20 September 2017

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of economic activity relative to trend in Australia. The index combines certain economic variables which are thought to lead changes in economic growth into a single measure which is claimed to be a reliable cyclical indicator for the Australian economy and a “critical” indicator of swings in Australia’s overall economic activity.

For the last three months, the Leading Index has returned values which imply below-trend growth. August’s reading returned -0.19% which is a modest decline from July’s revised reading of -0.04% (revised up from -0.10%).

According to Westpac chief economist Bill Evans, a deterioration in conditions since March has been driven in the main by two factors. Commodity prices have fallen, which means Australian exporters are likely to earn less income as shipments and payments are made on contracts in the period.

The other driving force was a change in the gradient of the yield curve, which is represented in this case by the spread between BBSW and the 10 year bond rate. The gradient of the yield curve is said to be a simple but reliable predictor of future economic activity and recently this spread has been contracting and getting closer to zero.

20 September 2017

At its latest September meeting, the Federal Open Markets Committee (FOMC) gave markets pretty much what was expected; no rate change and the beginning of quantitative tightening (QT).

While both were expected, there was also a sting in the tail as well. As ANZ put it, “The Fed did not surprise [us], but the underlying signal was more hawkish than markets expected, shooting the USD higher…Yields pushed higher as the Fed gave the signal for a December rate hike…”

The odds of another U.S. rate rise this year have shortened. According to Federal Funds futures contracts on the day prior to the FOMC statement, traders had placed a 57% chance on a December rate increase. By the close of business on the next day, the probability had jumped to 71%.

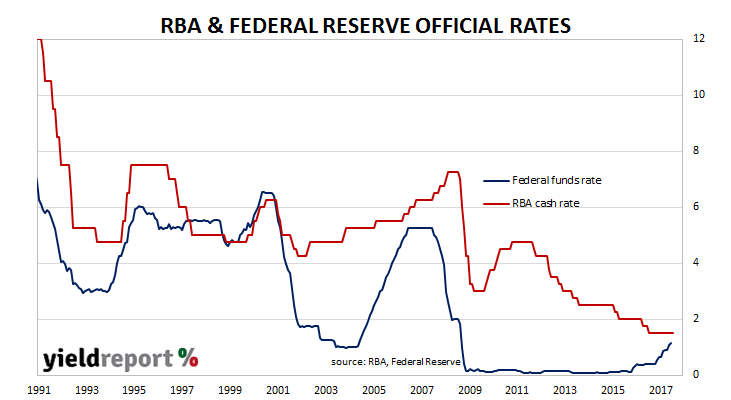

If the U.S continues at this pace, the official U.S interest rate will be above the Australian cash rate. Undoubtedly, Australian exporters would be happy and so would the RBA; a stronger currency has been offered as an impediment to Australian economic growth in more than a few minutes of RBA Board meetings.

20 September 2017

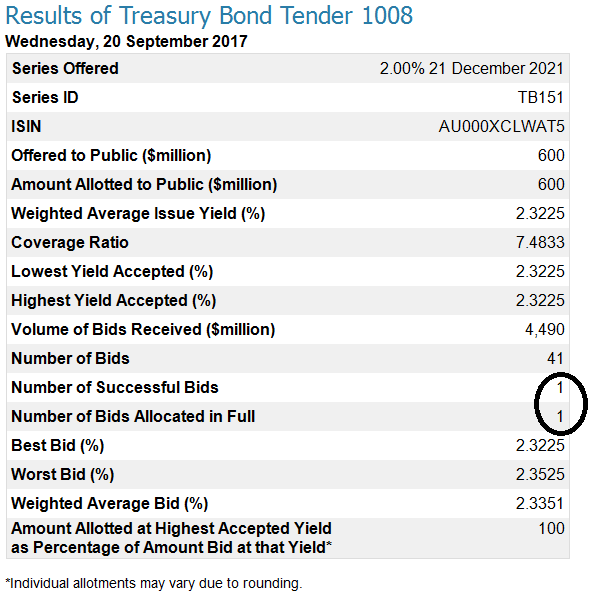

YieldReport has noted two AOFM bond tenders recently in which one bidder has bought the entire offering. The most recent occasion was three weeks ago at the very start of September and at that tender $500 million December 2021s were bought by one bidder.

Today the AOFM offered $600 million December 2021s for purchase by tender and again, one bidder bought the lot. What caught people’s attention was the fact the this tender and the previous one were for the same bonds, 2.00% December 2021s.

