06 February 2017

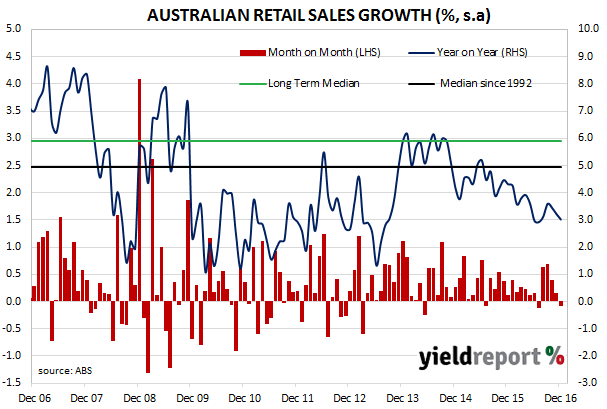

Australian consumers are buying more but paying less. That’s one of the conclusions to be had out of the latest retail sales figures. According to the Australian Bureau of Statistics, December retail sales growth was lower than expected and it was driven by an unusually large fall in the household goods category, which includes furniture, floor coverings, housewares, Manchester, electrical goods as well as hardware and building supplies.

In total, sales figures fell 0.1% over the month or 3.0% for the 12 months to the end of December. November’s comparable figures were 0.2% and 3.3%. The market was expecting 0.3% but some economists think the 2.3% decline in household goods may have been related to the closure of Masters Home Improvement stores.

Bond yields dropped on the day; 3 year bond yields fell 2bps to 1.98% and 10 year yields fell 3bps to 2.795%. However, US and UK 10 year bond yields were both down 3bps (Friday night, US/UK time) so the effect of the retail data on local bond yields is debatable.

06 February 2017

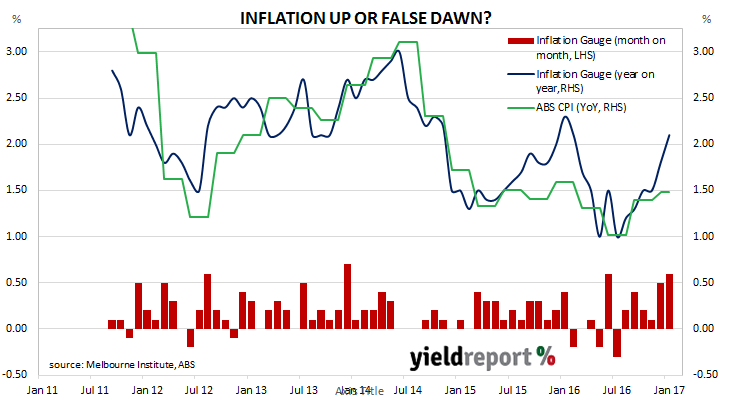

The Melbourne Institute Inflation Gauge rose during January for the sixth month in a row. This latest reading indicates consumer prices rose by 0.6% for the month and 2.1% for the year to the end of January. December’s comparable figures were 0.5% and 1.8% respectively.

Bond yields fell on the day and the AUD was slightly weaker against the USD. However, as December retail sales figures and ANZ job advertisement reports were released on the same day, it is problematic to say how each report was received. The yield on 3 year bonds was 2bps lower at 1.98% while the yield on 10 year bonds was down 3 bps to 2.795%.

06 February 2017

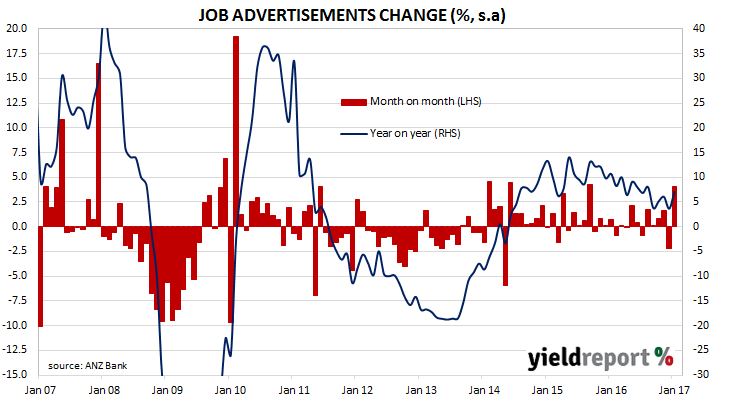

ANZ’s job advertisement survey is well-known as a leading indicator of employment. It reflects changes in demand for labour and provides another measure of activity in the economy. January’s figures totally reversed December’s decline and provided a glimmer of hope to job seekers. Total job advertisements rose by 4% for the month and 7.1% compared to January 2016, whereas December’s comparable figures were -2.2% and +3.7% (after revisions).

