11 April 2017

SEEK Ltd, the well-known employment website business, had made its bond market debut with the issue of $175 million worth of floating rate notes. Initially only $100 million had been sought but the issue was upsized after “strong support from investors”, according to the company’s chief financial officer Geoff Roberts. He also noted how the note issue would diversify SEEK’s sources of finance and extend the company’s average debt tenor.

Interest is payable at 3 month BBSW +230bps which, at the current BBSW rate of 1.78%, is equivalent to 4.08%. The notes will mature in 2022 and rank equally with SEEK’s existing senior unsecured debt.

SEEK’s senior debt is unrated by the ratings agencies such S&P Global Ratings, Moody’s Investor Services or Fitch Ratings. This issue is another in what appears to be a growing trend in Australia for corporates without credit ratings to access local debt markets. IMF Bentham, StockCo, Qube, TFS, CML Group, Capitol Health and Healthscope have all issued bonds within the last twelve months and none of them have credit ratings.

While this issue is SEEK’s debut debt security, it is not SEEK’s first attempt. In June 2012, SEEK sought to raise $125 million and it had even made available a prospectus to issue fixed-rate five year subordinated notes which were to be listed on the ASX. The issue was subsequently benched just over one week later when SEEK released a statement to the ASX which stated “it would not achieve acceptable terms.”

At the end of June 2016, $826.9 million of SEEK’s total available facilities of $1138 million had been drawn down but by 31 December 2016, this had risen to $893.8 million out of $1131.3 million.

10 April 2017

The period between the day on which an investor pays for a new issue of securities and the day on which trading commences can be a harrowing one. In this intervening period, nothing can be done. A contract has been made, securities allocated and yet the investor cannot dispose of the investment until trading begins. Not that investors typically choose to do so, but not having the option can be worrying when markets are volatile.

After weeks of waiting, Challenger Notes (ASX code: CGFPB) began trading on a deferred delivery basis on the ASX this week, with the opening trade going through at $101.20. The notes finished the day at $100.95, a small premium to their $100 face value. They have a call date on 22 May 2023 and an issue margin of 4.40% above BBSW which provides an initial yield around 6.185%. Normal trading is expected to begin on 13 April 2017.

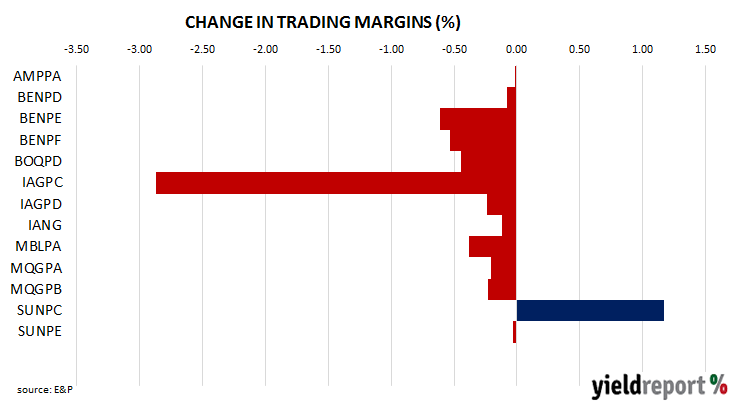

Since the issue was announced at the end of February, margins on ASX listed notes have fallen. The median trading margin has moved from 3.67% on the day of the announcement to 3.41% on the day trading commenced. The diagram below shows how trading margins of non-major bank hybrids fared over that period. Suncorp CPS 2 (ASX code: SUNPC) and Insurance Australia CPS 2 (ASX code: IAGPC) should be ignored as both securities mature in 2017 and small price changes have resulted in large changes to their respective trading margins.

07 April 2017

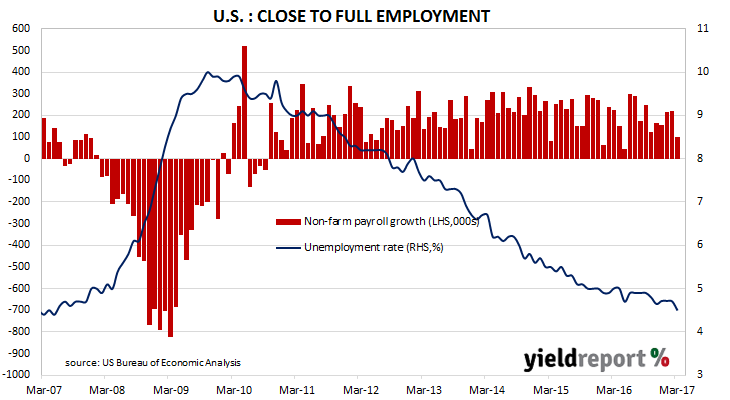

The U.S. unemployment rate is now at the lowest it has been since May 2007. The latest U.S. employment figures for March were less than expected but the U.S. economy appears to be creating jobs at a pace which exceeds population growth. According to the U.S. Bureau of Labor Statistics, only 98,000 jobs were created in the non-farm sector in March against expectations of 180,000. Poor winter weather and a shift to online retailing has been put forward as the cause of the lower-than-expected number of jobs created.

