06 July 2017

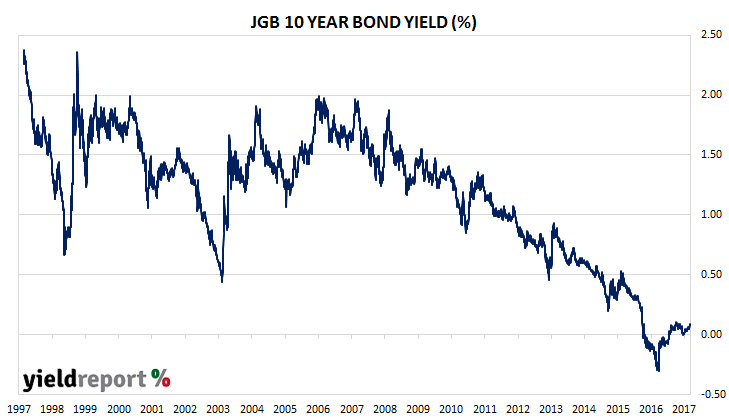

Just in case anyone thought the recent trend of Japanese ten year bond yields creeping higher was a sign the Bank of Japan was now accepting of a move away from zero, the BoJ made an announcement which made it clear it was not. The BoJ announced it would buy unlimited amounts of 10 year Japanese government bonds (JGB) in the secondary market at a yield of 0.11%. The announcement came after Japanese 10 year yields moved to 0.10% amid a recent rise in bond yields around the world.

It is the BoJ’s second intervention to enforce its (nearly) zero yield policy which was announced in September 2016. In February it announced it would buy unlimited amounts of 10 year JGBs, also at a yield of 0.11%. While its purchases did not force the 10 year bond yield back to zero at the time, the BoJ’s actions reinforced its message to investors and traders; it will not tolerate any meaningful gap between the prevailing market yield and its policy target.

06 July 2017

Edinburgh-based fixed income manager Cameron Hume has recruited a senior industry specialist as it seeks to grow its investment management capacity.

Russ Oxley will work with the firm on a consultancy contract agreed with his Edinburgh-based management company Avrox Investment Solutions.

Oxley was previously Head of Fixed Income Absolute Return at Old Mutual Global Investors. He joined from Ignis Asset Management where his team managed more than £4 billion of assets for its Absolute Return Government Bond fund as well as substantial assets in liability driven investment and other rates mandates.

His role will be to develop strategic investment ideas as part of Cameron Hume’s investment team.

He said: “I’m delighted to be joining Cameron Hume at such an exciting stage in their evolution. They are a small but highly ambitious asset management firm and I’m confident I can assist in helping them as they move to the next level of their development.”

Cameron Hume, founded in 2011 by Guy Cameron, a former partner at Baillie Gifford and Christian Torkington, held senior roles at Barclays, Standard Life and Scottish Widows and currently manages USD$700 million on behalf of Sanlam, one of South Africa’s biggest insurers.

Torkington said: “This is a very exciting time for Cameron Hume. Russ’ experience and expertise will be invaluable to our continued progression.”

05 July 2017

The AOFM, the financing body of the Australian Federal Government, typically holds several bond tenders each and every week of the year as it manages the government’s debt positions. Normally, tenders of Federal Government bonds are fairly tepid affairs and unkind people would say they have all the excitement of watching paint dry. However, Wednesday’s tender of $800 million April 2029s drew a bit of attention and got tongues wagging. Well, at least for a day or two, anyway.

The reason this particular tender stood out can be seen in the following email sent by the AOFM to interested parties giving details of the results of the tender:

As readers can see, there was one successful bidder and that one bid was filled “in full”. In other words, someone bid for $800 million worth at a yield above everyone else and they got the lot, leaving nothing for any of the other bidders.

