27 June 2017

European bond yields jumped on the back of comments in a speech by ECB president Mario Draghi to an ECB forum of central bankers and academics held in Sintra, Portugal. In a speech titled “Accompanying the Economic Recovery”, he made several comments which got economists thinking about the ECB’s planned exit from its negative interest rates and asset-purchase plans.

Amongst the comments were statements which suggest economic growth rates in the Eurozone are robust. According to Draghi, growth is “above trend and well distributed across the euro area”. Spare capacity is gradually being absorbed and “in time” pressures on wages and prices would rise. “And this is what we see,” he said.

He then implied the ECB would need to adjust monetary policy in a manner which would keep monetary conditions constant as European growth rates increased. In other words, rates would need to rise and/or asset purchases would be scaled back. As the neutral rate of overnight cash rose, a rate which is viewed as accommodative/loose/easy would also rise. “As the economy continues to recover, a constant policy stance will become more accommodative and the central bank can accompany the recovery by adjusting the parameters of its policy instruments; not in order to tighten the policy stance but to keep it broadly unchanged.”

However, the ECB chief is wary of financial market volatility which he said in the past has caused a tightening of financial conditions. In a move reminiscent of the U.S. Fed’s constant reminders regarding its planned policy normalisation, he said any change would be made gradually. “Any adjustments to our stance have to be made gradually, and only when the improving dynamics that justify them appear sufficiently secure.”

German 10 year bond yields rose 15bps on the day to 0.40%, while French yields rose 16bps to 0.76%. U.K. and U.S. bond yields rose less than their European counterparts but they were still caught up; yields on both U.K and U.S. 10 year bonds rose 9bps to 1.09% and 2.23% respectively. When Australian markets opened the next day, the local 10 year bond yield rose 10.5bps to 2.52%.

22 June 2017

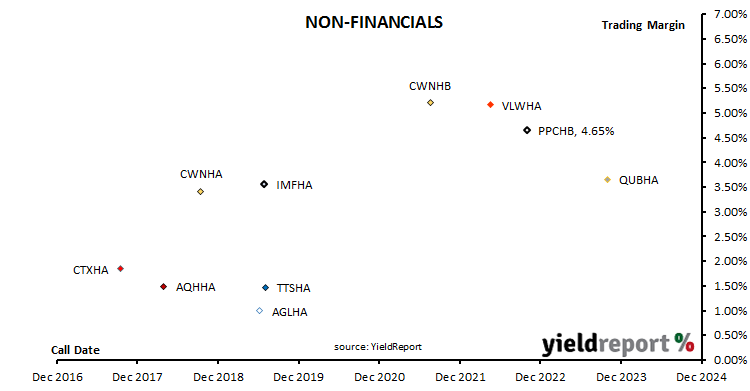

Barely more than a day after Peet announced it would be issuing a new series of ASX-listed notes, it has announced the margin on its new simple corporate bonds (ASX code: PPCHB). The company had initially sought to raise $50 million, but after Peet received additional demand for the bonds, the book-build was closed early. Even though Peet received offers in excess of $50 million, it decided to limit the amount raised and therefore there will be scaling back of applications.

Barely more than a day after Peet announced it would be issuing a new series of ASX-listed notes, it has announced the margin on its new simple corporate bonds (ASX code: PPCHB). The company had initially sought to raise $50 million, but after Peet received additional demand for the bonds, the book-build was closed early. Even though Peet received offers in excess of $50 million, it decided to limit the amount raised and therefore there will be scaling back of applications.

It has been some years since a margin was set not at the bottom of an issue’s indicative range and the margin on Peet’s new securities has stuck to this pattern. The indicative range was 4.65%-4.75% and hence the margin was set at 4.65%. When this margin is added to the current 3 month bank bill swap rate (BBSW) of 1.72%, investors can expect nearly 6.40% annualised for the first quarter and thereafter if BBSW rates do not alter materially. BBSW is typically at a fairly small margin to the RBA’s official cash rate which is currently 1.50%.

The chart below shows the trading margins of existing notes and bonds which are already listed on the ASX. In very simplified terms, a security’s trading margin is the sum of its annualised distributions as percentage of its price less BBSW. (In practice, unrealised annual capital gains/losses and accrued distributions are also taken into account.)

As at the close of business 22 June 2017.

