17 November 2016

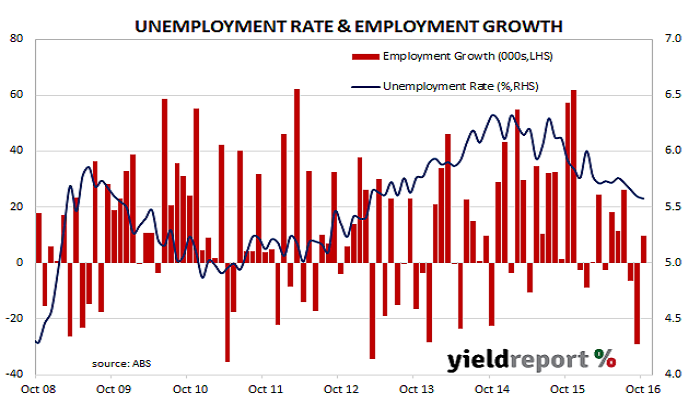

The loss of full time jobs in Australia came to a halt in October but, unlike recent ABS labour reports in 2016, doubts over its veracity were largely absent. The ABS released October employment estimates which indicated Australia’s unemployment rate remained steady at 5.6%. The total number of people employed in Australia in either full-time or part-time work rose by 9,800 during the month, in contrast with the market’s expectation of +20,000. The participation rate also fell again, this time from 64.5% to 64.4%, largely driven by males leaving the workforce.

While AMP Capital’s Shane Oliver referred to October’s report as being “messy” it was not because of ABS sampling processes. The ABS was at pains to point out how the estimation process was affected in September by an incoming group in Queensland, stating its influence had “been temporarily reduced as part of the estimation process.” One month later, this adjustment has now been reversed because the new group’s characteristics have been stable from month to month. “The ABS has therefore reversed the treatment applied in September, with the rotation group being given its full influence on September estimates.” The adjustment led to revisions in September’s data which meant full-time job losses were larger than reported at the time.

17 November 2016

The yield on Origin Energy Notes (ASX code: ORGHA) has fluctuated wildly over the past year in response to the state of its balance sheet and/or their expected redemption date. The notes have a call date in December 2016 but their final maturity date is in 2071. It is understandable for the price and yield to move considerably when investor sentiment shifted from expecting a redemption in 2016 to some undetermined date or vice versa.

Origin has given strong hints as to its intention to redeem its notes for some time. As far back as September 2015 when Origin had an equity raising, Origin investor presentations assumed the Notes would be redemed on the first call date in December 2016. However, without an official announcement, investors have factored in some probability of a change in conditions and as a consequence, a delayed redemption.

Finally Origin has confirmed it will redeem the notes this year. In a notice to the ASX, it said “it intends redeem, in whole, all of the Origin Energy Subordinated Notes” on 22 December, 2016. Holders who are on the register on 16 December will receive $100 plus $1.43 interest.

The notes’ yield fell immediately on the news as the price jumped above their $100 face value. At the closing price of $100.75, Evans and Partners calculate the yield to maturity is just short of 7% (annualised).

Trading is expected to cease on 13 December.

16 November 2016

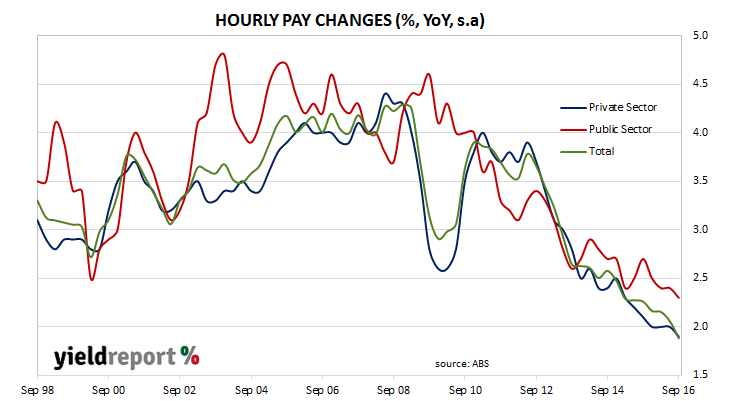

Australian wage growth created a new record and it’s not the sort of record employees wish to see. If inflation did pick up in Australia, it seems unlikely employee costs would be behind it as wages growth set a new record low in the September quarter. Although the series has only be around since 1997 it is still the lowest in twenty years.

