02 August 2017

One of the US Fed’s favoured measures of inflation is core personal consumption expenditure (PCE). The core version of consumer spending strips out energy and food components, which are volatile from month to month, in an attempt to identify the prevailing trend. It’s not the only measure of inflation used; the Fed also tracks the Consumer Price Index (CPI) and Producer Price Index (PPI) from the Department of Labor.

The latest core PCE figures have been published by the Bureau of Economic Analysis as part of June figures for personal income and expenditures. At 0.1% for the month and 1.5% year on year, the numbers were slightly above market expectations although they were in line with May’s comparable figures after revisions. As ANZ put it, the figures were “a touch stronger than expected…Nevertheless, the current trend is still down.”

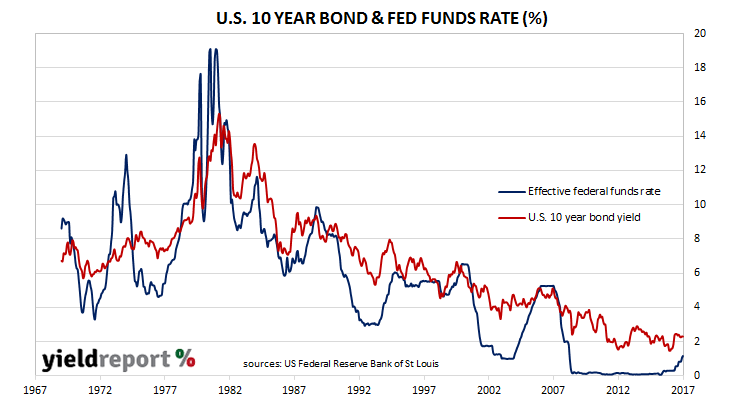

NAB senior economist David De Garis said the monthly changes in headline and core PCE deflators met expectations but they “reflected the still low inflation mould.” US 2 year bond yields closed 2bps higher at 1.36%, while 10 year yields rose by the same amount to 2.27%. The U.S. dollar fell against the euro but rose against the yen.

01 August 2017

No one expected the RBA Board to move the overnight cash rate in any direction at its August meeting. The Board obliged and kept the cash rate at 1.50%. The statement accompanying the decision referred to subdued wages growth, core inflation running below target and an uncertain outlook for consumer spending.

For some time, the RBA has been concerned with the build-up of household debt. It has also regularly made references to the Sydney and Melbourne housing markets which appear to be expensive according to several measures. Both of these topics and the language around each was basically unchanged.

A new topic of concern for the RBA was the rise in the AUD against the USD which occurred after the release of minutes of its June meeting. For all the anticipation about what the RBA would say with regards to the recent rapid movement of the Aussie against the USD, the RBA was refrained. Some economists noted the absence of any attempt to “jawbone” the Aussie to lower levels and the statement simply noted inflation and economic growth would be slower in the presence of “an appreciating exchange rate”.

Here’s what a few economists had to say.

Paul Brennan, Citi

There was a strengthening of the commentary around the exchange rate, which isn’t surprising. The Governor sees downside risks to output, employment and inflation from an appreciating AUD, which he sees as at least partly reflecting the lower USD. In our view the Bank would be particularly concerned if the AUD remains stubbornly high, should the terms of trade decline as the Bank is currently expecting…We continue to expect no change in the cash rate this year and well into next year.

Bill Evans, Westpac

Despite the Governor stating “the Bank’s forecasts for the Australian economy are largely unchanged”, it appears clear to us that it will revise down its growth forecast for 2018 from 3.25% to 3% in response to the rise in the AUD… I am a little surprised that the Bank is likely to take this step given generally positive developments around the world economy, the labour market and business confidence since May… We remain comfortable with our on hold call, and can only conclude from the Governor’s statement that the Bank is not as resigned to a rate hike in 2018 as may have been the case a month ago

31 July 2017

The Melbourne Institute’s Inflation Gauge is an attempt to replicate the ABS consumer price index (CPI) on a monthly basis instead of quarterly. It has turned out to be a reliable leading indicator of the CPI, although there are periods in which the Inflation Gauge series and the CPI have diverged, only for the two series to eventually converge over the space of six to twelve months.

During July, the Inflation Gauge increased by 0.10%, which is 2.70% higher than a year ago. Core measures of inflation, such as the Melbourne Institute’s version of “trimmed mean”, increased by 0.10% for the month or 2.30% on an annualised basis. This takes the core measure back into the RBA’s target range.

Although the gap between official and unofficial measures has expanded, a lot can happen between now and the next set of CPI figures which will be released in late October. However, as a leading indicator, one would expect official CPI figures to follow the Melbourne Institute measure. Readers will note from the chart above how the Inflation Gauge can reverse course in the short term and one should not read too much into any one month’s numbers.

