22 February 2017

The record for the largest single Commonwealth Government bond (ACGB) sale has been broken again this week. The Australian Office of Financial Management (AOFM) sold $11 billion November 2028 ACGBs via a syndicated process, an amount which is normally raised by the AOFM over the space of five weeks. Total bids were reported to have exceeded $20 billion and most of the bonds were purchased by domestic banks and fund managers, at a yield to maturity of 3.005%.

The size of the offer seems to have some, albeit a small, effect on bond yields. Westpac suggested bond yields “had moved a little higher in anticipation of this issue” and bond yield did actually rise on the day. The AOFM announced the syndicated sale on 17 February 2017 when the 10 year bond yield was at 2.835% and by the close of business on the day of the sale the yield had risen 3bps to 2.865%. Bond yields have moved up or down by this amount for little or no reason in the past so whether this movement is sale-related or just normal variation is debatable.

22 February 2017

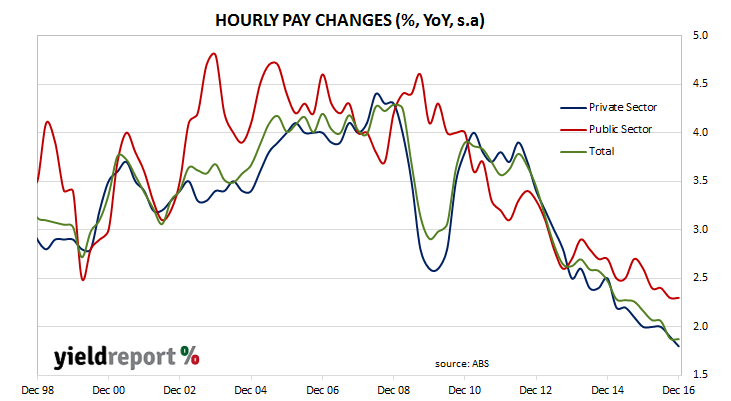

If there is a factor behind the cost of goods and services going up, it does not appear to be wages and salaries, at least not on average. For the past five years, the rate of growth of Australian wages and salaries on an hourly basis has been falling.

According to the latest December quarter figures published by the Australian Bureau of Statistics (ABS), hourly wages grew by 0.5% in the December quarter, which is the same as the September figure and in line with market expectations. Year-on-year growth was steady at 1.9% and still at a record low. The growth rate is now barely more than consumer inflation and unless employment rises and adds upwards pressure on wages, Australian pay rates may start to lag consumer price rises.

While the overall figures are being mostly influenced by private sector pay, even the public sector is struggling and hourly-wage inflation is the lowest since records began in 1998. Year-on-year figures for the public sector rose by 2.3%, the same as September’s number.

21 February 2017

The February RBA meeting is one of the four months of the year in which most RBA rate changes have been historically made. The reason for this is the meetings in these months follow quarterly CPI releases at the end of the previous month. This February no change was made to the cash rate.

The release of the minutes from the February meeting show the RBA board is concerned about potentially-slower rates of growth in consumer spending and a directionless labour market. On the other hand the Board acknowledges the recent improvement in the terms of trade as well as the view the recent drag on growth from investment numbers will cease soon as investment numbers come back to trend.

Adam Boyton, Deutsche Bank’s chief economist thinks a subtle change in the wording of the minutes holds a clue to the RBA’s view. “The final paragraph of the minutes hold an important tweak in our view, specifically, the inclusion of the phrase ‘and the level of the cash rate’…That inclusion of ‘the level of the cash rate’ is noteworthy as it implies the hurdle for easing is quite high given how low rates already are.”

Bill Evans, Westpac chief economist noted the RBA’s view of the opposing forces acting in Australia’s economy at the present. “We see nothing in these minutes to change our view that the official cash rate will remain on hold throughout 2017 and 2018. Markets continue to anticipate rate hikes in 2018 while a considerable number of commentators are predicting rate cuts in 2017. The middle course seems a much more likely outcome particularly given our view that growth momentum can pick up in 2017 but slow markedly through 2018 posing risks for the labour market and economic activity.”

