13 December 2017

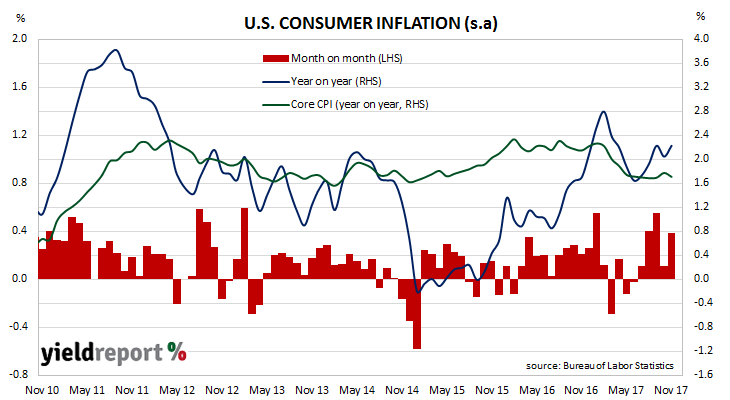

The U.S. consumer inflation rate increased in November on the back of higher fuel costs and, to a lesser degree, higher “shelter” costs. Consumer price index (CPI) figures released by the Bureau of Labor Statistics indicated consumer prices rose by 0.4% in November, ahead of market expectations of 0.3%. On a 12-month basis the consumer inflation rate rebounded from October’s 2.0% to 2.2%.

Core prices, or prices excluding food and energy, rose by 0.1% over the month and 1.7% for the year. Both these monthly and annual price changes were lower than October’s comparable figures of 0.2% and 1.8%. ANZ senior economist Felicity Emmett said core inflation rose less than the expected 0.2% as prices in a couple of retailing segments lived up to their highly variable nature. “Core US inflation rose slightly less than expected, but this was mainly due to volatile components like airfares and apparel undershooting.”

13 December 2017

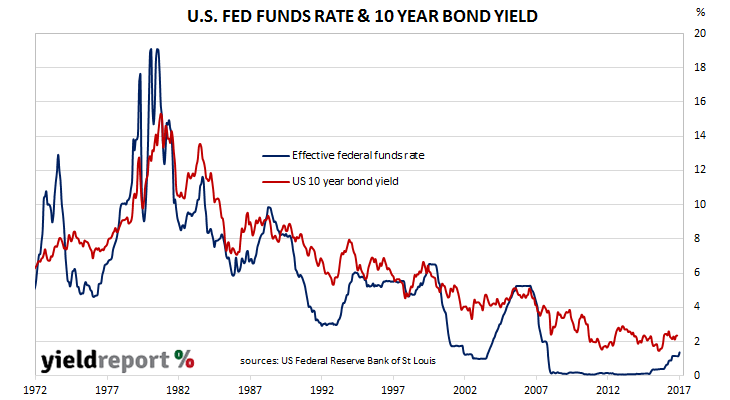

In July 2008, just as the public’s knowledge of the impending mortgage disaster in the U.S was becoming widespread, the federal funds rate was 5.25%. Six months later, it was essentially zero. The U.S. Fed was so concerned about a recession turning into a 1920s style depression, it took the extraordinary step of reducing the cost of borrowing among banks to almost nothing.

As expected, the Federal Open Market Committee (FOMC) announced another 25bps increase to the target range, taking the range to 1.25% to 1.50%. The decision was a reflection of the FOMC’s strategy of “gradual removal of monetary policy accommodation” in light of “solid” GDP growth and a “strong” labour market.

According to projections of FOMC members, there are more rate rises to come. These projections, often referred to as the “dot plots” (because each member’s forecast is represented by a dot plotted over time on a diagram), imply the FOMC expects three rate rises in 2018, taking the federal funds rate range to 2.00%-2.25% by the end of 2018. Another two 25bps rate rises are then expected for 2019.

13 December 2017

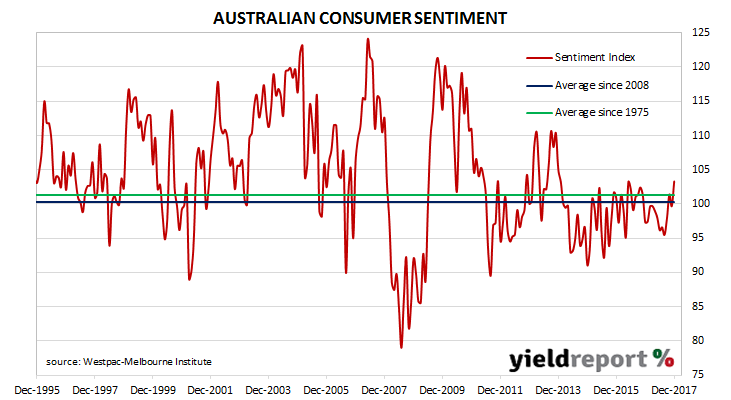

In recent months, commentators and economists have pointed to a divergence between consumer sentiment and business confidence in Australia. Most have put the difference down to a lack of wages growth. Low wages growth is good for business in keeping costs down. However, households’ propensity to spend is hampered. Other explanations, such as households’ debt levels and the threat of higher mortgage rates have also been put forward.