04 July 2017

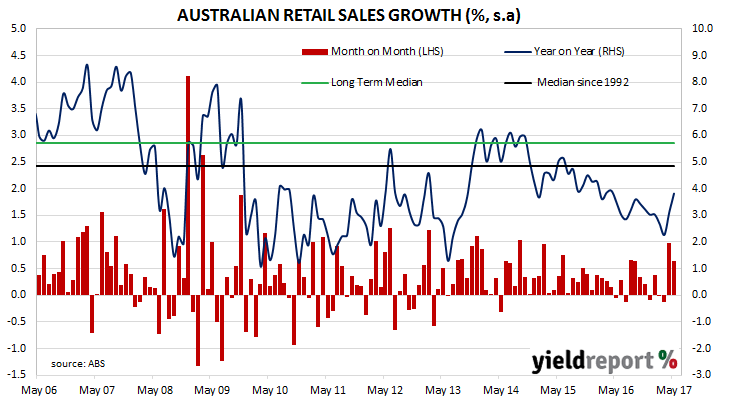

Australian consumers have kept their wallets open for a second month in row, according to May retail sales figures released by the ABS. Sales grew by 0.7% over the month, which is well over the +0.2% growth expected and a continuation of the strong result in April. On a year-on-year basis, sales grew by 3.8%, which is the highest annual rate since March 2016.

Some economists do not expect the high rates to continue. ANZ’s Daniel Gradwell said, “The recent increase in spending is a welcome development, but we remain sceptical of its longevity given the number of headwinds that households are facing…such as soft wages growth, slower house price increases, high leverage and out of cycle mortgage rate increases, all of which are likely to weigh on spending going forward.”

Deutsche Bank’s Adam Boyton took a similar view but related his thinking to overall consumer sentiment. “In our view a sustained 0.5% (month on month) growth rate is at odds with the current level of consumer sentiment. As a result, we would expect a softer pace of growth in retail sales over coming months. We also expect utility price increases from 1 July to have a negative impact on sentiment, ‘free’ household cash-flows and consumer spending as we move through the September quarter.”

03 July 2017

The ASX will soon have another income-focused ETF available for investors to trade when VanEck launches its Vectors Australian Floating Rate ETF. The new ETF will be an Australian floating-rate note ETF which will trade under the ASX code “FLOT”. The new ETF will be the first Australian ETF to offer investors exposure to a diversified portfolio of Australian floating-rate notes (FRNs). The fund will have a management cost of 0.22% p.a. and distributions will be made quarterly.

Arian Neiron, Managing Director of VanEck Australia said, “We are delighted to shortly be offering a passive FRN option for Australian investors. FLOT is designed to be a potential solution for investors who are seeking a defensive source of income with a higher yield than cash investments in an easy-to-access and easily tradable ETF. The strategy may suit investors such as retirees and self-managed superannuation funds who wish to preserve their capital but diversify out of very low yielding term deposits. Concerns about rising interest rates have prompted many investors to consider moving out of longer-term bonds where duration risk, or the risk that bond prices will fall if interest rates rise, is greater,” Neiron said.

“In contrast, returns on FRN coupons are designed to rise with short-term interest rates, which will benefit investors, while their capital stays relatively intact. We expect to see strong demand for this ETF, which will give broad exposure to investment grade quality short-terms bonds for a very low management cost.”

VanEck is one of the largest providers of ETFs worldwide, managing approximately USD$43 billion in both active and passive portfolios. In Australia, VanEck currently manages 13 ETFs listed on the ASX.

The new ETF will track the Bloomberg AusBond Credit FRN 0+ Yr Index which includes around 200 Australian-issued FRNs from over 80 issuers and has a running yield (as at 31 May 2017) of 2.74%.