21 June 2017

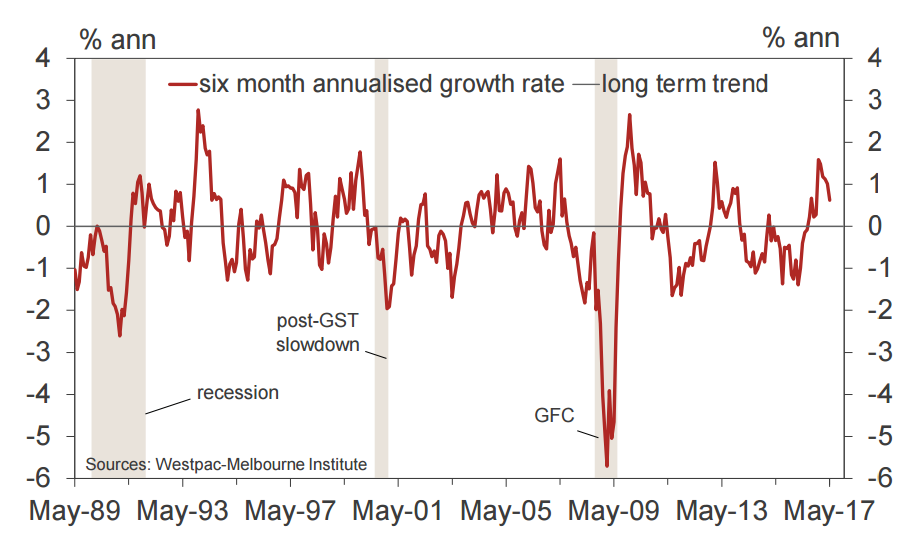

For the last ten months, Westpac-Melbourne Institute’s Leading Index (which indicates the likely pace of economic activity relative to trend) has returned a result above zero. This implies above-trend growth for the Australian economy. While the index dropped from a revised 1.01% in April to 0.62% in May, any number above zero implies Australia’s GDP growth in the next three to nine months will be higher than trend.

Trend growth was once taken to mean around 3% but recently the RBA and private sector economists have been suggesting it may mean 2.75%.

According to Westpac senior economist Matthew Hassan, commodity prices and the yield spread were behind the deterioration, although US industrial production provided some offset over the same period. Commodity prices had risen early in the last half of 2016 but then they fell between February and May, while the yield curve had flattened, a sign markets expect less growth and/or inflation.

20 June 2017

The minutes of the RBA’s June meeting were largely unchanged from those of the previous meeting in May which resulted in no change to official interest rates. As AMP Capital’s Shane Oliver put it, there was “nothing really new” in them. References to the labour market, house prices, household debt and wages were all highlighted as before. The acceleration of global growth was “continuing”.

Locally, “the transition to lower levels of mining investment following the mining investment boom was almost complete.” Forward-looking indicators of employment suggested “continued growth” and “a gradual erosion of the spare capacity in the labour market”.

Wage growth “was likely to remain” low for some time but wage growth and inflation “were expected to increase gradually” although there had been “isolated reports of localised and skills-specific labour shortages” forcing wages higher. However, on the whole, “low growth in incomes, along with high levels of household debt” were holding households back from spending.

There was one new area of interest. The RBA board referred to March quarter GDP/output growth several times; firstly as a blip on the path back to trend or above-trend growth and secondly, as one of the reasons for maintaining the current stance of monetary policy.

The RBA anticipated first quarter GDP figures would be weak (which they were) but it saw no need to lower the cash rate any further. Interest rates were already at a “low level” and monetary policy was already “accommodative”. However, the RBA is caught between a rock and a hard place as acknowledged near the end of the “Considerations for Monetary Policy” section.

“The Board continued to judge that developments in the labour and housing markets warranted careful monitoring.” The RBA is worried by the housing market, the level of household debt, wages, unemployment rates and how future household spending, or lack thereof, may feed into the economy. At the same time it appears to be hopeful the growth rate of the economy may rise back to trend levels and take care of some of its concerns.

20 June 2017

Argentina is back in the bond market spotlight this week, but not for any controversial reasons. It has joined the U.K, Ireland and Mexico as countries which have issued sovereign bonds which mature in 100 years or more.