The latest survey of consumer confidence may be the beginning of an alignment of the business and household sectors. According to the latest Westpac-Melbourne Institute Consumer Sentiment Index, households were more optimistic than a month ago as the Index reading jumped from 99.7 in November to 103.3 in December. Any reading below 100 indicates the number of consumers who are pessimistic is greater than the number of consumers who are optimistic. The long-term average reading is just over 101.

13 December 2017

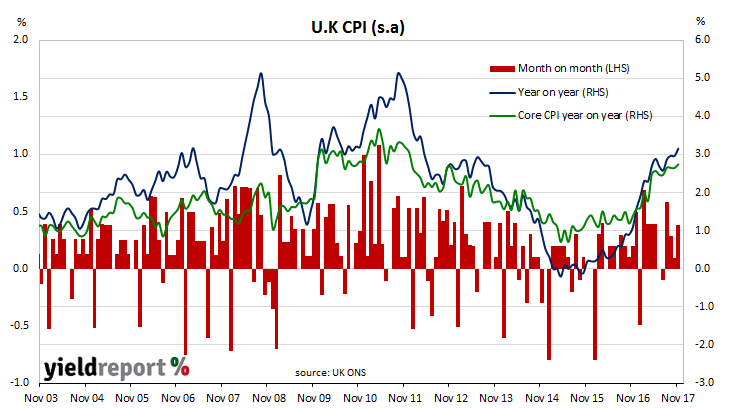

Central banks of advanced economies have kept official interest rates at historical lows since the GFC in an attempt to foster economic growth and increase inflation rates back to a commonly-preferred range of 2% to 3%. The Bank of England (BoE) is one of these banks.

The policy has been effective on both lowering the unemployment and increasing inflation rates. The unemployment rate has been under 6.0% for the last three years and under 5% since mid-2016. The inflation rate fell until around 2015 and then it began to increase gradually. In the last twelve months the pace has picked up and some measures of consumer inflation are above 3.0%.

It is too easy to tell but the BoE may be about to question the wisdom of the duration of its low-interest rate policy. According to the latest consumer price index figures from the U.K’s Office of National Statistics, consumer prices increased by 0.4% in November, up from October’s +0.1%. On an annual basis, consumer inflation rose by 3.2%, also an increase on October’s figure of 3.0%.

12 December 2017

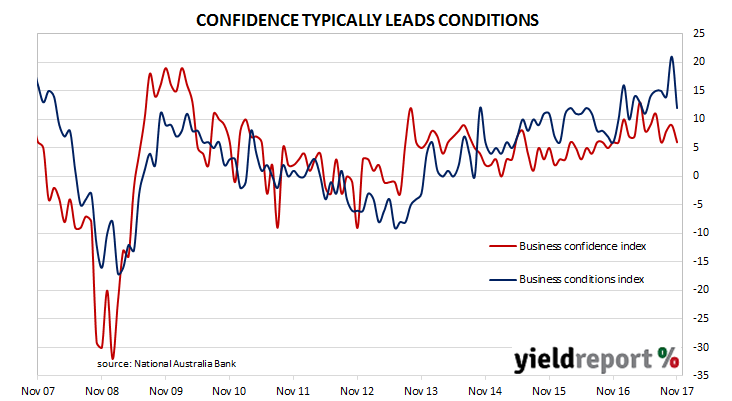

Australian business conditions have been described as “solid” by NAB economists despite a substantial fall from the previous month’s reading. According to NAB’s latest monthly business survey of 400 firms in late November, its Business Conditions Index dropped back from 21 to 12. This latest figure still represents well-above-average business conditions, as last month’s reading had been the highest on record since the index was first developed in the late 1990s.

Typically, NAB’s conditions index is led by its Business Confidence Index by around one month, although in recent months the two surveys have diverged. The confidence index recorded 6 in November, a figure pretty much in line with its average for the last two years. It is also the average of the series since the survey began.

ANZ senior economist Daniel Gradwell noted this divergence. “The persistent divergence between business conditions and business confidence perhaps suggests that businesses have been surprised by the current strength of the economy. The decline in confidence is not ideal, but historically we have seen that reported conditions are the better leading indicator of movements in the real economy.”

