31 January 2018

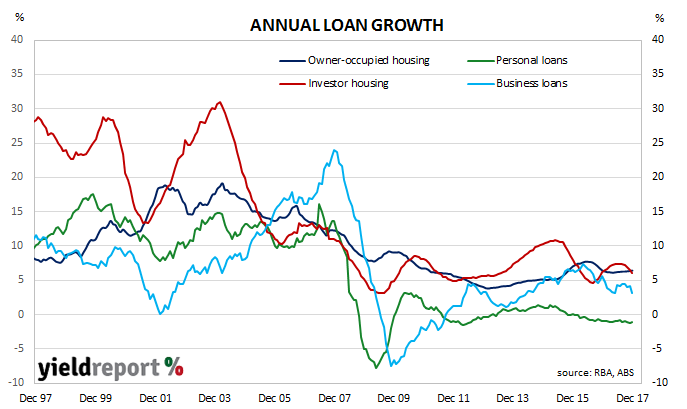

The pace of lending to the non-bank private sector by financial institutions in Australia fell again for a fourth consecutive month in December. The slowing in loan growth was noted by various economists and commentators but at the same time the various figures attracted little in the way of controversy. In any case, attention was focussed on December CPI figures which came out later in the day.

According to the latest RBA figures, private sector credit grew by 0.3% in December, down from the 0.4% growth rate recorded in November and less than the 0.5% expected. The year-to-December growth rate of 4.8% slipped from November’s comparable figure of 5.2% (after revisions) as personal loans contracted while business and investor loan growth rates slowed.

30 January 2018

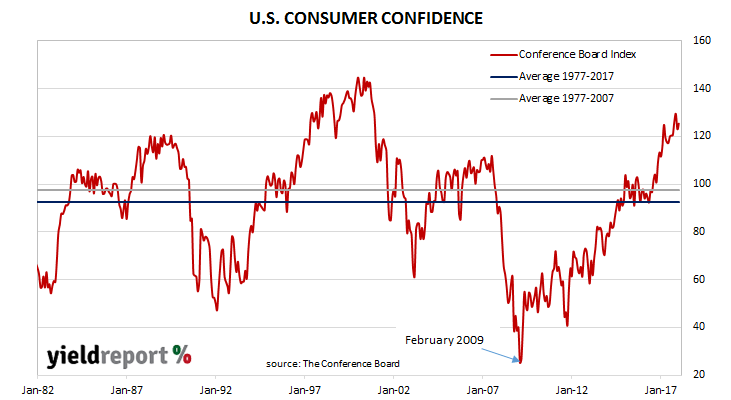

Consumer confidence surveys are important private sector surveys even though economists view them as lagging indicators. Their importance lies in the confirmation of spending patterns. As consumption in developed countries may amount to 60%-70% of GDP, knowing how it is behaving is important for financial markets’ forecasts of GDP growth rates, which in turn flow into credit growth and inflation rates.

The January reading of the Conference Board’s Consumer Confidence Index came in at 125.4, up from December’s revised reading of 123.1 and much higher than 2017’s comparable January figure of 111.6. The index was the result of a survey which ended on 18 January 2018.

Households’ views of current conditions slid, albeit from high levels. Expectations of the near-future improved although households were described by Lynn Franco, Director of Economic Indicators at The Conference Board as “ambivalent” about the prospects of pay rises. Even so, on balance, the household sector was optimistic. “Overall, however, consumers remain quite confident that the solid pace of growth seen in late 2017 will continue into 2018.”

Households’ views of current conditions slid, albeit from high levels. Expectations of the near-future improved although households were described by Lynn Franco, Director of Economic Indicators at The Conference Board as “ambivalent” about the prospects of pay rises. Even so, on balance, the household sector was optimistic. “Overall, however, consumers remain quite confident that the solid pace of growth seen in late 2017 will continue into 2018.”

