30 August 2017

The equity strategy team at Morgan Stanley Australia have gone out on a limb with their latest GDP forecast. Their GDP model has forecast just 0.2% growth in Australian GDP for the second quarter, a figure well under the market consensus of 0.5%. “On a year-ended basis, GDP growth is set to slow to the low-1s…in line with our view that Australia remains out-of-sync with growth recoveries in the US (2.1%), Europe (2.2%), Japan (2.1%) and Canada (4.6% in May).”

Their rationale is a low rate of growth in total household income, taking into account population growth, will lead to slower consumption growth. Consumption is such a large GDP component any weakness in it typically leads to a lower rate of GDP growth.

“We see cyclical headwinds shifting – from 1H17 weather disruptions and an ongoing resources capex unwind – towards a consumption squeeze amidst falling real wages, tighter credit conditions and a slowing housing cycle.”’

However, the Morgan Stanley team have left themselves some wriggle room and they are aware new wages data could produce a higher GDP forecast. “Key to any upside surprise would be a broader-based recovery in wages and income, which would allow the consumer to adapt to rising costs and also a higher debt burden…”

Second quarter GDP figures will be released by the ABS on 6 September.

29 August 2017

Hybrid securities have been popular for over twenty years in Australia. Each new issue of a hybrid provides another example of the ease at which companies, especially banks, are able to raise hundreds of millions of dollars by issuing these securities and usually with plenty of unsatisfied investor demand.

The latest ANZ capital raising via its latest Capital notes 5 offering is a good example. Already $552 million of the $1 billion offer has already been allocated to CPS 3 (ASX code: ANZPC) holders who are clients of brokers to the issue. Next in line are other ANZ security holders who were registered by 11 August. There is some chance ANZ will close the offer after this group of potential investors has had its pick.

Given the level of unsatisfied demand, there has been some discussion regarding the purchase of securities as a way of getting “closer to the front of the queue”, so to speak. There is one problem, however; the cut-off date for this priority is the same day as the announcement date. Once the announcement of a hybrid issue has been made, it is usually too late to buy the ordinary shares or some other ASX-listed security of the issuer.

With this in mind, Bell Potter’s Damien Williamson notes Suncorp’s CPS 3 hybrids (ASX code: SUNPC) and Bendigo’s CPS hybrids (ASX code: BENPD) are only a few months away from their December call dates. Typically, issuers offer a priority application to existing security holders and the latest ANZ issue is such an example. Williamson said, “For investors looking to pre-position into a short-dated hybrid with a likely refinancing issue, SUNPC on a 1.83% trading margin at $102.00 is our top pick. The $560 million SUNPC issue has two remaining quarterly coupons before its December call date, where we estimate the total income of $2.20 fully franked ($3.15 grossed up). A replacement issue for BENPD is also likely to be undertaken ahead of its December call date.”

24 August 2017

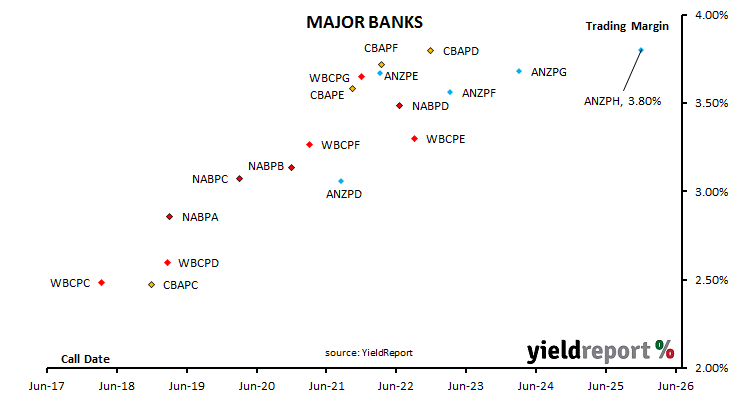

Last week, ANZ announced it would be offering to buy back its ANZ CPS 3 hybrids (ASX code: ANZPC) and issuing around $1 billion worth of ANZ Capital Notes 5 (ASX code: ANZPH). ANZ has now announced the margin above BBSW for distribution payments on the new capital notes.

