13 October 2017

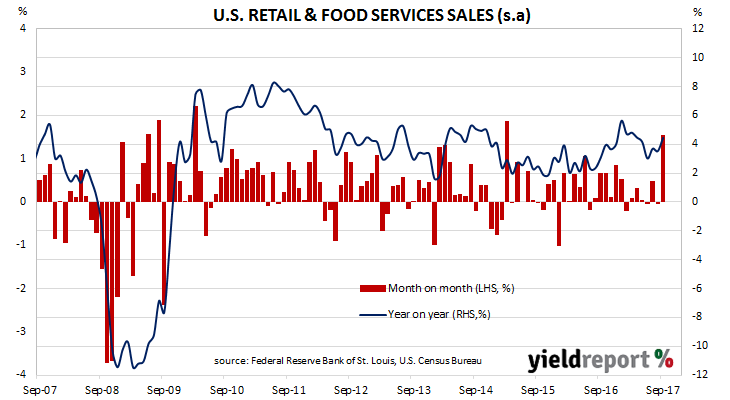

U.S. household spending has rebounded as consumers made up for reduced spending in August when Hurricanes Harvey and Irma swept through the south-east of the United States. According to the latest advance U.S. retail sales numbers released by the U.S. Census Bureau, retail sales increased by 1.6% during September, just shy of the 1.7% expected increase but well up on July’s revised figure of -0.1%. On a yearly basis, the increase was 4.4%, up from August’s comparable figure of 3.5% (after revisions).

In dollar terms the increase was driven predominantly by “non-store retailers”. Non-store retailers may include direct selling as well as online sales and other forms of electronic commerce. Petroleum sales, vehicle and parts sales, building materials and garden supplies were also major contributors.

12 October 2017

The Australian Bureau of Statistics (ABS) collects data on housing finance commitments made by significant lenders and their figures include secured (mortgage) finance commitments for the construction or purchase of owner-occupied dwellings and investment properties. It has some overlap with the RBA’s monthly private sector credit statistics which also includes investor lending and owner-occupier lending.

The ABS has released housing finance figures for August and the figures indicate the number of owner-occupier approvals rose by 1.0% over the month and by 7.5% when compared to August 2016. Excluding refinancing, the number of approvals was the same as in July but 17.1% higher than a year ago. These figures were largely in line with market expectations.

In dollar terms, owner-occupier loan approvals increased by 0.9% in August, an increase on July’s revised figure of +0.9% and 8.9% higher than in August 2016. Investor loans grew by 4.3%, a sharp turnaround from July’s 3.7% contraction and 6.5% higher than 12 months ago.

12 October 2017

The minutes of the FOMC’s September meeting added little to the market’s view of the timetable for U.S. rate increases. Financial markets reflected this and bond yields moved ever so slightly lower after the minutes were released.

However, for those in doubt of another rise in the federal funds rate this year, it is worth considering the following statement from the minutes. “Consistent with the expectation that a gradual rise in the federal funds rate would be appropriate, many participants thought that another increase in the target range later this year was likely to be warranted if the medium-term outlook remained broadly unchanged.”

According to Westpac, this sort of statement “solidified December Fed hike expectations” but “at the same time revealed ongoing concerns about persistent low inflation.” A rate increase is obviously not a certainty. Not all members think a rate rise is necessary. Note the following statement. “A few participants thought that additional increases in the federal funds rate should be deferred until incoming information confirmed that the low readings on inflation this year were not likely to persist and that inflation was clearly on a path toward the Committee’s symmetric 2% objective over the medium term.”

According to CME Group, the probability of a rate rise in December on the day prior to the release of the minutes was 87% and this remained unchanged after the release of the minutes. In any case, 87% is a clear sign the market currently expects a rate rise at the FOMC’s December meeting. The release of the latest U.S. CPI figures at the end of this week will be the next piece of data to reinforce or change the market’s view.

The full text of the minutes can be found here.

12 October 2017

Kangaroo bonds are Australian dollar-denominated bonds issued by non-resident entities in Australia. Most issuers are supra-nationals and sovereign agency entities but there are also a few private sector financial institutions and corporates which issue bonds in Australia even if they have no business operations here.

A small number of issuers are from New Zealand. Auckland Airport issued $110 million worth of kangaroo bonds this very week. Auckland Council has become a regular issuer and it last issued $50 million September 2027s in July, while Kiwibank has been much more sporadic and it has issued kangaroo bonds only twice since 2009. Spark Finance has just become the latest New Zealand corporate to join them.

