06 March 2017

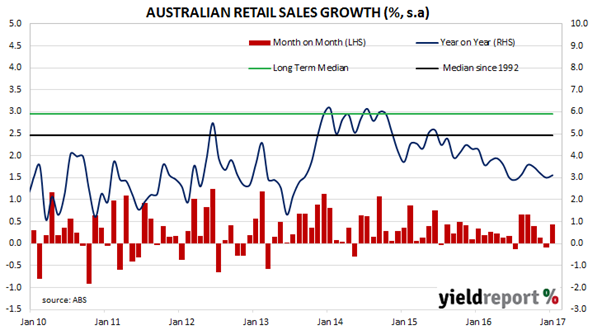

Australian consumers are finding it difficult to confidently spend up in the face of weak wage growth and general lack of optimism. That’s the view of Westpac senior economist Matthew Hassan in light of retail sales figures for January.

Sales figures grew by 0.4% over the month or 3.1% for the 12 months to the end of January which was in line with market expectations. December’s comparable figures had been -0.1% and 3.0% but those figures had been met with a suspicion. The closure of Masters Home Improvement stores was thought to have led to discounting while stock was cleared, so a comparison of the two months may be a little tainted.

Mr Hassan said the results in various categories was “mixed” and overall he was bordering on negative in his response to the figures. “Other results were disappointing…Total retail sales excluding household goods was up just 0.2%…Notably, weak wage income growth and consumer caution is contributing to relatively modest spending outcomes.”

06 March 2017

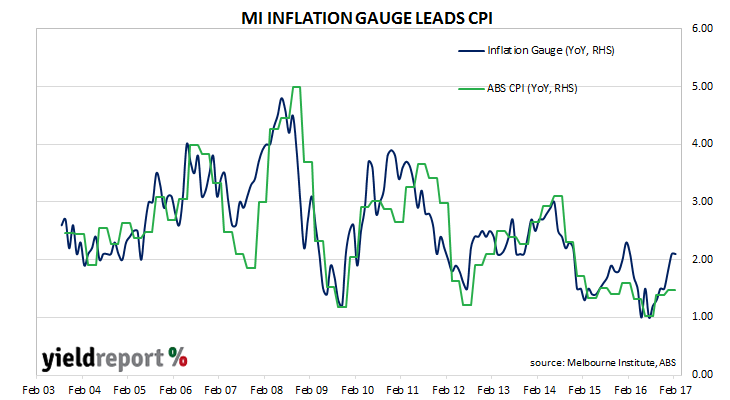

The Melbourne Institute’s Inflation Gauge is an attempt to replicate the ABS consumer price index (CPI) on a monthly basis instead of a quarterly one. It has turned out to be a reliable leading indicator of the CPI, although there are periods in which the Inflation Gauge series has diverged, only to return back to the official CPI series.

The Inflation Gauge fell during February for the first time since July 2016. This latest reading indicates consumer prices fell by 0.3% for the month even though the annual rate remained at 2.1%. January’s comparable figure was 0.6%.

Some bond yields were marginally higher on the day while the AUD was slightly weaker against the USD. In any case, retail sales figures and ANZ job advertisement reports were released on the same day, so it is problematic to say how each report was received. The yield on 3 year bonds was 1bp higher at 2.05% while the yield on 10 year bonds was steady at 2.795%.

A sizeable gap has existed between the two series for some time now. After the release of the January figures, YieldReport remarked on how unusual it is for such a gap to exist for long, as the average difference between the two series in any month is only 0.06%. Either the official CPI figures will rise or the Inflation Gauge will fall but readers can see the Inflation Gauge (blue line) has tended to lead the official CPI (green line) in the past.