16 February 2017

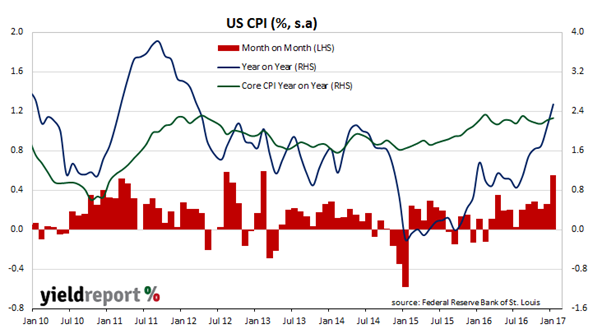

Finally, the US Fed may be about to have its desire for inflation fulfilled. Consumer inflation has risen, in terms of both the headline consumer price index (CPI) and core CPI. January CPI figures released by the Bureau of Labor Statistics indicate consumer prices rose by 0.6% for the month, or double December’s 0.3% and well above the consensus market forecast of 0.3%. On a year-on-year basis, the CPI increased by 2.5%, well up on December’s comparable figure of 2.1%. Core prices, the measure of prices which strips out food and energy prices changes, rose 0.3% for the month and more than the 0.2% expected. Over the last 12 months, core inflation edged up to 2.3% from December’s 2.2% (seasonally adjusted).

According to the Bureau, half the rise in the overall price level was driven by fuel prices, with housing, clothing and new vehicles also major contributors. In the core CPI measure, prices of clothing, new vehicles, car insurance and airfares all increased noticeably. ANZ Research made the observation the numbers were “largely positive. Inflation is normalizing, but a smoking gun of a sustained trend higher is still to materialise.”

16 February 2017

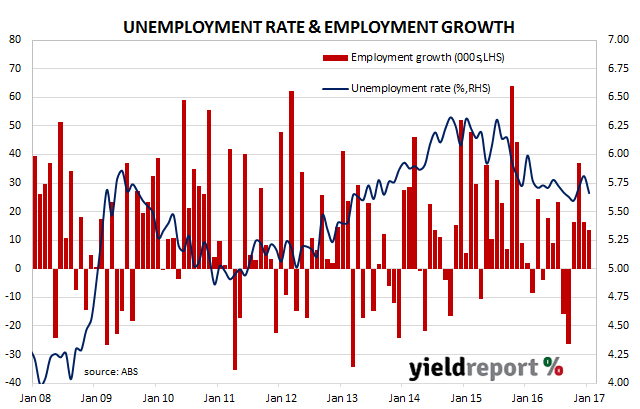

Australia’s unemployment rate dropped in January, although a drop in the number of people counted in the labour force was largely responsible. The ABS released January employment estimates which indicated Australia’s unemployment rate fell from 5.8% to 5.7%. The total number of people employed in Australia in either full-time or part-time work rose by 13,500 during the month, in contrast with the market’s expectation of +10,000. Total hours worked grew by 0.6% over the month and are1.2% higher than the comparable number from January 2015.

Financial market reaction was mixed on the day. Bond yields barely moved; 3 year bond yields rose 2bps to finish the day at 2.04% while 10 year yields rose 1bp to finish at 2.83% and the Aussie slipped about 0.2 US cents to back under 77 US.

Despite the generally–positive numbers, there were two aspects of the report which disappointed some economists. The participation rate fell back from 64.7% to 64.6%, a reversal of December’s rise and a large fall in full-time jobs and a large rise in part-time jobs. As Janu Chan, a senior Economist at St George put it, “On a less positive note, job growth was entirely driven by the part-time job category, where jobs rose 58.3k. This came at the expense of 44.8k full-time jobs. The unemployment rate stepped down from 5.8% to 5.7% in January, although this was largely reflective of the participation rate edging down.”

