09 June 2017

The continued growth in the popularity of ETFs as a low cost investment amongst investors has seen a flurry of listing activity in recent weeks, particularly in the income space.

This week saw three more funds listed on the ASX with the listing of the BetaShares Australian Bank Senior Floating Rate Bond ETF (ASX: QPON), and Blackrock’s iShares Core Cash ETF (ASX: BILL) and iShares Enhanced Cash ETF (ASX: ISEC).

BetaShares’ Australian Bank Senior Floating Rate Bond ETF is the first ETF in Australia to offer exposure to a diversified portfolio of floating rate bonds issued by banks. The fund aims to provide income paid monthly. QPON invests at least 80% of its assets in floating rate bonds issued by the big four Australian banks and up to 20% in bonds issued by the six ‘regional’ banks, including Macquarie Bank. The fund will hold a maximum of 14 securities from up to 10 issuers.

Commenting on the launch of the fund, BetaShares Managing Director, Alex Vynokur, said: “In the current environment of historically low interest rates, we believe the case for investing in floating rate bonds is very compelling. In the US, the Federal Reserve has raised interest rates twice in the past six months in the effort to return monetary policy to a more normal footing. In Australia, the last increase in the cash rate by the Reserve Bank was in November 2010, while the current cash rate is at historic lows.”

The fund’s investment objective is to provide an investment return that aims to track the performance of the Solactive Australian Bank Senior Floating Rate Bond Index, before taking into account fees and expenses. The fund will have an ongoing management cost of 0.22% p.a. and distributions will be made monthly.

Meanwhile, BlackRock has launched two income focused ETFs which will be benchmarked to the S&P/ASX Bank Bill Index.

The iShares Core Cash ETF will invest in cash deposits and negotiable certificates of deposit (NCDs), with the majority with the four major Australian banks. The fund can also invest in treasury notes and commercial paper issued by the Australian Government and other semi-government entities.

The iShares Enhanced Cash ETF will have a slightly riskier investment profile. It can invest in cash deposits and NCDs, with the majority being with the four major Australian banks. The fund can also invest in treasury notes and commercial paper issued by the Australian Government and other semi-government entities, corporate issued commercial paper and corporate issued fixed or floating rate notes. The fund can invest up to a maximum of 20% in FRNs and limits are placed on any individual security exposure, credit rating exposure and maturity (maximum FRN maturity of 5 years).

Both iShares funds will not invest in any deposits that have issuer-imposed repayment restrictions (e.g. term deposits). The ongoing management cost of the iShares Core Cash ETF is 0.07% p.a., while the cost of the iShares Enhanced Cash ETF is 0.12% p.a. For both funds distributions will be made monthly.

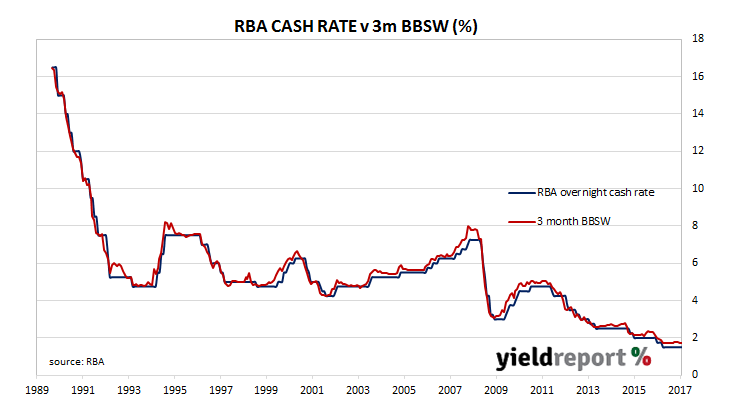

The index for both iShares funds consists of synthetic “securities” that cannot be purchased and sold. The constituents of the index are a series of 13 hypothetical weekly bills, ranging from one week to 91 days in maturity that are interpolated using the 24 hour cash rate and the 30 day, 60 day and 90 day bank bill swap rates (BBSW). Given the synthetic nature of the index, a full replication (or optimisation) passive investment strategy is not possible. Instead, BlackRock will construct a portfolio with consideration to the liquidity, average maturity, credit and interest rate characteristics of the index.

You can find a full list of ASX listed cash and fixed interest ETFs here.