27 January 2017

Sometime good news is viewed by financial markets as bad. In other times, the same news can be taken as good. In this case, while the news in question has not been viewed as good, what was generally seen as bad on the surface had been interpreted as being alright, if not slightly favourable.

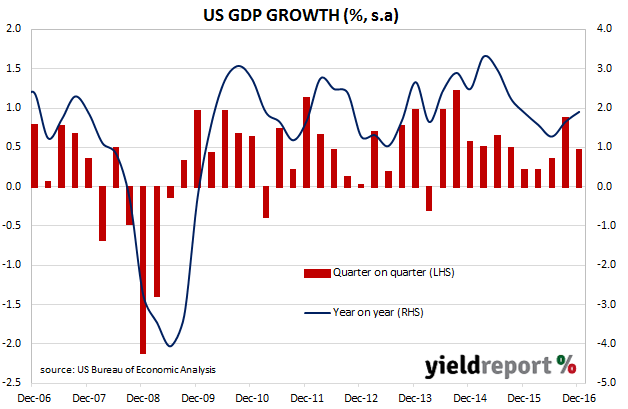

The US Commerce Department released Q4 “advanced” estimates of US GDP on Friday night Australian time. This estimate is the first of four estimates and subject to three more revisions over the next two months. They show an annualised growth rate of 1.9%, lower than the median estimate of 2.1% and well down up on the Q3 2016 figure of 2.9%.

Yields of US Treasury bonds did not alter much after the report. 2 year bond yields were essentially unchanged on the day at 1.22% and 10 year bonds were 2bps lower at 2.48%. The rationale for this is in the composition of GDP. Net exports were the main culprit because imports were higher. Strong economies suck in imports and so in a counter-intuitive manner, a higher net export figure which leads to a smaller GDP figure is indicative of strong domestic demand.

ANZ said the numbers “disappointed” but the bank pointed to “firm” private consumption figures as well other data it described as ”encouraging”. Westpac’s view was similar but it too found something positive in the figures when it said “the underlying detail was decent and inflation expectations ticked higher.”

US GDP numbers are published in a manner which is different to most other countries; quarterly figures are compounded to give an annualised figure. In countries such as Australia and the UK, an annual figure is calculated by taking the latest number and comparing it with a figure from a year ago. The diagram below shows US GDP once it has been expressed in the normal manner.

25 January 2017

The latest CPI figures have lent some credibility to the prospect of another rate cut this year. Figures for the December quarter have been released by the ABS and both headline and seasonally-adjusted figures were weaker than the market expected. Headline inflation was 0.5% over the quarter and 1.5% over the year to December. Seasonally-adjusted figures give the same results as the headline figures. Markets had expected a quarterly figure of 0.7% and an annual figure of 1.7%.

“Core” inflation measures favoured by the RBA, such as the “trimmed mean” and the “weighted median”, were slightly below consensus. For the quarter, both the trimmed-mean and the weighted-median increased by 0.4% and the average of the two 12 month rates came to 1.6%. The RBA aims to return core inflation back to its preferred range of 2%-3%.

25 January 2017

The Westpac-Melbourne Institute Leading index of Economic Activity was developed as a tool to identify turning points in the Australian economy. It provides a measurement of Australia’s likely rate of economic growth for the next three to nine months, relative to trend, and it is one of several important private sector estimates which provide markets with clues as to short term economic conditions. Its latest December reading rose for the fifth month in a row, from a revised November figure of 0.00% to 1.28%.

Westpac’s chief economist Bill Evans said the run of above-trend readings signalled a robust outlook for 2017. However, while Westpac was “comfortable” with its 3% 2017 forecasts, 2018 was another matter.

24 January 2017

AFIC Notes (ASX code: AFIG) are convertible notes issued in December 2011 and which are now just under one month away from the maturity date of 28 February, 2017. Unlike ordinary debt instruments, holders of convertible notes are faced with the necessity of making a decision prior to the maturity date.

A convertible note can be thought of as a corporate bond with an attached equity call option. The bond component has a face value of $100 and pays fixed-rate interest at a rate of 6.25%, payable semi-annually. The call option gives the holder the right but not the obligation to exchange the face value of the bond for 19.6603 ordinary shares in the issuer. At the current share price, 19.6603 AFI shares are worth around $116.80. AFI shares are listed on the ASX and so its ordinary shares will fluctuate in value, as will the value of the AFIC Notes.