It may be just a coincidence. Then again, perhaps one of the investment funds out there thinks the December 2021s are what it needs. $600 million is not all that much to investors the size of Norway’s sovereign wealth fund or the California Public Employees’ Retirement System (CalPERS) fund. It may even be the RBA, which has $3.5 billion to play with after it sold the AOFM $3.5 billion January 2018s earlier today in what the AOFM described as “cash management activities”.

20 September 2017

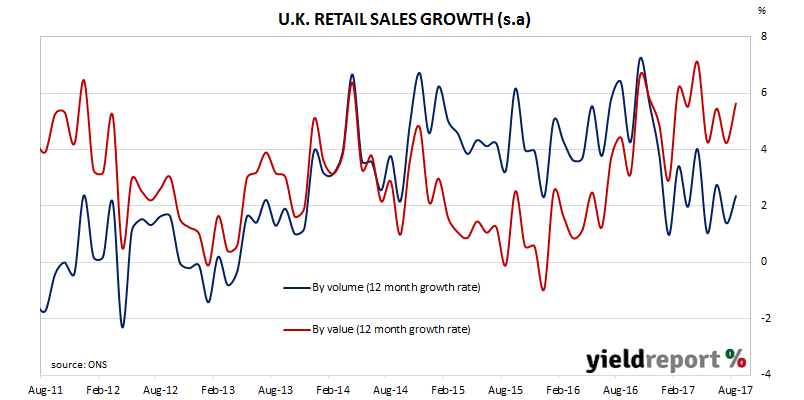

The rate rise in the U.K is almost a certainty after strong retail sales in August. Markets had increased the probability of a rate increase after recent comments from the Bank of England and the latest retail figures appear to remove any doubt.

Retail sales increased by 1.0% in both terms of value and volume during August. Compared to a year ago, sales were up by 5.6% in nominal terms and 2.4% in real terms. Excluding fuel, retail sales were up 5.8% for the year, or 2.8% in real terms which was about double the expected figure of 1.4%. July’s figures were also revised higher.

Retail figures are notoriously volatile but economists viewed the figures as further confirmation of solid economic growth in the U.K. ANZ senior economist David Plank said, “That [the retail figures] adds some credibility to the BoE’s argument that some modest adjustment…in policy is appropriate. The BoE cut 25bps last year because of concerns about a possible sharp growth slow down. That hasn’t really occurred.”

19 September 2017

Deutsche Bahn is the German state railway company formed from the merger of the East German and West German railways in the 1990s. Annual revenue is around €40 billion euro so it is no minnow. Gross financial debt was around €22.5 billion at the end of 2016.

After a two year absence from the kangaroo market, Deutsche Bahn has issued $600 million worth of bonds. It was divided between two fixed rate tranches; a $425 million tranche of September 2024s and a $175 million tranche of September 2027s.

Initial guidance for the deal was 85bps and 95bps over each tranche’s respective swap rates. It turned out to be on the money and final pricing was set in line with the guidance.

The bonds it has on issue are mostly denominated in euro but it also has bonds denominated in Swiss francs, sterling, Singapore dollars, yen, Swedish krona, Hong Kong dollars, Norwegian krone but surprisingly very little in U.S. dollars.

This latest transaction has been described as Deutsche’s inaugural transaction in the kangaroo market but it appears Deutsche has been here before. In late 2015, its subsidiary, Deutsche Bahn Finance, issued $180 million October 2025 bonds.

Deutsche Bahn is rated AA- by Standard & Poor’s and Aa1 by Moody’s.

15 September 2017

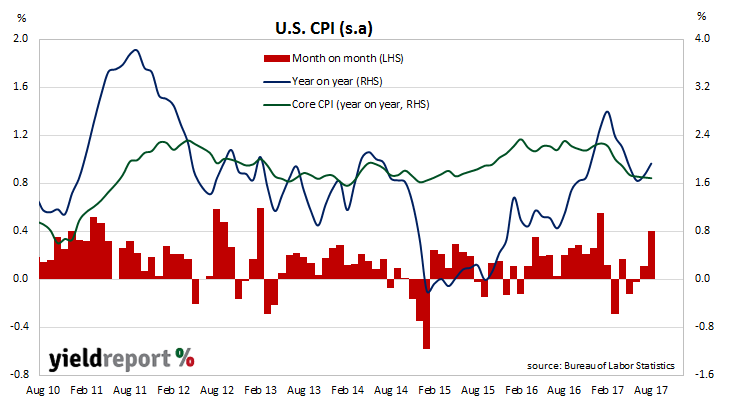

Higher fuel prices, rents and other lodging costs have driven U.S. consumer inflation higher than economists had expected. Consumer price index (CPI) figures released by the Bureau of Labor Statistics indicated prices rose by 0.4% in August, higher than the market expectations of a 0.3% increase. On a 12-month basis the consumer inflation rate increased from July’s 1.7% to 1.9%.