Wages grew by 0.4% in the September quarter, which is the same as the June quarter’s figure. However, year on year growth fell to 1.9%, down from 2.0%, and if quarterly growth figures continue at the current pace, annual figures will fall further. Markets largely took the figures for granted and in any case, they are being driven by offshore bond markets where the Trump factor still features prominently. The yield implied by 10 year bond futures fell from 2.63% to 2.61% while the yield on 3 year bonds fell a similar amount to 1.81%.

Falling wages inflation in Australia is being driven predominately by the private sector. Westpac’s Justin Smirk said, “Low and stable private sector wage inflation has been the dominant domestic underlying inflation story for a number of years now.” Private sector wages grew by 0.4% in September or 1.9% year on year while the public sector continued to be a more rewarding place for employees and, in that part of the labour market, wages grew by 0.6% or 2.3% for the year.

10 November 2016

In a move which was widely anticipated New Zealand’s central bank has announced a 25bps reduction to 1.75% three months after a 25 bps reduction in August. Westpac’s Imre Speizer said the statement accompanying the decision indicated a shift from an easing bias to a neutral one. He also noted the market’s response “was moderately hawkish.”

Governor Graeme Wheeler cited price falls in the tradables sector which have flowed from a strong exchange rate. Tradables are goods and services which can be imported or exported and therefore are subject to both foreign and domestic competitive pressures. “The exchange rate remains higher than is sustainable for balanced economic growth and, together with low global inflation, continues to generate negative inflation in the tradables sector.” The RBNZ is quite blunt about its hope for the New Zealand currency, stating, “A decline in the exchange rate is needed.” This is not the first time the Bank has engaged in the dark central bank art of jawboning. This latest reference to the exchange rate is an exact repeat of the phrase used in the statement accompanying the August rate reduction.

The Bank also was not shy is pin-pointing a source of future systemic shocks. “House price inflation remains excessive and is posing concerns for financial stability. Although house price inflation has moderated in Auckland, it is uncertain whether this will be sustained given the continuing imbalance between supply and demand.” In light of these concerns, another rate reduction is somewhat of a mystery.

For the full statement click here.

09 November 2016

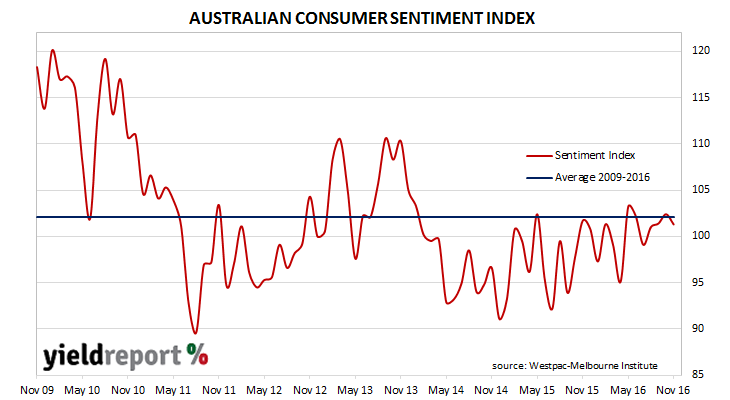

Consumer confidence has remained largely stable through October and optimists still slightly outweighing pessimists, according to the latest consumer survey. The November Westpac-Melbourne Institute consumer sentiment index fell from October’s reading of 102.4 to 101.3 which is roughly the same as the September figure. Any reading above 100 indicates the number of consumers who are optimistic is more than the number of consumers who are pessimistic.

08 November 2016

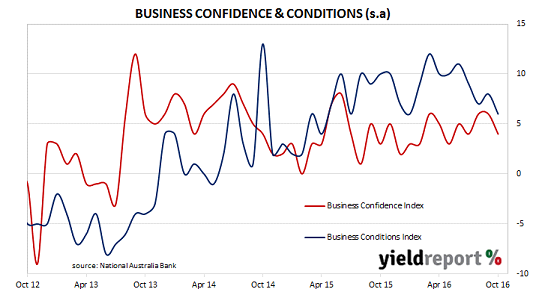

Australian businesses sentiment dropped down a notch in October and it is now at below-average levels. According to NAB’s latest monthly business survey of 400 firms across the non-farm business sector in the last week of October, the Business Confidence Index fell 2 points to 4 while the Business Conditions Index also fell back 2 points to 6.

Bond market yields were essentially unchanged and the local currency was slightly firmer against the USD, although domestic economic data was taking a back seat to speculation regarding the US presidential election on that night.