11 December 2017

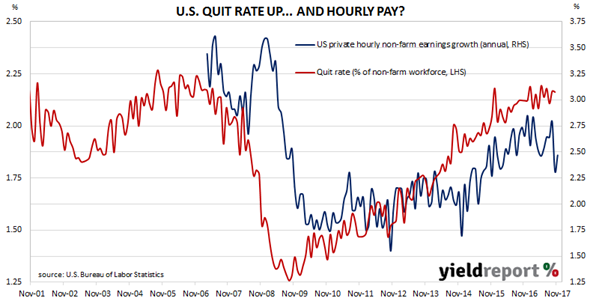

The Job Openings and Labor Turnover Survey (JOLTS) reports data collected from businesses regarding job openings and separations in the U.S. The report is perceived as an important piece of the labour market picture as it measures unmet demand for labour.

One interesting segment of the report is the “quits” rate. This figure is calculated by taking the number of employees who voluntarily leave their jobs as a percentage of the total number of (non-farm) employees. Understandably, over time it provides a guide to pressure on employers to raise wages in order to attract or keep employees. The U.S. Fed is said to pay it some attention because of its implications for inflationary pressures.

08 December 2017

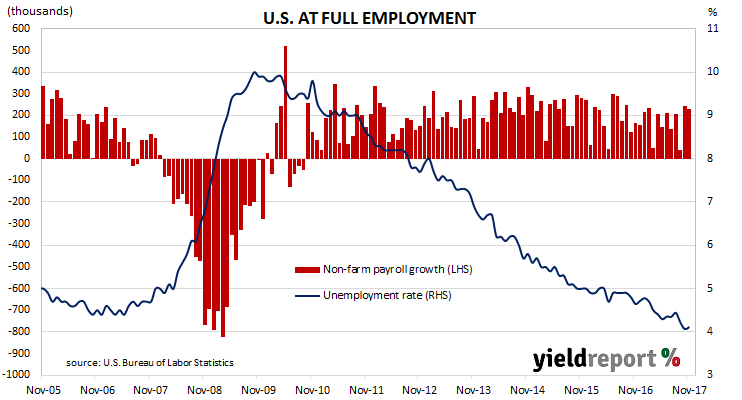

The U.S economy has managed to maintain a rate of unemployment which is the lowest for the period since February 2001. According to the U.S. Bureau of Labor Statistics, the U.S. economy gained 228,000 jobs in the non-farm sector in November while October’s figure was revised down from +261,000 to +244,000 but the September number was revised up from +18,000 to +38,000. The market’s median expectation for employment growth in November was +210,000.

After revisions to previous months’ figures, the unemployment rate remained unchanged at 4.1% as 90,000 either found work, retired or stopped looking for work. Average hourly pay rates reversed a dip in October and was 2.5% higher than in November 2016.

The total number of employed persons in the non-farm sector at the end of November was 147.2 million and 153.9 million overall. Over the past twelve months, 1.9 million jobs have been created in the U.S. with almost all of them in the non-farm sector. Another figure which is indicative of the state of the U.S. economy is the employment-to-population ratio. After a volatile few months, this ratio has settled down and came in at 60.1% for a second month in a row.

ANZ senior economist Felicity Emmett described the figures as “solid” but then she went on to focus on the wage inflation issue. “In a nutshell, economic and employment momentum remain very solid, but wage growth is subdued in the context of the broader environment….inflation expectations [are] well anchored, technological change, global integration of supply chains, increased labour mobility and low global inflation.”

Financial market reaction was unremarkable. The U.S. 2 year yield remained steady at 1.79% while the 10 year yield gained 1bp to 2.37%. The U.S currency was slightly stronger against the yen but steady against the euro. According to cash futures prices, the implied probability of a rate rise by the U.S. FOMC at its upcoming December meeting was unchanged at 100%.

06 December 2017

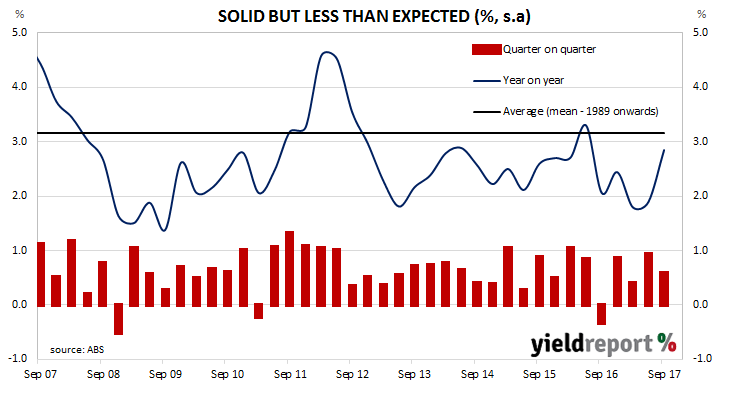

A recession is generally defined by economists as two consecutive quarters of negative GDP, an event which last occurred in Australia in 1991 which became known as “the recession we had to have”. Since that time, Australia has had the odd negative quarter, such as in the September quarter of 2016 and the March quarter of 2011, but not two in a row.