Core prices, a measure of prices which strips out food and energy price changes, rose by 0.2% after three months of 0.1% increases. Annualised core inflation remained steady at 1.9% after rounding. Both the monthly and 12 month figures were in line with expectations.

ANZ senior economist David Plank thought the figures provided evidence of a decline in deflationary pressures. “While the headline was affected by a hurricane-related boost to gasoline (+6.3%), there were signs that some of the things that have been dragging are now stabilising or at least slowing the pace of declines…More than one month’s data will be needed to confirm this, of course, but if it continues it would certainly provide some food for thought to bond markets around the prospects of future rate hikes.”

15 September 2017

The U.S. Federal Reserve has been slowly raising the federal funds rate since the first increase in December 2015. The Fed waited one year for the second increase but the pace has since picked up and there have been three increases in 2017.

It is not only the U.S. which has entered the rate rise part of the cycle. Mexico has been raising its official rate through 2017 and the Bank of Canada caught some investors by surprise with a rate increase in the first week of September. While the official rate in Canada is still only 1.00%, the latest rate rise has come only two months after its first rate rise since 2010.

Now the Bank of England is warning of a rate rise. If it were to raise its official rate, it would join an expanding group of countries which are moving away from ultra-low interest rates, a process the Fed refers to as “normalisation”.

The British economy recently recorded an unemployment rate of 4.3% while the consumer inflation rate rose to 2.9% in August. The BoE expects this rate to rise above 3% in October as the economy expands and price pressures build. “Recent developments suggest that remaining spare capacity in the economy is being absorbed a little more rapidly than expected at the time of the August Report, and that inflation remains likely to overshoot the 2% target over the next three years.”

14 September 2017

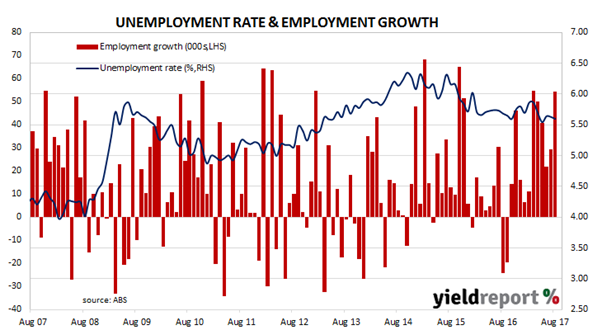

The Australian economy has recorded another month of employment gains and this time it was mostly in the form of full-time jobs. The ABS has released employment estimates which indicated the total number of people employed in Australia in either full-time or part-time work increased by 54,200 during August, which is more than the expected figure of 20,000.

Bond yields rose immediately after the release of the figures. By the end of the day, 3 year bond yields had increased from 2.03% to 2.07% and 10 year bond yields had added 6bps to 2.73%. In the currency market the Aussie added 0.35 U.S cents to 80.1 U.S. cents.

The total number of work hours across the whole economy increased by 0.4% when compared to July, as 40,100 more full-time jobs and 14,100 part-time jobs were created. On a 12 month basis aggregate hours worked grew by 2.6% as 251,200 full-time and 74,500 part-time positions were created.

The unemployment rate has been stuck around 5.6% since October 2016 and there are two factors behind this. Firstly, the participation rate increased. At the end of October 2016 it was 64.4% but by the end of August it was 65.3%, up from July’s 65.1%. The second factor is the total population. The Australian population grew by around 250,000 to 24.65 million, which is just over 20,000 persons per month. While not every additional person is part of the workforce, nearly two-thirds of them are or will be.