30 January 2018

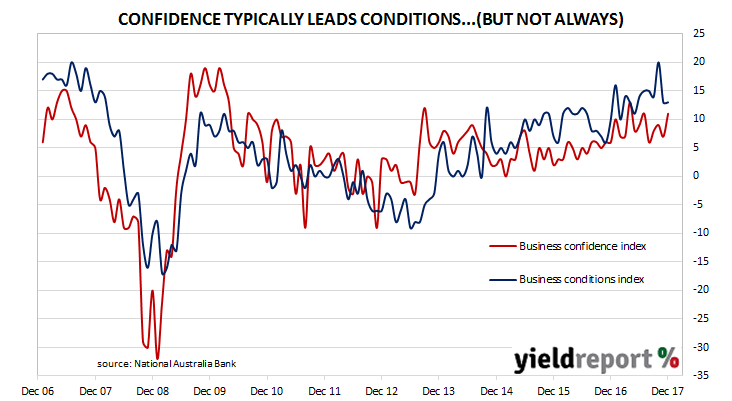

Early in December, business conditions had been described as “solid” by NAB economists; now they have upgraded their description to “strong”. According to NAB’s latest monthly business survey of 400 firms conducted in mid-January, its Business Conditions Index remained unchanged at 13 after revisions. This latest reading still represents well-above-average business conditions.

Bond and currency markets were reserved in their reactions. 3 year bond yields were steady at 2.27%, 10 year bond yields added 1bp to 2.87% but the local currency was slightly lower at around 80.85 U.S. cents.

Typically, NAB’s conditions index is led by its confidence index by approximately one month, although in recent months the two surveys have diverged and the condition index has led the confidence index higher in trend terms since late 2014. The confidence index increased from a revised figure of 7 at the end of November to 11 at the end of December, a figure well above its long-term average reading of 5.

30 January 2018

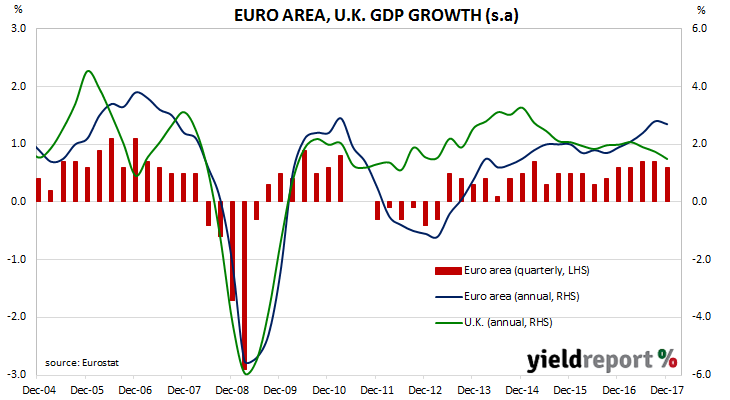

European GDP growth seems to have settled at a rate above 2%. Eurostat, the European Commission’s statistical division, released December quarter “flash” estimates of euro-area GDP on Tuesday night Australian time. They indicate GDP increased by 0.6% for the quarter and 2.7% over the last twelve months. The figures were in line with expectations but they were below September’s comparable figures of 0.7% for the quarter and 2.7% over the previous year.

These figures are the latest in a string of GDP growth rates above 2%. In response to recent stronger growth rates, the ECB announced in October it would wind back its asset purchase programme. Prior to January 2018, the ECB had been purchasing €60 billion worth of bonds and asset-backed securities each month. From January onwards, the new monthly pace of purchases was halved to €30 billion. Currently, the APP is expected to cease in September 2018.

Euro area growth rates have been higher than those of the U.K. since the June quarter. The latest December quarter growth rate in the U.K. was 1.5%.

30 January 2018

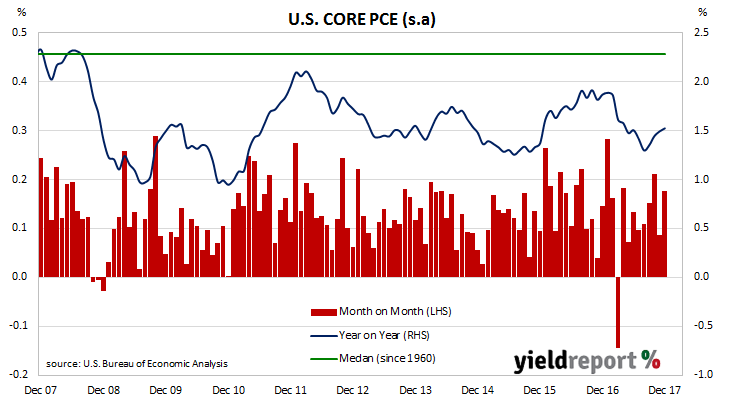

One of the U.S. Fed’s favoured measures of inflation is core personal consumption expenditure (PCE). The core version of consumer spending strips out energy and food components, which are volatile from month to month, in an attempt to identify the prevailing trend. It’s not the only measure of inflation used; the Fed also tracks the Consumer Price Index (CPI) and Producer Price Index (PPI) from the Department of Labor.

