07 March 2017

When the RBA’s Governor Phillip Lowe appeared before the Standing Committee on Economics in late February, he made it clear the RBA was concerned by house prices and the amount of household debt which is primarily in the form of mortgage debt. “With household debt as a share of household income already at a record high, is it really in the national interest to get a little bit more employment growth in the short run at the expense of creating vulnerabilities which could become quite dangerous in the medium term?”

With this in mind it would have been hard for the RBA to turn around and cut the official rate at its March meeting after its chief made this statement. The RBA chief and his staff would be aware of the history of housing market busts; ten years ago the GFC came out of a collapse in the US housing market and Australia’s 1990/91 recession followed a price bubble in the housing market here. The RBA’s decision to hold the cash rate steady at 1.50% therefore should come as no surprise. It may have also convinced a few more economists who expect another rate cut to reassess their positions.

There was little in the way of change in the statement which accompanied the decision. Some economists pointed to the addition of the sentence “Most measures of business and consumer confidence are at or above average” and noted the RBA’s favourable mention of the global economy and higher prices for Australia’s commodity exports. However, by and large, these changes did not signify any real change in the statement’s tone or outlook.

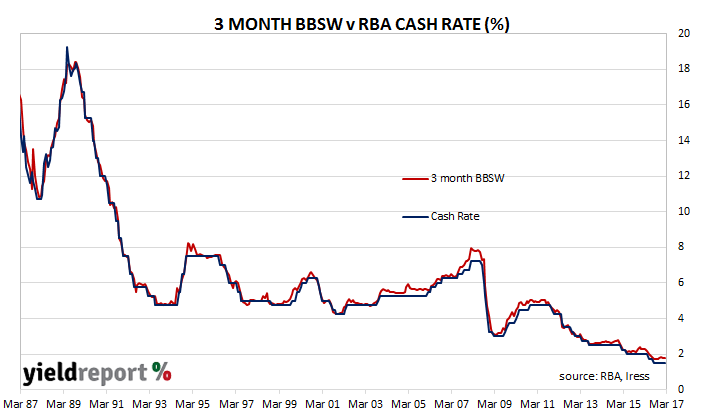

Accordingly, reactions in bond and currency markets were subdued. The Aussie was fractionally higher by the end of the day at around 75.9 US cents, while the 3 year bond yield rose 2bps to 2.07% and the 10 year bond yield increased from 2.835% to 2.85%. Prices in the cash market barely moved for 2017 contracts and the 1.50% cash rate is still expected to last through 2017. However, the probability of a February 2018 rate rise increased from 32% to 46%.

Here’s what some economists thought about the decision:

Kristina Clifton, Commonwealth Bank

Today’s RBA commentary confirms our view that the cash rate will remain on hold in 2017. There is little in the way of wage and inflationary pressures and underlying inflation is expected to remain below target until end 2018. However over the past few months Governor Lowe has expressed some discomfort with the prospect of household debt rising further. He has also acknowledged that conditions are strong in the housing markets in Sydney and Melbourne. These factors mean the cash rate is unlikely to move any lower.

Bill Evans, Westpac

On the less encouraging side, he refers to the insipid growth in household incomes and linked to that effect the observation that employment growth has been concentrated in part time jobs. Those considerable headwinds for the economy have been known for some time but, recently, he has not chosen to highlight them….We do not expect that the Australian economy will be sufficiently robust in 2018 to justify a return to a tightening cycle and continue to forecast rates on hold in 2017 and 2018.

Annette Beacher, TD Securities

To shift the RBA into a more hawkish stance we need to see a noticeable improvement in full-time hours worked. The February employment report is released March 16, and we did spot signs of life in the January report. We see the next move being up for the cash rate due to rising financial stability risks, strong national income growth, and inflation swiftly returning to the target band.

Ivan Colhoun, NAB

The bank is thus prioritising its concerns about household balance sheets at this point…It’s likely that the RBA will leave interest rates unchanged at least for the next six months. NAB’s forecasts for economic growth in 2018 are weaker than those of the RBA, largely because we expect a drag from lower commodity prices and a downturn in the housing construction cycle. This could see the RBA again considering a further cut to interest rates late this year.