Spark is a subsidiary of Spark New Zealand (formerly Telecom New Zealand). Group revenue was in the order of NZD$3.6 billion (AUD$3.3 billion) in 2017 while total assets amounted to around USD$3.3 billion (AUD$3 billion). Spark senior debt is rated “A-“ by S&P.

Spark will issue bonds with a coupon rate of 4.00% and an October 2027 maturity date. Initial guidance for the pricing of its inaugural kangaroo bond transaction was 130bps over 3m BBSW.

Demand for the $150 million worth of bonds on offer drove the final price 10bps tighter according to the Commonwealth Bank.

Spark has issued the majority of its existing bonds in its home New Zealand currency, including two series of bonds which are listed on the NZX. It also has £125 million May 2018 bonds and £150 million April 2020 bonds which were issued into the U.K bond market in 2011.

11 October 2017

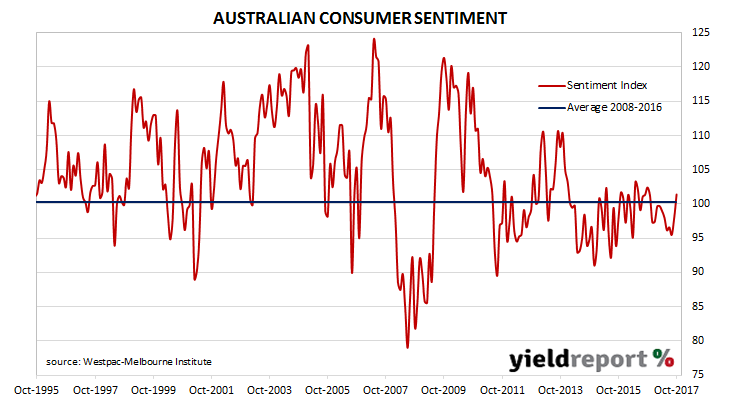

In recent months, commentators and economists have pointed to a divergence between consumer sentiment and business confidence in Australia during 2017. Surveys indicated business confidence has been trending up since 2013, while measures of consumer sentiment have been bouncing around a level just on the pessimistic side of neutral.

According to the latest Westpac-Melbourne Institute Consumer Sentiment Index, households were more optimistic than a month ago as the Index reading increased from 97.9 in September to 101.4 in October. Any reading below 100 indicates the number of consumers who are pessimistic is greater than the number of consumers who are optimistic. The long-term average reading is just over 101.

10 October 2017

Reports regarding a new hybrid from Bendigo and Adelaide Bank have emerged this week. The talk is Bendigo will aim to raise $400 million via a new series of hybrids to add to its three existing series.

One of these, the Bendigo CPS (ASX code: BENPD) has a call date in December and redeeming a hybrid security on this date has become standard practice. Redeeming callable securities on first call dates has been standard practice in the corporate bond market for a long time but callable hybrids only started to emerge in the last decade and it is only this year they have started to reach their first call dates.

Speculation has also turned to whether Bendigo will act in the same manner as ANZ did recently. ANZ allowed its ANZ CPS 3 (ASX code: ANZPC) holders the option of switching into its new series 4 capital notes (ASX code: ANZPH) or keeping their existing ANZPC holding. While holders of several hundred million dollars of ANZPC did switch, a sizeable proportion of holders choose to remain in the security. Now both securities trade on the ASX market.

The trading margin of Bendigo’s CPS has dropped in recent weeks to the point purchasers appear to be paying a premium for the hypothetical eligibility to switch into the new securities. Demand for the CPS suggests investors have been willing to bet on what Bendigo Bank may announce.

10 October 2017

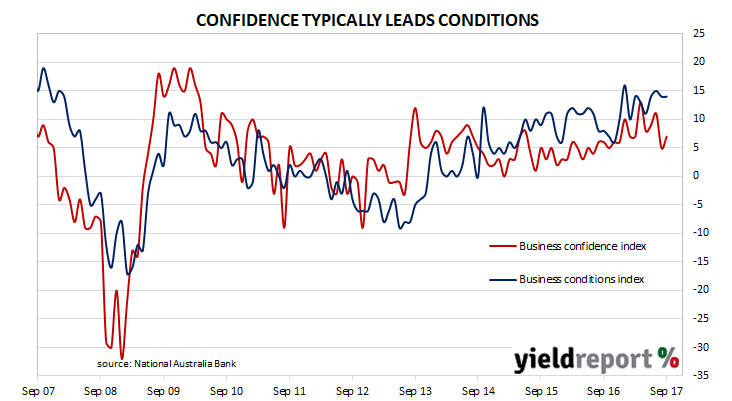

Australian business conditions remain close to the boom times of the mid-2000s and confidence has recovered. According to NAB’s latest monthly business survey of 400 firms in late September, its Business Conditions Index remained unchanged at 14 (after revisions), while its Business Confidence Index increased by 2 points to 7.

