25 July 2017

The Income Strategies team at Shaw & Partners have come up with a recommendation for holders of Westpac Capital Notes 2 (ASX code: WBCPE) to switch to ANZ Capital Notes 3 (ASX code: ANZPG). The switch would result in a lengthening of an investor’s investment period from September 2022 to March 2024 but the Shaws team argues the additional margin was worth it.

Below is a chart which shows how they and other ANZ and Westpac hybrids looked at the close of trading on 25 July.

The other switch idea was for holders of Challenger Notes (ASX code: CGFPA) to switch to Challenger Notes 2 (ASX code: CGFPB). As with the Westpac/ANZ switch, the investment period would be extended, in this case from May 2020 to May 2023. The trade-off was roughly a 0.80% per annum increase in trading margin.

21 July 2017

The release of the July minutes early in the week sparked a mini-storm in Australian financial market. Bonds yields, the probability of rate rise implied by futures markets and the local currency all jumped.

Guy Debelle is the Deputy Governor of the RBA and at the end of the week he gave a speech in Adelaide with the title” Global Influences on Domestic Monetary Policy”. In this speech he touched on various influences on domestic policy which act either through the real economy or through financial markets. A large part of the speech was devoted to a discussion of various influences on the neutral rate, one being “international factors”. It was a discussion of the neutral rate and the subsequent appearance of a paragraph in the RBA July minutes which set off the kerfuffle at the start of the week. Debelle’s speech was an opportunity to send a calming message.

In his speech there was a paragraph which comprised three sentences. This is the paragraph:

“There was a discussion of the neutral rate at the most recent Board meeting, as detailed in the minutes of the meeting released earlier this week. No significance should be read into the fact the neutral rate was discussed at this particular meeting. Most meetings, the Board allocates some time to discussing a policy-relevant issue in more detail and on this occasion it was the neutral rate.”

In other words, the RBA Board discusses concepts such as the neutral rate and the gap between it and the actual cash rate all the time.

While most of the speech was an academic view of international linkages with Australia, this section of the speech stands out. It stands out because it was not necessary. The conclusions which were reached would have been unaffected without these three sentences. Therefore, it stands to reason the inclusion was a deliberately designed to deal with fallout from the release of the July minutes. Why did the RBA think such a course of action was required?

20 July 2017

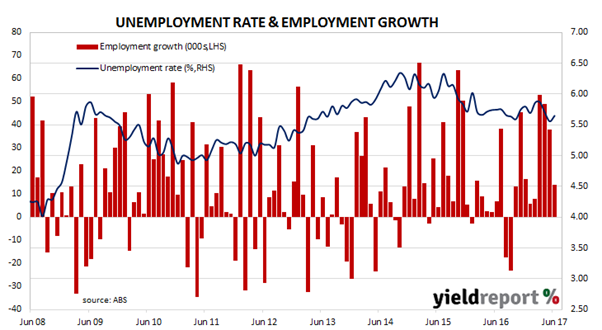

Australia added nearly one quarter of a million jobs over the 2016/2017 financial year and growth in employment numbers forecast by various leading indicators was still coming through in the latest figures. The ABS released employment estimates which indicated Australia’s unemployment rate remained steady at 5.6% while the participation rate rose from 64.9% to 65.0%. The total number of people employed in Australia in either full-time or part-time work rose by 14,000 during the month, which was close to the market’s expectation of +15,000. Total hours worked in June were 0.5% higher than in May and 3.3% higher than a year ago.

Hours worked rose by 0.5% or 3.3% compared to June 2016, the result of 62,000 more fulltime jobs and 48,000 fewer part-time roles.

Westpac senior economist Justin Smirk thought the figures were good but he and his colleagues see some weakness ahead. “All up this was positive update on the labour market following the robust trend sent by the leading indicators. We still expect the monthly numbers to be quite volatile month to month but our Jobs Index is pointing to total employment growth potentially hitting 2.5% by year’s end…We are, however, looking for employment growth to slow as we move into 2017 on the back of a correction to dwelling construction activity, on-going soft household consumption and an underwhelming lift in private investment.”

20 July 2017

APRA yesterday announced its assessment on the additional capital required for the Australian banking sector in order for their capital ratios to be considered “unquestionably strong”. In its assessment, APRA focussed on Common Equity Tier 1 (CET1) capital requirements, given it represented the highest quality of capital and is typically referred to by markets when assessing the strength of an approved deposit-taking institution (ADI).

