16 January 2017

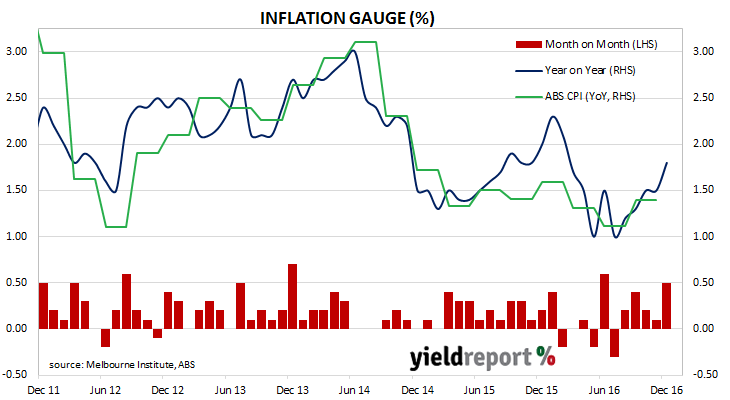

The Melbourne Institute Inflation Gauge rose again during December for the fifth month in a row. This latest reading indicates consumer prices rose by 0.5% for the month and 1.8% year on year. November’s comparable figures were 0.1% and 1.5% respectively.

3 year and 10 year bond yields both finished essentially unchanged. Both 3 year and 10 year yields remained steady at 1.99% and 2.73% respectively, while the AUD was slightly lower against the USD.

Readers will see from the chart above how the Inflation Gauge is an excellent estimator of annual CPI figures produced by the Australian Bureau of Statistics. Consumer inflation over the last five years has been edging down quite consistently, which has provided the RBA with an environment in which it could lower the official rate to a record low.

13 January 2017

During the week Evans and Partners’ Michael Saba spotted a pricing discrepancy in the two Macquarie Group hybrids listed on the ASX. “With some margin movements in past weeks, some switch ideas arise….switch into MQGPB from the shorter dated MQGPA on a relative basis. The scatter diagram shows MQGPB to sit above the pack whereas MQGPA just below the line.” The chart below is at the close of business on Friday but readers will see the gap between the two Macquarie securities was still quite sizable.

10 January 2017

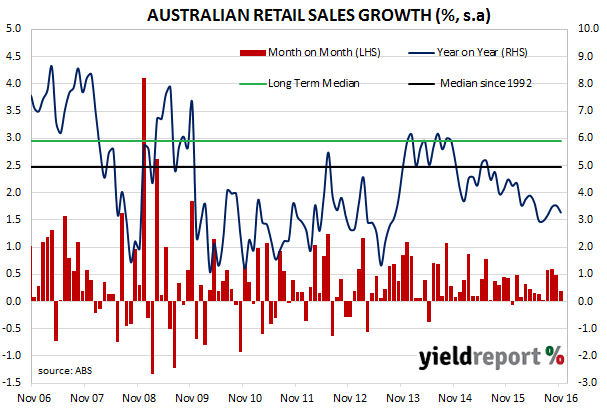

Australian consumers remain wary of opening their wallets and purses. According to the Australian Bureau of Statistics, November retail sales growth was lower than expected. Consumers favoured household goods, food, cafes, restaurants and takeaway food but clothing, footwear, personal accessories and department store sales were weak.