31 July 2017

NAB income securities (ASX code: NABHA) were issued in the late 1990s when floating rate securities were just being introduced. They were not well understood and some time was needed before the market a settled on an accepted band for its spread over BBSW.

Since then people have been speculating about the likely redemption of NAB’s income securities. The more fanciful sales spiel one will hear typically included the suggestion these securities would be redeemed at their face value of $100 and so buying them at $65 or $75 would provide the investor with a tasty capital gain. While such an outcome is not impossible, it has not happened so far and if NAB was inclined to redeem them, it would have done so already.

Damien Williamson from Bell Potter thinks there may finally be an incentive for NAB to now do so. As various income securities issued before December 2009 gradually lose their Additional Tier 1 status under Basel III rules over time until January 2022, their attraction as an inexpensive source of perpetual capital (BBSW +125bps) will fade. He speculated if trading margins were to drop down low enough, there would be an incentive for a bank to refinance these securities by issuing a new AT1 Basel III hybrid.

“It would appear to become increasingly attractive to refinance NABHA if NAB had the ability to issue a new Additional Tier 1 hybrid at a margin of 2.80% (grossed up for franking), the same rate as where CBAPD (PERLS 7) was priced in August 2014, particularly as NABHA’s Additional Tier 1 weighting steps down towards zero in January 2022.”

31 July 2017

Loans to the private sector continue to increase at a steady rate in June, driven by business loans and home loans to owner-occupiers. According to the latest RBA figures, private sector credit grew by 0.6%, up from May’s figure of 0.4% and a higher than the 0.4% expected by the market. The year-to-June number of 5.4% was also higher than May’s reading of 5.0%.

The larger-than-expected increase was almost equally driven by business loans and owner-occupier loans. These two types of lending account for most loans by value and thus any change in them has a greater effect in overall credit growth (see diagram below).

ANZ senior economist Daniel Gradwell said the strong business credit figures were encouraging “but we do not expect it to be sustained indefinitely. Business finance approvals have remained weak in recent months and suggest that growth in the stock of business credit is likely to ease from here.”

Growth in investor loans slowed again (+0.4%) during June but this type of loan grew by 7.4% on an annualised basis, which gives it the highest growth rate among the four categories (business, personal, investor, owner-occupier). However, according to the RBA, $1.3 billion of investor loans were reclassified as owner-occupier loans in June alone and an estimated $55 billion has been reclassified since July 2015.

28 July 2017

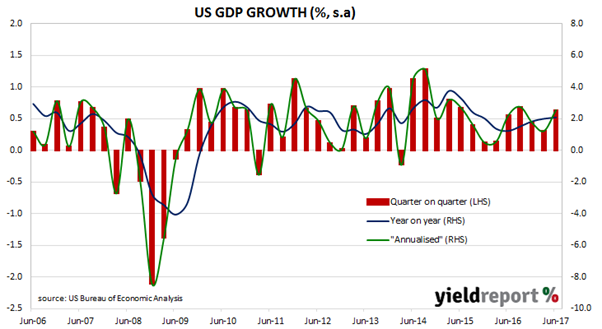

U.S. economics were dominated by two events this week. The first was the FOMC meeting and the second was the release of the June quarter GDP figures. The US Commerce Department released Q2 2017 “advance” estimates of US GDP on Friday night Australian time. This estimate is the first of four estimates and subject to three more revisions over the next two months.

The advance estimates indicate an annualised growth rate of 2.6%, which is broadly in line with the 2.7% median of market estimates but well up on the Q1 2017 figure of 0.7%. Westpac described the difference between the actual and forecast figures as “effectively a rounding error” but a more interesting comment was their observation the figures reinforced the “modest pace” of U.S growth in the first half of 2017. NAB currency strategist Rodrigo Catril saw the good in the figures but at the same time, he acknowledged some roadblocks. “The pace of growth should keep downward pressure on the unemployment rate, but the prospect of higher inflation remains elusive. Meanwhile, amid internal turmoil and Washington paralysis, the prospect of fiscal policy boosting growth above 3% is looking like an almost impossible objective.”

27 July 2017

ANZ has announced it is considering an on-market buy-back for its outstanding CPS 3 securities (ASX code: ANZPC). ANZ said any such offer would be in conjunction with an issue of a new series of hybrid which would include a re-investment offer for CPS 3 holders.

ANZ has done this before. As part of the issue of ANZ Capital Notes 2 (ASX code: ANZPE) in February 2014, ANZ offered holders of ANZ CPS (ASX code: ANZPB) the right to re-invest their face value amounts into the new securities. Holders who did not accept this offer had the Capital Notes 2 securities bought back at their $100 face value in June 2014.

