31 March 2017

Growth in private sector credit is a measure of confidence. The granting of credit, or new loans to businesses and individuals, is a measure of confidence on the part of business and individuals to borrow and confidence on the part of banks and investors to lend. Typically growth rates for new loans are low, or negative in a recession and high in a boom.

Borrowing can be split into three types. There is borrowing for investment purposes, which increases an economy’s capacity to produce goods and services. There is also borrowing for consumption, which brings forward spending from the future to spending in the present. Then there is borrowing to buy a dwelling, either to live in or to rent.

The latest figures from the RBA show total loan growth was 0.3% in February, lower than the 0.5% which was expected but higher than January’s 0.2%. Compared to February 2016, the value of loans was 5.0% higher.

31 March 2017

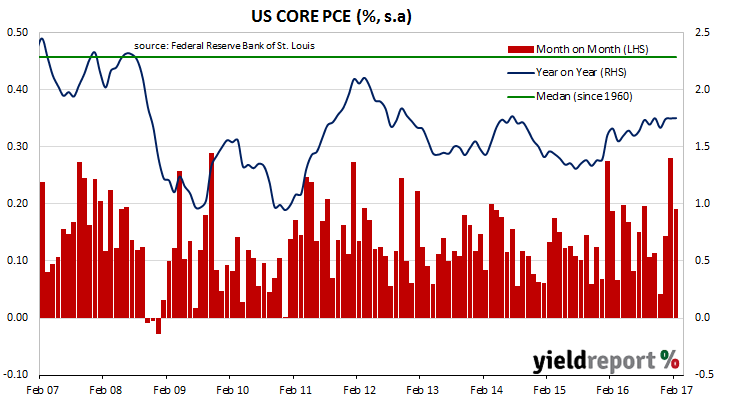

One of the US Fed’s favoured measures of inflation is core personal consumption expenditure (PCE). The core version of consumer spending strips out energy and food components, which are volatile from month to month, in an attempt to identify the prevailing trend. It’s not the only measure of inflation used; the Fed also tracks the Consumer Price Index (CPI) and Producer Price Index (PPI) from the Department of Labor.

The latest core PCE figures have been published by the Bureau of Economic Analysis as part of February figures for personal income and expenditures. Seasonally adjusted, personal expenditure rose by 0.2% for the month, compared to January’s revised figure of 0.3%. On an annual basis, core PCE rose by 1.8% which is the same as January’s figure. The numbers were in line with market expectations of 0.2% and 1.7% respectively.

27 March 2017

Villa World has announced the margin on its Villa World Bonds (ASX code: VLWHA) offering after the bookbuild was closed early due to what the company described as “strong demand”. As expected, it was at the bottom of the 5.75%-5.00% indicative range. When this margin is added to the current 3 month bank bill swap rate (BBSW) of 1.795%, investors can expect around 6.55% annualised for the first quarter and thereafter if BBSW rates do not alter materially. BBSW is typically at a fairly small margin to the RBA’s official cash rate which is currently 1.50%.

The chart below shows the trading margins of existing notes which are already listed on the ASX. In very simplified terms, a security’s trading margin is the sum of its annualised distributions as percentage of its price less BBSW. (In practice, unrealised annual capital gains/losses and accrued distributions are also taken into account.)

27 March 2017

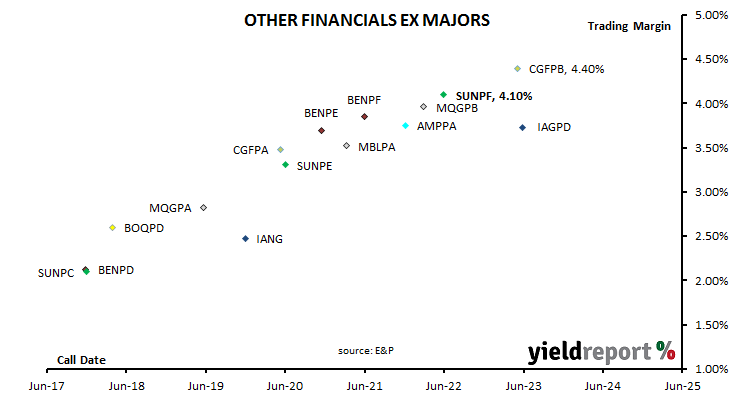

Just one day after Suncorp announced it would be issuing a new series of ASX-listed hybrids, it has announced the margin on its new capital notes (ASX code: SUNPF). The company had initially sought to raise $250 million, an amount brokers described as on the small side but after Suncorp received additional demand for the hybrids, the book-build was closed earlier than scheduled and the company allocated $300 million under the broker firm and institutional offers. The final size of the issue will depend on the amount allocated under the eligible security-holder offer.