06 March 2017

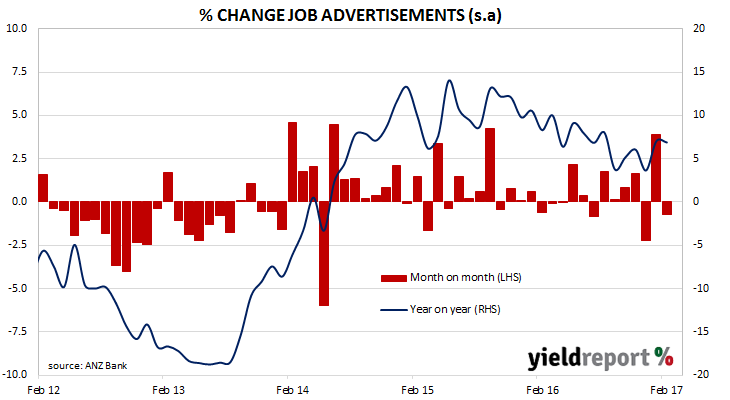

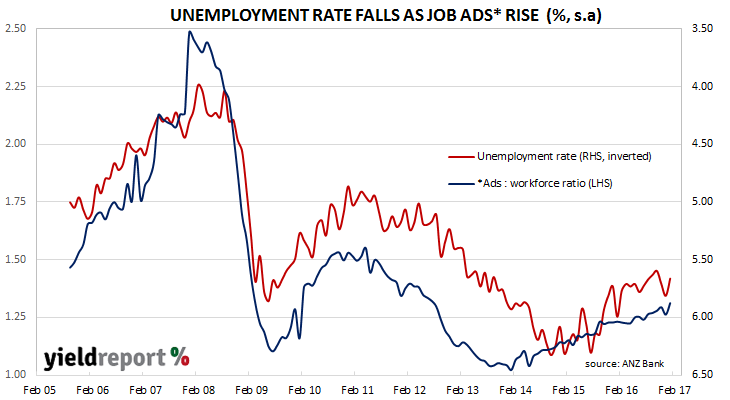

ANZ’s job advertisement survey is well-known as a leading indicator of employment numbers. It reflects changes in demand for labour and provides another measure of activity in the economy. Figures for February have been released and, after revisions were made to previously-recorded data, total advertisements were 0.7% lower than January’s figures but 6.9% higher than figures from January 2016.

David Plank, ANZ Head of Australian Economics, said the figures should be treated with some caution as they “may reflect the tricky nature of seasonal adjustment at this time of the year.” However, he was still optimistic about the implications of the latest numbers. “Looking ahead, strength in business conditions, firms’ profitability and an increase in capacity utilisation all point to an improvement in labour market conditions in our view. Overall, we expect the unemployment rate to slowly edge downward through 2017.” Other economists agreed. AMP Capital’s Shane Oliver thought the figures suggested “reasonable jobs growth” through 2017, as did the St George Bank’s chief economist, Besa Deda. “For the year to February, job ads lifted by 6.9%, suggesting employment growth could lift from its current level.”

02 March 2017

The probability of an increase in the US official rate, known as the federal funds rate, has gone ballistic in the last week. Prior to Tuesday (US time), markets had about a 1-in-3 chance of a 0.25% rate rise at the FOMC’s March meeting (the FOMC is the US Federal Reserve’s rate setting committee).

A look at the US futures trading on Tuesday shows how prices moved suddenly in a fashion which indicated traders thought the probability of a rate rise was considerably higher, only then to drop back by the end of the trading day. However, it set the trend for the rest of the week. The next day futures prices fell, implying a higher yield and a doubling in the probability of a move by the FOMC in the middle of March. Over the next two days, US traders increased the probability of a March rate rise to 80%.

02 March 2017

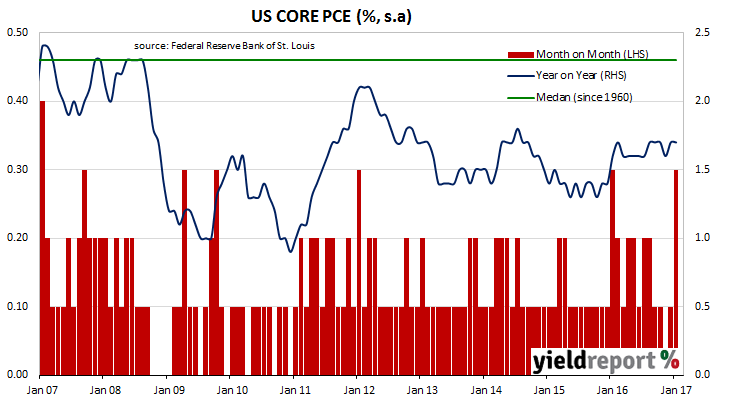

One of the US Fed’s favoured measures of inflation is core personal consumption expenditure (PCE). The core version of consumer spending strips out energy and food components, which are volatile from month to month, in an attempt to identify the prevailing trend. It’s not the only measure of inflation used; the Fed also tracks the Consumer Price Index (CPI) and Producer Price Index (PPI) from the Department of Labor.