09 January 2017

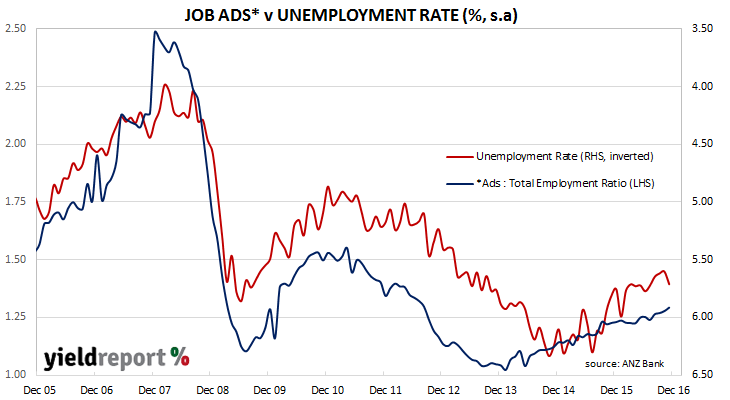

ANZ’s job advertisement is well-known as a leading indicator of employment. It reflects changes in demand for labour and provides another measure of activity in the economy. As such, government officials and economists would have been unhappy when they saw the latest figures from the monthly survey. Total job advertisements fell 1.9% in December (in seasonally–adjusted terms) after a revised 1.6% rise in November while the year-to-December figure of 3.7% was lower than November’s comparable figure of 6.0%.

ANZ senior economist Jo Masters described the result as indicating “the labour market as losing some of its previously strong momentum [but] not stalling.” The ANZ economist was quite optimistic conditions in the labour market would continue to improve. “While the labour market has clearly lost some momentum, business and consumer confidence remain elevated, capacity utilisation appears to be on the rise, and retail sales have strengthened recently. As such, we continue to expect conditions in the labour market to support an ongoing, albeit gradual, decline in the unemployment rate this year.”

09 January 2017

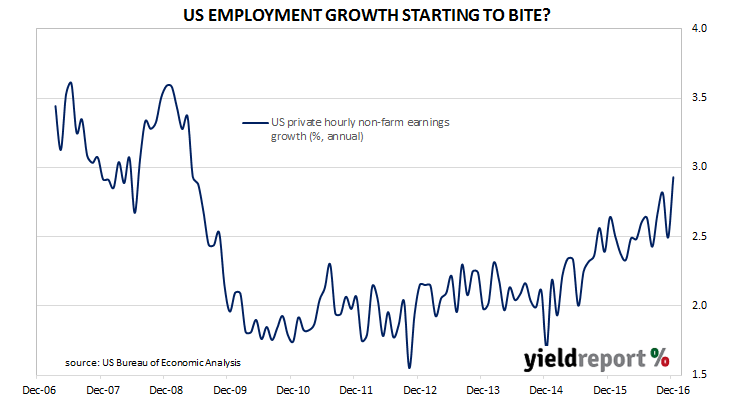

The US labour market may have added less jobs than expected but markets have found something else in the report on which to focus. According to the US Bureau of Labor Statistics 156,000 jobs were created in the non-farm sector in December against expectations of 175,000 but to offset this less-than-ideal result, November’s figures were revised up from 178,000 to 204,000 and over 2.1 million jobs were created during the calendar year 2016. The unemployment rate rose from 4.6% to 4.7% as the participation rate rose 0.1% to 62.7%

Analyst attention focused on the higher hourly pay rate. Now at USD$26.00 per hour, it is 2.9% higher than a year ago. Higher pay rates and greater weekly wages and salaries mean employees have additional money to spend and thus bid up consumer goods prices, although the extra money may well be saved or reduce debt.

15 December 2016

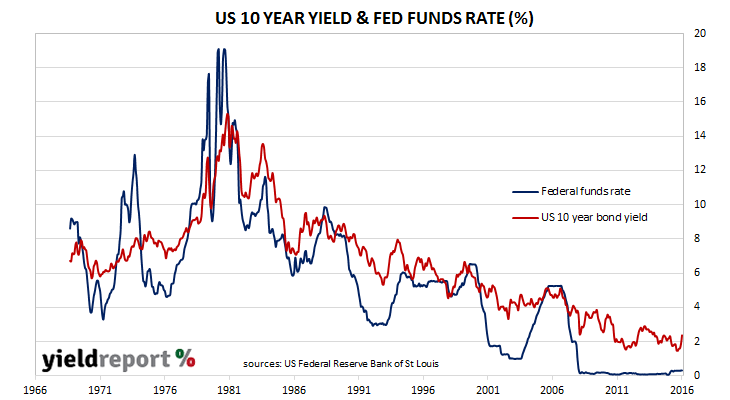

The US Fed has raised its official rate for a second time, one year after its last rise in December 2015. The Fed’s interest rate setting committee, known as the Federal Open Markets Committee (FOMC) raised the Federal Funds target rate from its 0.25% to 0.50% range to a range of 0.50% to 0.75%.