03 July 2017

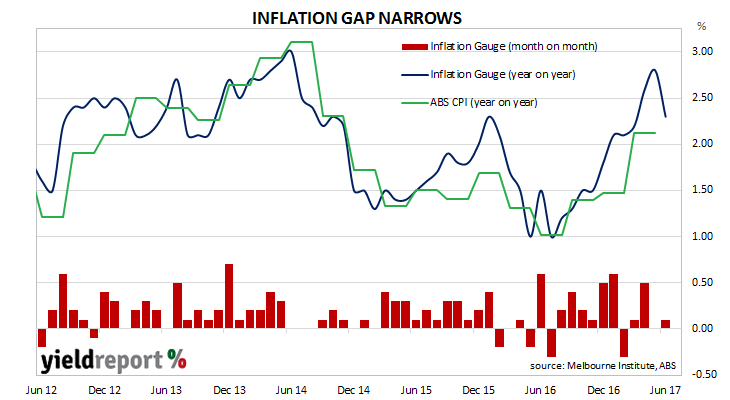

The Melbourne Institute’s Inflation Gauge is an attempt to replicate the ABS consumer price index (CPI) on a monthly basis instead of quarterly. It has turned out to be a reliable leading indicator of the CPI, although there are periods in which the Inflation Gauge series and the CPI have diverged, only for the two series to eventually converge over the space of six to twelve months.

During June, the Inflation Gauge increased by 0.1%, which is 2.3% higher than a year ago. Core measures of inflation, such as the Melbourne Institute’s version of “trimmed mean”, increased by 0.2% for the month or 1.9% on an annualised basis. This takes the core measure back below the lower boundary of the RBA’s target range.

03 July 2017

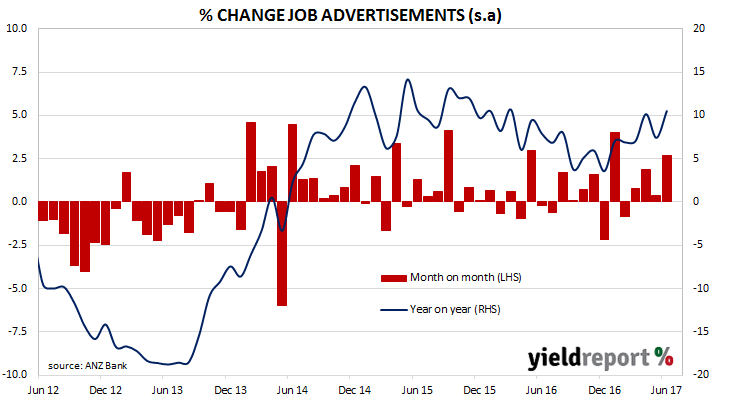

ANZ’s job advertisement survey is well-known as a leading indicator of employment numbers in Australia. It reflects changes in demand for labour and it provides another measure of activity in the economy. There is also a fairly good inverse relationship between changes in Australia’s unemployment rates and changes in the RBA cash rate. Having an understanding of where Australia’s unemployment rate is headed therefore provides clues as to future RBA rate changes.

Figures for June have been released and, after revisions, total advertisements in June rose by 2.7% to 175,091, which is 10.5% higher than a year ago.

30 June 2017

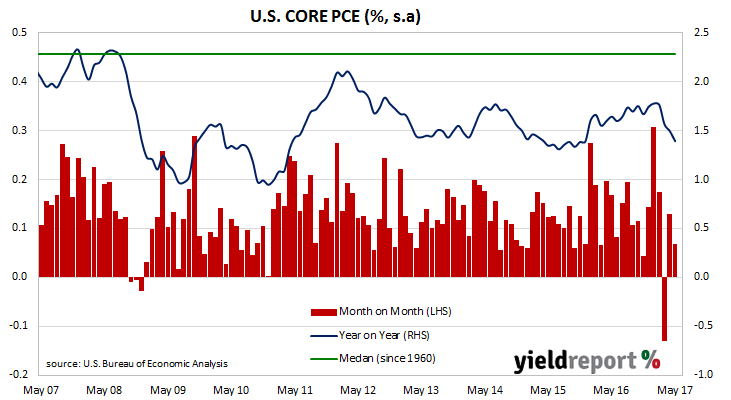

One of the US Fed’s favoured measures of inflation is core personal consumption expenditure (PCE). The core version of consumer spending strips out energy and food components, which are volatile from month to month, in an attempt to identify the prevailing trend. It’s not the only measure of inflation used; the Fed also tracks the consumer price index (CPI) and producer price index (PPI) from the Department of Labor.