In its assessment APRA stated its view is the four major Australian banks will need to have CET1 capital ratios of at least 10.5% to meet its “unquestionably strong” definition. As a result of this assessment, APRA will introduce prudential standards to achieve this outcome by effectively increasing requirements for the banks by the equivalent of around 150 basis points (bps). For all other banks and ADIs, the effective increase in capital requirements to meet the “unquestionably strong” benchmark will be around 50bps.

APRA expects all banks and ADIs to meet the new benchmarks by 1 January 2020.

As at December 2016, the average CET1 capital ratio of the four major banks was just above 9.5%, which is 1% above the minimum regulatory requirement. CBA had the lowest ratio at 9.6%, while Westpac (10%), ANZ (10.1%) and NAB (10.1%) all had very similar ratios.

Bearing in mind that the four major banks have, on average, already substantially increased their CET1 capital ratios since 2014, the additional 100 basis point increase will mean that those banks will have, on average, increased their CET1 ratios by the equivalent of more than 250bps since the release of the Financial System Inquiry report in 2014.

The major banks have so far taken the news in their stride. CBA chief financial officer (CFO) Robert Jesudason said, “CBA is well positioned to meet this new capital benchmark”, while ANZ advised it was comfortable with its CET1 capital position. Meanwhile NAB Group CFO, Gary Lennon said, “NAB is well placed to respond to these new requirements” while Westpac’s CFO stated “Westpac is well positioned to meet this new benchmark”.

14 July 2017

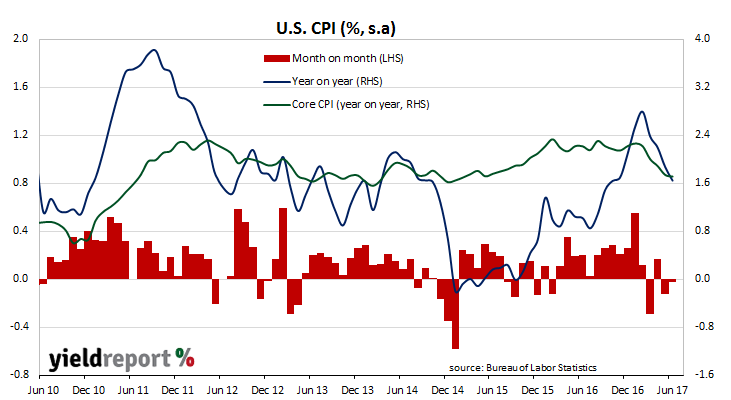

Lower fuel prices have driven U.S. consumer inflation lower again in June. Consumer price index (CPI) figures released by the Bureau of Labor Statistics indicated prices were stable over the month, missing market expectations of a 0.1% increase. On a 12-month basis the CPI growth rate dropped again, this time from 1.9% in May to 1.6%.

Core prices, a measure of prices which strips out food and energy price changes, rose by +0.1% for a third month in a row. The figures were under the expected 0.2% rise, which meant annualised core inflation slipped a little lower, although it remained at 1.7% (seasonally adjusted) after rounding. So far, the annualised figure has dropped each month this calendar year.

The low inflation figures prompted some speculation of a delay of the Fed’s next rate rise. CPI inflation is not the U.S. Fed’s preferred measure of inflation, but core CPI does tend to track core PCE growth (which is the Fed’s preferred measure). Any fall in consumer inflation is therefore viewed as an indicator of a potential fall in core PCE growth.

13 July 2017

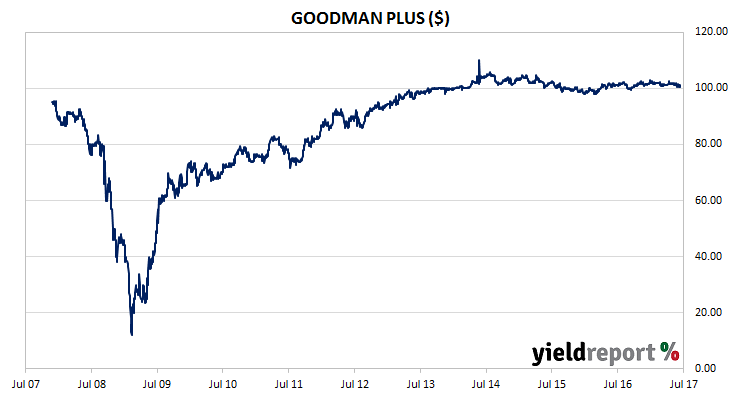

Goodman group first issued $325 million of its Perpetual Listed Unsecured Securities (PLUS) in 2007. The securities paid BBSW + 190bps on the $100 face value until September 2012 when a restructure of the Goodman Group led to an amendment of the terms of the securities. The margin was increased to 390bps and the first “Remarketing” date was moved to 31 December 2017.

