to grow faster in 2018 than it did in 2017” and noted this was different from February’s Statement on Monetary Policy forecast of 3.25% in 2018 and 2019. He said the difference “can be interpreted as the Bank now feeling comfortable with growth being above 2.5%, which is a major qualification of the Bank’s previous growth outlook.”

The other point of interest was the RBA’s forecast of an end to slow wage growth. “Notwithstanding the improving labour market, wage growth remains low. This is likely to continue for a while yet, although the stronger economy should see some lift in wage growth over time. Consistent with this, the rate of wage growth appears to have troughed…” Evans’ interpreted this statement as evidence the RBA is more confident in its outlook. “This is an upgrade from the wages commentary in previous statements.”