US bond markets reacted severely. US 2 year bond yields finished 11bps higher at 1.27% and 10 year bond yields finished 10bps higher at 2.57%, while the greenback soared. Australian bonds followed suit when the market opened next morning; yields on 3 year bonds rose 9bps to 2.02% and 10 year bonds rose 8bps to 2.91%.

The decision itself was widely anticipated but what was not expected was the hardening of language regarding inflation and the reversal of the downward trend of FOMC members’ expectations for where the official rate is likely to be in coming years. For the first time in some years FOMC members’ interest rate projections have increased, the language regarding inflation was noticeably stronger and eleven of seventeen FOMC member now expect three rate increases next year. Westpac’s Chris Elliott said, “For inflation, the tone was a little stronger; “Inflation has increased” replaced “inflation has increased somewhat”, while inflation expectations are now seen as having risen “considerably” despite “still” being low.” He also noted how inflation expectations, an important factor for central banks had changed since the US presidential election. “The change in market inflation expectations is entirely due to the anticipated impact of Trump’s mooted policies.”

15 December 2016

Australia’s unemployment rate rose in November despite the creation of over 39,000 jobs.

The ABS released November employment estimates which indicated Australia’s unemployment rate rose from 5.6% to 5.7%. Part-time employment barely changed but full-time employment rose by 39,300 to produce a net increase of 39,100, well in excess of consensus expectations of 17,500. The unemployment rate rose as more people joined the workforce with the participation rate 0.2% higher at 64.6%. Total hours worked for the month fell by 0.6%, which brought the annual figure back to just 0.1% higher than the comparable from November 2015.

The figures had little or no effect on financial markets, which were still dealing with the US Fed’s latest interest rate decision. Bond yields rose sharply before the employment figures were released; 3 year bonds finished the day 9bps higher at 2.02% and 10 year yields rose 8bps to 2.91%.

Underemployment, which has been in the spotlight in recent months, fell 0.3% to 8.3%. In the 1980s, underemployment was under 5% but it jumped to around 7% during the 1990/91 recession and then jumped again during the GFC. Lengthy periods of economic expansion have not made much of a dent in it, although it did decline in the mining investment boom.

14 December 2016

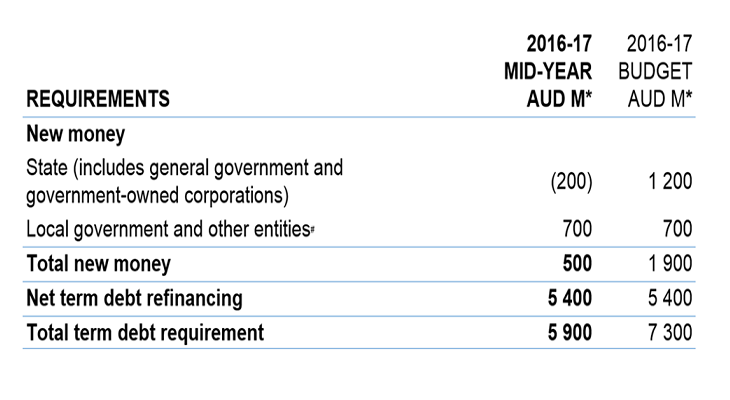

Following the release of the Queensland Mid-Year Fiscal and Economic Review, the Queensland Government has published its amended funding programme for the year to June 2017. It was previously expecting to require $7.3 billion to cover maturing bonds and government spending but the figure has been revised down to $5.9 billion on the back of higher royalties from coal mining. Other estimates remained the same.

So far this financial year, Queensland Treasury Corporation (QTC) has raised $4.1 billion, which leaves around $1.8 billion of additional financing to be raised in the next six months. In this latest statement, QTC said it aims to “smooth and extend” its maturity profile while maintaining at least $5 billion of short-term debt securities on issue.