Goodman has now announced it will issue a Realisation Notice as per the product disclosure statement terms to repurchase all Goodman PLUS. Holders of PLUS registered on 25 September 2017 will receive the $100 face value plus $1.414027 per security for the last distribution period. These amounts will be paid on 2 October 2017.

It has been a rocky road for PLUS holders (see chart below). The securities were issued just as problems in the U.S mortgage market were starting to gain public attention. As these problems morphed into what is now known as the GFC, the price of PLUS tanked. However, as with most hybrids on issue at the time, the price recovered dramatically but holders would have had an eye-opening experience all the same.

12 July 2017

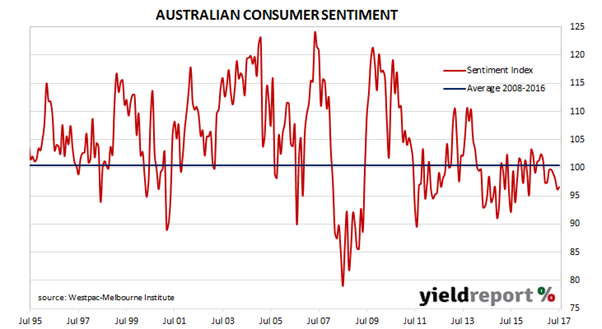

While conditions are near pre-GFC highs in the business sector, Australian households are not nearly as optimistic. According to the Westpac-Melbourne Institute Consumer Sentiment Index, households are less pessimistic than a month ago but they are still on the negative side of the ledger. The index increased marginally after three months of falls to record a rise from 96.2 in June to 96.6 in July. Any reading below 100 indicates the number of consumers who are pessimistic is more than the number of consumers who are optimistic.

Confidence among those with mortgages actually rose while other parts of the survey indicated people were less confident regarding their family’s finances over the next twelve months. Survey respondents were slightly less pessimistic about keeping their jobs and their expectations of becoming unemployed were just a little above the long-term average. However, their view of becoming unemployed has essentially been static since October 2015 and at this stage an improving trend is not clearly evident.

11 July 2017

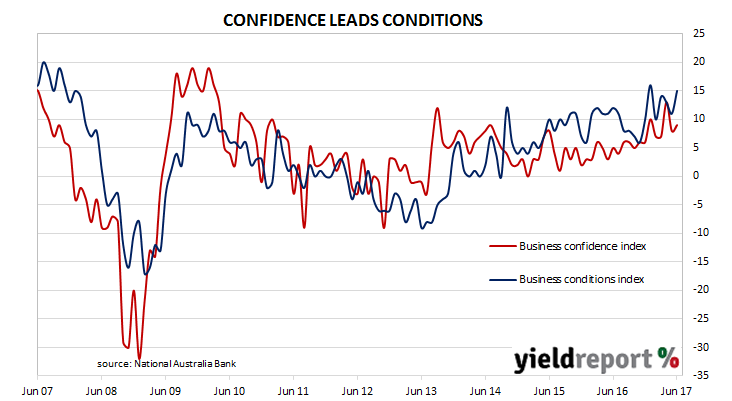

The Australia business sector has continued to do well in June and, on average, businesses have enjoyed conditions close to the boom times of mid-last decade. According to NAB’s latest monthly business survey of 400 firms in late June, its Business Conditions Index rose 4 points to 15 from a revised reading of 11 in May, while its Business Confidence Index edged up a point to 9 from May’s revised index reading of 8, which is 2 points above its long term average.

The capacity utilisation rate, generally accepted as an indicator of future investment expenditure, fell back to 81.9% from its revised May figure of 82.5%. According to NAB, capacity utilisation in the manufacturing and wholesale sectors deteriorated and they joined transport and mining as utilising less than their long term averages. Even so, NAB seemed unconcerned as they pointed to increases in other leading indicators such as capital expenditure.

Trading conditions and profitability drove the increase in the Conditions Index while employment conditions remained largely unchanged. Alan Oster, NAB’s chief economist, restated his view after the May results but with a small addition. Solid business conditions now exist across most industries and states rather than just across industries, “which suggests the recovery is becoming more entrenched.” Westpac senior economist Andrew Hanlon took pretty much the same view. “Directionally, the survey suggests that the Australian economy is experiencing a trend improvement in underlying conditions after the slowdown in mid-2016, which was associated with the July Federal election.”