The bonds are denominated in U.S. dollars and they were issued at a yield-to-maturity of 7.917% after reportedly receiving $9.75 billion worth of bids. Argentina’s bonds are well below investment-grade status and that is after Standard & Poor’s raised Argentina’s credit rating one notch in April from B- to B. However, indicative pricing on the USD$2.75 billion worth of bonds was at 8.25% and the value of bids suggests there was no shortage of demand.

Argentina has been a problematic sovereign bond issuers in its 200 year history. Its first bond default was in 1827, just 11 years as after it was founded in 1816 as a modern state. Its last bond default was in 2014, but that was a legal hangover from its default in 2001/2002. Depending on your definition of default, in that 200 years it has defaulted either seven or eight times. In other words, about every 25 years on average.

19 June 2017

Moody’s has announced it has cut the credit ratings of Australia’s four major banks as well as several regionals and former credit unions and building societies. The rationale behind the downgrades is macro-economic in nature and not particular to any one bank. That is, the downgrades are a function of Moody’s view of the Australian economy and what this may mean in future for banks operating within Australia. It was however relevant to institutions with mortgages on its books.

Moody’s was particularly concerned with low rates of wage growth and high levels of household debt associated with high dwelling prices. “Latent risks in the housing market have been rising in recent years, because significant house price appreciation in the core housing markets of Sydney and Melbourne has led to very high and rising household indebtedness.”

However, it is not a housing bust which concerns Moody’s. It is the effect on household spending should the unemployment rate or interest rates rise. Households with less savings and or more debt would be inclined to reduce expenditure as confidence levels fall. “The household sector’s resilience to weaker employment levels and/or rising interest rates has materially reduced.” In turn, a reduction in spending would flow to the rest of the economy and businesses and employees on the edge would topple over.

“Any increase in household sector stress would have the potential to weaken consumer confidence and consumption, creating negative second and third order impacts on overall economic activity and, accordingly, bank balance sheets.”

15 June 2017

The U.S. Fed’s Open Market Committee (FOMC) was expected to raise the federal funds rate range at its June meeting. It was also anticipated to have something to say about its holdings of Treasury bonds and asset-backed securities. It delivered on both items.

The U. S Fed announced it has raised its target range for the federal funds rate to 1.00%-1.25%. It would also begin to reduce re-investment of proceeds of matured bonds this year. “The Committee currently expects to begin implementing a balance sheet normalization program (sic) this year, provided that the economy evolves broadly as anticipated.”

While the exact timing has been left unstated, the amounts have been disclosed as starting at USD$6 billion (AUD$7.9 billion) Treasury bonds per month and USD$4 billion (AUD$5.3 billion) mortgage securities per month. Every 3 months the amounts will increase until they hit USD$30 billion and USD$20 billion respectively. To put his into perspective, the U.S Fed’s last quantitative easing programme, referred to as “QE3”, bought an additional USD$45 billion mortgage securities per month. Westpac estimate the run-down in holdings will take place over at least four years.

15 June 2017

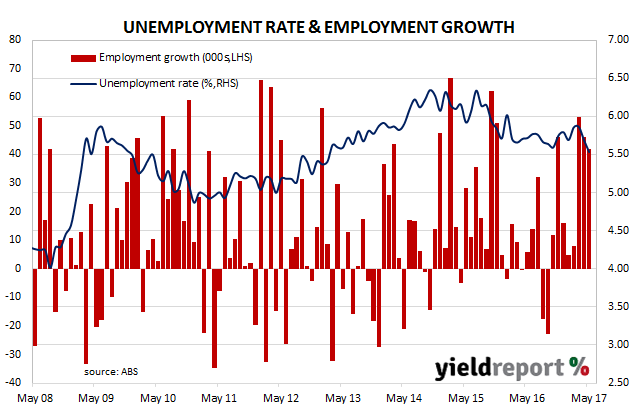

The growth in employment numbers forecast by various leading indicators seems to have finally appeared. Australia’s unemployment rate dropped in May and it was not because of a drop in the number of people counted in the labour force. The ABS released employment estimates which indicated Australia’s unemployment rate fell from 5.7% to 5.5% while the participation rate rose from 64.8% to 64.9%. The total number of people employed in Australia in either full-time or part-time work rose by 42,000 during the month, in contrast with the market’s expectation of +10,000. Total hours worked in May were 1.9% higher than April and 2.3% higher than a year ago.