03 February 2017

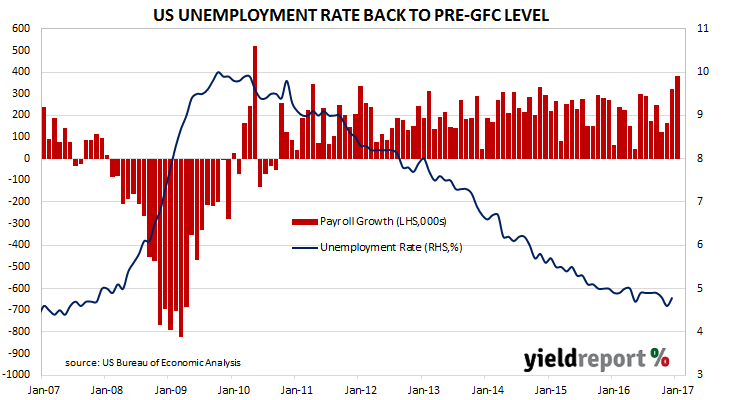

The US labour has added more jobs in January but economists seem to be focussed on parts of the report which suggest pay rises are slowing. According to the US Bureau of Labor Statistics 227,000 jobs were created in the non-farm sector in January against expectations of 180,000. The unemployment rate rose from 4.7% to 4.8% as the participation rate rose again, this time from 62.7% to 62.9%.

While the number of jobs created was more than expected, average hourly earnings increased by only 0.1% instead of an expected 0.3% and there were downwards revisions to previous months. On an annual basis, average hourly pay rose 2.5% year on year, down from December’s figure of 2.8%.

Westpac said, “US non-farm payrolls for January recorded a solid number but the detail does not compel the Fed to put March on the table.”. US 10 year yields initially fell substantially when the report was released but they recovered during the rest of the day and closed at 2.47% after a couple of Fed officials reiterated the need for several rate increases this year.

02 February 2017

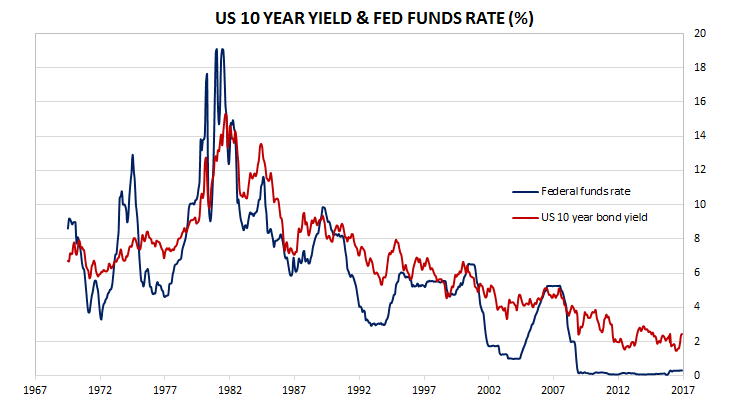

As expected, the US Fed left its official rate steady. The Fed’s interest rate setting committee, known as the Federal Open Markets Committee (FOMC) kept the Federal Funds target rate at its range of 0.50% to 0.75%. US bond yields initially fell after markets took the view there was little chance of a rate rise any time soon, but ended the day 1bp higher at 2.47%.

The language used in the accompanying statement changed in a slightly hawkish manner. According to NAB’s Tapas Strickland, “…the Fed seemingly upgraded its inflation outlook ever so slightly, noting that inflation ‘will rise to 2%’…The Fed also noted the recent improvement in consumer and business sentiment of late.”

However, Westpac economist Eliot Clarke said the statement did not change his view of the path of US official interest rates in 2017 or further out. “Changes made to the statement’s language offered no justification to alter our view that the Committee will look to raise the Fed Funds Rate twice this year and another two times in 2018…”

Even though Fed officials as senior as Janet Yellen have alluded to three rises per year through to the end of 2019, markets are still expecting a fairly measured pace of increases. According to cash futures pricing, March is viewed as about a 1 in 8 chance for a rate rise and even May is rated as 1 in 3.

However, economists typically are taking a more hawkish view. UBS economist Samuel Coffin said, “We continue to expect two 25 bps hikes this year, but better capex, faster employment growth, or a stimulative enough fiscal package could shift our expectations to three.” Goldman Sachs were more definitive; “We see limited implications for the near-term policy outlook, and continue to assign a 35% chance that the committee raises rates as soon as the March 14-15 meeting. Our modal forecast remains three hikes this year, at the June, September and December FOMC meetings…”

02 February 2017

A spate of maturities of hybrids and notes listed on the ASX have contributed to recent falls in yields, according to Morgans. So much so, it is recommending certain hybrids be sold. “We attribute the strength in the ASX listed space to the redemptions of ANZPA, ORGHA and WOWHC which occurred during December and resulted in $2.7bn of funds hitting investors’ accounts.”

Morgans thinks investors tend to be attracted by hybrids with high issue margins (the margin above BBSW when the securities were first issued) and warns against choosing an investment based soley on the income side. “We caution investors about focusing solely on running yield and not considering the total return (yield to call) offered by the security. Yield to call takes into account the amortisation of the security’s price back to its face value over time as well as the income paid…We recommend clients trim positions in AMPPA, ANZPD, BENPE and WBCPE and remain cautious about adding to portfolios at current levels.”

