01 June 2017

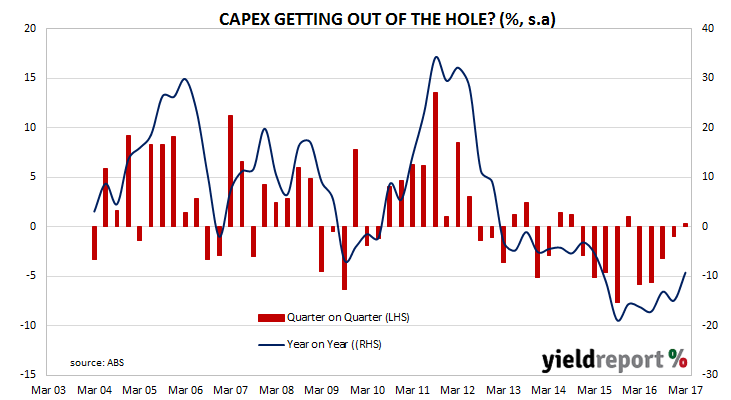

First quarter private capital expenditure (capex) figures have now been released by the ABS and the +0.3% quarter-on-quarter figure was in line with market expectations. Year on year, capex was 9.3% lower, as mining investment falls back to more normal levels after the mining investment spike of 2011/2012.

The Aussie dropped by about 0.25 US cents immediately after the figures were released and then finished another 0.25 cents lower at around 73.75 U.S. cents. Both 3 year and 10 year bond yields had edged up 1bps to 1.68% and 2.43% respectively but retail sales figures were released simultaneously and thus the markets’ reactions to either report is somewhat clouded.

The reception the figures received was on a scale ranging from vaguely positive to quite negative. NAB economist Tapas Strickland had one of the more negative views. “The non-mining investment outlook for 2017/18 failed to lift further, while flat equipment investment in the quarter presents downside risks to Q1 GDP…The lack of a lift in the non-mining components of the survey will be discouraging for the RBA, which has been patiently awaiting a lift in non-mining investment intentions in the data.” The team at ANZ Research shared his sentiment. “Importantly, spending on plant and equipment, which feeds into next week’s Q1 GDP, fell 0.1%. This is much softer than our expectation of moderate growth. As such it poses downside risk to our already soft pick for Q1 GDP.”

CBA senior economist Gareth Aird provided one of the few (slightly) positive views out there. “The NAB Business Survey continues to suggest a lift in investment is forthcoming. But we think the softness in consumer demand is holding investment back. Fortunately there is a decent amount of public capex to come because the outlook for private investment remains weak.”

01 June 2017

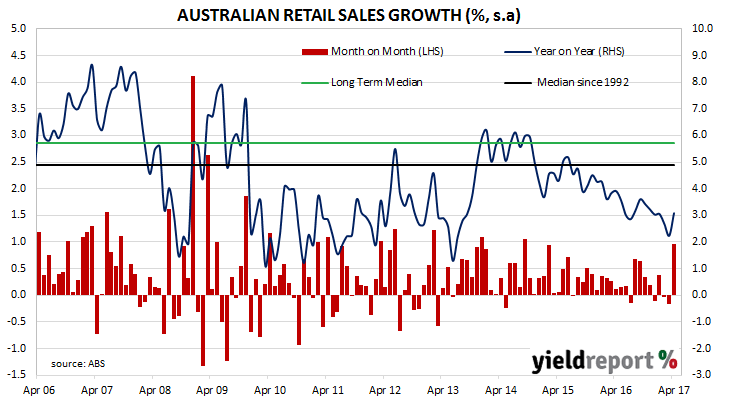

Australian consumers have shrugged off their aversion to spending or, at least temporarily, according to April retail sales figures released by the ABS. Part of the rebound was related to a bounce in spending in Queensland after Cyclone Debbie while some of it came from higher fresh fruit and vegetable prices which was also Debbie-related. Sales grew by 1.0% over the month, which is well over the +0.3% growth expected and a reversal of declining sales in February and March. On a year-on-year basis, sales grew by 3.1%, which is a return to January’s annual rate after February and March annual figures fell towards 2%.

Westpac senior economist Matthew Hassan points to Queensland as providing the impetus for the rebound. “Retail sales came in better than expected for April with a stronger post-cyclone rebound in Queenland and some solid gains across other states. Overall the result is considerably better than feared, confirming temporary impacts from weather events were a factor in March and suggesting underlying conditions have improved somewhat.”

