05 March 2018

The Melbourne Institute’s Inflation Gauge is an attempt to replicate the ABS consumer price index (CPI) on a monthly basis instead of quarterly. It has turned out to be a reliable leading indicator of the CPI, although there are periods in which the Inflation Gauge series and the CPI have diverged, only for the two series to eventually converge over the space of six to twelve months. Generally, the Inflation Gauge’s annual rate tends to overestimate changes in the CPI inflation by about 0.08%.

During February, the Inflation Gauge decreased by 0.1%, taking the annual rate to 2.1%. In January, the comparable figures were 0.3% and 2.0%. While the latest month’s inflation rate was lower than January’s rate, the annual rate rose as the February 2017 index reading had been 0.3% lower than the January 2017 figure. Therefore, the year-on-year rate started from a lower base. (Last month we wrote how this may lead to a jump in the annual rate in the following month.)

05 March 2018

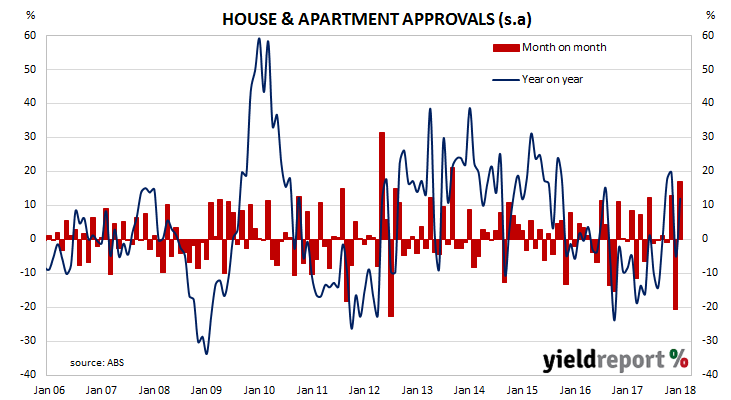

Aside from engineering and architectural design, one of the earliest requirements of a building project is to obtain approval from the relevant statutory body. As a result, building approvals data is a leading economic indicator of future construction. While not all projects which have been approved are completed, all completed projects will have been granted approval. Approvals data thus provides a useful indicator of future construction.

The latest building approval figures have been released by the Australian Bureau of Statistics and they indicate total approvals bounced back after falling in a hole in December. Total January dwelling approvals were 17.1% higher than December’s revised total and well above the median forecast of +5%. On a 12 month basis and after revisions, total approvals were 12.0% higher.

While house approvals fell by 0.9% in January, over a 12 month period approvals were still 5.9% higher. After revisions, the corresponding figures for December were +1.3% for the month and +6.2% for the year.

Apartment approvals are a lot more volatile (see chart below) and they rebounded by 43.28% in January after they plummeted 39.5% in December. Compared to January 2017, apartment approvals were 18.9% higher.

05 March 2018

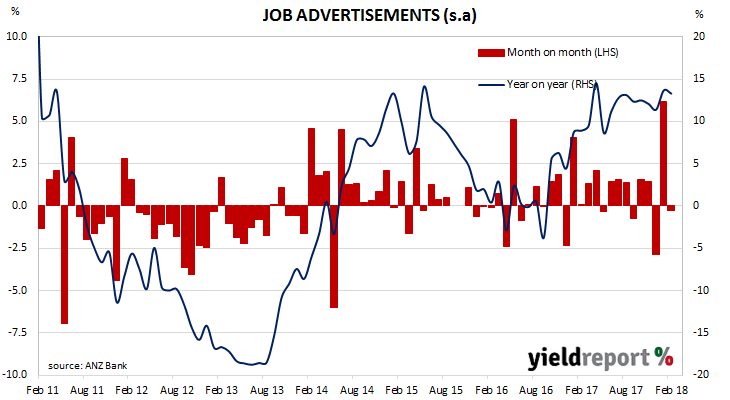

ANZ’s job advertisement survey is well-known as a leading indicator of employment numbers in Australia. It reflects changes in demand for labour and it provides another measure of activity in the economy. There is also a fairly good inverse relationship between changes in Australia’s unemployment rates and changes in the RBA cash rate. Understanding the path of Australia’s unemployment rate has historically provided a reliable indicator of RBA rate changes.