02 February 2017

Tabcorp Holdings has given notice of its intention to redeem all its ASX-listed subordinated notes (ASX code: TAHHB). Holders on the register on 14 March 2017 will receive $100 face value plus the final interest payment of $1.43 per note on 22 March 2017. The last day of trading is 10 March 2017.

The number of ASX-listed notes and bonds is set to decline over the next few years. There were around twenty or so securities of this type listed on the ASX, not including income securities, before ORGHA and WOWHC matured at the end of 2016. Of these, six will mature in 2017, another six will mature in 2018 and a further three will mature in 2019. Previous issuers of notes and bonds seem to have been favouring capital notes and preference shares in recent years. As their notes mature, there are few new securities to replace them. Qube Holdings Notes (ASX code: QUBHB) were the only ASX-listed notes issued in 2016 with Australian Unity notes the only issue of this type in 2015.

02 February 2017

For some years now trade figures have been greeted with a mix of resignation. Australia has, for many years, imported more than it has exported, with the balance financed by borrowing from overseas investors or selling assets to them.

However, those days may have come to an end. The mining investment boom has led to greater volumes of coal and iron ore being sold. It’s not just export volumes. According to Westpac senior economist Andrew Hanlan, prices have risen as well, especially prices for coal. “The trade position improved dramatically over the second half of 2016 as a spike in commodity prices, particularly coal, boosted export earnings.”

Normally, markets note the Australian trade figures, figuratively shrug their shoulders and move on. However, the presence of a large Q4 trade surplus greatly reduces the likelihood of a negative December quarter GDP figure. This is relevant in the context of a negative September quarter GDP figure. Two negative GDP figures in a row constitute the technical definition of a recession and confidence would have taken a hit.

31 January 2017

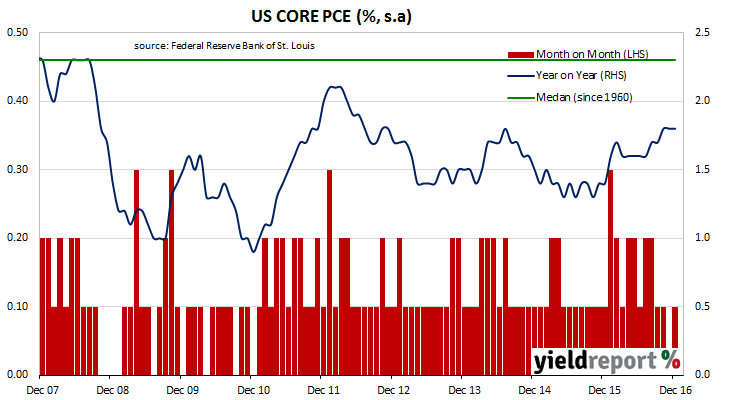

The US Fed takes into consideration several price indices when evaluating the rate of inflation. It says it does so because “various indexes (sic) can send diverse signals about inflation”. One of its favoured measures of inflation is the core personal consumption expenditure. The core version of consumer spending strips out energy and food components, which are volatile from month to month, in an attempt to identify the prevailing trend. It’s not the only measure of inflation used; the Fed also tracks the Consumer Price Index (CPI) and Producer Price Index (PPI) from the Department of Labor. Its view of inflation is important as it forms the basis for the FOMC’s interest rate settings.

The latest core PCE figures have been published by the Bureau of Economic Analysis as part of December figures for personal income and expenditures. At 0.1% for the month and 1.7% year on year, the figures were in line with market expectations.

31 January 2017

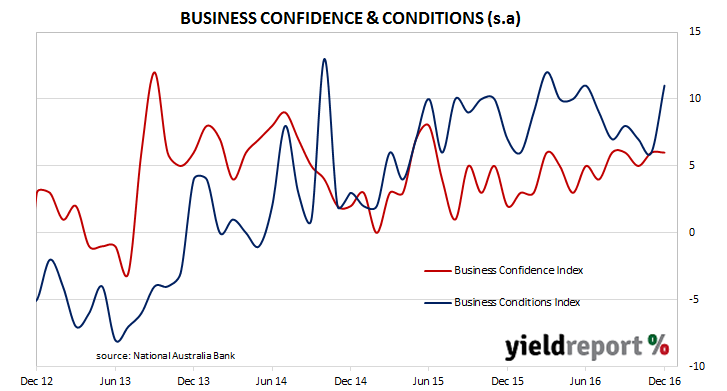

Australian businesses are enjoying conditions last seen in 2006, the result of buoyant trading conditions and higher profitability. According to NAB’s latest monthly business survey of 400 firms across the non-farm business sector in the last week of December, the Business Confidence Index was stable at 6 while the Business Conditions Index kicked up 5 points to 11. However, NAB thought some of the responses from the survey are contradictory, which suggests some reversal when the next survey takes place.