31 May 2017

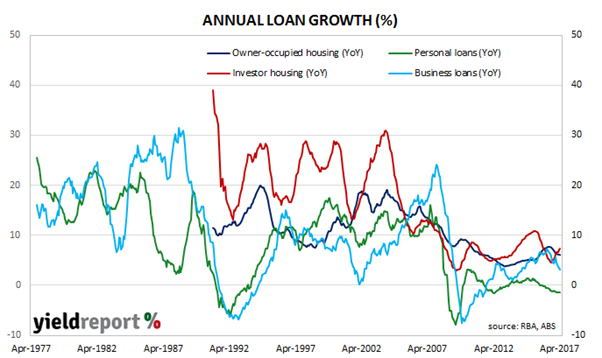

Loans to the private sector grew at a slightly lower rate in April, driven by a slowdown in lending to “owner-occupiers” and the business sector. Figures released by the RBA indicate total private credit growth in April was 0.4%, in line with expectations and at the same rate as in March. However, total credit growth for the last 12 months was 4.9%, down from the 5.0% growth rate recorded for March.

Growth in personal loans continued to fall and lending in this segment is 1.5% lower than a year ago. Since October 2008, Australians have been generally reluctant to take on additional personal debt, which is in stark contrast with their views on housing loans. Investor loans grew by 7.3% year on year, up from March’s comparable figure of 7.1%, while owner-occupier loan growth slipped from 6.2% in March to 6.1% in April. ANZ senior economist Daniel Gradwell contrasted households’ views on personal debt with their views on mortgages. “It’s interesting to note that the stock of personal credit is now 5% below the pre-GFC peak in February 2008. On the other hand, housing credit has increased nearly 80% over the same period. Australian households have added significant to their total debt levels since the GFC, entirely driven by housing.”

31 May 2017

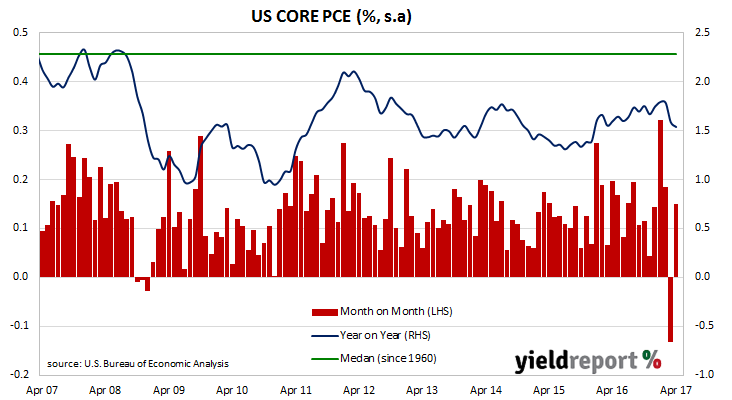

One of the US Fed’s favoured measures of inflation is core personal consumption expenditure (PCE). The core version of consumer spending strips out energy and food components, which are volatile from month to month, in an attempt to identify the prevailing trend. It’s not the only measure of inflation used; the Fed also tracks the consumer price index (CPI) and producer price index (PPI) from the Department of Labor.

The latest core PCE figures have been published by the Bureau of Economic Analysis as part of April figures for personal income and expenditures. On a month-on-month basis, core PCE rose by +0.2%, which is up from March’s figure of -0.1%. However, the year-on-year figure of +1.5% is down on March’s comparable figure of +1.6%.

25 May 2017

Not only is there a good chance the U.S will raise its official rate next month for the second time this year, there now seems to be a hardening of the view the beginning of the end of bond purchases by the U.S Fed is not far away.

According to the Federal Open Market Committee (FOMC) minutes of May’s meeting “Policymakers agreed that the Committee’s Policy Normalization Principles and Plans should be augmented soon to provide additional details about the operational plan to reduce the Federal Reserve’s securities holdings over time.” In other words, the FOMC will state its plan and timetable for reducing its bond purchases soon.