February’s figures have been released and, after revisions, total advertisements were 0.3% lower at 177,284 (seasonally adjusted), down from January’s revised figure of 177,731. On a 12 month basis, total job advertisements grew by 13.3% in February while January’s comparable growth rate was 13.7%.

ANZ Head of Australian Economics David Plank viewed the latest figures in a positive light even though they were lower than January’s numbers. In his opinion, the modest fall represented a consolidation after a big jump. “Encouragingly, ANZ Job Ads have held on to their gain in January and, as such, a slight fall in February is not cause for concern. Business conditions remain elevated, job security continues to improve and capacity utilisation now sits at the highest rate since 2008. This suggests further gains in employment and ongoing inroads into the unemployment rate, at least through the first half of the year.”

The inverse relationship between job advertisements and the unemployment rate is quite strong (see below chart). An increasing number of job advertisements as a proportion of the labour force should lead to lower unemployment rates in the near-future.

02 March 2018

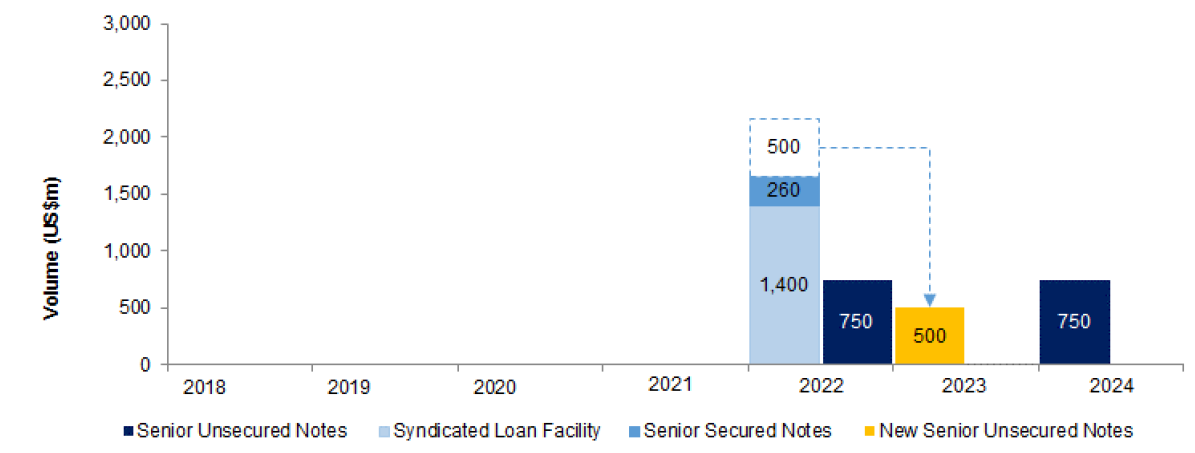

Fortescue Metals Group has announced a re-arrangement of its existing debt. The company has priced USD$500 million senior unsecured notes with a March 2023 call date.

The proceeds will be used to partly finance the redemption of USD$2.16 billion senior secured 2022 bonds, which became callable on 1 March 2018. These bonds were issued in April 2015 and were themselves used to refinance existing FMF bonds outstanding at the time.

The difference between the USD$500 million raised by this latest bond issue and the USD$2.16 billion required to redeem the 2022 bonds will be financed via a new USD$1.4 billion term loan which was announced in early February. Existing cash reserves will cover the balance.

The new March 2023 bonds will have a 5.125% coupon whereas the existing 2021 bonds have a coupon rate of 9.75%. Fortescue’s chief financial officer said the change would save the company around USD$130 million per annum in interest costs.