10 July 2017

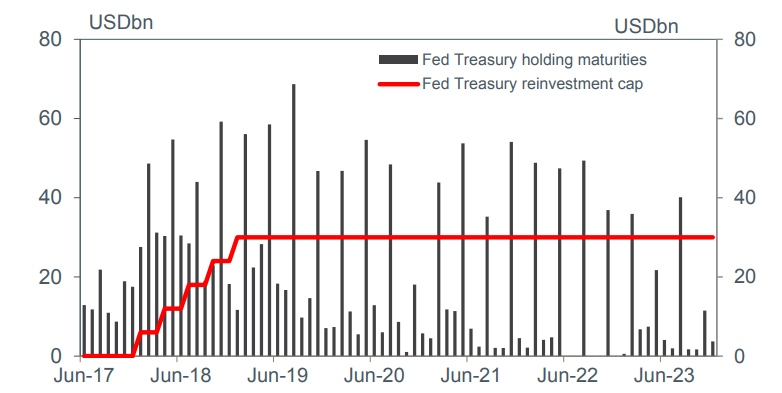

During the GFC, the U.S. Fed slashed its official rate, known as the federal funds rate, down to zero. It also bought U.S. Treasury bonds and mortgage-backed securities on an unprecedented scale in an attempt to keep yields low while expanding the monetary base*, thus (hopefully) injecting money into the U.S. economy. Eight years later, the U.S. central bank thinks it is time to back away from the emergency measures deemed necessary during and after the GFC.

For some months now, the U.S. Fed has flagged its plan to “normalise” its monetary policy. The first part of its plan involves the raising of the federal funds rate and the first increase occurred in December 2015. The second part involves the disposal of its bond holdings which it plans to do by not reinvesting matured bonds.

For now, markets seem to be sanguine about the gradual removal of such a big holder of bonds from the U.S. market. However, people such as JP Morgan Chase chief Jamie Dimon think the reversal of such a massive programme may have its setbacks. “We’ve never have had QE like this before, we’ve never had unwinding like this before….We act like we know exactly how it’s going to happen and we don’t.”

While there are these sorts of doubts, Westpac’s Rates Strategy team of Damien McColough and Rob Thompson think this part of the normalisation plan will not disrupt financial markets and they make two points as to why they think so.

Firstly, the plan will be phased in. Reinvestment will be reduced by USD$6 billion in the first month and USD$12 billion in the second month and so on until reinvestment in any given month is reduced by $30 billion (see below chart). While this may sound like a lot, at one point the U.S. Fed was purchasing USD$80 billion worth of bonds each and every month.

source: Westpac, Federal Reserve

07 July 2017

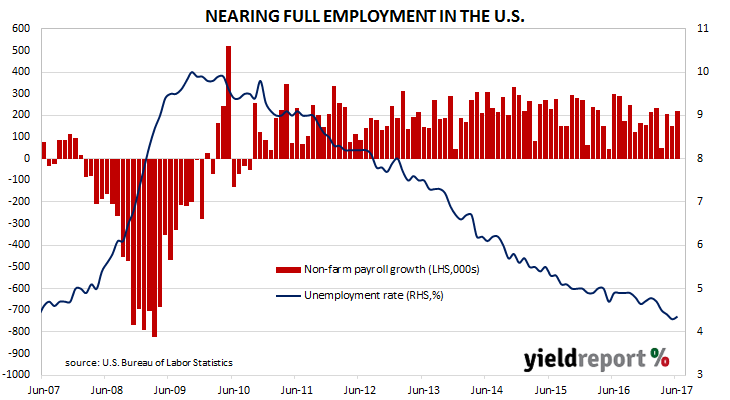

The number of people employed in the U.S. has hit a record high at the end of June after another month of employment growth. According to the U.S. Bureau of Labor Statistics, the U.S. economy created 222,000 jobs in the non-farm sector in June against expectations of 178,000. After revisions to previous months’ figures, the unemployment rate rose from 4.3% to 4.4% while the average hourly pay rate rose by 2.5% over the last 12 months.

The total number of employed person in the U.S at the end of June was 146.4 million in the non-farm sector and 153.2 million overall. Since the start of the year over 1 million new jobs have been created in the non-farm sector. While employment growth was strong and the employment-to-population ratio increased from 60.0% to 60.1%, the unemployment rate increased as more people joined the search for work and the participation rate increased from May’s rate of 62.7% to 62.8% in June.

The U.S. has not had a negative employment growth figure since September 2010 which is 81 months ago. There have already been two rate rises this year and some expect a third rise later this year. However, the hourly wage increase of 2.5% was described as “benign” by Westpac’s Imre Speizer, although he described the overall result as the numbers as “decent”. On balance, he did not think the employment figures would be a possible obstacle to tighter U.S. monetary policy. “This will not alter the basic Fed profile for another hike before the year is out, nor the commencement of reinvestment tapering, although some of the doves will feel emboldened to hammer home the low wage/inflation theme.”