15 February 2017

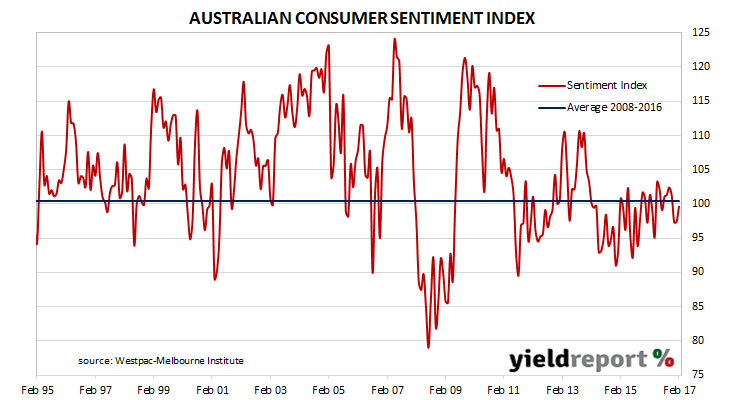

Australian consumers think interest rates will be higher in 2017 but despite this they are more optimistic, or less pessimistic than they were in December. The Westpac-Melbourne Institute consumer sentiment index rose in January, recording a 2.2 increase to 99.6. Any reading below 100 indicates the number of consumers who are pessimistic is more than the number of consumers who are optimistic. Westpac described the readings as indicating sentiment was at “cautiously pessimistic”’ levels and the result of “renewed concerns about the economic outlook combined with signs of increased pressure on family finances.” All five components of the index improved, although other parts of the survey such as the Unemployment Expectations Index deteriorated to some degree.

By the close of business, 3 year and 10 year yields were both 5bps higher at 2.04% s and 2.82% respectively. The AUD was around 0.5 US cents higher at just over 77.10 US cents.

15 February 2017

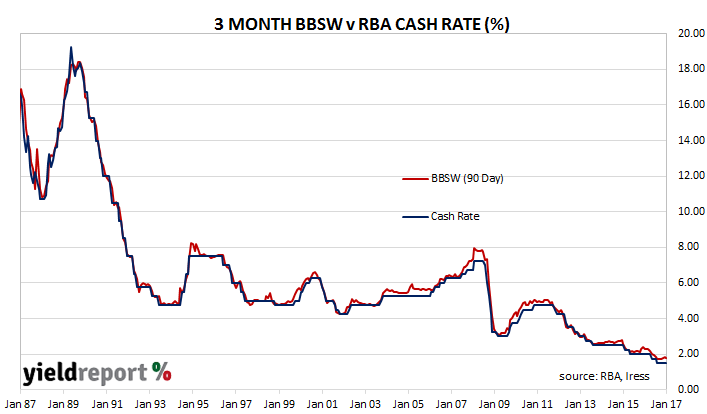

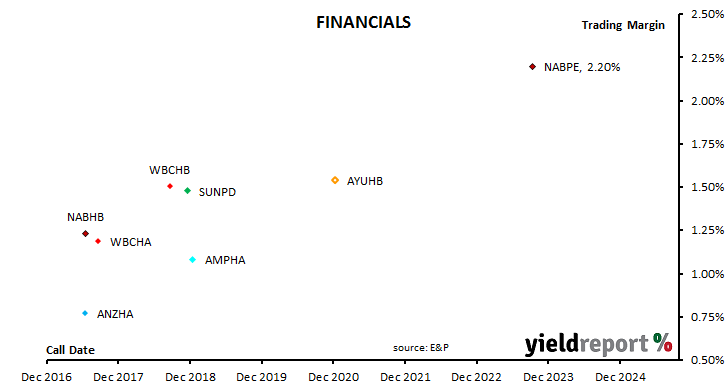

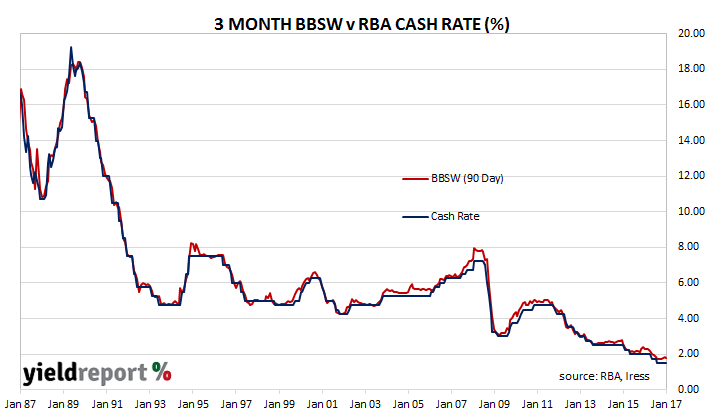

NAB’s latest ASX-listed note offering has had its margin set at the lower end of the 2.20% to 2.30% indicative range. The margin on NAB Subordinated Notes II has been set at 2.20% and, when added to the current 90 day bank bill swap rate (BBSW) of 1.775%, investors will receive an initial 3.975% per annum. The actual amount of income investors receive over time is subject to changes in the BBSW rate each quarter, which tends to follow the official cash rate closely (see below).

NAB has announced the issue will raise at least $800 million “following strong demand”. Trading on the ASX will begin on 21 March 2017 and the first quarterly distribution will be paid on 20 June 2017 with the amount based on the 90 day BBSW rate on the first business day of each payment period.