*Numbers are rounded to the nearest $100 million. source: QTC

*Numbers are rounded to the nearest $100 million. source: QTC

#Retail water entities, universities, grammar schools and water boards.

Click here for the full Mid-Year Fiscal and Economic Review document.

14 December 2016

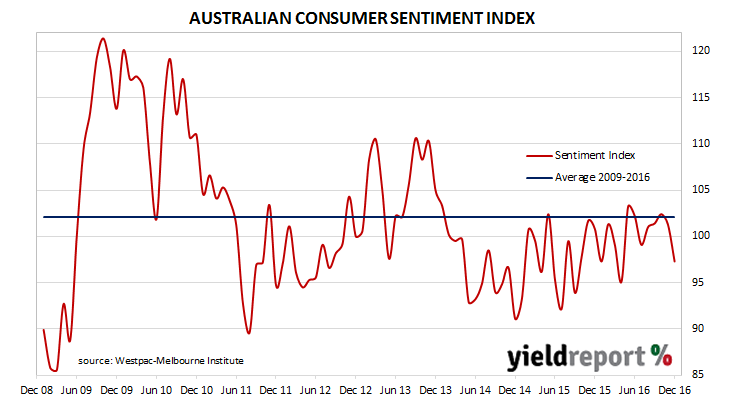

Consumers seem to have taken the latest negative GDP figures to heart. According to the latest survey of consumer sentiment, Australians are generally more pessimistic than they were a month ago. The December Westpac-Melbourne Institute consumer sentiment index fell for the second month in a row from November’s reading of 101.3 to a reading of 97.3. Any reading below 100 indicates the number of consumers who are pessimistic is more than the number of consumers who are optimistic.

Financial markets largely ignored the results in the lead up to the US Fed’s interest rate decision. By the close of business, 3 year and 10 year bond yields were both down 3bps to 1.93% and 2.83% respectively while the AUD was a little lower at just under 75 US cents during afternoon trading.

13 December 2016

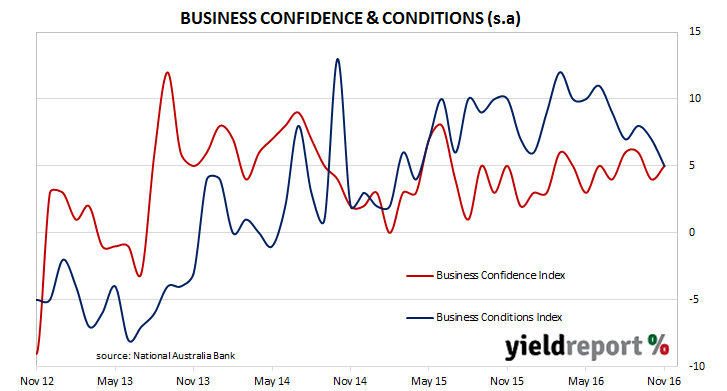

Australian businesses are apparently more confident about the future although they are less happy about the current trading environment. According to NAB’s latest monthly business survey of over 510 firms across the non-farm business sector in the last week of November, the Business Confidence Index rose 1 points to 5 while the Business Conditions Index fell back 2 points to 5 from its revised October value of 7. To put this in a longer-term context, the average for business confidence is 5 while the average for business conditions is 6.

On the day, reactions in financial markets indicated the figures were interpreted as vaguely negative for the economy. Although probabilities of RBA rate changes barely changed in the cash markets, bond yields fell with both 3 year and 10 year bond yields falling 3bps to 1.94% and 2.80% respectively.

Andrew Hanlan, senior economist at Westpac said, “The Australian economy clearly lost momentum in 2016, with official data reporting that output contracted in the September quarter. A key question, are conditions beginning to recover from this soft patch, boosted by recent RBA rate cuts and post the Federal election? On this, there are mixed signals. The NAB survey reports conditions continue to moderate. The AiG surveys reveal a rebound across the three months to November, up from the low of August, consistent with official retail sales.”