Westpac’s chief economist, Bill Evans, thought the data suggested Australia’s economy has just finished passing through a tough patch mid-year. “We interpret the current weakness in business conditions as suggesting that the Australian economy hit a soft-spot around mid-2016. Jobs growth has slowed after overshooting in 2015, the housing sector had cooled in the wake of tighter lending conditions and real retail sales fell by 0.1% in Q3.”

Leading indicators such as forward orders and capacity utilisation also fell. NAB described these falls as worthy of “close monitoring” but they are not yet significant enough to change NAB’s outlook unless they continued in coming months. “…if the recent trends were to continue, it would be unsettling and imply that the non-mining recovery has started to run out of steam earlier than expected.” Bill Evans was more positive in his short term view for the Australian economy. “At this stage, we expect conditions to regain momentum as we move into 2017. Also, some of the uncertainty around public policy has eased with the Federal election behind us. A risk to this view is that weakness in employment is more enduring than we expect, with flow-on effects to consumer spending.”

NAB’s chief economist Alan Oster partly agrees with his Westpac counterpart about 2017. “For now though, we would only be looking to slightly lower 2017 forecasts and remain reasonably comfortable with the near-term outlook – which is expected to be supported by commodity exports and the housing construction cycle.” However, he expects interest rate cuts as Australia’s economy slows in 2018. “Beyond the near-term, impetus from those growth drivers will fade which will see the economy slow into 2018…Two more 25bp rate cuts are still expected from the RBA next year in response to ongoing low inflation and a more subdued growth outlook.”

07 November 2016

Unemployment in the US fell to 4.9% in October as the number of people in employment increased and despite a rise in the participation rate. According to the US Bureau of Labor Statistics, 161,000 new jobs were created, less than the 173,000 expected. However, it was the 2.8% rise in average hourly earnings which attracted attention, as it is the highest annual rate since 2009. US 10 year bonds fell from 1.81% to 1.76% on the day but the move was probably more a reflection of Donald Trump’s likely chance of winning the presidential election in light of FBI investigation of Hillary Clinton.

07 November 2016

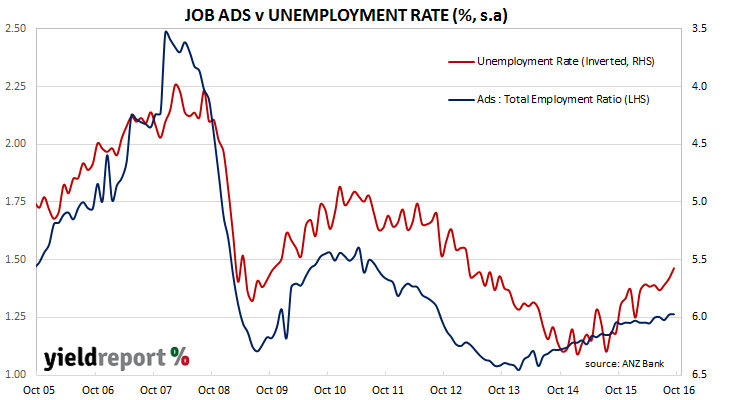

Total job advertisements rose in October (in seasonally–adjusted terms) after a fall in September, according to ANZ’s monthly job advertisements survey. The month-on-month figure rose by 1.0%, while the year to September figure increased to 5.2%, up from August’s comparable figure of 3.6%.

Domestic bond markets largely ignored the results as offshore bond market yields spiked on news of Hilary Clinton’s clearance by the FBI. The 3 year bond yield increased by 1bp to 1.69% while the 10 year bond yield moved up 2bps to 2.32% on the day. The AUD was up about half a US cent on the day, which is an indication the forex market thinks there is an increased probability of higher future interest rates.

ANZ’s Head of Australian Economics, Felicity Emmett expects employment numbers to increase and for economic conditions in general to remain robust. “The rise in ANZ job ads is encouraging and points to ongoing improvement in labour market conditions. It is consistent with the moderate pace of economic growth, as well as above average business and consumer sentiment.”

Labour force figures for October have not yet been released and thus the job advertisements to total employment ratio is not known. The chart below shows the inverse relationship between this ratio and the unemployment rate. As the ratio rises (more advertisements per potential employee) the unemployment rate falls. However, the rate of advertisements per potential employee is still far from pre-GFC levels.