14 February 2017

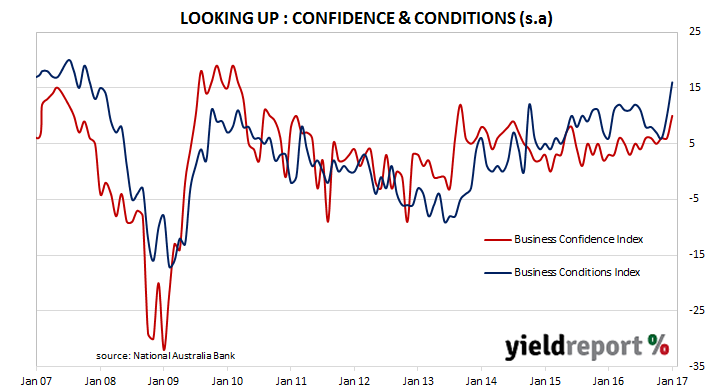

Australian businesses are enjoying conditions seen once a decade, as trading conditions remain elevated and profitability is maintained. According to NAB’s latest monthly business survey of 400 firms, its Business Confidence Index jumped 4 points to 10 while the Business Conditions Index kicked up 6 points to 16. Westpac senior economist Andrew Hanlon said, “The survey adds to the evidence and supports our view that the economy is emerging from the soft spot that prevailed during mid-2016.”

Bond and cash market yields were higher by the end of the day. The 3 year bond yield was 4bps higher at 1.99% and the 10 year bond 3.5bps higher at 2.77% as markets forecast the RBA would be less likely to lower the official rate in light of buoyant business conditions.

The reversal NAB had expected after the previous survey did not take place and perhaps the explanation is what NAB refers to as “diverse and rapidly changing seasonal influences at this time of year.” In any case, NAB urges caution with regards to analysis of its latest figures while it is also concerned as to the sustainability of current conditions. “NAB Economics also have concerns for the longer-term growth picture, as the contribution from LNG exports, temporarily higher commodity prices and the residential construction boom fade, keeping pressure on the labour market.”

However, the figures were positive enough for NAB to change its interest rate forecasts for 2017 from two rate cuts to just the one at the RBA board meeting in November. Other economists, such as UBS economist George Tharenou, start from a higher base; he thinks it’s not a matter of less rate cuts but rather rate rises. “Overall, we still see the RBA on hold ahead, but business conditions have now clearly moved into historical rate-hike territory.”

10 February 2017

The RBA’s quarterly Statement on Monetary Policy (SoMP) sets out the RBA’s view of domestic and international conditions. It also provides forecasts for Australian inflation and GDP growth based on the most recent data. While its view of international conditions will not move international markets, past SoMPs have moved Australian bond and currency markets from time to time.

On this occasion, there was little in the statement which was not already anticipated. Economists had already anticipated various growth forecasts would be pared back, especially the period regarding the year to June 2017. A 0.25% reduction in the June 2017 inflation forecast was no great shock, either.

07 February 2017

February is one of the four months of the year in which rate changes traditionally occur, although the RBA can change the official rate on any day should it so choose. The February meeting, along with May, August and November meetings, follows a quarterly CPI release which may provide the impetus for the RBA board to act. In this case current CPI figures, along with other measures of inflation and economic activity, have not proved sufficiently weak for the RBA to act and it has left the official rate at 1.50%.

The RBA expects GDP growth to rebound in December, boosted by exports. On top of export growth, a moderate increase in consumption and higher non-mining investment are expected to keep GDP growth at around 3% for the next two years. Inflation forecasts have remained intact with wages growth to remain low.

Reactions in bond and currency markets were somewhat contradictory. The Aussie went from 76.3 US cents to 76.8 before it fell back, while the 3 year bond yield fell 3bps to 1.95% and the 10 year bond yield fell from 2.795% to 2.725%. Prices in the cash market barely reacted; there’s still a slim chance a rate cut through to August 2017 and an increasing chance of a rate rise from October 2017.

Here’s what some economists thought about the RBA decision:

Ivan Colhoun, NAB

“The Statement seemed both a little more upbeat on the global growth outlook (conditions described as having improved in recent months) and reasonably relaxed about the Bank’s view of both the Australian growth outlook and an expected slow return of inflation to the target. The Bank would likely need to change one of these views significantly to alter its policy rate in the near term.”