After revisions to previous months’ figures, the unemployment rate fell from 4.7% to 4.5% as the participation rate remained steady at 63.0% and the employment-to-population ratio rose 0.1% to 60.1%. The U.S. has not had a negative employment growth figure since September 2010 or 78 months and these latest figures will provide ongoing pressure for higher official interest rates.

ANZ described the report as “it’s not all bad” while AxiTrader’s Greg McKenna pointed out the increasing difficulty of creating 200,000 jobs when an economy is at, or close to, full employment.

Market reaction was mild but economic data releases were overshadowed by the fallout from U.S. strikes against a Syrian airbase. US 2 year and 10 year bond yields both rose 4bps to 1.28% and 2.38% respectively.

06 April 2017

Back in mid-March, the Federal Reserve raised the U.S. official interest rate, otherwise known as the federal funds rate, by 0.25%. Although a rise had not really been expected until a couple of weeks before the meeting, when the decision came no one was surprised, as a procession of Fed officials had made it very clear a rate rise was very, very likely.

The minutes of this meeting have now been released and they have raised the spectre of the US Fed finally reversing the massive increase it oversaw in its balance sheet since 2009. Prior to the GFC, the U.S. Fed had around USD$850 billion of assets. As of March 2017, the Fed’s balance sheet was around USD$4500 billion, the result of years of buying US Treasury bonds and mortgage-backed securities.

The Fed would accomplish this reduction not by selling these assets, but by simply letting them mature and not buying any more. These assets are interest-bearing securities and they will be redeemed on their maturity dates. “In particular, participants agreed that reductions in the Federal Reserve’s securities holdings should be gradual and predictable, and accomplished primarily by phasing out reinvestments of principal received from those holdings.” The Fed hopes this path will avoid financial market volatility experienced in the past when discussions of “tapering” had emerged.

There was also confirmation of how the U.S. Fed views the Trump Administrations plans. “…most participants continued to view the prospect of more expansionary fiscal policies as an upside risk to their economic forecasts.” In other words, the “participants”, otherwise known as senior Fed officials including chair Janet Yellen, acknowledge their forecasts for economic growth and inflation may be on the conservative side and in need of adjustment.

06 April 2017

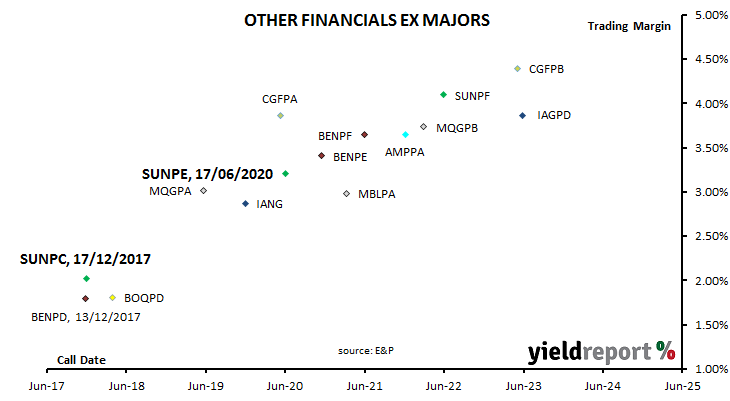

Evans and Partners’ Head of Income Products, Michael Saba, is suggesting those who are interested in short term investments look at Suncorp CPS 2 (ASX code: SUNPC). He thinks Suncorp’s recent $300 million issue of new capital notes may have caused holders of Suncorp’s other ASX-listed hybrids to sell them in order to fund the new notes. “Subsequently margins have widened on two of the listed Suncorp securities. As shown below, the margins for SUNPC and SUNPD have risen this week, possibly as investors fund the new issue via the old.”

04 April 2017

The March RBA meeting is not one of the four months of the year in which most rate changes have been historically made and for that reason alone no one expected anything to happen. Aside from this historical observation, reasons for a rate change in one direction were balanced by reasons for a move in the other direction.

The main points to come from the statement which accompanied the March meeting were somewhat contradictory in what they mean for future RBA action. “Core inflation remains low” is a tick in favour of keeping the cash rate at historically low levels. “The various forward-looking indicators still point to continued growth in employment over the period ahead” is a tick in favour of raising the cash rate positive back to “normal” levels. “Growth in household borrowing, largely to purchase housing, continues to outpace growth in household income” is a tick in favour of higher rates in order to pressure borrowers to be more conservative with their borrowings.

According to economists, there were two things which plainly stood out and each has direct bearing on Australia’s official cash rate. As Westpac’s Bill Evans put it “the commentary around the domestic economy is somewhat less upbeat” and “considerable attention is given to the housing market.”

Most economists touched on one of these points or both of them. Here’s what a few of them had to say.

Bill Evans, Westpac

“We do expect that macro prudential and banks’ self-regulatory policies will be successful in taking most of the heat out of the housing market over the course of the remainder of this year. Even though spare capacity is expected to persist in the labour market and low wage and inflation conditions remain the Bank will not opt for further policy easing given the risks of reigniting house prices.”

