21 November 2017

The RBA held the official cash rate steady at its board meeting in November and so the minutes of the meeting were only expected to provide the odd hint as to the RBA’s thinking of the path Australian monetary policy is likely to take.

As AMP Capital’s Shane Oliver put it, there was “nothing new” in these minutes. However, not everyone agreed. JP Morgan Research said the minutes “reveal growing uncertainty around the outlook for wages”. The RBA stated wage inflation “had been somewhat weaker than expected” but as Philip Lowe said later in the day, “In Australia, we are still some way short of our estimates of full employment of around 5%, so it is not surprising that wage growth is below average.”

Financial markets were largely unmoved. 2 year bond yields were steady at 1.94% while 10 year yields added 1bp to 2.57%. The Aussie dollar dropped after release of minutes but then moved up around 0.25 U.S. cents to around U.S. 75.80 cents over the rest of the day.

ANZ Head of Australian Economics David Plank thought the main takeaway of the minutes was the discussion regarding monetary policies of other central banks. “While we agree there are no ‘mechanical’ implications, the path of monetary policy elsewhere is still important in thinking about the likely direction of RBA policy. In particular, the impact on the AUD [dollar] from a domestic monetary policy shift is likely to be less than otherwise [expected] if the shift is in the same direction as those in other countries. Our expectation of two RBA rate hikes in 2018 will be harder to sustain if the Fed does not tighten further from this point.”

21 November 2017

Michael Saba, Head of Income Products at Evans and Partners, made an interesting observation recently. He and his team looked at the relationship between hybrid margins and implied volatility and they found a rather good explanation for changes in trading margins since mid-2013.

Without going into the finer details of options pricing, implied volatility can be thought of as an indicator of the expensiveness of an options contract, all other things being equal. If participants in an options market think future prices of the underlying asset are likely to be more volatile for a future period (than average), then prices of options on that underlying asset tend to rise, whether they are “call” options or “put” options. In the absence of mispricing, higher option prices can be said to imply expectations of higher price volatility.

16 November 2017

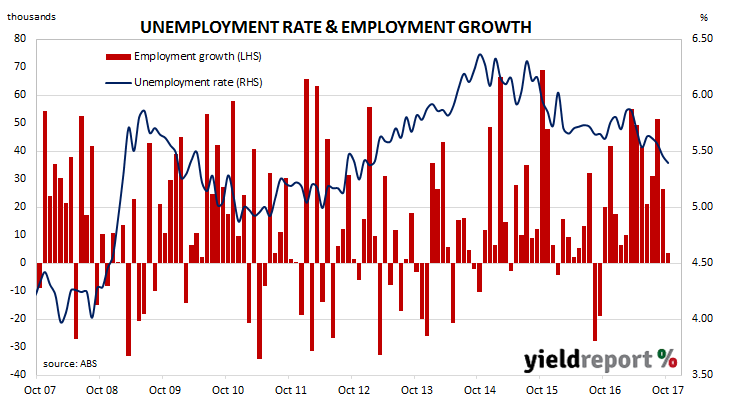

The Australian economy has recorded another month of employment gains, with new full-time positions outweighing fewer part-time positions. The ABS released employment estimates for October and the total number of people employed in Australia in either full-time or part-time work increased by 3,700. This figure did not meet market expectation of 18,000 new positions, although September’s increase was revised up from 19,800 to 26,600.

Bond yields had been creeping up in the lead up to the release and then they rose another basis point or two over the next two hours. However, by the end of the day, 3 year bond yields inched up 1bp to 1.96% while 10 year bond yields slipped 1bp to 2.60%. In the currency market the Aussie initially shot up against the USD but then it slipped back to finish largely unchanged at around 75.85 U.S. cents.