The latest core PCE figures have been published by the Bureau of Economic Analysis as part of May personal income and expenditure data. On a month-on-month basis, core PCE rose by +0.2%, which is down from April’s figure of +0.2% but in line with expectations. On a year-on-year basis, core PCE grew by +1.4% which is also lower than April’s comparable figure of +1.5%.

The U.S. Fed is known to have a 2% target for annual core PCE but the recent two months of soft PCE data does not appear to have changed Fed officials’ view of the need for official rate “normalisation”. Bond yields rose on the day but possibly not because of the report. Yields on 2 year Treasury bonds rose 1bp to 1.38% while yields on 10 year bonds rose 3bps to 2.30%.

29 June 2017

Shaw and Partners Income Strategies desk just published a simple but illuminating review of interest rate securities’ returns for the financial year to 29 June 2017. Here it is:

source: Shaw and Partners

source: Shaw and Partners

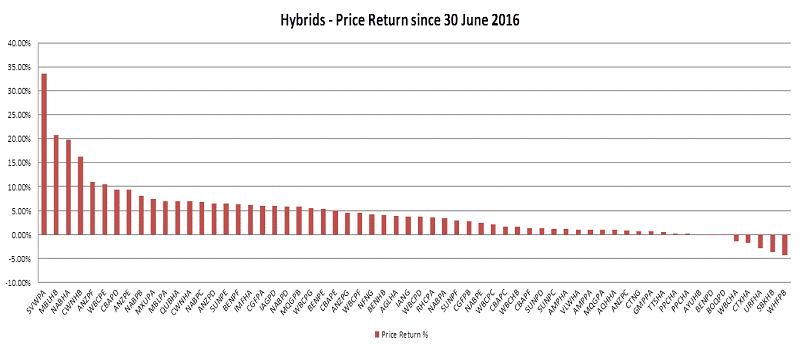

The best returning securities were typically hybrids which have passed their step-up dates, such as Seven TELYS 4 (ASX code: SVWPD) and some income securities such as those issued by Macquarie (ASX code: MBHLB) and NAB (ASX code: NABHA). These securities have undefined maturity dates and they will only mature when the issuers make a decision to redeem or convert them; holders do not have any say in the matter. The issuers have not done so far and there is little reason to expect a change any time soon. At various times in past years, these securities have been at the other (negative) end of the diagram.

Securities which produced negative returns have done so as their prices fell to the extent the unrealised capital loss outweighed any income paid to investors over the year. There does not seem to be any pattern to securities which went backwards but they include some income securities such as Suncorp-Metway Notes (ASX code: SBKHA) and some step-ups such as Ramsay Health’s CARES (ASX code: RHCPA).

The message from this is while 2016/2017 has produced double–digit returns for some holders, it would be a courageous holder of these securities to expect 2017/2018 to be as profitable. However, note the high ratio of the total number of positive returns to total number of negative returns and how the negative returns are all less than 5%. One could expect this behaviour in most years due to the nature of the large number of securities which have defined maturity dates, unlike the best and worst performers which tend to have no maturity dates.

27 June 2017

Trading margins of some hybrids are at levels which are close to 2017 highs and as such, Evans and Partners’ Michael Saba thinks there is some value for investors. Saba is especially interested in three of the shorter-dated ones: CBA’s PERLS 6 (ASX code: CBAPC), Westpac Capital Notes (ASX code: WBCPC) and Westpac Capital Notes 2 (ASX code: WBCPD). This view was supported by Shaw’s Income Strategies desk, which referred to these securities as “attractive relatively defensive investment option[s]” a few days earlier.

Here’s how the trading margins of the three securities have performed since late October 2016. As at 23 June 2017.