11 August 2017

Caltex Notes were issued in September 2012. They paid a floating rate of interest equivalent to 3 month BBSW + 425bps, had a first call date of 15 September 2017 and a final maturity date in 15 September 2037.

In a notice to the ASX, Caltex said it intends to redeem all of the Caltex Subordinated Notes on 15 September, 2017. The redemption will be funded out of existing bank debt facilities. Holders who are on the register on 7 September will receive $100 plus $1.5678 interest per note.

This announcement was expected and it had little effect on the notes’ yield. At the closing price of $101.19, the internal rate of return (IRR) was just under 4.0%.

10 August 2017

Magellan Financial Group is set to float a new ASX-listed investment trust, the Magellan Global Trust (MGT). The Trust will invest in a focused portfolio of high quality global companies and it intends to target a 4% cash distribution yield.

MGT will be a closed-end investment trust listed on the ASX which will invest in a portfolio of between 15 and 35 companies of “high quality” global companies. The investment mandate will be flexible to enable the Magellan Global Trust to hold up to 50% of the portfolio in cash. Magellan also intends to manage the currency exposure. Magellan’s Chief Executive Mr. Hamish Douglass and Mr. Stefan Marcionetti will be acting as the portfolio managers.

MGT plans to pay its cash distribution semi-annually. The first distribution of 3.0 cents per unit is expected to be paid in January 2018 and the second distribution of 3.0 cents per unit is expected to be paid in July 2018.

Mr Douglas commented saying: “We believe that the Magellan Global Trust will be an attractive vehicle for investors making an investment in global equities. We believe that many retail investors value regular cash distributions and this has been missing in many global equity products. We consider that the target 4% cash distribution yield differentiates this offering from many other global equity products.”

The initial public offering (IPO) will comprise a Priority Offer for Magellan shareholders and a broker firm/general public offer. Commonwealth Securities, National Australia Bank, Ord Minnett and Taylor Collison will act as lead brokers, while the co-managers include Bell Potter, JBWere, Morgans Financial, and Macquarie Equities. The record date for determining eligibility for the Priority Offer was 1 August 2017.

This IPO is another example of diversified income strategy products coming to market for investors looking for alternative ways of generating yield from their portfolio.

10 August 2017

The ASX will soon have another income-focused fund available for investors to trade when Metrics Credit Partners (MCP) lists its MCP Master Income Trust (ASX code: MXT). MXT is targeting a minimum yield equal to the RBA cash rate plus 3.25% per annum which is currently around 4.75%, net of fees and costs. Distributions will be paid monthly.

The initial public offering (IPO) opens on 10 August 2017 and it is seeking to raise up to $500 million from investors in Australia and New Zealand at a unit price of $2.00. The offer is expected to close on 19 September 2017 and the units are scheduled to list on the ASX on 9 October 2017.

The Trust will be the first ASX-listed investment trust offering exposure to corporate lending. It will provide investors with exposure to a portfolio which reflects activity in the Australian corporate loan market, diversified by borrower, industry and credit quality. The trust initially will have exposure to over 50 individual investments with a near-term target of 75-100 individual investments.

MXT initially will be a “fund of funds”. It will obtain its exposure via a series of wholesale funds managed by the Metrics Credit Partners team. The funds and their initial exposures will be as follows:

- MCP Diversified Australian Senior Loans Fund 60-70%

- MCP Secured Private Debt Fund II 20-30%

- MCP Real Estate Debt Fund 10-20%

09 August 2017

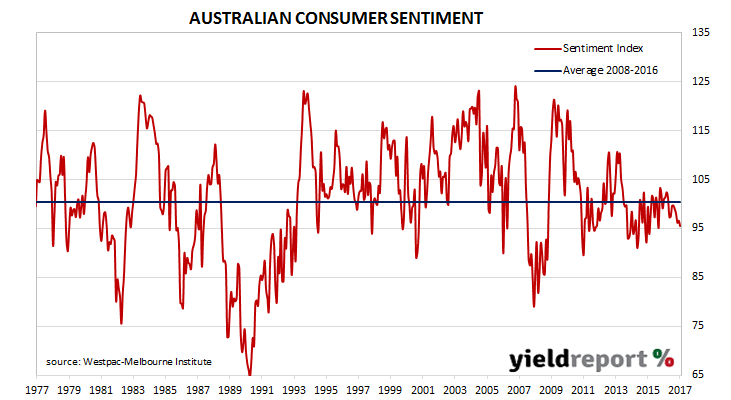

NAB’s latest business survey indicated the business sector continued to experience buoyant conditions, with confidence levels to match. This rosy picture has not extended to Australian households, a divergence some economists attribute to low rates of growth in wages and salaries. According to the latest Westpac-Melbourne Institute Consumer Sentiment Index, households were slightly more pessimistic than a month ago as the Index slipped from 96.6 in July to 95.5 in August. Any reading below 100 indicates the number of consumers who are pessimistic is greater than the number of consumers who are optimistic.

