08 December 2016

After three consecutive quarters of 3% plus GDP figures, Australia’s economy has gone into reverse. The economy shrank by -0.5% over the September quarter, a figure which was much lower than the median forecast of 0.2%. On a year-on-year basis, GDP growth was 1.8% which was also much lower than the 2.5% median forecast.

In previous quarters the public sector at the state and local government levels had added significantly to GDP growth. In this quarter, public sector investment decreased by 10.4%, which had the effect of lowering GDP growth by 0.5%.

Given the shock number, it was surprising financial markets did not react more. Currency markets sent the AUD 0.3 US cents lower and bond yields dropped on the news but by the end of the day 3 year bond yields were 5bps lower at 1.91% and 10 year yields were 3bps lower at 2.765%. However, after a closer inspection of the numbers, economists came to the same conclusion as the RBA and viewed the contraction as temporary.

Australia is still within reach of the record for longest number of quarters without a recession. In economics, a recession is commonly defined as two quarters in a row of negative GDP growth. At 103 quarters, the Netherlands has the longest non-recessionary period since records were kept. If Australia goes back into positive territory in the December quarter, only one more quarter of positive growth will be needed to equal this record.

06 December 2016

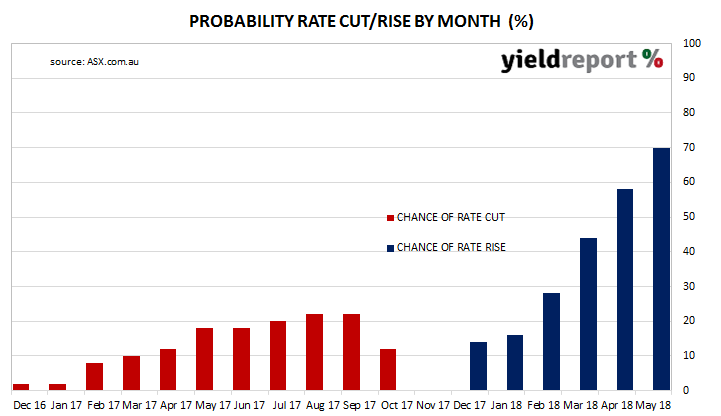

In a decision which most economists expected, the RBA has held the official cash rate steady at 1.50%. Reactions in bond and currency markets were subdued. The AUD fell roughly 0.1 US cents on the day, while the 3 year bond yield rose 1bps to 1.96% and the 10 year bond yield rose from 2.76% to 2.79%. Futures prices in the cash market reacted in a way which implied investors thought the chances of a rate cut through to November 2017 had increased while the chances of a rate rise from December 2017 onwards had fallen.

The RBA can change the official rate on any day but traditionally it will only do so at its monthly meeting unless the circumstances are extraordinary. However, meetings held in the months of February, May, August and November are favoured as they come just after the release of quarterly CPI figures. There is no January meeting and so the focus of economists will turn to February’s meeting as the next possible time when the RBA will seriously consider a rate change.

05 December 2016

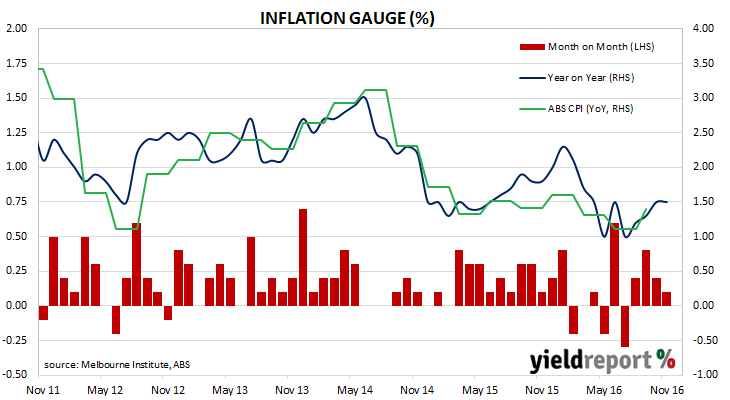

The Melbourne Institute Inflation Gauge rose again during November for the fourth month in a row.

This latest reading indicates consumer prices rose by 0.1% for the month and 1.5% year on year. October’s comparable figures were 0.2% and 1.5% respectively.

3 year and 10 year bond yields both finished lower on the day. 3 year yields fell 4bps to 1.95% while 10 year yields fell 7bps to 2.76%. It is worth noting ANZ Job Advertisements were also released on the same day so to suggest the Inflation Gauge numbers were responsible for sending yields lower is debatable.

Last month we wrote how October’s robust number was some way from marking the end of inflation’s downtrend. November’s soft numbers are a reminder of why calling an end to a trend is a perilous venture.