For some years there have been concerns regarding the effect of the sampling process on labour force figures and these concerns are still present. According to NAB economist Tapas Strickland, “82% of [the] employment gains came from changes to the sample…” and he wonders whether there may be some reversal in next month’s figures. “[T]his could represent genuine improvement, but it also suggests some statistical payback is likely next month.”

Westpac economist Justin Smirk described the figures as a “solid” and he was impressed by some aspects of the report. “Further signs of the overall strength of this report was the 1.9% (over May) jump in hours worked taking the annual pace to 2.3% per year. This lift in hours worked was driven by a lift in both total employment and hours worked per person, 2.0% and 1.6% respectively.

However, he was surprised by the drop in the unemployment rate. “We had been looking for the unemployment rate to fall over the next few months but had not expected it to get to 5.5% so soon.” A glass half full approach would be to welcome the employment growth which produced such a result. A glass half empty approach would be to doubt the result. UBS economist George Tharenou was definitely in favour of the former approach. “Overall, employment remains very strong and clearly improved in recent months, with 2% year on year growth the best in over 2 years and now more consistent with the positive leading indicators. The unemployment rate has also surprisingly dropped to a cycle low of 5.5%. This supports the RBA’s positive outlook…and keeps rates on hold.”

15 June 2017

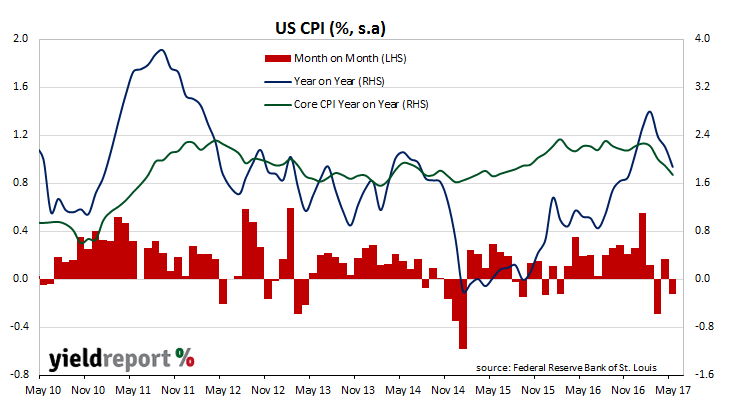

A 6.4% fall in petrol prices had driven the overall U.S. consumer inflation lower in May. Consumer price index (CPI) figures released by the Bureau of Labor Statistics indicated prices fell by 0.1% for the month, missing market expectations of a flat (0%) result. On a 12-month basis the CPI growth rate dropped back to 1.9% from April’s comparable figure of 2.2%.

A 6.4% fall in petrol prices had driven the overall U.S. consumer inflation lower in May. Consumer price index (CPI) figures released by the Bureau of Labor Statistics indicated prices fell by 0.1% for the month, missing market expectations of a flat (0%) result. On a 12-month basis the CPI growth rate dropped back to 1.9% from April’s comparable figure of 2.2%.

Core prices, a measure of prices which strips out food and energy price changes, rose by 0.1% for a second month in a row. Annualised core inflation dropped again for a third month in a row to 1.7% (seasonally adjusted) from April’s 1.9%. The figures were under market expectations of a 0.2% rise; prices fell in the clothing and new/used vehicles segments and certain non-food and non-energy commodity prices fell.

The CPI numbers were released on a busy day for economic reports and announcements. U.S. May retail sales data were released and the U.S. FOMC announced its new higher target range for the federal funds rate. On the day, U.S 2 year yields fell 4bps to 1.33%, U.S 10 year yields fell 8bps to 2.12% while the U.S. dollar was steady against the euro and sterling but weaker against the yen.

14 June 2017

The Queensland Government has released it 2017-18 budget and as a result Queensland Treasury Corporation (QTC) estimates it will borrow $6.8 billion in 2017-2018 which is about $2.7 billion less than forecast in QTC’s mid-year statement. QTC’s gross issuance was around $10.8 billion in 2016-2017.

Most of the borrowing will be done to finance existing debt worth $9.4 billion which will mature during the year. $600 million is expected to be needed for “other entities” such as universities, schools and water utilities. $3.2 billion has already been borrowed, either in 2016-2017 or earlier years which leaves a net $6.8 billion.

QTC’s benchmark series will form the bulk of the bonds which will be issued but QTC also flagged the potential for green bonds, bond with maturities as long as 30 years and other types of debt securities.