The latest PCE figures have been published by the Bureau of Economic Analysis as part of the December figures for personal income and expenditures report. At 0.2% for the month, core PCE inflation was in line with the market’s expectation. On an annual basis, it was steady at 1.5%. November’s comparable annual figure was 1.5% and October’s was 1.4%.

26 January 2018

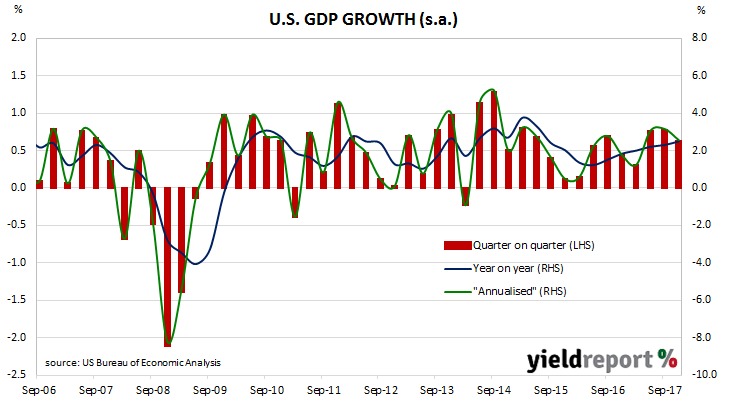

While the Davos World Economic Forum and some of its speakers absorbed a lot of attention, the U.S. economy confirmed it was doing just fine despite some blemishes. The U.S. Commerce Department released fourth quarter (Q4) 2017 “advance” estimates of US GDP on Friday night Australian time and they indicate U.S. GDP grew at an annualised growth rate of 2.6%. The growth rate was under the 2.9% median of market estimates and lower than the third quarter figure of 3.2% but generally economists and other commentators did not seem perturbed.

US GDP numbers are published in a manner which is different to most other countries; quarterly figures are compounded to give an annualised figure. In countries such as Australia and the UK, an annual figure is calculated by taking the latest number and comparing it with a figure from a year ago. The diagram below shows US GDP once it has been expressed in the normal manner.

ANZ senior economist Daniel Gradwell saw some good and bad in the figures. “The increase was slightly below consensus of 3%, but underlying details were reasonable.” However, in a comment reminiscent of the discussion going on in Australia, he remarked on the household income issue. “Durability of consumption growth will be questioned with spending continuing to outpace income growth, pushing the saving rate to a decade low of just 2.6%.”

24 January 2018

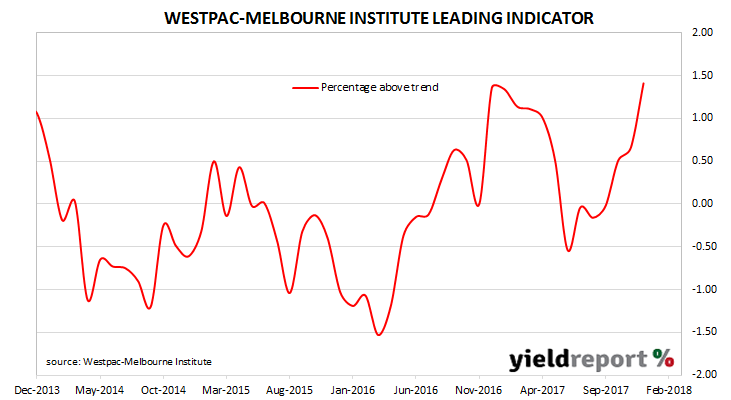

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of economic activity relative to trend in Australia. The index combines certain economic variables which are thought to lead changes in economic growth into a single variable. This variable is claimed to be a reliable cyclical indicator for the Australian economy and an indicator of swings in Australia’s overall economic activity.

Since October, the Leading Index has returned values which implied above-trend growth in the near future. In December, the indicator moved further into positive territory as it went from a revised +0.66% to +1.41%. These figures represent a growth over and above trend annual growth, which is generally estimated to be around 2.75% for Australia.