ANZ’s Martin Whetton said the use of the word “soon” indicated June this year. However, he thought the Fed had given themselves an out in the minutes. He said the minutes stated “ ‘it would be prudent’ to wait for evidence that a recent slowdown in economic activity had been transitory. The Fed also said it would look for a gradual, predictable way to unwind its balance sheet…”

Westpac’s Imre Speizer thought “soon” was not quite that soon and it had to be in the context of further rate rises. “A June hike still seems to be on the table, but the outlook beyond is slightly more uncertain given the potential for balance sheet shrinkage to start in late 2017.”

Bond yields fell on the day. The yield on U.S. 2 year bonds finished down 2bps at 1.28% while 10 year bonds fell 3bps to 2.25%.

24 May 2017

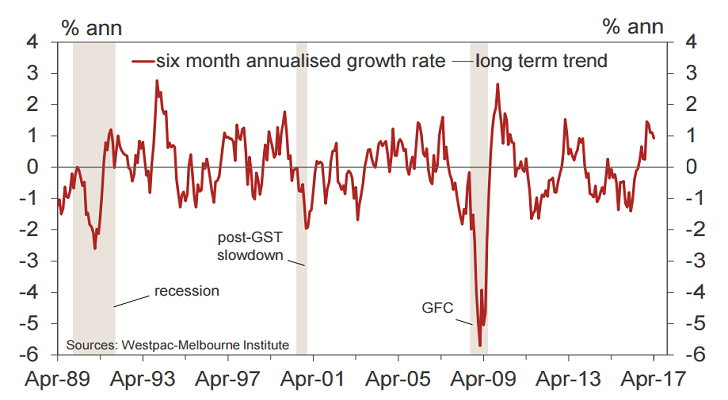

For the ninth month in a row, the Westpac-Melbourne Institute’s Leading Index has returned a result above zero. This implies above-trend growth for the Australian economy. While the index dropped from 1.11% In March to 0.92% in April, any number above zero implies Australia’s GDP growth in the next three to nine months will be higher than trend. Trend growth was once taken to mean around 3% but recently the RBA and private sector economists have been suggesting it may mean 2.75%.

In the May Statement on Monetary Policy, the RBA’s latest forecast for GDP growth in calendar 2017 was in the range 2.5%-3.5%, or 3% if using the midpoint. Westpac‘s chief economist Bill Evans is in broad agreement with the RBA’s 2017 forecast. “Westpac concurs with the Bank’s forecast of 3% growth through 2017. That is above trend and consistent with the positive leads from the Index over the last nine months.” However, the RBA forecast 3.25% growth in 2018, whereas the Westpac economist expects economic growth to slow. He expects house construction and export growth to fall back while the prices of exports are also likely to fall in his view. As such, Westpac expects official rates to be hold though 2017 and into 2018.

22 May 2017

Increased private sector debt and higher residential property prices have led S&P to cut the ratings on over twenty Australian banks and building societies. The one notch downgrade is the result of what S&P described as “an increased risk of a sharp correction in property prices” after years of debt-fueled property investment. S&P says if such a price drop were to occur, “all financial institutions operating in Australia are likely to incur significantly greater credit losses than at present.”

The ratings downgrades have been largely restricted to financial institutions outside of the four major banks and Macquarie, although these banks remain on “negative outlook”. The rationale is the major banks can expect “timely financial support” from the Australian government should it be required, whereas other banks may not be deemed important enough to save should loan losses wipe out their capital.

Not all banks outside the majors and Macquarie were downgraded. S&P says the parent companies of Suncorp-Metway and QT Mutual Bank Ltd would be likely to provide support, as would the parent companies of a swag of foreign-owned banks such as ING Bank, Citigroup and HSBC.

While S&P thinks potential problems arising from the Australian property market are worth a downgrade, it also thinks Australian financial institutions operating in the mortgage market face conditions which are “relatively benign by global standards.” S&P thinks recent actions by APRA should assist an orderly unwinding of high levels of debt as it forecasts property price growth to slow or for prices to fall mildly. S&P points to previous cycles in Australia in which this has occurred without any significant losses.

Lower ratings will increase the banks’ cost of funding and early estimates of the cost increases range from 5bps to 15bps per annum. These higher costs will not immediately feed through as banks raise funds over time and it is only the cost of each new dollar which will be affected. However, whatever advantage was granted by the Federal Government’s 6bps bank levy is set to disappear.