Felicity Emmett, ANZ

“Changes to the RBA’s statement were concentrated around the housing market commentary, highlighting the Bank’s concerns about financial stability. The measures announced by APRA last week are expected to help at the margin, but the Bank is clearly concerned about the risks from rising household debt…“We continue to see rates on hold at 1.5% for an extended period, with concerns around persistently low inflation offset by the strength in the housing market.”

Gareth Aird, Commonwealth Bank

The most interesting feature in the governor’s statement today was the second last paragraph, which was new. The entire paragraph was devoted to a discussion on lending for housing. Lowe’s comments come in the wake of APRA’s additional supervisory measures, announced last Friday, to address risks that continue to build within the mortgage lending market. At the margin, the changes should cool investor‑related demand for housing, but not sufficiently so to put a rate cut back on the table.

03 April 2017

The Australian Prudential Regulation Authority (APRA) has announced additional supervisory measures aimed at moderating the growth of investor lending in particular. APRA has written to all banks and other approved deposit taking institutions (ADIs) setting out its expectations for mortgage lending going forward which in summary includes:

- limit new interest-only lending to 30% of total new residential mortgage lending with strict limits where the loan to valuation ratio (LVR) is above 80%

- manage lending to investors to comfortably remain below the previously advised benchmark of 10% growth

- ensuring that loan serviceability metrics (including interest rate and net income buffers) are set at appropriate levels for current conditions

- a continued restraint on lending growth in higher risk segments (e.g. high loan-to-income loans, high LVR loans, and loans for very long terms).

APRA has indicated that it is likely to impose additional requirements on an ADI if the proportion of new lending on interest-only terms exceeds 30% of total new mortgage lending. In the case where an ADI operates above the 10% growth benchmark for investor lending, APRA has indicated that such a breach will prompt an immediate review of the adequacy of the ADI’s capital requirements.

The latest APRA review and focus is undoubtedly aimed at curbing bank and ADI lending for investment purposes. What we can expect to see is a further tightening in the supply of new lending in these sectors from traditional bank and ADI lenders. This may come in the form of imposing additional requirements on borrowers or refusing to lend outright due to its (the bank’s) internal constraints.

This of course doesn’t necessarily mean that loans being “rejected” by banks and ADIs are necessarily inferior. Rather, the current operating environment (i.e. regulatory environment) of traditional lenders such as banks makes potentially less economically viable, particularly if (for example) a bank’s capital requirements are increased.

03 April 2017

The Melbourne Institute’s Inflation Gauge is an attempt to replicate the ABS consumer price index (CPI) on a monthly basis instead of a quarterly one. It has turned out to be a reliable leading indicator of the CPI, although there are periods in which the Inflation Gauge series has diverged, only to return back to similar levels as the official CPI series.

During March, the Inflation Gauge rose by 0.1% and by 2.2% over the last 12 months. February’s comparable figures were -0.3% and 2.1%.

February retail sales and ANZ job advertisement figures were also released on the same day so it is difficult to state if these inflation figures had any real effect on financial markets. The fact the month-on-month change was small but positive probably means bond and currency markets took little notice of them. Yields on 3 year bonds and 10 year bonds were both 2bps lower at 1.93% and 2.71% respectively on the day.

03 April 2017

ANZ’s job advertisement survey is well-known as a leading indicator of employment numbers. It reflects changes in demand for labour and provides another measure of activity in the economy. Figures for March have been released and, after revisions, total advertisements were 0.3% higher for the month (previously -0.8%) and 7.0% higher for the year (previously 6.9%).

David Plank, ANZ’s Head of Australian Economics, said the figures were inconsistent with recent employment data. The unemployment rate fell from 5.7% in January to 5.9% in February but this latest survey suggests conditions in Australia’s labour market may be quite robust. He said, “While somewhat at odds with recent employment data, the improvement in job ads is consistent with other forward indicators such as our Labour Market Conditions Index and solid business conditions. As such, we continue to expect a gradual improvement in labour market conditions through 2017.”

03 April 2017

Australian consumers are not confident about their finances, while competition among retailers is hotting up and driving prices lower. That’s the conclusion economists are drawing from the latest batch of retail sales figures released by the Australian Bureau of Statistics.

Sales figures shrank by 0.1% over the month or 2.7% for the 12 months to the end of February. These numbers were less than market expectations of 0.3% for the month and they do not compare favourably with January’s figures of 0.4% (month) and 3.1% (year).

Jo Masters, senior economist at ANZ said, “Consumer confidence around personal finances has slipped in recent months and together with intense competition suggests that retail sales may remain lacklustre for some time.”

Westpac economist Matthew Hassan thinks the figures also gave clues about consumers’ current priorities. “Indeed whereas basic food retail sales were up 0.3%, non-food retail as a whole was down 0.4%. That pattern is a signature sign of consumer belt-tightening with discretionary spend reined in and “switching” giving support to staples.” He also referred to “particularly weak” sales of clothing, footwear and furniture.