As has been the usual practice in recent years, the margin has been set at the lower bound of the range. The indicative range was 3.80%-4.00% and hence the margin was set at 3.80%. When this margin is added to the current 3 month bank bill swap rate (BBSW) of 1.705%, investors can expect around 5.50% (annualised) for the first quarter and thereafter if BBSW rates do not alter materially. BBSW is typically at a fairly small margin to the RBA’s official cash rate which is currently 1.50%.

$552 million of the $1 billion offer has already been allocated to CPS 3 (ASX code: ANZPC) holders who are clients of syndicate brokers. Eligible CPS holders and other eligible ANZ security holders will have the next bite at the new capital notes. ANZ stated the final size of the offer will be determined after the ANZ Security-holder offer closes. If allocations reach $1 billion at this point, ANZ will close the offer and not proceed with the broker firm offer.

The chart below shows the trading margins of existing notes and bonds which are already listed on the ASX. In very simplified terms, a security’s trading margin is the sum of its annualised distributions as percentage of its price less BBSW. (In practice, unrealised annual capital gains/losses and accrued distributions are also taken into account.)

As at the close of business 23 August 2017.

23 August 2017

Every week the AOFM issues Treasury bonds and notes via a tender system to raise funds for the Commonwealth Government. In recent years, typically there would be two bond tenders and one note tender each week, with some variations along the way. Most of the time it is to issue an existing line of bonds or notes but as bonds have a finite life and come to an end, every so often a new line of bonds will be issued.

Quite often when a new line is issued, it is not via a tender but via a syndicated process. This is where a syndicate of banks will individually find investors willing to purchase the new bonds. A market-clearing yield is negotiated and the bonds are issued.

This is what happened this week. On Tuesday the AOFM announced it would issue by syndication a new 0.75% November 2027 Treasury Indexed Bond of a benchmark size. “Benchmark” issues are always the largest issues by value as both issuers and investors want a liquid security and size helps in this regard. On Wednesday, a syndicate which comprised Citi, Deutsche Bank (Sydney), UBS (Australia) and Westpac Institutional Bank had lined up investors and $3 billion worth of these index-linked bonds (ILBs) were issued.

They are called index-linked bonds or “linkers” for short as the face value is linked to CPI and adjusted every 3 months. As they are inflation-adjusted, their 0.8725% yield is “real” and not “nominal”.

Most investors in these latest ILBs are domestic and that is generally true of all AOFM bond issues. Fund managers account for the majority of purchasers by value but in recent years banks’ trading desks have been taking on more ILBs. While there has not been a lot of ILB issues, until 2015 trading desks would take around 10%. Now it is more like 25-30%.

18 August 2017

As part of the announcement regarding a new capital note (ANZ Capital Notes 5), ANZ has outlined the options available to holders of ANZ CPS3 hybrids (ASX code: ANZPC).

Under the (revised) terms of the CPS3 securities, holders who were registered on 11 August may

- reinvest the face value of their holdings into the new capital notes

- sell into a buy-back offer

- do nothing and continue to hold their securities.

In order to be able to offer the buy-back and re-investment options to CPS3 holders, ANZ had to amend the CPS3 terms so as to allow a pro rata dividend payment to all CPS3 holders, including eligible CPS3 holders who participate in the buy-back facility. The pro rata dividend will be paid for the period from 1 September 2017 to the buy-back settlement date which is expected to be 28 September 2017. To be eligible for the pro rata dividend, holders will need to be registered on the expected record date on 20 September 2017.

Holders who wish to keep their CPS 3 securities may do so until they are sold on the ASX or ANZ exchanges them under the CPS 3 rules. ANZ has stated it has “not made any decision how it will deal with the CPS3 which are not bought-back under the Buy-Back Facility” but it points out the factors which it would take into account if it were to do so. These factors include APRA approval and replacement with “tier 1 capital of the same or better quality” unless APRA deems otherwise.

These CPS3 holders who are still holding their CPS3 in March 2018 will receive a dividend calculated from 28 September 2017 (or the buy-back settlement date if it differs) instead of 1 September 2017. Other holders who become registered after 11 August 2017 will be in the same position as holders who decide not to reinvest into the new capital notes nor sell into the buy-back offer.