The latest core PCE figures have been published by the Bureau of Economic Analysis as part of January figures for personal income and expenditures. At 0.3% for the month and 1.7% year on year, the numbers were under market expectations of 0.5% and 1.8% respectively. Even so, they were noted but generally ignored by markets who were focussed on the stream of public statements made by Fed officials with regards to the next increase in the federal funds rate.

These numbers may be used by some in the Fed to support a cautious approach to raising the US official rate. As NAB’s Global Co-Head of FX Strategy, Ray Attrill suggested they are “something that the likes of Fed dove Neil Kashkari will use to support his claim the Fed should be in no rush to tighten.” However, in light of the number and strength of recent hawkish statements by other Fed officials, it would appear members such as Kashkari are in the minority.

01 March 2017

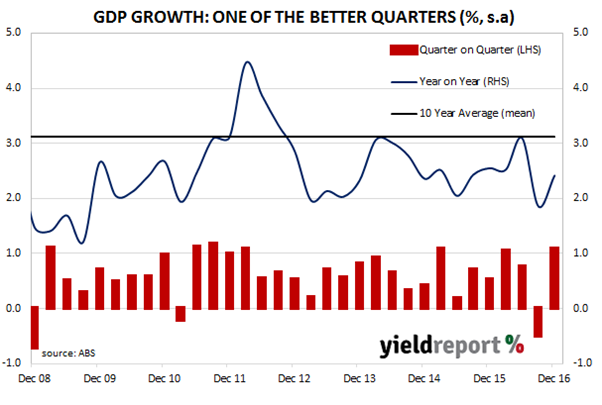

Australia’s negative GDP figure for the September quarter had surprised economists, commentators and investors alike. As a result, there was some apprehension in the lead up to the release of the December numbers. Another negative quarter would have confirmed a recession for Australia, the first since the early 1990s.

Economists had forecast Q4 GDP to be about 0.6%-0.7%. The actual number came in at 1.1% (seasonally adjusted), taking the year-on-year figure up to 2.4%. Unlike the September quarter, public sector investment expanded and added 0.3% of the 1.1% total growth. The bulk of GDP growth came from private consumption expenditures (0.5%) and exports (0.5%) while imports subtracted 0.2%.

Currency markets sent the AUD 0.2 US cents higher and bond yields rose on the day. 3 year bond yields finished 6bps higher at 1.91% and 10 year yields were 8bps higher at 2.83%, although these movements may have been influenced by higher yields in US bond markets overnight.

There was some concern higher consumer spending was at the expense of savings rates. Given a low (and possibly dropping) rate of wage and salary inflation in Australia, consumption spending growth may be difficult to sustain. NAB’s Riki Polygenis counted this as a potential brake on growth in 2018. “We are not as sanguine about growth in 2018 as the RBA…we see a 25bps easing in November 2017 as necessary to prevent a rise in unemployment and inflation undershooting again in 2018.”

28 February 2017

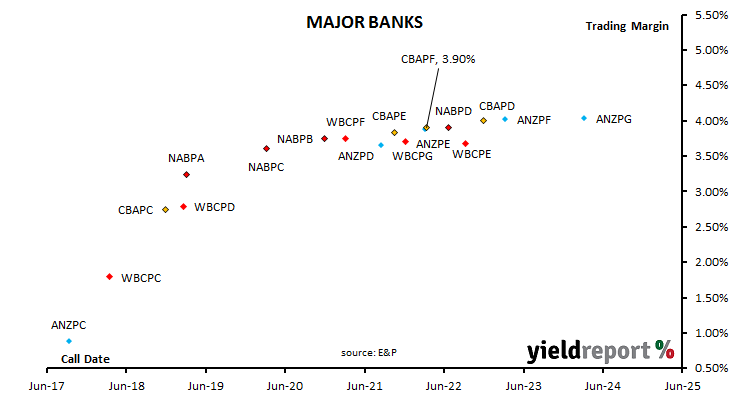

Commonwealth Bank has announced the margin on its latest CBA PERLS IX (ASX code: CBAPF) offering and, as expected, it was at the bottom of the 3.90%-4.10% indicative range. When this margin is added to the current 3 month bank bill swap rate (BBSW) of 1.78%, investors can expect around 5.68% annualised, inclusive of franking credits, for the first quarter and thereafter if BBSW rates do not alter materially. BBSW is typically close to the RBA’s official cash rate which is currently 1.50%.