Source: FMG

01 March 2018

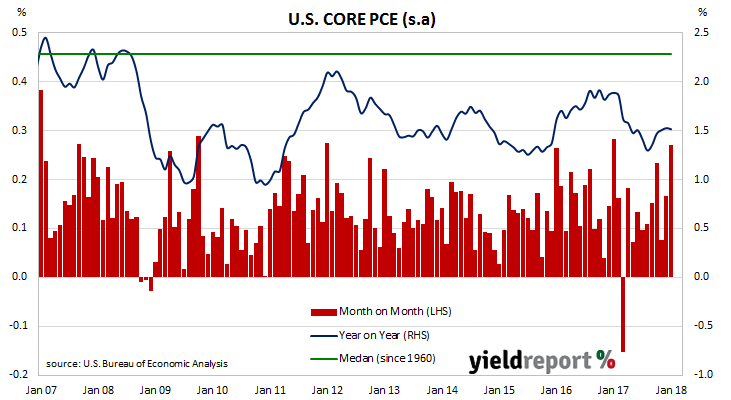

One of the U.S. Fed’s favoured1 measures of inflation is core personal consumption expenditure (PCE). The core version of consumer spending strips out energy and food components, which are volatile from month to month, in an attempt to identify the prevailing trend. It’s not the only measure of inflation used; the Fed also tracks the Consumer Price Index (CPI) and Producer Price Index (PPI) from the Department of Labor.

The latest PCE figures have been published by the Bureau of Economic Analysis as part of the January figures for personal income and expenditures report. At 0.3% for the month, core PCE inflation was in line with the market’s expectation but higher than December’s 0.2% increase.

Annual core PCE inflation has been in range of 1.3% to 1.6% since March 2017. The latest reading for annual core PCE was unchanged at 1.5% and thus the same as comparable figures for November and December.

28 February 2018

NAB is the latest major bank to change its view of official rates in 2018. It now expects just the one 25bps rate rise in 2018.

28 February 2018

The pace of lending to the non-bank private sector by financial institutions in Australia fell again for a fifth consecutive month in January. Lending has slowed to such a degree APRA chief Wayne Byres said the 10% cap on lending to real estate investors was probably “redundant”.

According to the latest RBA figures, private sector credit grew by 0.3% in January, the same as the 0.3% growth rate recorded in December and less than the 0.4% expected. The year-to-January growth rate of 4.9% also remained unchanged from December’s revised figure of 4.9% as business lending went into reverse (-0.1%) and owner-occupier loans and investor loans maintained their respective 0.6% and 0.2% per month growth rates.

The overall increase was driven by owner-occupier loans, which increased by 0.6% over the month or 8.0% for the 12 months to January. Business credit growth slowed from a 0.1% growth rate in December to -0.1% in January although its annual growth rate increased after four consecutive months of falls, this time from 3.2% to 3.4%. These two segments of total lending account for nearly three-quarters of new loans by value and thus any change in them has a greater effect on overall credit growth.

21 February 2018

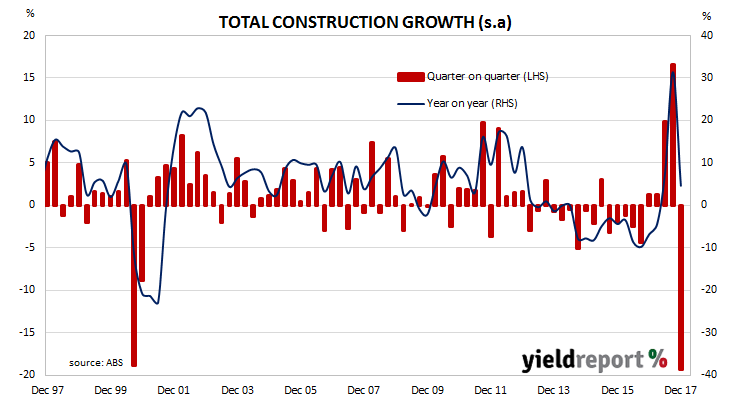

Quarterly construction data compiled and released by the ABS are not considered to be of a “primary” nature in the same way as unemployment (Labour Force) and inflation (CPI) figures. However, the figures are viewed by economists and analysts with interest as they directly feed into quarterly GDP figures which follow two weeks later.