In this case, the offer to repurchase the CPS 3 securities will made via a stockbroking firm which would stand in the (ASX) market and purchase all and any CPS 3 securities at face value. ANZ said as a result of this, it “will not formally exercise its right to redeem the CPS3 on 1 September 2017.” That is, any holder at that point would be likely to hold the CPS 3 until the mandatory conversion date.

ANZ CPS were issued in September 2011 with an optional exchange date on 1 September 2017 and a mandatory conversion date in September 2019. At this stage there has been no formal announcement by ANZ but by making announcing this announcement it would appear to be just a formality.

27 July 2017

The July meeting of the U.S. Fed’s Open Market Committee (FOMC) was expected to keep the federal funds rate range unchanged at between 1.00% and 1.25%. Markets were also on the lookout for some insight into the Fed’s plan to reduce its balance sheet which had been increased by a factor of five since 2009.

The FOMC left the federal funds rate unchanged, as expected, “in view of realized (sic) and expected labor (sic) market conditions and inflation”. The statement regarding inflation running below 2% as opposed to “somewhat below 2%” drew some comments but the observation of the difference represents a tweak rather than something fundamental.

On the second point, its statement regarding the beginning of reducing its balance sheet changed from “this year” to “relatively soon” but the statement was essentially the same, “provided that the economy evolves broadly as anticipated.”

Westpac’s Imre Speizer said the statement suggested the FOMC had “some concern the weakening (of inflation) will be more long lasting”. In conjunction with the Fed’s plan to normalise its balance sheet” “relatively soon”, he said the statement ruled out September’s meeting for a rate rise.

26 July 2017

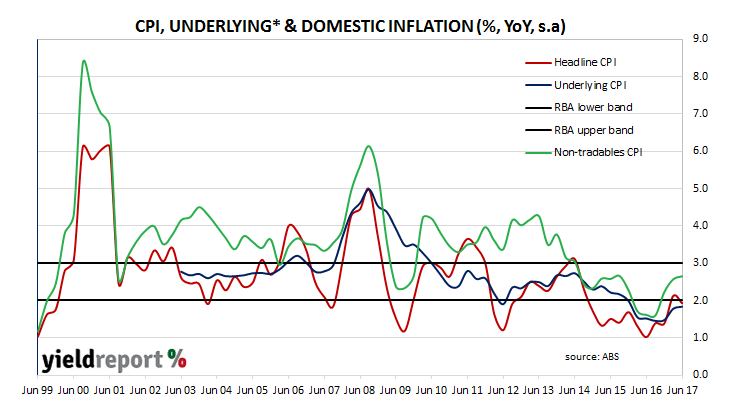

A lack of inflation was once seen as a good thing. However, in recent years, it has been viewed as symptomatic of an economy which is under-utilised, even as employment in some countries approaches levels which have historically been considered to represent full employment.

A lack of inflation was once seen as a good thing. However, in recent years, it has been viewed as symptomatic of an economy which is under-utilised, even as employment in some countries approaches levels which have historically been considered to represent full employment.

Figures for the June quarter have now been released by the ABS and while the headline number was weaker than the expected 0.40%, seasonally-adjusted and core inflation figures were pretty much in line with expectations. The headline rate of inflation was 0.20% for the quarter while seasonally-adjusted inflation came in at 0.40%. On a 12-month basis, each recorded 1.90%.

“Core” inflation measures favoured by the RBA, such as the “trimmed mean” and the “weighted median”, were in line with consensus when considered together. For the quarter, both the trimmed-mean and weighted-median measures increased by 0.50% and the average of the two annual rates came in at 1.8%.

The main drivers of the low headline inflation figure were lower petrol prices, falls in prices for telecommunication equipment and services as well as women’s clothing. Cyclone Debbie was expected to have an effect on fruit and vegetable prices but apparently supermarket competition negated price pressures from reduced supply.

25 July 2017

After a three year absence from international bond markets, Greece has successfully issued €3 billion worth of five year bonds at a yield of 4.625%. The issue was in conjunction with a buy-back of 2019 bonds. Greece last accessed international bond markets in 2014 when it sold Greece sold an equivalent amount of five year bonds at 4.95%.

The Greek economy has been through the wringer since 2009 after the country lost credibility when it lost the ability to service its sovereign debt without external support. Not only was its tax collection system openly rorted by its citizens but its national government also engaged Goldman Sachs in 2001 to mask the true extent of its deficit to circumvent EU budget deficit rules.

Greece’s plans for two more bond issues before the expiry in August 2018 of its latest international bailout “could prove to be a positive turn for that economy and a signal Greece can stand on its own feet,” according to Westpac.

S&P raised its outlook for Greece from “stable” to “positive,” on the basis of recent cost-cutting and an expected return to growth this year. S&P rates Greek government debt as “B-“ while Moody’s has assigned a Caa2 rating to its debt.