Business confidence had taken a minor battering in August which was the result of a change in customer demand, margin pressure and government policy. The 2 point increase in September took the index back to just above its long-term average.

ANZ senior economist Daniel Gradwell thought the report provided reason to be positive about the Australian economy’s outlook. “The details of the September report are encouraging and suggest that employment growth should remain solid. We see further evidence that the post-mining boom adjustment is nearly complete, and construction in the non-mining states will be an important part of Australia’s growth.”

Not every economist shared the ANZ’ economist’s view and Westpac senior economist Andrew Hanlon was not convinced. “The NAB business survey for September was positive overall, but conditions are uneven, which is concerning for the outlook.”

06 October 2017

The U.S unemployment rate hit a new low since February 2001 after Hurricane Harvey and its effects distorted employment figures. According to the U.S. Bureau of Labor Statistics, the U.S. economy lost 33,000 jobs in the non-farm sector in September against expectations of an 88,000 gain. However, after revisions to previous months’ figures, the unemployment rate dropped from 4.4% to 4.2% as over 331,000 people either found work in the farm sector or retired.

The total number of employed persons in the non-farm sector at the end of September was 146.7 million and 154.3 million overall. Over the past twelve months, 2.4 million jobs have been created in the U.S. with nearly 1.8 million of those in the non-farm sector. Another figure which is indicative of the strength of the U.S. economy is a higher employment-to-population ratio. In September the ratio jumped from 60.1% to 60.4%, while the participation rate increased from 62.9% to 63.10%.

06 October 2017

Elanor Investors Group (ASX code: ENN), has announced it has finalised the issue of $40 million worth of unsecured notes. Elanor’s note issue makes the Australian property investor and funds management company the latest addition to a growing list of local companies without credit ratings which have raised funds by issuing high yield bonds in Australia.

The company intends to use a proportion of the proceeds to invest in two new projects. One is the seeding of its $80.6 million Elanor Metro and Prime Regional Hotel Fund which will comprise a portfolio of three hotels. The other is its $60.35 million Bluewater Square Syndicate fund.

Although bond yields have risen by nearly 1% over the last year, interest rates are still a lot closer to historically-low levels. As such, the search for a higher rate of interest has taken some investors into higher-risk assets such as those issued by unrated issuers. The notes have a 7.10% coupon and they will mature on 17 October 2022.

The 7.10% coupon is under the 7.50% – 9.00% range established over the last three years by similar unrated issuers and it is significantly lower than StockCo’s 8.75% coupon set on its callable notes issued in 2016.

As with most, if not all, of these unrated bond and note issues, the offer was open only to eligible sophisticated investors in accordance with the Corporations Act.

05 October 2017

Australians seem to have decided to go on a nationwide diet in August. Retail sales of food fell by 0.6% during the month and purchases of food and beverages prepared outside the home also fell as spending in cafes and restaurants fell by 1.3%. These two segments plus household goods account for around nearly three quarters of all retail sales.

Total retail sales fell by 0.6% (seasonally adjusted) in August, after falling by 0.2% in July. On a year-on-year basis, sales grew by 2.1%, down from the 3.5% annual rate recorded in July. August is the fourth month in a row where the growth rate has fallen.

The figures took local markets by surprise. Firstly, economists were expecting sales to rise by +0.3%. Secondly, July’s figures were also revised down from 0% to -0.2%. The local bond market and currency markets reacted by sending yields and the AUD lower. The yield on 3 year government bonds dropped 4bps to 2.12% while 10 year yields lost 3bps to 2.81%. The local currency was sold off against the USD and it finished about 0.7 U.S. cents lower at around 77.95 U.S. cents.

This is not the first time this year the retail sales annual growth figure has fallen close to 2%. After revisions, March’s 12 month growth rate was 2.2% but then sales in April and May were especially strong and the growth rate jumped to 3.7%. However, this is still below the average rate of sales growth which is close to 5% since 1992.