According to the latest construction figures published by the ABS, the value of construction work dropped back by what would normally be seen as an alarming 19.4% in the December quarter. On an annual basis, the growth rate dropped back from September’s 12 month revised figure of +31.4% to +4.6% in the December quarter.

The reason analysts and economists were not particularly concerned by the massive drop is they expected a reversal after the presence of two particular items in previous quarters. Construction work had grown by outsized amounts in the June and September quarters after two LNG platforms were imported and included in those quarters’ figures. The December figures represented a return to “normal”.

21 February 2018

The minutes of the FOMC’s meeting in late January has all but confirmed another 25bps increase to the federal funds rate at its next meeting in late March. While the minutes did not add anything of a controversial or unexpected nature, they did reinforce the view the Fed would raise its official rate several times this year.

Financial markets reacted by sending U.S bond yields and the USD higher. 2 year bond yields gained 4bps to 2.26%, 10 year yields increased by 6bps to 2.95% and 30 year yields rose by 7bps to 3.22%. The USD strengthened by between 0.4% and 1.0% against all major currencies.

According to Philip Brown, a senior fixed-income strategist at Commonwealth Bank, the minutes “showed the Fed is increasingly confident on the economic and inflation outlook…” and they “also reinforced the growing FOMC optimism and ongoing hawkish intentions as outlined in previous communications – including the widely expected rate hike in March.” What’s more, Brown pointed to a section of the minutes which states “a majority of participants noted a stronger outlook for economic growth raised the likelihood that further gradual policy firming would be appropriate”. Data regarding economic activity since the December’s FOMC meeting had been stronger than anticipated and rate rises are likely to be required.

21 February 2018

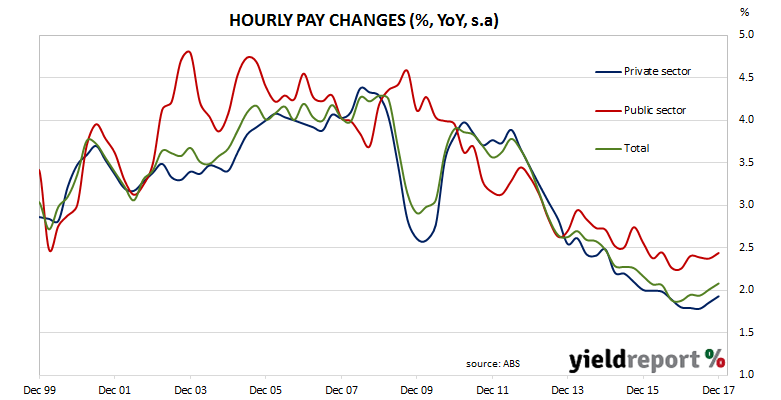

Each quarter the Australian Bureau of Statistics (ABS) surveys around 3000 enterprises regarding a sample of jobs in each workplace to measure changes in the price of labour across around 18000 jobs. The results are used to construct a wage price index (WPI). Changes in the WPI over time provide a measure of changes in wages and salaries independently of changes in the quality or quantity of work performed.

According to the latest wage price index (WPI) figures published by the ABS, hourly wages grew by 0.6% in the December quarter, up from the 0.5% increase in the September quarter and above the market’s expectations of a 0.5% increase. The year-on-year growth rate remained unchanged at 2.1% (after revisions) which makes this the second quarter in which the annual growth rate has not fallen. It is, however, still barely just above the lowest growth rate since the beginning of the series in 1999.

Financial markets reacted to the wage figures by sending yields and the AUD lower. The local bond market ignored overnight leads from offshore and 3-year bond yields finished the day 3bps lower at 2.15% while 10-year bond yields fell 4bps to finish at 2.86%. The AUD fell around 0.8 U.S. cents to 78.00 U.S. cents, although it is worth noting the USD strengthened against the euro and the yen on the same day.

Public sector hourly wage growth has continued to outstrip its private sector counterpart. Public sector hourly wages grew by 0.6% over the quarter while the growth rate in the private sector was 0.5%. On an annual basis, public sector hourly pay maintained its 2.4% growth rate while the comparable figures for the private sector remained at 1.9%.