05 December 2016

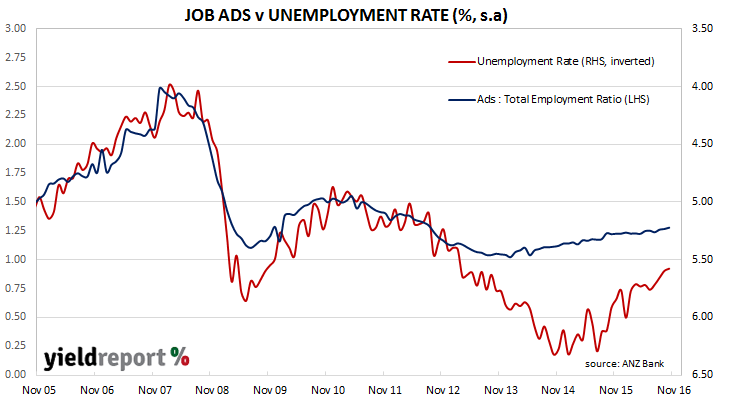

Australian employment conditions remain “quite encouraging” according to ANZ’s latest survey of job advertisements. Total job advertisements rose 1.7% in November (in seasonally–adjusted terms) after a 1.0% rise in October, according to ANZ’s monthly job advertisements survey. The year-to-November figure was also higher at 6.1%, up from October’s comparable figure of 5.2%.

3 year and 10 year bond yields both finished lower on the day. 3 year yields fell 4bps to 1.95% while 10 year yields fell 7bps to 2.76%. The Melbourne Institute’s Inflation Gauge for November was also released at the same time so it is debatable as to the influence each report had on yields. The AUD was slightly higher on the day, which indicates the forex market thinks there is an increased probability of higher future interest rates.

02 December 2016

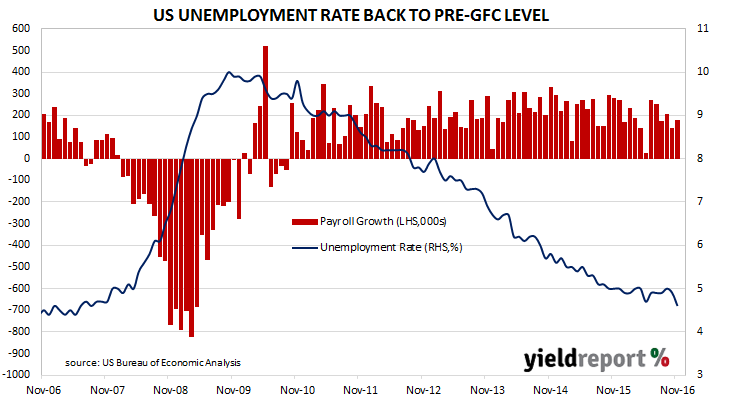

The US unemployment rate is back to pre-GFC levels after the US created another 178,000 jobs and the participation rate fell. According to the US Bureau of Labor Statistics, the US unemployment rate fell from 4.9% to 4.6% as the number of jobs created in November was broadly in line with market expectations of 180,000, while the participation rate fell to 62.7%. US 10 year bond yields fell on the day and were down 6bps from 2.45% to 2.39%.

Average hourly earnings were lower than in October but they were still 2.5% higher than at the same time a year ago. NAB said the “0.1% fall in average hourly earnings…trumped the drop in the unemployment rate to a new post GFC low of 4.6%…” Westpac took a similar view. “The main surprise, however, was the fall in average hourly earnings of -0.1%, well below expectations at 0.2%…The annual rate is now at 2.5% vs 2.8% last month, leaving the overall trend for much of the year largely sideways. There is no change to expectations of a rate hike next week.”

01 December 2016

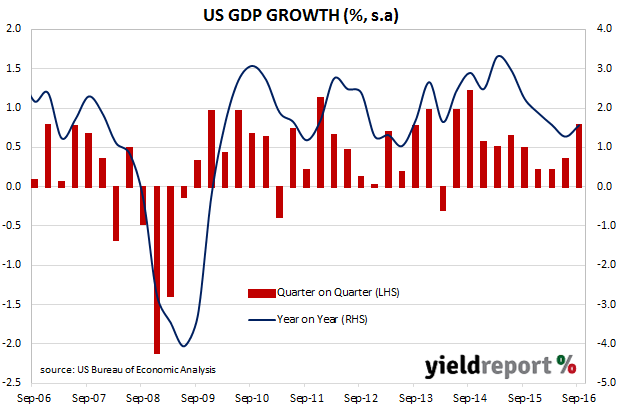

US economic growth in the third quarter seems to have been better than first thought. According to US Bureau of Economic Analysis “second estimate” figures released this week, Q3 GDP growth was 3.2% annualised, up from the advance estimate of 2.9%. The higher number was the result of higher consumer spending and higher investment in housing and lower business investment. The latest estimate is also well up on the second quarter comparable figure of 1.4% and therefore it is likely to cement the market’s expectation of a 25bps rate rise at the next US Fed meeting in early December.