15 November 2017

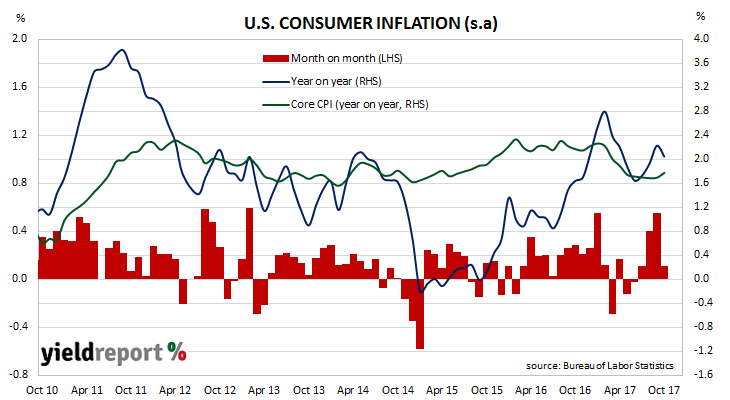

The U.S. consumer inflation rate fell back in October as higher housing costs were offset by lower fuel prices. Consumer price index (CPI) figures released by the Bureau of Labor Statistics indicated consumer prices rose by 0.1% in October, in line with market expectations. On a 12-month basis the consumer inflation rate fell back from September’s 2.2% to 2.0%.

Medical care, used vehicles, tobacco, education, vehicle insurance and personal care were among the categories where average prices increased. Average prices of the new vehicles, recreational activities and apparel categories all declined.

Core prices, a measure of prices which strips out food and energy price changes, rose by 0.2%, a rise from September’s increase of 0.1%. Both the monthly and 12 month core figures were in line with expectations. Annualised core inflation rose to 1.8% after spending five months unchanged at 1.8%. ANZ Rate Strategist Martin Whetton said the figures cleared the way for the U.S Fed to raise the Federal funds rate next month. “With the data broadly in line with expectations, and the details showing tentative signs that some of the factors that had weighed on inflation earlier in the year are abating, medical services especially, it seems fair to believe that a hike now looks locked and loaded.”

ANZ Rate Strategist Martin Whetton said the figures cleared the way for the U.S Fed to raise the Federal funds rate next month. “With the data broadly in line with expectations, and the details showing tentative signs that some of the factors that had weighed on inflation earlier in the year are abating, medical services especially, it seems fair to believe that a hike now looks locked and loaded.”

15 November 2017

The high yield bond market in Australia is set to become a little larger this week. QMS Media (ASX code: QMS) has announced it has finalised the issue of $70 million worth of senior unsecured notes. The outdoor advertiser adds another issuer to a growing list of local companies without credit ratings which have raised funds by issuing high yield bonds in Australia.

The company sought to raise a minimum of $50 million but investor demand led to the issue being upsized to $70 million. The notes have a 7.00% coupon and they will mature on 17 October 2022.

The notes may be called earlier and there are two optional redemption dates; one on 21 November 2020 and the second on 21 November 2021.

On the first optional redemption date or the next interest payment date, QMS may redeem the notes at 102% of face value. On the second optional redemption date or the next interest payment date QMS may redeem the notes at 101% of face value.

It is not uncommon for modest penalties to apply to companies which redeem bonds early. Firstly, investors would need to re-invest the redemption proceeds at a time not of their choosing. Secondly, they would miss out on interest payments for the last year or two of the life of the bonds or notes.

15 November 2017

Each quarter the Australian Bureau of Statistics (ABS) surveys around 3000 enterprises regarding a sample of jobs in each workplace to measure changes in the price of labour across around 18000 jobs.