13 September 2017

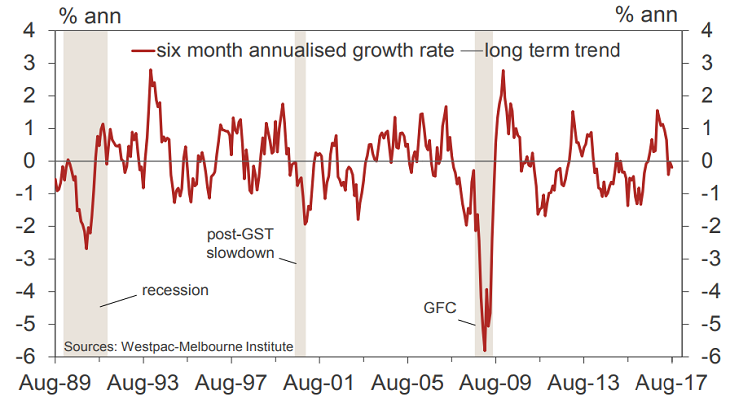

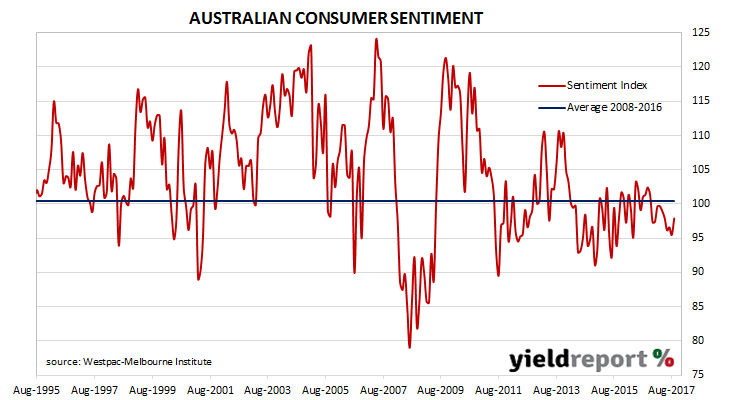

A lot has been made of the recent divergence between consumer sentiment and business confidence in Australia. On the one hand, business sentiment has been buoyant, although after a fall in the latest survey it is back to its long-term average, which is on the optimistic side of neutral. On the other hand, consumer confidence has been slightly pessimistic since December 2016.

According to the latest Westpac-Melbourne Institute Consumer Sentiment Index, households were slightly less pessimistic than a month ago as the Index reading increased from 95.5 in August to 97.9 in September. Any reading below 100 indicates the number of consumers who are pessimistic is greater than the number of consumers who are optimistic. The long-term average reading is just over 101.

The survey was held in the first week of September when the RBA held the cash rate steady and job advertisements increased again. According to Westpac chief economist Bill Evans, the survey indicated finances were the main concern of households. At the same time, households’ expectations of the economy generally were positive, as were impressions of labour market conditions. “The consumer mood remains downbeat with September marking the tenth consecutive month that pessimists have outnumbered optimists. Pressures on family finances, concerns around interest rates, deteriorating housing affordability and rising energy prices have all weighed on confidence in 2017. These factors are more than offsetting the boost from an improved outlook for jobs particularly when a stronger labour market has not been associated with increased wages growth.”

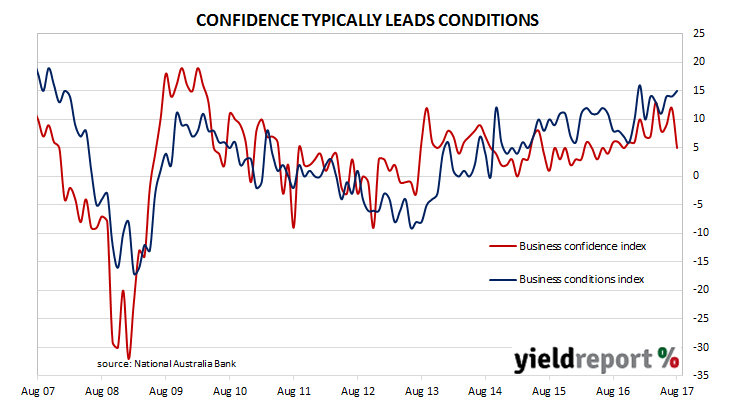

12 September 2017

Australian business conditions remain close to the boom times of the mid-2000s but confidence has slipped. According to NAB’s latest monthly business survey of 400 firms in late August, its Business Conditions Index rose 1 point to 15 from a revised reading of 14 in July, while its Business Confidence Index slumped 7 points to 5.

The fall in confidence was driven by customer demand, margin pressure and government policy. Energy costs also featured while geopolitical risks were well down the list. In spite of the large fall, confidence in all of the industry sectors remained positive.

The capacity utilisation rate, generally accepted as an indicator of future investment expenditure, slipped from 81.9% to 81.6%. Sector capacity utilisation was close to or above long-term averages for all sectors of the economy except for mining and transport and utilities. In a curious turn, spare capacity in July had been lowest in the transport/utilities sector but in August this position reversed significantly.