07 November 2017

The November meeting of the RBA Board is one of the four months of the year traditionally associated with RBA rate changes. November, along with February, May and August are statistically much more likely to be the months in which the RBA changes its official rate. The thinking is these are the months following quarterly releases of CPI figures and the RBA uses the data to confirm its forecasts of the likely trajectory of inflation.

Prior to this particular November meeting few, if any, economists or commentators expected a rate change of any sort. Prices of contracts in the cash futures market implied a near-zero chance of a change, not only for November but for other contracts well into 2018.

As expected the RBA held the official rate steady at 1.50%. The press release which accompanied the decision is largely unchanged from that of the October meeting. The global economy “continues to improve” and the RBA’s forecasts for Australian GDP “are largely unchanged”. GDP is expected to average “around 3% over the next few years.” The labour market continues to strengthen. “The unemployment rate is expected to decline gradually” and “various forward indicators continue to point to solid growth”. Finally, underlying inflation “is likely to remain low for some time”.

The housing market remains at the heart of the RBA’s concerns. “Housing debt has been outpacing the slow growth in household income”. However, the RBA expects pressure to ease through a combination of demand and supply changes, all other things being equal. Demand should ease after credit standards “have been tightened” while a “considerable additional supply of apartments is scheduled to come on stream”.

Reactions from economists was quite diverse. Some think the RBA is too optimistic and overstating Australia’s growth rate in 2018 and beyond while others went the other way. Here’s what a few of them had to say about the decision and the RBA statement:

Felicity Emmett ANZ

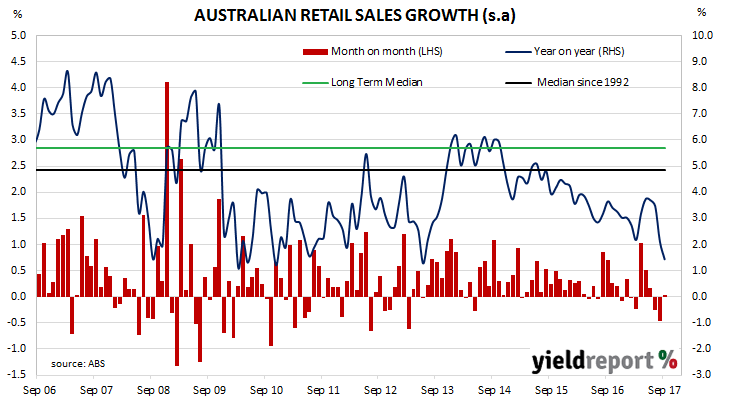

Given recent disappointments on retail sales and inflation, today’s statement was keenly anticipated to gauge the RBA’s assessment on the outlook. The RBA held the line though and remained relatively upbeat about the outlook. While concerns around the consumer remain, the Bank remains positive about the investment outlook, both private and public, and seems to be more optimistic about the unemployment outlook. The statement noted that the forecasts for growth to be published in the Statement on Monetary Policy on Friday are largely unchanged, but we see a risk that the unemployment rate forecast for December 2019 is revised down as far as 5%.

Michael Workman CBA

Today’s RBA statement was not markedly different to the previous one. An RBA rate rise is definitely in the next chapter. The current chapter has unusually low inflation and wages trends against a background of slowly improving growth in local and trading partner economies. From a monetary policy perspective, the unchanged cash rate of the last 16 months looks to have another year to run.

Damien Boey Credit Suisse

We think that the RBA has too positive a view of the economy and its drivers…The risk is that growth slows as the RBA leaves rates unchanged over the next few months. We expect that the bond market will react to this with more curve flattening, as rate hikes are priced out, and easing risks are increasingly factored in. Our real yield curve model continues to point to at least another 35bps of flattening in the next few months.

Tim Baker Deutsche Bank

All up, the RBA has made few material changes, with the statement retaining a neutral bias. We remain less confident about a wages pick-up than the RBA, and look forward to Friday’s SMP for further detail on how the RBA sees the consumer outlook. We continue to view the RBA being on hold until 2019.

George Tharenou UBS

Overall, the RBA held rates and stayed neutral as we expected. They still see “little change” to their view of improving global growth supporting better GDP & gradually higher CPI – but [it] will likely still downgrade both in Friday’s SOMP. Looking ahead, we still expect the RBA to keep the cash rate on hold until 2H-18, while they wait to see the extent to which better global growth leads to faster domestic activity and CPI, as well as the impact of macro-prudential policy tightening on housing and consumption.

Bill Evans Westpac

There remains a difference of opinion between us and the Bank on the growth and inflation outlook. The Bank is expecting above-trend growth next year despite uncertainty around the household sector and with the associated closing of the output gap along and a gradual move towards full employment, they will continue to forecast inflation moving back to 2.5% in 2019.

We accept that if that dynamic does come to pass, then the Bank will see opportunity to raise rates next year. However, our growth outlook is much flatter, particularly given our view on household incomes and wages, we do not expect that the need will arise to raise rates in 2018.