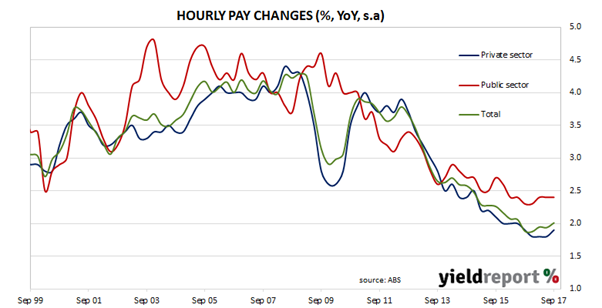

According to the latest wage price index (WPI) figures published by the ABS, hourly wages grew by 0.5% in the September quarter, the same rate as in the June quarter although it was less than the market’s expectations of a 0.7% increase. The year-on-year growth rate increased from 1.9% to 2.0% (after revisions) but this rate is still barely just above the lowest growth rate since the beginning of the series in 1999.

Public sector hourly wages growth grew at a slightly higher rate than its private sector counterpart over the quarter although both figures came in at +0.5% after rounding. On an annual basis, public sector hourly pay maintained its 2.4% growth rate while the comparable figures for the private sector increased from 1.8% to 1.9%.

When June’s figures were published, ANZ senior economist Felicity Emmett said she expected September quarter figures to “pop higher” as a result of the increase in the minimum wage rate in June. After the latest data release she said the figures implied overall wages growth had slowed if the minimum wage decision was factored in. “The lack of any apparent impact from the larger-than-usual rise in the minimum wage suggests that underlying wage growth actually slowed in the quarter.” In her opinion further falls in the unemployment rate will be required “before we see a more sustained rise in wage growth.”

14 November 2017

In recent months, commentators and economists have pointed to a divergence between consumer sentiment and business confidence in Australia during 2017. Surveys indicated business confidence has been trending up since 2013, while measures of consumer sentiment have been bouncing around a level just on the pessimistic side of neutral. The latest surveys has not altered the divergent paths taken by the business and household sectors.

According to the latest Westpac-Melbourne Institute Consumer Sentiment Index, households were more optimistic than a month ago as the Index reading dropped back from 101.4 in October to 99.7 in October. Any reading below 100 indicates the number of consumers who are pessimistic is greater than the number of consumers who are optimistic. The long-term average reading is just over 101.

The survey was held in the first week of November. Westpac chief economist Bill Evans thinks attention on rising interest rates may be behind the fall, a theory which makes sense when Australian households are known to be carrying record amounts of debt. “Constant media coverage around the prospect of rising interest rates may be unnerving households. The confidence of respondents who hold a mortgage fell by 4.5% compared to a more modest fall of 1.4% for those owners who are mortgage free and a 0.5% increase for tenants.

Deutsche Bank chief economist Adam Boyton has what appears to be a simple fix for household confidence; higher wages. “Plotting labour costs from the NAB (business) survey against consumer sentiment and allowing for the apparent lag, suggests in fact that there is a high degree of alignment between what businesses are telling us about wages and what consumers are saying about their own circumstances.”

Yields on 3 year and 10 year bonds both finished the day 5bps higher at 2.01% and 2.68% respectively while the Aussie was a touch higher at 76.32 U.S. cents.

14 November 2017

Australian business conditions are as good as they get according to the latest NAB survey. According to NAB’s latest monthly business survey of 400 firms in late October, its Business Conditions Index jumped from 14 to 21, a reading which has not been exceeded in the last twenty years.

Typically, NAB’s conditions index is led by its Business Confidence Index by around one month, although in recent months the two surveys have diverged. The confidence index dropped in August before making a minor recovery in September. It then stabilised in October at a reading of 8, which is 2 points above its long-term average.

The capacity utilisation rate, generally accepted as an indicator of future investment expenditure, gave back most of September’s increase as it fell from 81.9% to 81.7%. Sector capacity utilisation was at or above long-term averages for all sectors of the economy except for the mining, transport/utilities and wholesale sectors.