It has been some years since a margin was set not at the bottom of an issue’s indicative range and Suncorp did not upset this pattern. The indicative range was 4.10%-4.30% and hence the margin was set at 4.10%. When this margin is added to the current 3 month bank bill swap rate (BBSW) of 1.80%, investors can expect around 5.90% annualised, inclusive of franking credits, for the first quarter and thereafter if BBSW rates do not alter materially. BBSW is typically at a fairly small margin to the RBA’s official cash rate which is currently 1.50%.

The chart below shows the trading margins of existing hybrids which are already listed on the ASX. In very simplified terms, a security’s trading margin is the sum of its annualised distributions as percentage of its price less BBSW. (In practice, unrealised annual capital gains/losses and accrued distributions are also taken into account.)

As at the close of business 27 March 2017.

22 March 2017

Australian GDP growth is likely to be above 2.75% for calendar year 2017.We are only two months into the year but if the Westpac-Melbourne Institute’s Leading Index maintains its record of being a reliable indicator of the Australian economy’s growth rate over the next three to nine months, GDP growth is likely to be around 3% or higher.

Although the index fell from 1.34% in January to 1.08% in February, this latest reading still suggests the Australian economy is likely to grow above the trend growth rate for most, if not all, of 2017. Trend growth was once taken to mean around 3% but recently the RBA and private sector economists have been suggesting it may mean 2.75%.

The index switched to positive in mid-2016 after fifteen months of negative readings. Westpac chief economist Bill Evans said the index had forecast weakness in the Australian economy through the middle of 2016 and therefore this recent run of positive monthly figures suggests 2017 GDP should be robust. “The latest reads point to above trend momentum carrying through the middle of 2017 consistent with Westpac’s forecast for 3% growth for the full year.”

21 March 2017

The March meeting of the RBA held near the beginning of the month left the overnight cash rate steady at 1.50%, as expected. Historically, RBA meetings in March have been uneventful as rate changes are typically made in February, May, August and November after quarterly CPI figures have been released. However, the minutes from such meetings provide clues with regards to the RBA’s state of mind and where their focus is likely to be in coming months.

The minutes from the March meeting indicated the RBA board focussed on several issues. Most of these issues are positive in the sense they are symptomatic of economic growth both locally and offshore. For instance, the minutes referred to a higher rate of global inflation, improved terms of trade and how September quarter GDP weakness was temporary.

On the other hand, one vaguely negative aspect was a labour market which “remained difficult to assess” and where “spare capacity remained.” Another clearly negative aspect was the reference to the “build-up of risks associated with the housing market.” The last two interest rate cuts appear to have spurred local house price higher and the RBA would be aware of this, leaving them with little inclination to cut rates further for fear of inducing a full-on bubble. As J P Morgan’s Sally Auld put it, “…the explicit commentary on risks around the housing market – against a backdrop in which the soft underbelly to the labour market is becoming more evident – make the case for further macro-prudential regulations more pressing.”

Matthew Hassan, Westpac senior economist, thought the RBA focussed more on the negative than the positive in an overall sense. “Although the central view is still constructive on global and local growth prospects, the commentary placed more emphasis on weaknesses in labour markets and household incomes, tending to downplay the potential boosts from rising commodity prices. The commentary also sounded a touch more urgent around risks in the housing market.”

The release of the minutes had little or no effect on financial markets. Prices in cash markets barely changed, indicating the odds of rate changes in 2017 and 2018 remained largely the same. Yields on 3 year bonds and 10 year bond yields were 1-2bps lower at 2.04% and 2.85%. The full text of the minutes can be found here.

21 March 2017

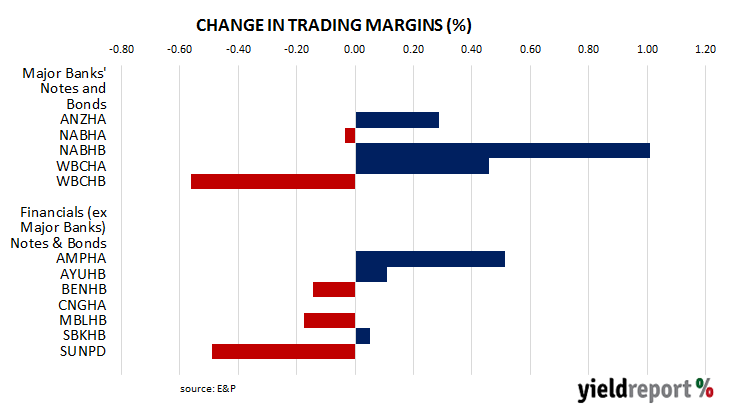

National Australia Bank Subordinated Notes 2 (ASX code: NABPE) began trading on a deferred delivery basis on the ASX this week. The first trade was at $100.80 and the notes finished the day at $100.50, a small premium to their $100 face value. They have a first call date of 20 September 2023, a final maturity date of 20 September 2028 and an issue margin of 2.20% above BBSW (an initial yield just under 4.00%). Normal trading is expected to begin on 27 March.