CBA said it had received strong demand from syndicate brokers and institutional investors and $1.45 billion worth of PERLS IX have been allocated under the broker firm offer. The offer will remain open to CBA security-holder applications until the closing date or until otherwise announced. There is no general offer open to the public.

27 February 2017

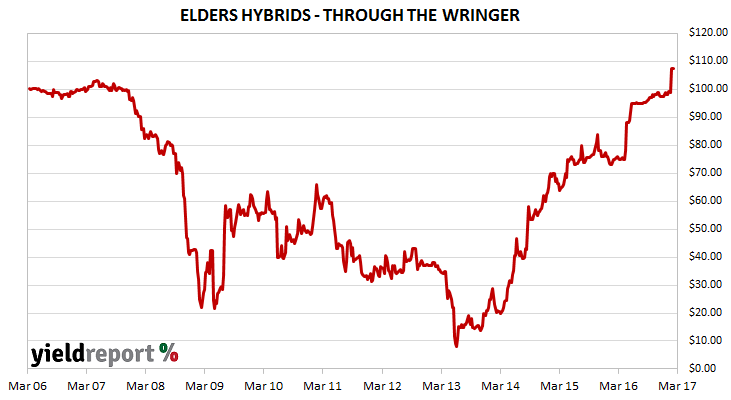

Elders Hybrids holders who have held the securities since they were first issued in early 2006 will be glad the experience is finally coming to an end. For all but a brief period they have been trading under par, sometimes by as much as 90%. Distributions are at the discretion of Elders directors and there have not been any since 2009.

Elders has now announced the securities will be “resold” on 30 March 2017. That is, Elders will sell holdings to a third party and in return, holders will receive the face value plus accrued distribution for the last twelve months which comes to $108.48.

The third party happens to be Elders Finance Pty Ltd which already owns 72.04% of the Elders Hybrids on issue. This holding was acquired via two buy-back offers in 2015 and 2016. When Elders announced an initial $30 million buy-back in August 2015 at $80 each, investors began to see light at the end of the tunnel. Speculation then turned to when the remaining securities would be redeemed. $100 million worth were purchased at $95 by the subsidiary in June 2016. This latest transaction will purchase the remaining 419,415 securities which are currently held by non-Elders holders.

Trading on the ASX will cease at the end of trading on 17 March 2017.

22 February 2017

More than a few respected economists are forecasting further rate cuts by the RBA in 2017. Employment growth is patchy and inflation is low. However, according to the Westpac-Melbourne Institute’s Leading Indicator index, economic growth is expected to remain above trend for the next three to nine months. Although the index fell from 1.36% in December to 1.30% in January, any reading above zero indicates above-trend growth. Given the index suggests the likely pace of economic activity three to nine months in the future, this latest reading implies the Australian economy is likely to grow through 2017.

Westpac chief economist, Bill Evans said, “However, the run of six consecutive above or at trend readings is signalling a better outlook for the first half of 2017. In particular, whereas over the September–November period the Index had been losing momentum, albeit still in positive territory, the December and January results represent a very strong rebound. Westpac concurs with the forecast of the Reserve Bank of 3% growth through 2017.”

22 February 2017

The next 25bps rate rise in the US cannot be far away. There does appear to be some disagreement as to when the first will come and how many there will be this year. Pricing in markets indicate there will be only two rises this year even as various Fed officials, including the Fed chair Janet Yellen, repeatedly point to three rises as long as the data does not change.

According to the Federal Open Market Committee (FOMC) minutes of February’s meeting “many participants expressed the view that it might be appropriate to raise the federal funds rate again fairly soon if incoming information on the labor (sic) market and inflation was in line with or stronger than their current expectations…” This section of the minutes got the most attention and analysis from economists and other observers but there was little reaction in US markets.

Westpac noted what seemed to be little reaction from markets even in the face of a chance the Fed would move at it March meeting. “[T]he Fed is primed to move and that March is a live meeting…and though there was some short term volatility into the release, markets were little changed…”.

CBA’s view on the reaction of US bond markets said it all, “The lack of a clear endorsement of March and the seeming queasiness at contemplating three successive hikes helped USTs (US Treasury bonds) to rally.”. When bond prices rise (rally), bond yields fall.