The survey was held in the first week of August and households at the time were just about as pessimistic as they had been just prior to the RBA’s first of two rate cuts in 2016. However, at the moment there is virtually no thought of further rate cuts as other economic indicators are not as they were in 2016. The global environment has also changed and the global rate of growth is now higher. Consequently, central banks around the world either have entered the rate rising part of the cycle (the U.S., Canada, Mexico) or are contemplating it (the ECB). Despite the RBA stating recently it is not in lockstep with other central banks, it will soon face the same pressures to normalise rates as every other central bank.

Westpac chief economist Bill Evans said, “The consumer mood has deteriorated over the last year with August marking the ninth consecutive month where pessimists are outnumbering optimists. We have not seen such a succession of weak reads since 2008. The survey detail suggests increased pressures on family finances, concerns around interest rates and housing affordability in NSW and Victoria are more than outweighing increased confidence around jobs.”

08 August 2017

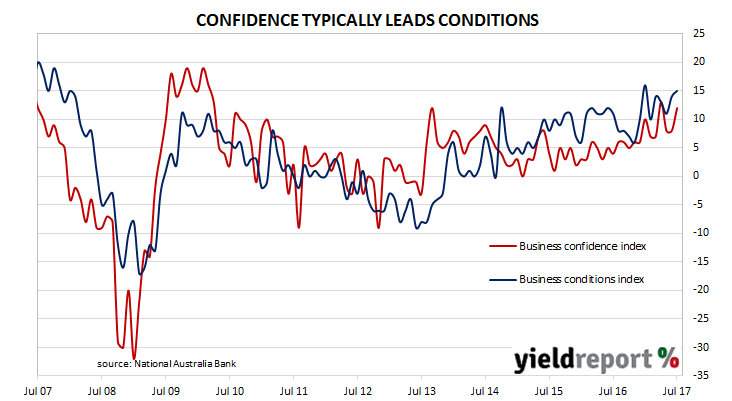

The Australia business sector has continued to do well in July and, on average, businesses have enjoyed conditions close to the boom times of mid-last decade. According to NAB’s latest monthly business survey of 400 firms in late July, its Business Conditions Index rose 1 point to 15 from a revised reading of 14 in June, while its Business Confidence Index jumped 4 points to 12 from June’s revised reading of 8. Both indices are now well above their long term averages.

The capacity utilisation rate, generally accepted as an indicator of future investment expenditure, remained steady at 81.9%. Capacity utilisation was at or was above long-term averages for all sectors of the economy except for mining. Spare capacity was lowest in the transport and utilities sectors.

NAB chief economist Alan Oster thought current economic conditions in Australia warranted the RBA holding the official rate at 1.50%. “Given the risks to the outlook, only tentative signs of moderation in the housing market, and a reluctance to see the AUD strengthen further, the RBA should be content with keeping interest rates on hold for an extended period.” However, some indicators were strong enough for him to consider a time when the RBA may have higher rates in mind. “That said, the recent strength in employment growth and business conditions does give some reason for optimism, and if maintained could signal a change in the balance of risks on the horizon.”

07 August 2017

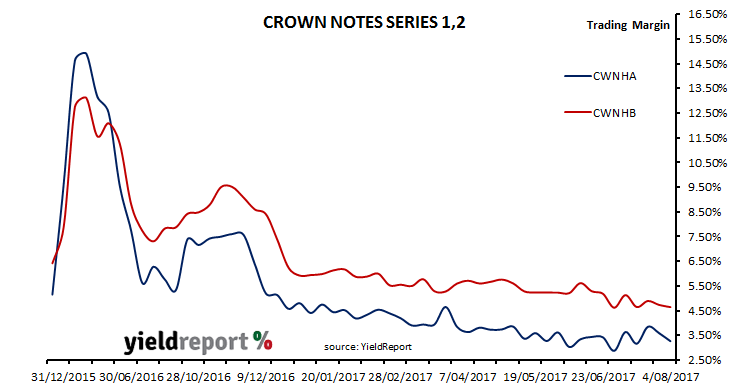

According to Bell analyst Damien Williamson, Crown series I Notes (ASX code: CWNHA) are more than worthwhile. He says the full year’s profit result “underpins the outstanding value currently provided by CWNHA” as Crown’s net debt has been reduced to only $174 million at the end of the financial year.

“The 5.00% issue margin on CWNHA equates to expensive debt for a cashed up Crown…This virtually ensures Crown will redeem the remaining CWNHA securities on issue at the 14 September 2018 call date.”

Crown has been buying Series 1 notes at its discretion for some months but in recent weeks few, if any, notes have been purchased. As at 11 August 2017, a cumulative total of 1,266,277 Notes out of 4,053,423 have been bought back by Crown so there is no shortage of notes left outstanding. According to YieldReport calculations, the trading margin on Crown’s Series 1 Notes was 307bps as at the close of business on 11 August 2017.