Westpac chief economist Bill Evans thought the December figures to be indicative of a higher rate of economic growth in Australia over the coming months. “This is a very strong above trend reading and, following the solid results in October and November, points to solid above trend growth in the early part of 2018.” In his view sub-indices underlying the Leading Indicator point to “a healthy mix of both international and domestic factors”.

19 January 2018

The University of Michigan’s Index of Consumer Sentiment is one of two monthly U.S. consumer sentiment indices, the other being the Conference Board’s Consumer Confidence Survey. It covers personal finances, business conditions and buying conditions.

The latest survey indicates U.S. consumers think current economic conditions were less favourable in January than at the time of the previous survey in December. However, the deterioration was small and related to current conditions, while expectations regarding the future remained unchanged. Measures of personal finances and buying intentions were described as exhibiting “persistent strength”.

Tax changes were mentioned by around one third of all respondents and the majority of these responses anticipated the impact “would be positive”. However, some uncertainty was expressed with respect to how much of a tax cut could be expected and how it would affect people on different rates of tax and in different states. Fuel prices and inflation expectations were largely unchanged and “consumers continued to remain very optimistic about the low national unemployment rate.”

18 January 2018

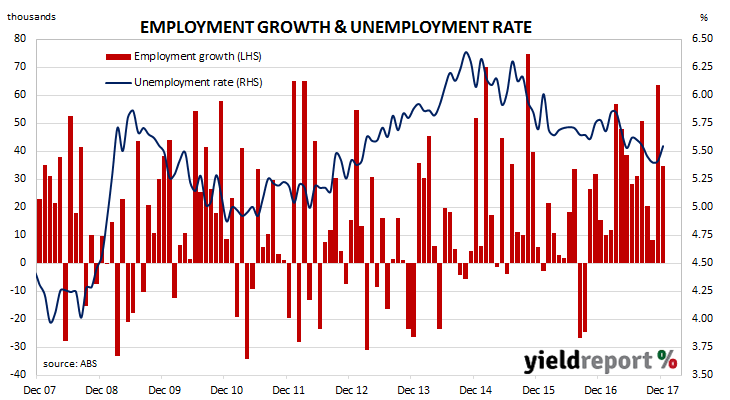

The Australian economy has recorded the fifteenth consecutive month of employment gains, as employers expanded both full-time and part-time positions. The run of monthly consecutive gains has exceeded the 14 month stretch from August 1979 to September 1980 and it is equal to the 15 months of gains from May 1993 to July 1994.

The ABS released employment estimates for December which indicate the total number of people employed in Australia in either full-time or part-time work increased by 34,700. Market expectations prior to the report’s release were for 15,000 new positions.

Bond yields finished the day higher. 3 year and 10 year bond yields each gained 3bps to finish at 2.25% and 2.82% respectively. In currency markets the Aussie initially dropped by 0.3 U.S. cents to 79.55 U.S. cents before it finished around 79.50 U.S. cents.

The participation rate increased from 65.5% to a near-record 65.7% as an additional 55,200 people entered the labour market. While total employment increased, the total number of unemployed also increased (by 20,500) and thus the unemployment rate rose from 5.4% to 5.5%.

17 January 2018

When ANZ announced the issue of its latest hybrid security in August of last year, among the various offers and options it provided to its existing securities holders, one was to buy back Converting Preference Securities III (CPS3) first issued in 2011. The offer to buy the securities at face value did not raise any eyebrows; after all, the first optional exchange date, what is generically referred to as a call date, was only months away in March 2018.

However, there was some doubt as to what ANZ had planned for the CPS3 which remained on issue. At the time ANZ itself said, “As at the date of this release, ANZ has not made any decision how it will deal with the CPS3 which are not bought-back under the Buy-Back Facility.”

Well, now there is no longer any uncertainty. ANZ announced it will pay $100 for the remaining CPS3 still on issue on 1 March 2018, plus $1.4753 franked which represents the accrued distribution up to that date.

One curious aspect of the deal is the repurchase will take place via a $99.9999 per CPS3 capital return and then a redemption of each CPS3 for $0.0001. The capital return keeps the securities “alive” in a sense whilst effectively repaying almost all the face value back to holders. The securities will be then redeemed for the balance.

The last day of trading on the ASX will be 12 February 2018.