18 May 2017

Australia’s latest employment figures appear to be good on the surface but the reaction among economists has not been unanimous. The ABS released employment estimates which indicated Australia’s unemployment rate fell from 5.9% to 5.7% in April. In some months the unemployment rate can drop purely because the participation rate falls. On this occasion, the participation rate was steady at 64.8 and the total number of people employed in Australia in either full-time or part-time work rose by 39,700, well above the market’s expectation of +5,000. However, despite more people working, total hours worked fell by 0.3% over the month, although over a 12 month period this figure grew by 1.3%, which is higher than the comparable figure from March (+0.7%).

Economists were mixed in their reactions to the figures. Andrew Hanlan, a senior economist at Westpac said “considerable” labour market slack exists and there would be little pressure for wages to increase. He also does not expect this rate of growth in employment numbers to continue. “Looking further ahead, in 2018, we expect the labour market to cool – as home building activity turns down and as China slows and commodity prices retreat further.” NAB senior economist David de Garis was more positive; he saw the figures as “another slice of evidence that the softness in the reported employment data is dissipating and importantly is catching up to more positive forward-looking indicators of the labour market.” He also thought employment numbers would continue to grow. “Looking forward, leading indicators of the labour market remain positive and the NAB Business Survey is suggesting employment growth averaging around 20,000 a month – enough to put downward pressure on the unemployment rate.” ANZ’s view was a little more circumspect than the NAB economist but still positive. David Plank, ANZ’s chief of Australian Economics said, ”Given the strength of labour market indicators from sources such as business confidence and ANZ Job Ads we are not overly surprised by the strength of the April jobs report, even if it was above our forecast. We think this could continue for a while yet, hopefully stemming the trend decline in consumer confidence seen since the start of the year.”

Bond yields were mixed in their reaction on the day. 3 year yields rose 1bp to 1.79% while 10 year yields fell 3bps to finish at 2.53% and the Aussie eased about 0.1 US cents to 74.20 U.S. cents.

18 May 2017

The rating agency is of the view that the recent budget announcements are a path to fiscal balance, however, additional restrictive measures are still required. Of particular concern was their view of the potential for wage growth and inflation to remain on the low side, with downside risk to the government’s current projections of achieving surplus by 2021.

According to Standard & Poor’s, Australia’s international investment position remains a major weakness in the sovereign credit profile. At 246% of current account receipts, Australia’s net external liabilities are the second largest among all investment-grade rated sovereigns, just behind the U.S. This weak external position is a result of decades of sizeable current account deficits, financed in part by external borrowing. While the level of debt was seen as a problem overall, the agency expects Australia’s external borrowers to maintain easy access to foreign funding.

The agency view’s Australia’s economic growth as sound. It estimates headline GDP growth to be around 2.3% in 2017 and expects the growth rate to rise to around its potential growth rate in the following years. The agency’s credit outlook has been negative since July 2016.

18 May 2017

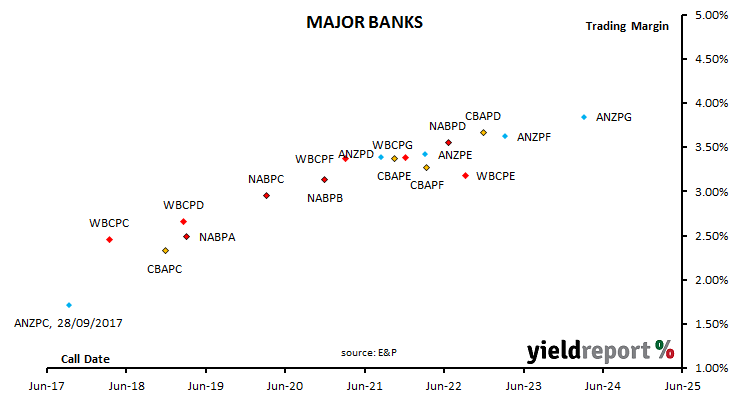

Evans and Partners Michael Saba thinks some of Westpac’s hybrids stand out. He pointed to Westpac Capital Notes 3 (ASX code: WBCPF) as having a similar trading margin to Westpac Capital Notes 4 (ASX code: WBCPG) and more than Westpac Capital Notes 2 (ASX code: WBCPE) with less maturity risk (that is, less time to maturity). He also thinks investors interested in short-term investment may want to check out Westpac CPS (ASX code: WBCPC).

As at the close of business 18 May 2017