01 November 2016

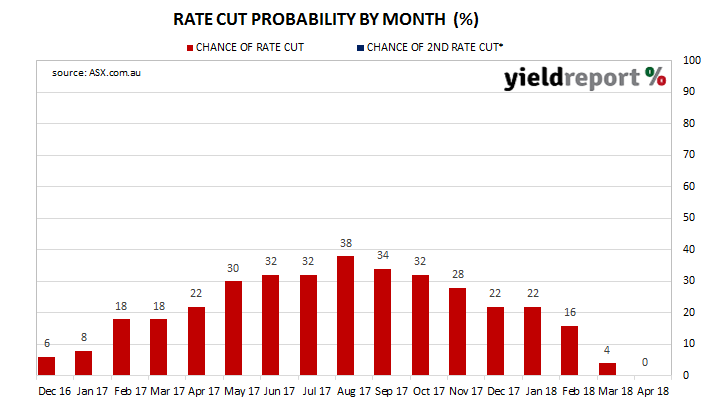

Although some economists thought November’s RBA meeting was “live”, most pundits gave little weight to such an outcome. Just as well, because the RBA announced this week it had chosen to keep the cash rate at 1.50%.

Reactions in bond and currency markets were subdued but both hinted of an expectation by participants of higher rates in the future. The AUD rose 0.4 US cents on the day and the 10 year bond rate implied by futures contracts rose from 2.325% to 2.360%.

Westpac chief economist Bill Evans said the statement accompanying the decision confirmed his view Australia’s inflation outlook “is unlikely to be the source of any future policy adjustment.” That is, unless inflation is unexpectedly and abnormally low, the RBA will not cut rates again in this cycle on the basis of inflation figures. Then again, he is not totally against the possibility of a rate cut. “However, with inflation only likely to track along the bottom of the 2-3% target band next year there will be scope to ease further should growth, and the labour market in particular, profoundly disappoint.” He also concedes if there were any movement from the RBA next year, “it will be down rather than up in 2017.”

Close of business, 1 November 2016

The focus now moves to February’s meeting, which is the next meeting after December quarter statistics such as CPI and employment figures are released. One of the interesting developments since October’s meeting has been the ratcheting back of expectations for a rate cut as implied by cash contracts. At the end of Melbourne Cup Day, not only were contracts implying buyers and sellers placed less than a 50% chance of a rate cut in 2017, they are close to implying a rate rise in 2018. Not yet, however, and as we have seen over the last twelve months, expectations can change rapidly.

31 October 2016

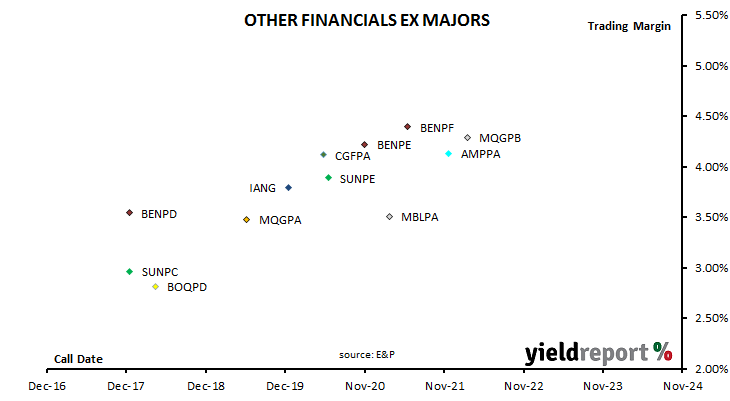

Bell Potter, in a note to clients has recommended Insurance Australia Reset Exchangeable Securities. These securities, which were actually originally issued by IAG’s New Zealand subsidiary, were originally issued in pre-GFC days, before the days of Basel rules, non-viability clauses and capital trigger events. Bell Potter thinks “one key advantage of IANG relates to it being an old style preference share…” but as always the main attraction is the near 400bps trading margin in conjunction with the December 2019 reset date, when holders can “request” redemption.

The use of the term “request” sounds as if the company has some wriggle room to deny a holders redemption instructions but in reality it is a lot more prescriptive. According to the 2004 prospectus, requesting redemption does not necessary mean redemption will occur. However, when a holder requests redemption the issuer must “redeem the RES for a cash amount equal to the redemption amount…convert the RES into a number of ordinary shares calculated according to the conversion number with a value equivalent to the redemption amount…or sell your RES to a third party on your behalf for the issue price ($100) plus any accrued interest payments, and deliver to you the cash proceeds…” in each case the holder will be delivered the face value or shares equivalent to the face value which can be quickly sold to produce cash.