17 August 2017

The Australian economy has just recorded its tenth month of employment gains. The ABS has released employment estimates which indicated the total number of people employed in Australia in either full-time or part-time work increased by 27,900 during the month, more than the generally-expected figure of 20,000. Consequently, the unemployment rate fell from a revised June figure of 5.7% to 5.6% at the end of July (although in a technical sense the difference arose from rounding and it was basically unchanged at 5.65%).

The total number of work hours across the whole economy fell by 0.8% when compared to June as 48,200 more part-time jobs were created and 20,300 full-time jobs disappeared. However, on a 12 month basis the figures were more encouraging; aggregate hours worked grew by 1.9% as 155,800 full-time and 113,000 part-time positions were created.

On the surface of things, the unemployment rate has been stuck around 5.6% since October 2016. However, in this period, more people have been encouraged to return to the workforce and the participation rate has increased from 64.4% at the end of October 2016 to its current figure of 65.1%.

On the day bond yields fell and the local currency was weaker against the U.S. dollar. Three year bond yields slipped from 1.98% to 1.97% and 10 year bond yields dropped 2bps to 2.64%.

Here’s what a few economists thought of the figures:

Felicity Emmett, ANZ

Some of the detail was a bit softer than the headline: full-time jobs fell, hours worked were down and the jobs gains were narrowly based. But we wouldn’t overplay these details. The labour market is clearly improving and additional job gains look likely in the near term. Further out, we continue to think that ongoing inroads into the unemployment rate will be more difficult to achieve, in part because the strong pace of public sector employment gains is unlikely to be sustainable.

Josh Williamson, Citi

Coming on the back of the soft 0.4% private sector wages growth data for Q2, the July labour force data do not suggest that wages growth will pick-up in Q3 outside some influence from the stronger-than-expected regulated increase in minimum wages. Furthermore, the strong employment gains in recent months have been unable to lower the unemployment rate from an average of 5.6% and annual growth in both employment and the labour force look like they have peaked.

16 August 2017

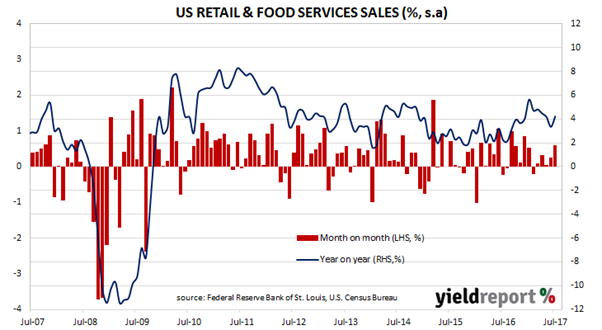

US households have surprised economists with the size of retail spending in July. According to the latest advance U.S. retail sales numbers released by the U.S. Census Bureau, figures indicated retail sales increased by 0.6% during July, well in front of the 0.3% expected and up on June’s revised figure of 0.3%. On a yearly basis, the increase was 4.2%, up from June’s comparable figure of 3.4% (after revisions).

In dollar terms the increase was driven predominantly by vehicle/parts sales as well as sales of building material and gardening equipment. However, the largest percentage increase came from the “non-store” category which increased by 1.3% for the month and 11.5% for the year. Non-store sales currently account for around 11% of total retail sales.

According to ANZ’s Daniel Gradwell, the figures were “were much stronger than expected” and the numbers “point to strong consumption at the start of Q3 and possible upward revisions to the Q2 GDP figures.” He thinks the U.S. economy is at “above-trend” levels that is why FOMC member William Dudley and other support “another rate rise later this year.”

US bond yields moved higher by the end of the day. Both 2 year and 10 year Treasury yields increased by 2bps on the day to 1.35% and 2.27% respectively.

16 August 2017

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of economic activity relative to trend in Australia. The index combines certain economic variables which are thought to lead changes in economic growth into a single measure which is claimed to be a reliable cyclical indicator for the Australian economy and a “critical” indicator of swings in Australia’s overall economic activity.

For the last couple of months, the Leading Index has returned values which imply below-trend growth. July’s reading returned -0.10% and while it was a negative result it was an improvement over June’s revised reading of -0.54% (revised up from -0.76%).