23 January 2017

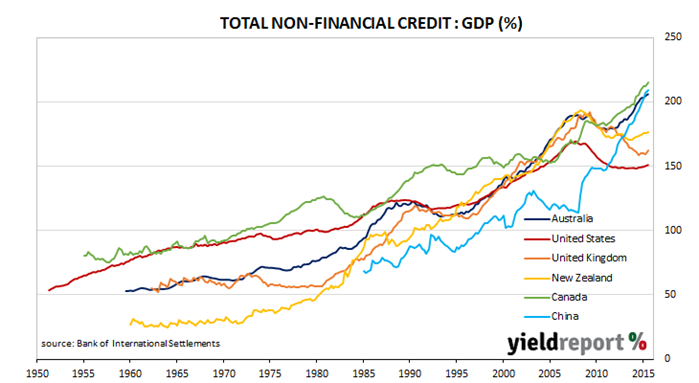

The team at M&G Investments were having a look at Bank of International Settlements (BIS) data to highlight the dangerously high ratio of Chinese non-financial debt to GDP. A high debt-to-GDP ratio is viewed as dangerous to a country in the same way high personal debt levels relative to one’s annual income are potentially hazardous to one’s financial health. What type of debt is included is a matter of the type of analysis taking place but financial debt is typically excluded because it is usually debt on-lent to non-banks. As banks are in the business of lending, counting their debt would be counting the same debt twice.

23 January 2017

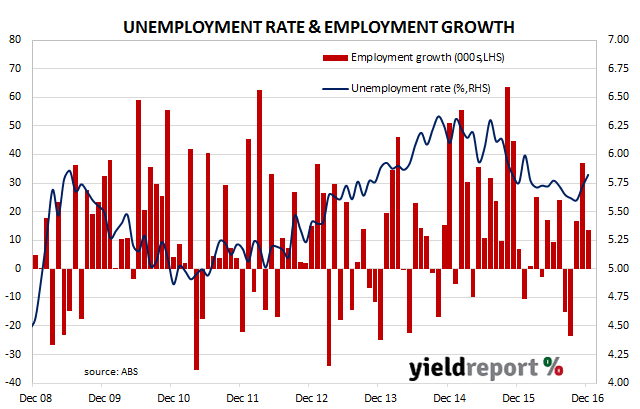

The ABS released December employment estimates which indicated Australia’s unemployment rate rose from 5.7% to 5.8%. The total number of people employed in Australia in either full-time or part-time work rose by 13,500 during the month, in contrast with the market’s expectation of +10,000. The participation rate rose again, this time from 64.6% to 64.7%. In terms of total hours worked, levels are 0.7% higher than in December 2015. Westpac senior economist Justin Smirk said “While this suggests that we may have passed the point of a softening labour market it does not suggest that a more robust recovery has started.”

18 January 2017

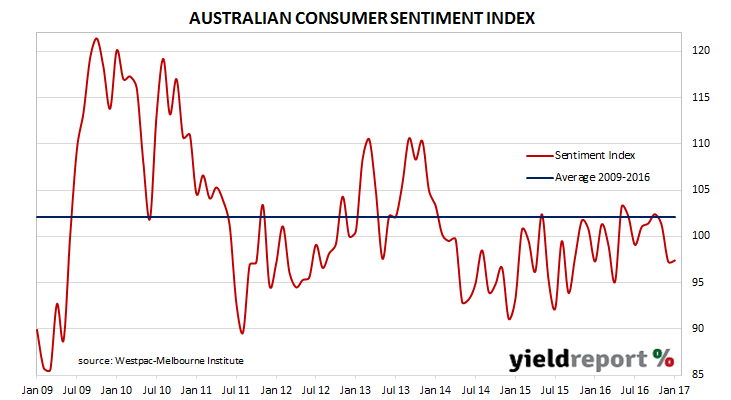

Australian consumers may be relatively more optimistic than they were at the end of 2017 but that itself may be an optimistic description. A more accurate picture would be given by describing consumers as slightly less pessimistic than they were a month ago. The Westpac-Melbourne Institute consumer sentiment index rose ever-so-slightly in January, recording a 0.1 increase to 97.4. Any reading below 100 indicates the number of consumers who are pessimistic is more than the number of consumers who are optimistic.