The latest figures released by the ABS indicated third quarter GDP grew by 0.6%, just under the 0.7% expected by economists. Even though the growth rate over the September quarter was less than June’s 0.9%, the year-on-year figure increased from 1.9% (after revisions) to 2.8%, which was also under the 3.0% figure expected.

Bond yields and the Aussie dropped on the release of the figures. 3 year bond yields finished the day 7bps lower at 1.96% and 10 year yields were 9bps lower at 2.53%. The local currency dropped from 76.15 U.S. cents to 75.85 U.S cents and then finished around 75.80 U.S. cents.

05 December 2017

Most of the time when one thinks of long term bonds, maturity dates 20 or 30 years from now come to mind. Those readers who have been around financial markets are probably aware the U.S Government has been an issuer of 30 year bonds for decades and even the Australian Government has joined the thirty-year club recently. However, there is long term and then there is really long term; fifty years, seventy years or even one hundred years.

One hundred year bonds are not common but they are not exceptionally rare, either. China, the Philippines, Mexico, Austria, Belgium, Ireland all have issued “century” bonds. Even serial defaulter Argentina got one away as in June this year.

It is not just sovereigns which issue the ultra-long bonds. There are also corporate 100 year bonds on issue. Coca Cola, Petrobas and Disney all have them, although Disney’s bond is callable after 30 years in 2023.

The latest century bond issuer is the University of Oxford. Oxford recently received a AAA credit rating from S&P in preparation for its inaugural £750 million (AUD$1.35 billion) bond sale. The bonds mature in December 2117 and have a 2.544% coupon. According to Westpac, they were priced at U.K treasury bonds + 85bps (although it is a bit of a mystery as to which maturity Treasury bond the comparison was made).

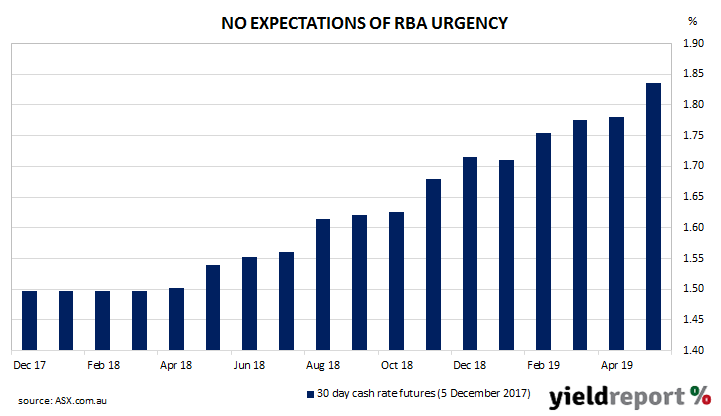

05 December 2017

The December meeting of the RBA Board is not one of the four months of the year traditionally associated with RBA rate changes. November, along with February, May and August are statistically much more likely to be the months in which the RBA changes its official rate. The thinking is these are the months following quarterly releases of CPI figures and the RBA uses the data to confirm its forecasts of the likely trajectory of inflation.

No economists or commentators expected a rate change to come out of this meeting. Prices of contracts in the cash futures market implied a near-zero chance of a change at this meeting and for several months in 2018. Prices were largely unchanged after the decision was announced.

As expected the RBA held the official rate steady at 1.50%. The press release which accompanied the decision has some amended sections but the essence of the message is largely unchanged from that of the November meeting. On the plus side, the global conditions “have improved over 2017” and the RBA’s forecasts for Australian GDP growth “to average around 3% over the next few years”. The labour market has been strong over 2017 and “various forward indicators continue to point to solid growth”. Finally, underlying inflation “remains low”. On the minus side, household incomes are growing slowly and debt levels are high.

Westpac chief economist Bill Evans said “the most interesting change” in Governor Philip Lowe’s statement was the reference to the Australian dollar. The exchange rate of the Aussie no longer appears to be an issue for the RBA. He also noted the RBA’s recent tendency to note reports of employers’ difficulties in finding workers “with the necessary skills.” He thinks this has not yet become a pressing issue for the RBA because Lowe stated “wage growth remains low and is likely to continue for a while yet”.