Since the issue was announced at the beginning of February, margins on ASX listed notes have fallen with the median trading margin moving from 1.71% on the day of the announcement to 1.62% on the day before trading commenced. The diagram below shows how notes of banks and other financial institutions have fared over that period. Perhaps it is not coincidental NAB subordinated Notes 1 have performed the worst of this type of security and its trading margin has risen by the largest amount.

21 March 2017

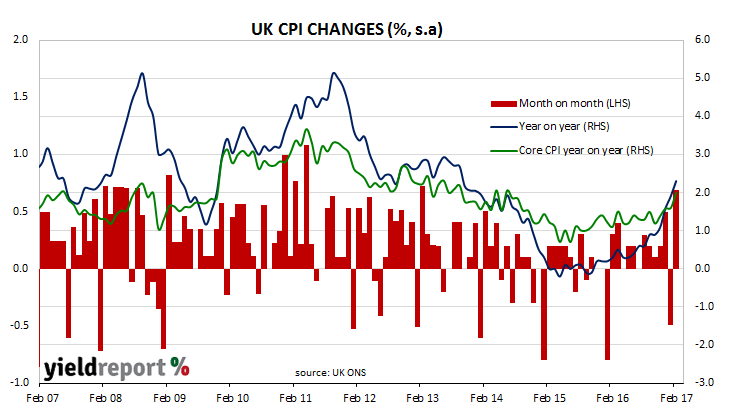

Central banks want higher inflation. This has not always been the case. In previous decades central banks preached about the evils of inflation and how it diminished consumer spending power while it increased uncertainty regarding investment planning. However, all this changed after the GFC brought in fears of Japanese-style deflation and the “horrors” which came with that.

In recent years, almost every advanced economy has had extended periods where the various measures of inflation have been below central bank’s targets. Inflation figures above an annualised 2% have been rare and, on the occasion when they have been produced, there is not a great degree of conviction they will last.

Perhaps the first of the advanced economies to produce inflation figures close to or at its central bank’s inflation target is the UK. Headline consumer price inflation (CPI) in February was 0.7% and 2.3% year on year. Core CPI, which is CPI excluding food, energy, alcohol and tobacco, increased by 2.0%, up from 1.6% in January.

Higher oil prices are partly responsible for the surge in the headline rate but it is the fall in the UK’s exchange rate after the Brexit vote which is viewed as the driver behind higher core inflation.

20 March 2017

Citi Fixed Income Indices recently announced the eligibility for inclusion of Chinese onshore bonds to its emerging markets and regional government bond indices. This sees the expansion of the World Government Bond Index family with two new indices, the World Government Bond Index – Developed Markets (WGBI-DM) and the World Government Bond Index – Extended (WGBI-Extended) to complement the existing World Government Bond Index. This change was in response to the further opening of the China Interbank Bond market for eligible foreign institutional investors.

“We are pleased to see regulatory changes that enable market access, allowing us to reflect and provide new investment opportunities in our indices,” said Arom Pathammavong, Global Head of Citi Fixed Income Indices. He added, “We recognise the importance of appropriate market representation of our family of indices and are excited to grow our WGBI index family to suit investors’ needs.”

After an extensive review which included consultations with market participants, Citi concluded that China was eligible to join three existing government bond indices – the Emerging Markets Government Bond Index (EMGBI), Asian Government Bond Index (AGBI), and the Asia Pacific Government Bond Index (APGBI). With all indices, the impact on price will be determined by the relative importance, relevance and scale of use that the current indices in question currently have. What is clear is that the Chinese bond market is starting to become more relevant and a more realistic investment option for institutional investors than was previously the case.

17 March 2017

NAB has announced it has priced the world’s first gender equality bond. $500 million March 2022 bonds were issued at Swap +95bps to a selection of Australian and offshore investors. The new bonds are rated in the same manner as other senior unsecured bonds issued by NAB; they have a AA- (negative outlook) from S&P Global Ratings and a Aa2 (negative outlook) from Moody’s Investor Services. For all intents and purposes they are standard vanilla bonds, the only difference is the restriction on how the proceeds of the bond sale are used.

The proceeds will be used to finance or refinance organisations who are cited by the Workplace Gender Equality Agency as “employers of choice” for gender equality and whose primary activities avoid a range of proscribed activities such as gambling, tobacco products, the transport of live cattle or whaling. The organisations which have initially qualified are Lend Lease, Mirvac, Stockland, Monash University, Australian Catholic University, PwC, KPMG Australia, King & Wood Mallesons (Australia), Clayton Utz, Gilbert + Tobin, Minter Ellison, Corrs Chambers Westgarth, Ashurst Australia and Henry Davis York.