Financial markets were unperturbed by the results. By the close of business, 3 year yields were unchanged at 2.0% while 10 year yields slipped 1bp to 2.72%. The AUD was around 0.5 US cents lower at just over 75 US cents.

Economists had different responses to the data, ranging from the outright negative to something a vaguely encouraging. Westpac’s Elliot Clarke described the result as disappointing but then again “there are likely to be lingering effects from the shock of the announcement just before the December survey that the economy contracted by 0.5%.” Commonwealth Bank economist Kristina Clifton’s view was also surprised a bounce in confidence had not eventuated “given that the economic data since the GDP result has generally been positive. The good news is that unemployment expectations fell by 0.8% and should ease further this year as the unemployment rate moves lower.”

18 January 2017

We are not even into the final week of January and the Federal Government has already arranged borrowings to the tune of $11.4 billion. Mind you of this, $9.3 billion is from the syndicated sale of December 2021 bonds just announced, with settlement on 27 January, 2017. $9.3 billion is the largest bond sale ever undertaken by the AOFM, with the previous record held by a syndicated sale of $7.6 billion March 2047s in mid-October 2016.

Bids totalled $15.3 billion so the coverage ratio was around 1.65, which is a ratio usually considered to be quite low. However, the AOFM is known for surveying investor demand prior to auctions and sales. The transaction was also held in conjunction with a buy back of $3.1 billion of bonds maturing in 2017 so one could argue the net amount to be borrowed is substantially lower at $6.2 billion.

Source : AOFM

To put all of this in context, the AOFM issued bonds totalling $116.5 billion in 2016. Some of this was to finance maturing bonds or other bonds nearing maturity which were repurchased, but a good chunk of it was to finance the budget deficit as well as any other expenditure which is deemed not to part of the budget. In the 2016/2017 financial year, gross issuance is expected to be around $100 billion and about $74 billion in net terms.

17 January 2017

Mozambique is an African country which is not in Australian news all that often, if at all. It is described as “one of the poorest and most underdeveloped countries in the world” in Wikipedia, the result of nearly 20 years of civil war after it gained independence from Portugal.

This week its woes got a little worse, although its citizen are possibly past caring. Mozambique’s finance ministry announced it would not pay the January coupon on its 10.5% January 2023 bond which is denominated in USD. The country is now officially in default and it has stated it will struggle to make debt payments during the rest of 2017.

Depending on how default is defined, we should not be too surprised; Mozambique was in default for about ten years from the early 1980s to the early 1990s.

17 January 2017

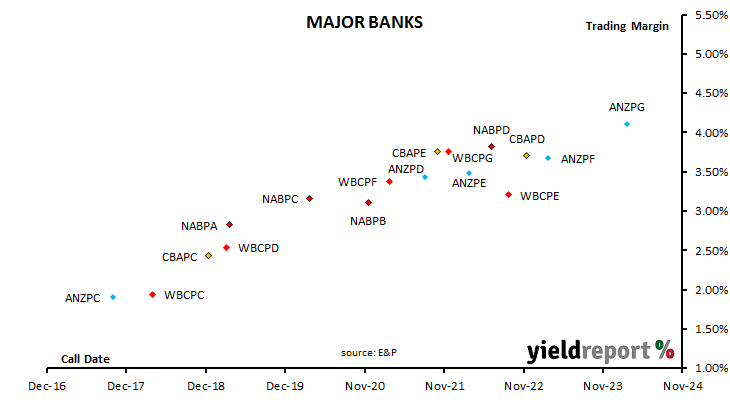

Evans & Partners’ Head of Income Products, Michael Saba thinks Westpac’s Capital Notes 2 (ASX code: WBCPE) stands out and not for the right reasons. “The scatter plot shows WBCPE to be still too low in margin with better value in shorter dated issues. ANZPG tends to top the volume list most days however it sits about right given its longer maturity profile.”

Its annual coupon, is equal to 90 day BBSW + 305bps (inclusive of franking credits). Sometimes investors focus on the income part of a hybrids return but given its coupon is not particularly high relative to other existing hybrids issued by major banks, this does not appear to be the motivation behind investor demand. Perhaps it is just another price anomaly which has built up over time.

As at close of business 17/01/2017