10 November 2017

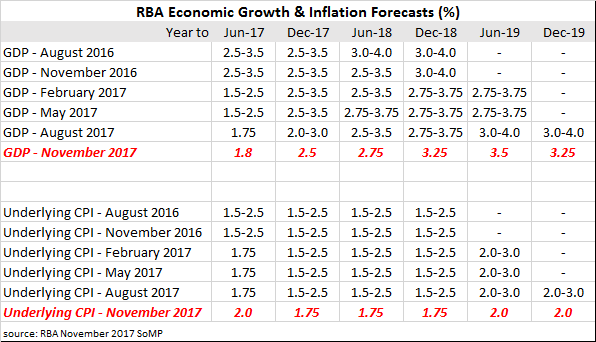

The Statement on Monetary Policy (SoMP) is released each quarter and it is closely watched for the updates to the RBA’s own forecasts. In this quarter’s Statement, the RBA has lowered its forecasts for GDP growth and inflation. It forecasts GDP growth in 2018 to be 2.75%, down from 3.0%, while forecasts for headline and core inflation rates for 2017-18 have been cut by 0.25% to 2.00% and 1.75% respectively.

The RBA is aware its current policy is accommodative and quite some way from a neutral stance. While it appears to be optimistic about unemployment, there is nothing in this SoMP to indicate any likely change in its policy stance. “The stimulatory setting of monetary policy in Australia has supported the economy and helped generate a decline in unemployment. Over the period ahead, further progress on reducing spare capacity in the economy is expected, which in turn would support the forecast gradual increase in inflation.” In other words, do not expect the RBA to raise the official rate until further slack has been used up.

The RBA’s forecast for employment did not change from its previous statement in August. The unemployment rate is forecast to remain at 5.5% through 2018 and 2019. This is a little strange given the RBA’s reference to leading indicators of employment in its recent board meeting press release.

09 November 2017

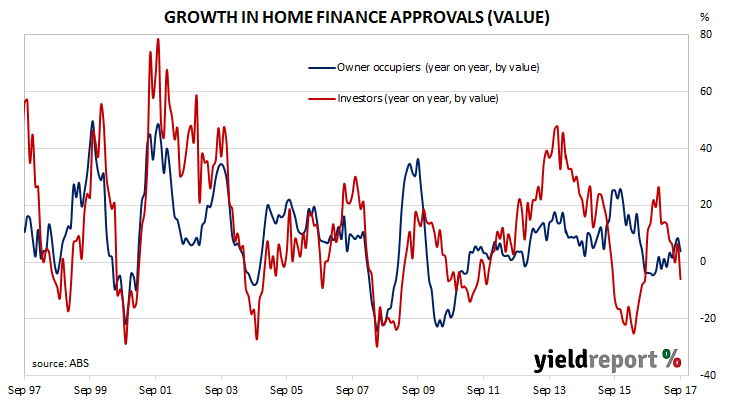

The Australian Bureau of Statistics (ABS) collects data on housing finance commitments made by significant lenders and their figures include secured (mortgage) finance commitments for the construction or purchase of owner-occupied dwellings and investment properties. It has some overlap with the RBA’s monthly private sector credit statistics which also includes investor lending and owner-occupier lending.

The ABS has released housing finance figures for September which indicate the number of owner-occupier approvals excluding refinancing fell by 2.3% over the month. Excluding refinancing, the total number of approvals fell by 2.9% for the month but grew by 11.8% for the year.

In dollar terms, owner-occupier loan approvals (excluding refinancing) fell by 2.1%, down from August’s revised figure of -0.6%. In annual terms the value of approvals rose by 13.3%, also down from August’s revised annual rate of 17.1%.

Investor loan approvals also fell. On a monthly basis, approvals in this segment fell by 6.2% after a 4.8% rise in August. On an annual basis September finance approvals were down by 6.0%, a substantial turnaround from August’s +6.4%.

ANZ senior economist Daniel Gradwell said he thought the numbers indicated the housing market had further cooling to come. “Housing finance commitments in September recorded the largest decline in two years, and falling auction results suggest the market has further to cool through the remainder of 2017 and into 2018.”