07 August 2017

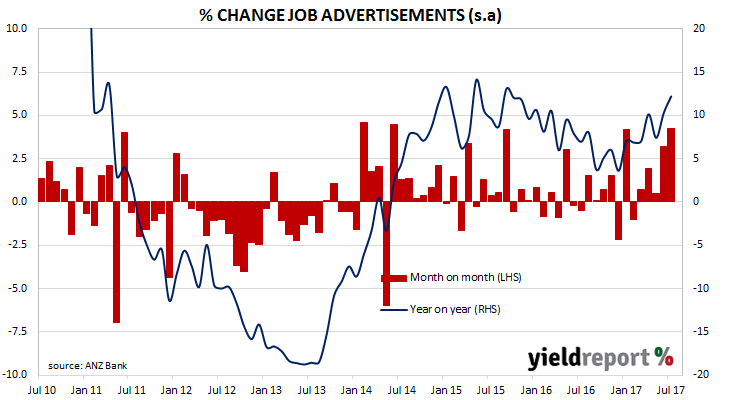

ANZ’s job advertisement survey is well-known as a leading indicator of employment numbers in Australia. It reflects changes in demand for labour and it provides another measure of activity in the economy. There is also a fairly good inverse relationship between changes in Australia’s unemployment rates and changes in the RBA cash rate. Understanding the path of Australia’s unemployment rate has historically provided a reliable indicator of RBA rate changes.

Figures for July have been released and, after revisions, total advertisements in July rose by 4.2% to 177,879 (seasonally adjusted), up from June’s comparable figure of 175,175. On a 12 month basis, job advertisements were 12.2% higher when compared to July 2016 and an increase from June’s comparable figure of 10.3%.

The inverse relationship between job advertisements and the unemployment rate is quite strong (see below chart). An increasing number of job advertisements should be accompanied by lower unemployment rates.

04 August 2017

Australian consumers increased their spending, albeit at a slower rate, for a third month in row, according to June retail sales figures released by the ABS. Sales grew by 0.3% over the month, which is just over the +0.2% growth rate expected by markets but down on May’s revised growth rate of +0.6% and April’s 1.0%. On a year-on-year basis, sales grew by 3.8%, the same annual rate as in May’s figures and the highest annual rate since March 2016.

The figures were described by ANZ senior economist Jo Masters as “a solid outcome given the strength in the previous two months.” She said the figures were indicative of a strong contribution by private consumption to upcoming second quarter GDP figures but “we remain cautious about the outlook for consumption as households grapple with a variety of headwinds”. These headwinds comprised “weak wage growth, high indebtedness, slowing house price growth and higher energy bills”.

Westpac’s Matthew Hassan viewed the figures in a slightly more positive light than his ANZ counterpart. “Overall this is a significant upside surprise. Although the retail survey is a partial measure that does not always map to the quarterly consumption figures in the national accounts, the jump from a flat Q1 to strong Q2 is a clear positive signal.”

04 August 2017

CBA’s woes with Austrac over its failure to report over 50,000 suspicious transactions appears to have limited effect in the market for CBA’s ASX-listed hybrids. While trading margins on all CBA hybrids increased compared to a week ago, only CBA PERLS 6 (ASX code: CBAPC) margin increased by a larger-than-usual amount (+66bps) over the week. The PERLS 6 have just over 12 months to maturity and so changes in trading margins tend to be amplified.

03 August 2017

Suncorp announced its 2017 profit results and the market did not take them well. Ordinary shares fell nearly 6.5% on the day. Evans & Partners Head of Income Products Michael Saba noted the poor response of the market to the results and had a look at Suncorp’s various hybrids which trade on the ASX.

Suncorp announced its 2017 profit results and the market did not take them well. Ordinary shares fell nearly 6.5% on the day. Evans & Partners Head of Income Products Michael Saba noted the poor response of the market to the results and had a look at Suncorp’s various hybrids which trade on the ASX.

“The recently-listed SUNPF (Suncorp Capital Notes) has shown some response to the share price weakness. Suncorp hybrid margins have been widening with the share price weakness prior to today.

Trading margins of Suncorp’s various hybrids and notes did not rise materially on the day and, in the cases of Suncorp Notes (ASX code: SUNPD) and Suncorp Capital Notes (ASX code: SUNPF), trading margins actually fell a little.

However, Saba was surprised by this behaviour. His analysis suggests Suncorp’s hybrid margins tend to rise and fall with Suncorp’s ordinary share price (see his chart below).

“Today’s fall is not yet reflected and will depend on the share price level over the next week.”

The chart below shows how Suncorp’s various ASX-listed hybrids looked relative to other hybrids at the end of the day.