Westpac chief economist Bill Evans contrasted recent readings with those at the start of the year. “Despite the improvement in the growth rate it remains negative for a second consecutive month pointing to below-trend growth momentum and a sharp turnaround from strong positive, above trend reads at the start of the year.” He thinks the Index suggests a 2018 growth rate which was more consistent with Westpac’s forecast than the RBA’s recent forecast of 3.25% growth contained in its August Statement on Monetary Policy. “Westpac is currently forecasting growth of 2.50% in 2018. Trend growth is generally assessed as 2.75%.”

16 August 2017

Each quarter the Australian Bureau of Statistics (ABS) surveys around 3000 enterprises regarding a sample of jobs in each workplace to measure changes in the price of labour across around 18000 jobs.

According to the latest wage price index figures published by the ABS, hourly wages grew by 0.5% in the June quarter, down from the revised March figure of 0.6% but in line with market expectations. Year-on-year growth was steady at 1.9% (after revisions) which means it is still at the lowest growth rate since the beginning of the series in 1999.

ANZ economist Felicity Emmett said the figures were “broadly in line” with the RBA’s expectations “although the tick down in private wage growth would be disappointing.” However, she expects the figures to “pop higher” in the September quarter as a result of the “larger-than-usual” increase in the minimum wage rate handed down by the Fair Work Commission in June.

Public sector hourly wages growth continued to grow faster than private sector hourly pay. Public sector hourly pay grew by 0.6% for the quarter and 2.4% for the year to June while the comparable figures for the private sector were 0.4% and 1.8%.

The hourly wages growth report produced another figure at the bottom of readings since the series began in 1999 and hourly pay growth in the private sector has now slipped below the annual rate of headline consumer inflation. However, some economists have been speculating the downward trend of slower and slower rates of growth may have come to an end. UBS economist George Tharenou said, “it now seems likely the WPI has finally troughed, amid clearly stronger jobs and business conditions and more importantly the surprising 3.3% minimum wage increase…”

15 August 2017

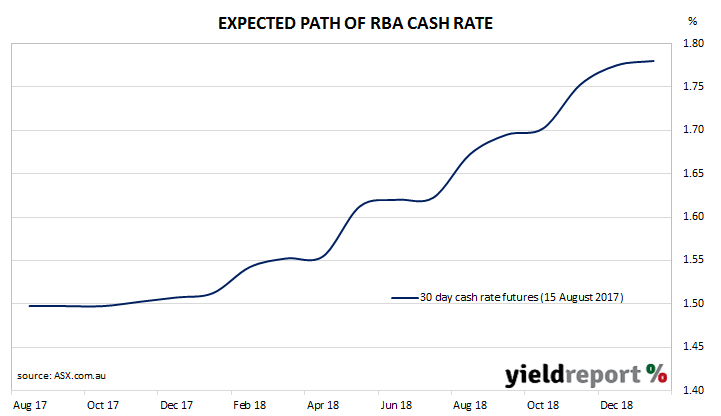

The publication of the minutes of the RBA’s August meeting was a fairly innocuous affair and they did not cause the same ruckus as the publication of the July minutes. Unlike a month ago, bond yields moved just a little higher while the local currency was a little lower. That is not to say these minutes did not contain any important hints about RBA thinking but at least they did not provoke such a strong reaction as in July.

There were the standard areas of RBA interest; global economic conditions, which had continued to improve, especially in China and the local outlook, which was little changed from a month before. Local GDP growth was expected to be around 3% and inflation was expected to increase “gradually”. There was also the obligatory reference to the effect of a stronger local currency which would “result in a slower pick-up in inflation and economic activity than currently forecast.” All fairly usual stuff.

Then there were the changes from the previous minutes. These are what most economists and observers are interested in. ANZ senior economist David Plank thought there were two issues which were worthy of comment. The first was the concern the RBA regarding the level of household debt. The reference to “the risks associated with high household debt in a low-inflation environment” in the last paragraph is a measure of its importance in the RBA’s thinking. The second was its concern regarding “relatively strong” housing price growth in Melbourne and Sydney and a lack of progress in slowing price growth in these two markets.