NAB interpreted the figures as suggesting US consumers remain untroubled. Consumption accounts for roughly two thirds of GDP in advanced economies and thus it is the major determinant of economic growth.

24 November 2016

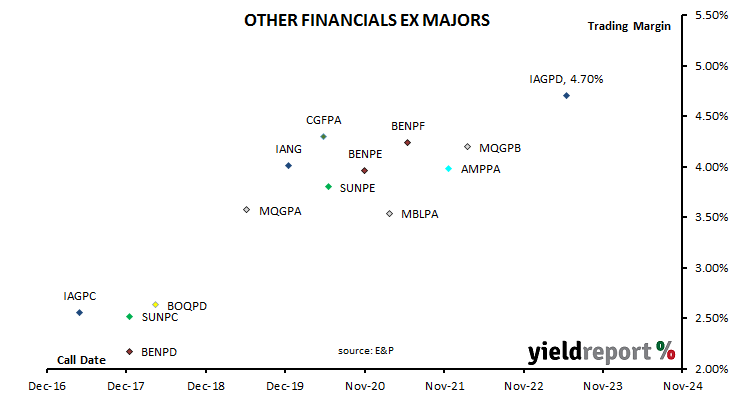

IAG has announced the margin on its latest IAG Capital Notes (ASX code: IAGPD) offering and, as is the fashion in recent years, it was at the bottom of the 4.70%-4.90% range. Added to the current 3 month bank bill swap rate (BBSW) of 1.75% and inclusive of franking credits, investors can expect around 6.45% annualised for the first quarter and thereafter if BBSW rates do not alter materially. (BBSW is largely close to the RBA’s official cash rate.)

24 November 2016

After several false starts, it looks as if the US will finally have a rate rise this year. Now the presidential election is out of the way, the US Fed can act without being accused of interfering with the political process. The minutes of the US Fed’s November meeting all but confirmed a rate rise of the next meeting, stating that a rate rise should come “relatively soon”.

According to the minutes, the argument for raising the official rate “had continued to strengthen”, which is a continuation from September’s theme where the case for a rate rise had “strengthened”. From that point, markets began to gradually ratchet up the probability of a rise and currently the probability implied by futures contracts is pretty much a certainty. Commonwealth Bank said, “December looks to be a done deal”. What’s more, additional rises through 2017 are also more likely. According to ANZ, “A December hike is already priced at 100% odds, but markets are now putting decent odds on a follow-up move by June.”

23 November 2016

Three years after Australia Post last issued bonds into the Australian market, it has returned with a $200 million deal comprising two $100 million tranches. The deal was similar to the two-tranche structure used in 2013 and in that deal, Australia Post issued a $175 million worth of 10 year bonds and a $250 million worth of 7 year bonds, both with fixed-rate coupons. This time around there was also a 10 year tranche but the other tranche was for 5 years and its coupons are floating instead of fixed.

The 10 year tranche was priced at Swap + 130bps, 15bps higher than pricing on the 10 year tranche in 2013 while the 5 year floating rate tranche was sold at 3m BBSW + 105bps. The bonds were issued by Australian Postal Corporation, which is rated AA- by S&P Global Ratings and they are one of the few AA-rated issuers in Australia which is not a major bank. NAB and ANZ acted as Joint Lead Managers to the transaction.

18 November 2016

Another South American supranational has joined the Kangaroo market and completed its debut deal. The Central American Bank for Economic Integration (CABEI) has become the second supranational issuer from South America to issue AUD-denominated bonds into the local market. CABEI lends money to both the public and private sectors of Central American countries, with the spilt being around 70/30.

It joins Corporación Andina de Fomento (CAF) as the only other South American issuer in the Kangaroo market. CAF was last active in the local market in April of this year when it issued 10 year bonds at ACGB +180bps. The pricing of CABEI’s deal is not all that different, despite a difference in credit ratings. CABEI is rated A by S&P Global and /A1 by Moody’s, whereas CAF is rated AA-/Aa3. CABEI issued its November 2026s at ACGB + 188bps, which is close to the price CAF achieved for its April transaction. The explanation is in the tightening of spreads which occurred as investors have traded higher credit ratings for higher yields. As bond yields moved lower and lower, some investors have moved funds away from their traditional areas of interest, for instance AA rated borrowers, to issuers with lower credit ratings, thereby creating pressure for a narrowing of the gap between issuers with different ratings.